Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Dumbest Guy in the Room

May 11, 2015 “This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“So what would need to be different in order for this to be a more viable idea? Like what would I need to change and come back with?” I asked.

“Come back?! COME BACK?! Don’t come back,” she shouted while taking my business plan and literally crumpling it into a ball and throwing it on the ground. She then got up and left. She was shaking from the rage. I was the dumbest person she ever encountered and it took effort for her not to kill me.

This experience happened to me three years ago when a NYC-based Venture Capital group sent out invitations to a free seminar and workshop. I liked the refreshing thought of hearing what VCs had to say, especially those not familiar with the merchant cash advance industry. Besides, I had a few concepts I wanted to get feedback on, and thought this would be a great opportunity to do it.

The seminar was more of a fireside chat, held by a zen-like VC I’ll refer to as Rain. He was in his mid-30s, wore a long flowy purple velvet shirt and sat indian style and barefoot in the front of the room. It was a stark contrast to the attendees in the audience, all of whom were wearing suits. Rain walked the crowd through his experience as a VC, most of which seemed to be an annoyance to him. Startups were full of personal drama of which he often got roped into. There was always a partner who was an idiot, a delusion the founder(s) couldn’t see past, or an insatiable need for additional funds.

And during the Q&A at the end, an attendee asked him if he would ever consider using a VC to raise money if he were not a VC himself. “Put the phones down guys, this stays here,” he said. “I wouldn’t.”

However confusing that might come across as, it didn’t change the energy in the room. Just about everyone who attended had an idea for a startup and desperately wanted VC funding.

Afterwards, you were allowed to schedule a one-on-one with one of their startup experts to develop your ideas further. It sounded cool and it was free, so I signed up.

I drafted up a concise business plan based upon a model that was just starting to take root in the merchant cash advance industry. It had its own little twist and I’m sure flaws too, but I believed this one-on-one would be a helpful conversation where I could get honest feedback without giving anything away to potential competitors.

Three minutes into the meeting, I was being scolded. “What do you mean it would break even for the first 2 years?!”

“Oh, well what I’m try –,” I attempted to respond. She talked over me. “You mean to tell me you would make no money in the first 2 years? Are you starting a charity?!”

“Well I was under the impress–,” I started, but she kept going. “This is the absolute dumbest thing I’ve ever seen.”

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

Not me though. I was the dumbest guy in the room, too dumb to even come back with something better. It was a humiliating moment considering I thought this was supposed to be an instructional meeting where the experts would essentially help you master a business plan.

As I walked out of the office towards the elevator, I noticed that even the cheery receptionist who had excitedly welcomed me in, ignored me with her head down as I walked out.

There goes the dumbest guy that ever existed, I imagined she was thinking.

My world spinning as the elevator descended, I tried to recount how it went wrong so quickly. I had showed her a pro-forma P&L that broke even for the first two years as I would reinvest 100% of the profits back into marketing to scale. I personally didn’t like it that way. I wanted to make money, but everyone around me was bleeding red and raising tens of millions along the way. I had started to believe that sacrificing any shred of profitability in exchange for growth is what got investors excited.

My expert didn’t share that view. A business that wasn’t profitable wasn’t a business. It was dumb, and not just regular dumb, but the dumbest thing that anyone ever thought of. EVER.

A couple of days later when I had shaken off the blow to my self esteem, I was thankful for the experience. She was a New Yorker to the core and so was I. I had no inner desire to start a business that didn’t make money (for the sake of disrupting or whatever), but I was being swept up in the craze of companies that were doing just that. She brought me back to reality, though she left a lasting imprint of a boot on my ass.

Three years later, companies with models similar to the one I had cooked up have raised hundreds of millions of dollars. They don’t break even. They lose money, lots of it. But they are looked upon and celebrated as some of the brightest guys in the room. Many of those guys are smarter than me and are probably executing their concepts way better than I ever could. But the lose-a-lot-of-money and grow model isn’t meant for everyone. It all depends on who you’re talking to.

