Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Gregory J. Nowak, Partner at Troutman Pepper, Has Passed Away

April 13, 2021 Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

The firm’s website introduced Nowak as a veteran attorney that was “sought after for advice on complex securities law matters, particularly on issues arising out of the Investment Company Act of 1940; the Investment Advisers Act of 1940; federal and state securities laws and regulations; broker dealer, FINRA, CFTC and NFA regulatory matters; and corporate and M&A transactions.”

That perfectly sums up the context in which I first encountered Nowak in 2017 when he spoke at a small event put on by the Alternative Finance Bar Association where I was the only non-lawyer in the entire audience. One might expect a presentation on the finer minutiae of securities law of which he gave, to be a mundane, easily forgotten experience for a financial journalist such as myself, but his energetic delivery and fluid command of the subject matter translated complex securities questions into a folksy debate wherein one could feel confident in resolving the Howey Test over the dinner table just as easily as they could in the courtroom.

In fact, I approached him afterwards to thank him on his presentation and even followed up later over email, asking if I might have the honor to list him as a recommended securities attorney on the deBanked website. That was four years ago and as fate would have it, he remained the only recommended attorney that deBanked formally listed under the securities category, despite my coming to know very many accomplished and competent attorneys in the same field of law.

Nowak was one of the earliest public voices in the world of merchant cash advance participations and syndication where the securities question was a consideration some weren’t even sure applied as the industry created new products and investing structures at a furious pace.

He spoke at deBanked’s first major conference in 2018 on the subject of “Syndication and Raising Capital,” and he continued to generate recognition of the need for securities legal support in the burgeoning industry.

He was a co-author of an article published with a colleague at Pepper Hamilton LLP (now Troutman Pepper) that he had given permission to be reprinted on deBanked in December 2018, titled MCA Participations and Securities Law: Recognizing and Managing a Looming Threat. It was read by more than 1,500 people on the deBanked website that first day alone.

Nowak was highly sought out on merchant cash advance issues. “Most judges want to see consistency of treatment and that includes your vocabulary,” Nowak said in an interview with deBanked in April 2019. “The word ‘loan’ should be banned from their email and Word files.”

Although our relationship was one of professional acquaintances, I often told those seeking advice about MCA syndication that they should “probably call Greg Nowak about that.”

In “Does Your Merchant Cash Advance Company Pass The Scrutiny Test?“, Nowak explained that funders that decide for business purposes to solicit money from investors, have to be careful not to run afoul of SEC rules. He said that he recommended funders treat these fundraising efforts as if they are issuing securities and follow the rules accordingly. Otherwise they risk being the subject of an enforcement action where the SEC alleges they are raising money using unregulated securities.

“You need to be very careful here because these rules are unforgiving. You can’t ignore them,” Nowak said.

California’s Business Loan & MCA Disclosure Law Is Nearing Finality

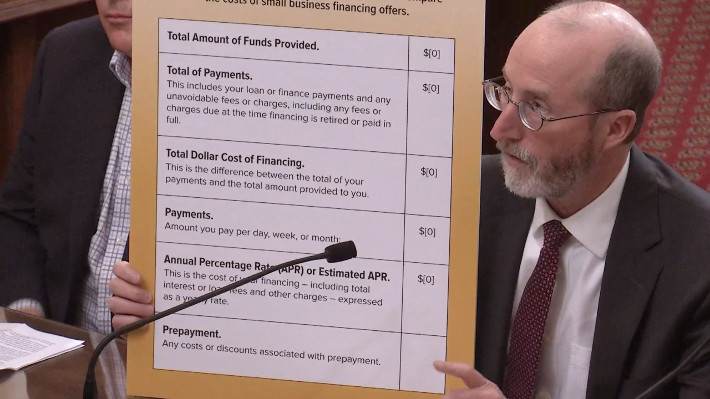

April 13, 2021 Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

The 52-page document is the result of years of negotiations between various parties that all have a stake in its implementation. Among the finer details are the characteristics of the fonts permitted in the disclosures, what column a certain disclosure can be placed in, and the aspect ratio of the columns themselves.

But that’s the easy part. Here’s the hard part, according to a brief published in Manatt’s newsletter yesterday.

“The modified regulations continue to require use of the annual percentage rate (APR) metric, rather than annualized cost of capital (ACC), to disclose the total cost of financing as an annualized rate. This appears to be a final decision, which will make it difficult if not impossible for many commercial finance companies to comply given the significant challenges of calculating APR on products with substantial variance in the amounts and timing of payments or remittances.”

Manatt highlights other issues, including that all the necessary disclosures be provided “whenever a payment amount, rate, or price is quoted based on information provided by the proposed recipient of financing…”

This requirement, the firm says, is not even required under Federal Regulation Z for consumer loans.

