Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

How I Failed to Become a Bitcoin Millionaire

December 18, 2017 This past Fall, an industry colleague congratulated me on my newfound wealth. “What newfound wealth?” I reply. “What are you talking about?”

This past Fall, an industry colleague congratulated me on my newfound wealth. “What newfound wealth?” I reply. “What are you talking about?”

“Aren’t you a bitcoin millionaire now?” he says, smiling brightly, with a look in my direction that suggests he can see through my deceptively coy demeanor. “You were talking about it for years. You were right about it!”

“Oh, yeah… Bitcoin,” I say back while looking at the ground, embarrassed by what I am about to tell him. “I spent nearly all my Bitcoins well before the price jump,” I reveal.

He didn’t believe me, but it didn’t matter. I had no regrets up until that moment when I decided to look back and see how much my Bitcoins would’ve been worth had I just held on to them. Doing the math ultimately turned out to be a bad idea.

$500,000.

That’s the rise in value I missed out on by spending the Bitcoins I had been acquiring in 2014-2016. It’s not a million dollars, but it’s enough to sit back and think, what if. [Editor’s note. The market value of those Bitcoins since the time this issue went to print reached about a million dollars after all. DAMN.]

Bummer

But why spend or sell them if I was a supposed true believer? I never cared much for speculating. I liked and still like Bitcoin because it’s a payment methodology that exists outside the purview and control of banks and government. It is the ultimate way to de-bank. And hey, that’s what all the fuss of this publication is about.

I started reporting on Bitcoin here in deBanked as early as 2014, mainly to an audience that didn’t know what they were and didn’t care to know. I couldn’t blame you all. Talk of digital currency, mining, and block sizes doesn’t exactly go hand-in-hand with things like online lending, merchant cash advance, and brokering deals.

A handful of diehard Bitcoin fans at the time told me they were happy to see Bitcoin legitimized through our coverage. Others told me it was complete garbage, a ponzi scheme even, that didn’t deserve any attention whatsoever.

In those days, I took a tour through the whole ecosystem by mining Bitcoin, buying it, selling it, paying people with it, and accepting payment with it. I read books about it, attended seminars on it, and watched documentaries about it. I even experimented with turning my computer into a node in the Bitcoin network to keep the ecosystem itself running smooth. I repeatedly heard critics argue that it was all a scam and I walked away every time remaining unconvinced.

Bitcoin allows users to carry their money across borders without hassle and to retain possession of their funds even if a bank or government agency wants to seize it. Perhaps these benefits appeal to criminals, but surely they also do to law-abiding citizens.

I didn’t like the volatility of it so much back when I was acquiring them. It wasn’t a very good store of value and it still isn’t. The fact that a Bitcoin I acquired for $300 is now worth $10,000 [market value at the time it went to print] is amusing but also terribly unnerving. What good is Bitcoin to legitimately use as money if the value can swing massively in an hour? And what to do if I bought 1 Bitcoin now at $10,000 and it retreated back to $300?

In a way, I may have been more excited to have held all those Bitcoins for another year without them experiencing any increase in value, rather than to have accidentally profited handsomely thanks to speculators who do not care about the underlying utility of Bitcoin.

Maybe I’m an idealist. Or maybe I’m just rationalizing why I shouldn’t cry myself to sleep over having missed out on 500k in profit. I personally believe Bitcoin will be at its most valuable when its price is stable. If we can get to that point and the world economy becomes more accepting of it as a form of payment, well then I’d be very interested in holding on to Bitcoin indeed.

I wondered, of course, if the me of three years ago would’ve agreed with my philosophy now. A blog post I wrote in November 2014 answers that question.

Below are some of the points I made then:

“Bitcoin is more than a currency. It’s not the Euro, the Yen, or the Peso. It’s a detachment from governments and banking. It’s self-control. Without the private key, your bitcoins can’t be seized.”

“I’m not necessarily speculating though. I spent almost half my bitcoins shopping on Overstock on Black Friday.”

“A 5% swing might be acceptable for an investment but it’s quite ugly for a currency.”

“Your money is not really yours. You have rights to it, but only to an extent. It can be garnished, frozen or confiscated. That’s the price of liquidity and relative stability. If you can afford to color outside the lines, where you can remove [bankers] and their control, why not experiment? There’s something pure about [Bitcoin], liberating. And when you add in the fact that it’s governed by math, it’s more than that, it’s beautiful.”