“Many companies will not be able to comply with this requirement absent radical changes to their California application and underwriting procedures, as it is common today for companies to have preliminary discussions with applicants about potentially available financing terms before full underwriting has been completed.”

Manatt’s newsletter on the issue can be found here.

Any interested person may submit written comments regarding SB 1235’s modifications by written communication addressed as follows:

Commissioner of Financial Protection and Innovation

Attn: Sandra Sandoval, Regulations Coordinator

300 South Spring Street, 15th Floor

Los Angeles, CA 90013

Written comments may also be sent by electronic mail to regulations@dfpi.ca.gov with a copy to jesse.mattson@dfpi.ca.gov and charles.carriere@dfpi.ca.gov.

The last day to submit comments is April 26, 2021

Coinbase Generated $800M Profit in a Single Quarter

April 7, 2021 The emerging powerhouse in the fintech industry isn’t a lending or payments company, it’s a cryptocurrency exchange. One can express as much skepticism as they want about Coinbase, but the company, which goes public on the Nasdaq next week, generated nearly $800 million in profit in Q1 of 2021 alone.

The emerging powerhouse in the fintech industry isn’t a lending or payments company, it’s a cryptocurrency exchange. One can express as much skepticism as they want about Coinbase, but the company, which goes public on the Nasdaq next week, generated nearly $800 million in profit in Q1 of 2021 alone.

Coinbase has 56 million verified users and holds $223 billion in assets, equal to about 11.3% of the entire crypto market.

The company says it is “building the cryptoeconomy, a more fair, accessible, efficient, and transparent financial system enabled by crypto.”

The company launched in 2012. Its last private market valuation was at about $90 billion.

Facebook Ads Don’t Work For Finance?

March 29, 2021 In an op-ed by Brittney Holcomb in Leasing News, Holcomb wrote that “when it comes to developing lead generation, social networks are not the answer.”

In an op-ed by Brittney Holcomb in Leasing News, Holcomb wrote that “when it comes to developing lead generation, social networks are not the answer.”

Holcomb breaks down her reasoning, explaining that Likes do not equal leads. It’s worth a read if you have advertised or have thought about advertising on Facebook, but I will respectfully disagree with her on the basis of her arguments.

“People don’t log on to social networks to search for products or services,” she writes, “They use social media to communicate with their friends and family.”

Perhaps so, but there are many different ways in which to approach Facebook advertising, and I say this as someone who has had success advertising in the B2B universe on the platform. Users weren’t searching for my product or service either and I wasn’t advertising for the sake of branding, something I personally do not even consider doing.

You can use social networks like Facebook to convert a lead you almost got or lost. For example, not everybody that comes to your website ends up completing a form and for those that do, fewer yet will end up signing a contract.

What happens is your prospects get distracted, decide to do more research, or get wooed by a competitor. Maybe they just weren’t convinced the timing was right. This is where social network advertising comes into play because you can relay that website visitor data or unclosed leads to Facebook and serve ads ONLY to those prospects. By knowing exactly where your prospect left off with you, you can set your campaigns to target them with the most appropriate advertising. That prospect might not be searching for your product on Facebook (just as Holcomb suggests), but you can appear right there like magic in their feed to remind them of exactly where they left off last time they engaged with you.

You can pretty much do anything you want especially if you’re actively managing and monitoring your web traffic and analytics.

Maybe you only want to serve ads to visitors who didn’t fill anything out on your website but clicked around for more than 2 minutes. Worth a shot, perhaps?

Consider the person shopping around who spent a few minutes researching a financial solution on three different company websites. They don’t fill anything out but instead resolve to make a decision on where to apply in the next couple days. That night and each night thereafter, one of those companies appears in their Facebook feed constantly, telling them why they’re better than the competition or that they’re the goto-brand. It’s an ad, yes, but it creates the impression that this company is everywhere and can place them top of mind when it’s time to decide. That can be money well-spent. It’s also the fundamental way in how social media advertising works these days, which is why we sometimes get creeped out by how well ads seem to know us. Anyone can do this.

Admittedly, one might not have any leads to target on social media if they don’t have website visitors to begin with, hence why paid search would be a better medium to choose if given the option between one versus the other.

I believe the two are not mutually exclusive, however. First get the prospects to your website (be that through paid search or organic means or whatever), and then close those prospects through social network advertising. Your competitors are already doing it and that’s why some of them are doing so well.

Facebook Ads Can Work For Finance. They just have to be properly tailored. And once you get it right, you’ll be kicking yourself for not having taken advantage of it for so many years.

Funding Circle US Originated $800M in 2020, More than 90% of Borrowers Were Making Payments

March 26, 2021 Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle’s US loans generate low annual returns, its highest being a projected return of 4.1% to 4.9% for its 2016 cohort. Its 2020 cohort is projected to generate an annual return of between 1 – 3%.

Overall, Funding Circle reported a total net loss of £108.1M (approx $150M US) on just £103.7M in revenue, a massive loss that stemmed entirely from the first half of the year, attributed mostly to a write-down in “fair value.”

Funding Circle’s primary market is the UK. When comparing the market with the US, the company said that the US is in an earlier stage of development even though the market is 5x larger.

No, Corporations Can’t Sue For Usury in New York, Appellate Division Rules

March 25, 2021 Businesses hoping to use the New York State court system to invalidate an MCA or financing agreement, suffered a major defeat on Wednesday. The Appellate Division, Second Judicial Department, ruled that corporations cannot assert usury as a cause of action, even if the allegations meet the criminal usury basis. In deciding this, the Appellate Court was simply affirming what New York’s statute on the matter plainly says.

Businesses hoping to use the New York State court system to invalidate an MCA or financing agreement, suffered a major defeat on Wednesday. The Appellate Division, Second Judicial Department, ruled that corporations cannot assert usury as a cause of action, even if the allegations meet the criminal usury basis. In deciding this, the Appellate Court was simply affirming what New York’s statute on the matter plainly says.

This has not stopped plaintiffs from asserting criminal usury as a cause of action in New York, however, but now such attempts will probably be fruitless.

In May 2016, Global Merchant Cash, Inc. (GMC) entered into a merchant agreement to buy the future receivables of Paycation Travel, Inc. Paycation breached the contract and GMC ultimately filed a confession of judgment. Paycation then tried to vacate the judgment by suing GMC on several grounds including its theory that the judgment was void and unenforceable because the underlying agreement was for a criminally usurious rate of interest.

GMC moved for summary judgment to dismiss the complaint and its motion was denied. GMC appealed the decision insofar as it believed Paycation could not assert criminal usury as a basis for a cause of action.

On March 24, 2021, the Court rendered its decision on the narrow debate in GMC’s favor.

“A transaction . . . is usurious under criminal law when it imposes an annual interest rate exceeding 25%” (Abir v Malky, Inc., 59 AD3d 646, 649; see Penal Law § 190.40). General Obligations Law § 5-521 bars a corporation such as the plaintiff from asserting usury in any action, except in the case of criminal usury as defined in Penal Law § 190.40, and then only as a defense to an action to recover repayment of a loan, and not as the basis for a cause of action asserted by the corporation for affirmative relief (see LG Funding, LLC v United Senior Props. of Olathe, LLC, 181 AD3d 664, 666; Intima Eighteen, Inc. v Schreiber Co., 172 AD2d 456, 457). Accordingly, the Supreme Court should have granted that branch of the defendant’s motion which was for summary judgment dismissing so much of the first cause of action as alleged criminal usury in violation of Penal Law § 190.40.

This decision did not decide the entirety of the case and litigation between the parties is still pending. It does, however, bring conclusive clarity to whether or not corporations can assert usury as a cause of action, even if it’s alleged to be criminal.

The case number is 52579/2017 in Westchester County in New York Supreme Court. The Appellate decision can be viewed here.

Tune In Tuesday at 10:30 AM EST: deBanked TV Live – With Guests From the Business Funding Industry

March 22, 2021 deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked’s massive in-person conference, Broker Fair, will return to NYC later in the year on December 6th at Convene at Brookfield Place in lower Manhattan.

Connecticut Introduces Commercial Financing Disclosure and Double Dipping Bill

March 20, 2021 Ever since New York State Senator George Borrello famously questioned the meaning of “double dipping” in a commercial financing transaction, states have rushed to include the term in proposed laws despite no one knowing exactly what it means.

Ever since New York State Senator George Borrello famously questioned the meaning of “double dipping” in a commercial financing transaction, states have rushed to include the term in proposed laws despite no one knowing exactly what it means.

The latest state is Connecticut, which introduced SB 745 in February, an “Act Requiring Certain Financing Disclosures.” It is essentially a copy & paste of New York’s recent law which is slated to go into effect in June.

The Connecticut bill similarly applies to factoring, merchant cash advance, business lending and more. It was introduced by State Senator Saud Anwar (D).

A hearing held on March 2nd, drew testimony from the Commercial Finance Coalition, Small Business Finance Association, Electronic Transactions Association, Innovative Lending Platform Association, and Secured Finance Network.

If the bill passes, it is designed to go into effect in October of this year.