“There are indeed those holding [Bitcoin] and not spending. Rampant speculation is both a cause of volatility and an argument for its long term unsustainability. Speculators are hoping the digital currency will appreciate and make them filthy rich. If that day never comes, a big sell off will cause its value to drop.”

And so it was in 2014, I was interested in the utility of Bitcoin while concerned about the volatility of it. The value has since shot up to the moon, largely due to speculation. Along the way my views caused me to miss out on becoming a Bitcoin millionaire.

And I couldn’t care less. Wake me up when the price stabilizes.

Editor’s Note: Between the time this story was sent off to print and now (when it’s being published online), the market value of those Bitcoins had increased from $500,000 to nearly $1 million. Incredibly, I legitimately would’ve been a Bitcoin millionaire.

Editor’s Note 2: It’s been a long time since I have played around with being a Bitcoin node. More recently, I have become a node on Ethereum, a blockchain for decentralized applications that also serves as the backbone platform for things like Initial Coin Offerings.

deBanked Connect: Miami — SOLD OUT

December 12, 2017deBanked’s cocktail networking event on January 25th in South Beach is now SOLD OUT!

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

With 20 sponsors already signed on, Broker Fair is sizing up to be the biggest event in the MCA and small business lending industry of the entire year! During this exclusive full-day conference, brokers, lenders, funders and service providers alike can expect education, inspiration and opportunities to connect and grow their business. You can view our preliminary agenda here.

DON’T GET LEFT OUT. REGISTER FOR BROKER FAIR 2018 TODAY!. Got questions? E-mail: info@brokerfair.org

Originations Since Inception

December 8, 2017After several company announcements recently, we’ve compiled a milestone chart to plot where they rank. Originations may indicate business loans or MCAs funded on balance sheet, brokered, or placed through a marketplace. These rankings are a work in progress. This chart may not include companies for which public data is not available. If you’d like your figures to be listed here, e-mail sean@debanked.com.

| Company | Origination Volume Since Inception | Year Founded |

| OnDeck | $8 Billion | 2007 |

| Kabbage | $4 Billion | 2009 |

| Yellowstone Capital | $2 Billion | 2009 |

| BFS Capital | $1.7 Billion | 2002 |

| Funding Circle | $1 Billion (US only) | 2010 |

| IOU Financial | $500 Million | |

| Lending Club | $500 Million (SMB loans only) | 2006 |

| SmartBiz Loans | > $500 Million (SBA loans) | 2009 |

| Lendio | > $500 Milllion | |

| Forward Financing | $275 Million | 2012 |

| Blue Bridge Financial | $200 Million | 2009 |

Law Firm or Law Fail? Debt Settlement Company’s Legal Footing Called into Question

December 6, 2017The first major volley in the lawsuit filed by plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) against a debt settlement company and their alleged ISO partners has been exchanged. And it’s a doozy.

Three of the eight defendants, Mark D. Guidubaldi & Associates, LLC (d/b/a Protection Legal Group) aka PLG, Corporate Bailout, LLC, and PLG Servicing, LLC have sought to collectively dismiss the complaint on the grounds that they are attorneys “engaged in the practice of law with the Merchants as their clients.”

PLG, a self-described “multi-jurisdictional law firm that practices law in various jurisdictions nationwide,” argues in their motion papers that those employed by Corporate Bailout and PLG Servicing carry out certain administrative and support tasks for PLG. And it’s okay that no one at either of those companies are attorneys, they claim, because PLG supervises it all. That enables them to be covered as attorneys in an attorney-client relationship, they assert.

If true, they might want to try harder at supervising. As you might remember, Corporate Bailout, a telemarketing debt settlement firm, was featured on the cover of the New York Post earlier this year after being sued for running an operation “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street.’”

If true, they might want to try harder at supervising. As you might remember, Corporate Bailout, a telemarketing debt settlement firm, was featured on the cover of the New York Post earlier this year after being sued for running an operation “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street.’”

Corporate Bailout’s principal office is in New Jersey. PLG, the law firm, is based in Illinois. Can it really be that the former is considered a law firm through a relationship with the latter?

Whoa, not so fast, says an amended complaint filed by the plaintiffs on Tuesday, which argues that not even PLG is a legitimate law firm. “In fact, none of the Debt Relief Defendants is a law firm engaged in the provision of legitimate legal service,” they contend. “PLG is not even registered as a law firm in Illinois, as required by the rules of the Illinois courts,” they add.

If true, then this case could potentially have far-reaching consequences beyond simple tortious interference.

Some excerpts from this bombshell allegation:

PLG has one employee who is a lawyer, but does not as a rule advise or represent its customers. The advice those merchant customers receive is given by non-lawyers at Corporate Bailout and PLG Servicing, who approach and recruit merchants in ways no lawyer subject to the Rule of Professional Conduct 7.3 would ever be permitted to solicit clients. The non-lawyer personnel at Corporate Bailout and PLG Servicing are not supervised by the solitary lawyer at PLG, but by [Mark] Mancino and [Michael] Hamill, who are not lawyers – an arrangement that, if PLG were a law firm engaged in the provision of legitimate legal services, would violate Rule of Professional Conduct 5.3. To the extent that any of the advice the non-lawyers at Corporate Bailout and PLG Servicing give to merchants in furtherance of the Debt Relief Defendants’ tortious activity is legal advice at all, giving it violates the prohibition on the unauthorized practice of law. PLG orchestrates this activity, which damages the merchants as well as their Merchant Cash Advance Providers, in flagrant and deliberate disregard of the law.

[…]

Although the merchants are told that they are paying the funds into an “escrow account,” in reality PLG does not treat the funds like client escrow funds; it pays itself from them from the beginning, regardless of whether it is providing any services, and with no differentiation between client funds and funds payable to PLG. If PLG really were a law firm engaged in the provision of legitimate legal services, its practices with respect to client funds would be barred by the Rule of Professional Conduct 1.15.

– plaintiffs in the Amended Complaint (<-- click to download a copy)

Plaintiffs have also added Michael Hamill as an individual defendant. Fellow co-defendants Mark Mancino, American Funding Group, Coast to Coast Funding, LLC, ROC Funding Group, LLC, and ROC South, LLC did not file a response to the original complaint.

Are Lawsuits the New UCCs?

December 5, 2017 Back when merchant cash advance funders first began to file UCCs, competitors immediately began to look them up and turn them into leads. The practice became so widespread that MCA funders began filing under pseudonyms to throw people off the scent. But soon, competitors began to figure out who the pseudonyms belonged to and the game continued. Funders tried other methods like having the UCC service providers themselves be named as the secured parties. Eventually, competitors realized that although they couldn’t figure out who the true secured party was on these, they could at least reasonably identify the named debtor as having obtained funding. Eventually some funders gave up and stopped filing UCCs altogether.

Back when merchant cash advance funders first began to file UCCs, competitors immediately began to look them up and turn them into leads. The practice became so widespread that MCA funders began filing under pseudonyms to throw people off the scent. But soon, competitors began to figure out who the pseudonyms belonged to and the game continued. Funders tried other methods like having the UCC service providers themselves be named as the secured parties. Eventually, competitors realized that although they couldn’t figure out who the true secured party was on these, they could at least reasonably identify the named debtor as having obtained funding. Eventually some funders gave up and stopped filing UCCs altogether.

These days, a new breed of public records detectives are harvesting the NY state court records for lawsuits against merchants in default. Though they don’t always wait until a merchant has already been sued, the public dockets make it easy for them to obtain all the details they need to pitch services such as debt settlement and legal aid.

An unfortunate consequence of that is that these so called advocates may not have the merchants’ interests at heart and they can greatly complicate communication between the parties.

See previous coverage:

- 4th Alleged Co-conspirator in Fake Debt Settlement Company Arrested

- ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

- Is The End Near For This Debt Settlement Firm?

- A Tale of “Debt Restructuring”?

The practice of trolling the dockets is becoming so popular that a similar trend may be cropping up, funders filing lawsuits under obscure entity names. While it’s too early to tell if debt settlement lead hunters could get so aggressive as to actually make it untenable to file a lawsuit or a confession of judgment, it is something to keep an eye on. Unlike a UCC, which may only reveal a description of the secured interest and the merchant’s name, the dockets may reveal the actual contract itself, all of the terms, what platform it was funded on, how much remains outstanding, etc. There’s vastly more than could ever be gleaned from a UCC. The downside, of course, is that it suggests a merchant breached a contract and may not be an ideal candidate for additional funding. But to a debt settlement firm (unsavory or not), that might just be the prospect they’re looking for.

Are lawsuits the new UCCs? Time will tell.

Is Lending Club Misleading New Investors About Past Performance?

December 3, 2017

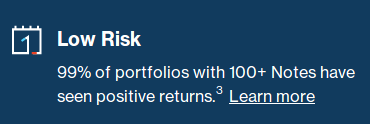

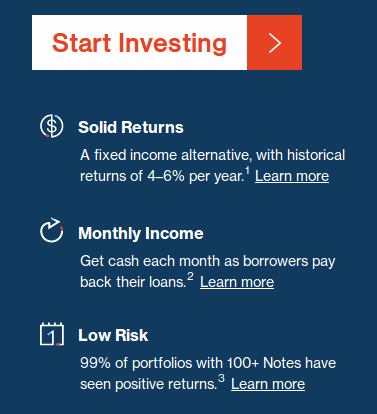

New retail investors interested in the Lending Club platform are greeted with a friendly statistic, that “99% of portfolios with 100+ Notes have seen positive returns.” That’s a slippery statement, which is probably why they footnoted it.

The footnote says that only applies to A through E notes, the only grades of securities that Lending Club is still selling. F and G grades are excluded, presumably because they are no longer for sale as of last month after they noticed “an increase in prepayment and delinquency rate.”

By excluding the notes that significantly underperformed, Lending Club has apparently been able to raise the portfolio performance statistic being marketed to new investors.

On October 28, 2017, for example, Lending Club was reporting that 97% of portfolios with 100+ notes had positive returns. That was representative of all notes. Immediately after announcing that they were discontinuing F and G notes, they raised that number to 99% and added a line about how F and G notes were excluded from past performance.

:::Poof::: And just like that, the bad loans and their drag on returns no longer exist from the history reported to new investors.

The problem with ignoring the letter grades that bamboozled some investors in the past is that Lending Club determines the letter grade of the security, not an independent ratings agency. That means that an F or Grade-grade borrower in October could just be deemed a D or E-grade in December and nobody would be the wiser. Retail investors have no way of knowing because Lending Club’s grading system is proprietary. Go figure.

The problem with ignoring the letter grades that bamboozled some investors in the past is that Lending Club determines the letter grade of the security, not an independent ratings agency. That means that an F or Grade-grade borrower in October could just be deemed a D or E-grade in December and nobody would be the wiser. Retail investors have no way of knowing because Lending Club’s grading system is proprietary. Go figure.

Even if Lending Club did not do that, they’re setting a terrible precedent. If portfolios underperform, again, what’s to prevent them from continuing to make similar inflated claims about returns with a new footnote that excludes D and E notes?

It’s important to bear in mind that Lending Club is in the business of selling securities to unsophisticated retail investors. That 99% of portfolios allegedly yield positive returns is no doubt a major selling point to those worried about the risks of online lending. Why else would Lending Club feel the need to make that a big headline in their marketing?

Online lending is very risky. That’s why in October, the number of portfolios with positive returns wasn’t 99%. Lending Club should not be permitted to sweep past investor losses under the rug.

Bad form Lending Club. Bad form.

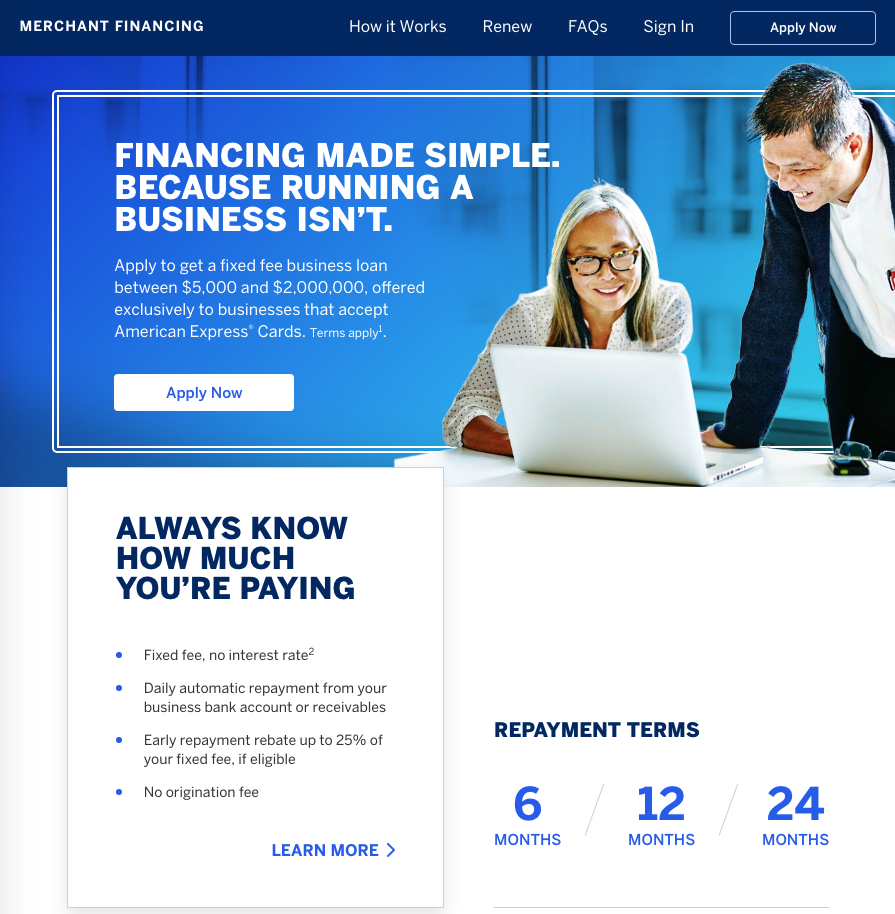

Institutions Like American Express Are Mainstreaming Daily ACH Payments

November 30, 2017A takeover-style ad on CNN’s website rang very familiar earlier today. The ad, paid for by American Express, preached merchant financing with a fixed fee.

The ad brought me to a page that offered a fixed fee business loan between $5,000 and $2 million with daily ACH repayment and no interest rate. Terms were 6 months, 12 months, or 24 months.

While this is more similar to an OnDeck loan, than say perhaps, a merchant cash advance, the concept of fixed fee business financing is becoming a standard even among institutional finance providers.

Square, as I experienced firsthand, is another company mainstreaming the fixed fee model. The difference there is that the payments are monthly rather than daily.

The good news for many online lenders and MCA companies of course, is that merchants that may not qualify with some major financial companies, are at least being introduced to the concept of fixed-fee short-term capital and even daily payments.

SBA Loans Go Online: A Q&A With SmartBiz

November 28, 2017 A while back, a merchant deBanked interviewed told us they had obtained what sounded like impossibly good terms from an online lender not known for low rates. When I requested a fact check of it, we learned that the online lender had actually referred the borrower to SmartBiz and that SmartBiz had secured an SBA loan for them. It was so seamless that the borrower had hardly noticed.

A while back, a merchant deBanked interviewed told us they had obtained what sounded like impossibly good terms from an online lender not known for low rates. When I requested a fact check of it, we learned that the online lender had actually referred the borrower to SmartBiz and that SmartBiz had secured an SBA loan for them. It was so seamless that the borrower had hardly noticed.

Curious, I caught up with Sean O’Malley, president and co-founder of SmartBiz last month at Money2020. Below is a modified excerpt of our conversation:

deBanked: [tells the above story about the merchant who got an SBA loan] – So you actually have other alternative lenders and online lenders going through you too. What is really the biggest channel that you tap into to get small business owners to you? Is it other online lenders or do you go direct to merchants?

O’Malley: Well, there are three different areas where customers come to us. The first is through our marketing efforts. We have our own online presence and marketing initiatives that go on, where small business owners are interested in the SBA loan product. The second area lies in our strategic relationships. These are partnerships with companies like Sam’s Club where we’re actually on their lending center; we have been doing that for a number of years. Another channel would be partnerships with companies like Fundera who bring customers to us through their online channels.

deBanked: How about like Lendio?

O’Malley: Yes. We’ve built a relationship with them over the years. Lastly, the third area is the independent financial consultant channel, like our partnerships with accountants.

deBanked: Okay. Didn’t SmartBiz recently celebrate a major milestone?

O’Malley: Yes! We recently passed the $500 million threshold of originated capital on the platform.

deBanked: All SBA loans?

O’Malley: Correct, all the originated capital is a result from SBA 7(a) loans. Today, we have six bank partners on our platform who are doing SBA loan origination. It’s all been facilitated through our platform. There are really four major components to what we do. The first part is we provide an online presence and origination solution for small businesses. They come through our technology solution and then they go through an application process where we’re able to pre-qualify them. So, that’s the first piece. The second piece is really the technology platform around packaging of the loan.

deBanked: What do you mean by packaging?

O’Malley: After a business pre-qualifies, there are still documents that need to be captured and some of the specific analysis also needs to be done. A large piece of that is automated through our platform. Some of it does require sort of a white glove experience for small business. We provide that as well. Then the third piece is the bank’s underwriting platform, where we digitize the bank’s underwriting and provide them with an underwriting platform that they license from us. Leaving us with the fourth part, the marketplace.

deBanked: Can you explain the fourth piece, marketplace?

O’Malley: The core of what we do is we connect small business owners with banks. And the interesting part of that is that because we’re the marketplace, we’re able to say yes more to the small business than any single bank because they all have their own different credit boxes. In effect, we’re able to get more customers approved because we’re able to fit more use cases for that small business owner. If you combine all these, the ultimate value prop is that we’ve reduced the time to originate a loan. It traditionally takes about 120 days for a bank to originate an SBA loan. We’ve reduced that to as little as seven days. And on the bank side, we’ve reduced their costs up to 90%. As a result, we’ve made these loans more profitable for banks. And they’re then more willing to originate as part of their standard business. Whereas you know, in the small business space, banks have not been super eager to be making smaller sized loans because it costs as much for them to originate that type of loan as it does for them to originate a $5 million loan. So, we’ve made it super efficient.

deBanked: So you’re kind of filtering out applicants on your own that they would normally have to deal with.

O’Malley: That’s right. Our platform allows us to filter out all the applications and only feed a bank the deals that they can do. When we provide a deal to a bank, they’re funding it anywhere between 90-95 percent of the time. They’re funding the deals that come from us because we have the knowledge of how the bank looks at their deals.

deBanked: Is there a world in which you move outside of SBA loans and potentially offer other types of bank loans or maybe even non-bank loans or facilitate them? Not necessarily make them, but facilitate them?

O’Malley: We recently just launched a conventional bank loan. So, yes, we are expanding on our product line, and we did this as a result of really looking at that type of product and filling a gap in the marketplace as well. We’re trying to help the customers out and support their needs.

deBanked: Are you noticing a trend with maybe borrowers applying for loans on like a mobile phone? I mean, any loan is a pretty big commitment, right? They go online and apply for $5,000, you know what I mean, for a personal expense or whatever and that’s not such a huge deal because it’s a small loan. I think an SBA loan is a much bigger commitment, you know, it’s long term. Are you seeing borrowers apply for the loans you offer from a mobile device?

O’Malley: About a quarter of our small businesses start the applications over a mobile device. And they are able to get pre-qualified through a mobile device. That said, the majority of borrowers still want to talk to someone. There are still a lot of traditional relation-based elements to a small business lender. When somebody is taking out a couple hundred thousand dollars, like you said, there needs to be some white glove experience for that. And it can’t just be 100% automated. In fact, small businesses a lot of times don’t want 100% automation.

deBanked: Because it’s such a big commitment.

O’Malley: That’s right. And that’s where the market is today. In the future, we look to certainly automate as much as possible, but we hyper-target where we interact with the customer so that we provide the most unique customer-centric solution so that they feel comfortable about the process. If you look at our TrustPilot customer reviews that we use on our site, you will note that people really speak very highly about their experience. We’re super proud of that because we’ve been able to match up technology with people in the right way so that we can hyper-target where human interaction is needed to make sure that the customer feels at ease with the process. We’ve been able to become the trusted source for them getting the loan that they’re looking for.

deBanked: Do you think in the future borrowers will apply for SBA loans entirely online? Will there be an age where they’re not necessarily going to the bank to meet somebody to talk about an SBA loan? Do you think it’s all going to kind of become like an online digitized process or will it always be a layer of I wanna go and sit and talk with somebody in the bank office?

O’Malley: Well, we’re proving small businesses want to do it primarily online. In fact, you know, the point too is that if you just consider the small dollar amount category, we are now the largest provider of SBA loans in the country for loans under $350,000.

deBanked: Anything else I should know about SmartBiz?

O’Malley: We really seek to be an advocate for small businesses. We have gone beyond SBA in supporting our customers with the more conventional product, but we’re always trying to get businesses into SBA loans because it’s the best product out there. And so, our focus is always first and foremost trying to get our businesses SBA loans if at all possible. And it appears to be working. Recently, we were named as one of the fastest growing companies in the Bay area. We’re looking at certainly scaling this solution with as many small businesses as possible.