In HBO’s Silicon Valley, a hit that many view as more of a reality show than a sitcom, they poke fun at a truth purveying the California startup scene. Forget profits, the show explains, just having revenues hurts your chances of raising money.

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

Two years ago, Bezos was worth $25 billion and was the 20th richest person in the world. Some experts might say a business model that loses money for 20 years would qualify as the new winner for dumbest thing that ever existed ever. It’s apparently just the opposite.

But once you find an investor that believes in the loss model, do you take the money and then go out and disrupt, hoping that somehow you’ll end up a billionaire?

Loan broker Ami Kassar is faced with that very dilemma. In his recent blog post, he wrote about the offer he has on the table from a VC, “While I could substantially grow my top line – the chances of making any profit are small and the chances of losing money are high.”

Fictional billionaire Russ Hanneman would surely approve, but over in realityville, Kassar is balking. “I can only speculate that they’re more interested in market share – than profits. Their investors want growth. They’re on the venture capital treadmill.”

Admittedly, I poked fun at Kassar, an entrepreneur I’ve often sparred with online. “Should I be worried that in their quest for growth they will build a train and run me over?” He asked in his blog.

Of course I linked to it in the following manner:

Kassar concludes that sustainable long term value is the only logical way forward. Is he wrong?

The current investment atmosphere where anybody with a model and a programmer is raising hundreds of millions of dollars to basically see how fast they can spend it all, is affecting those that have always believed in profits and longevity.

In another post by Kassar just a week earlier, he wrote, “Am I missing the boat and doing something wrong? That’s how I have felt lately as I’ve watched the emergence of the online small-business financing space. It seems every other week I wake up to another announcement about a company in the small-business financing space who has raised a lot of money from venture capitalists at a really high valuation.”

Just last week, consumer lending startup Affirm raised $275 million in a Series B round. Many people in the alternative lending community had never heard of Affirm but they are apparently so good that they can raise a quarter billion dollars.

Investors are scrambling. They don’t want to be left out. On multiple occasions, I have heard of investors skipping basic due diligence in a rush to capture a deal. Some of those deals blew up in a matter of weeks, others in months when they realized they didn’t even know who the owners were or what financial standing they were in.

Lending Club and OnDeck have received billion dollar valuations. That’s what everybody wants, though the market has temporarily cooled on OnDeck, a company that has lost money for almost eight straight years.

Even Shark Tank investor Kevin Harrington has gotten in on it, through his new business loan marketplace, Ventury Capital.

One thing looks certain three years after I met with that expert. The supposed dumbest thing that could ever be conceived of ever has made tons of people millionaires.

A year ago, Kevin Roose of New York Magazine wrote this of profitless startups, “They’re simply taking millions of dollars in venture capital with the hope of keeping prices low, pushing rivals out of the market, and eventually finding a way to turn a profit.” It can be predatory pricing, Roose argues. Basically large venture backed companies can sell below their cost using unlimited funds until the competition is out of business. Then with the entire market all to themselves, they can figure out a model towards profitability.

There seems to be a lot of this happening in the alternative lending space where the lenders backed by hundreds of millions of dollars are not only undercutting the competition at a loss, but they’re running lobbying campaigns that accuse their profitable brethren of being greedy and predatory. The media and general public eat this message up. There is no defense for a lender who has been accused of charging too much by one charging less even if the one charging less will need to declare bankruptcy if it does not raise a fresh round of new capital to sustain operations.

Only the rare observer can read between the lines as Forbes contributor Marc Prosser did. In his own research, he discovered that, “a company which loans money to small businesses at an interest rate of more than 50% was losing money.”

Though I won’t name names, there are a few players out there that believe the answer to their cycle of losses is to push regulatory agencies to attack profitable companies, or at least constrain them through penalties and new laws. Essentially, if it looks like they can’t win the war of attrition, then they might as well stick the government on them.

Speaking of the war of attrition, the race to bring costs to merchants down to zero doesn’t seem to be having the desired effect on the competition. In OnDeck’s Q4 earnings call for example, CEO Noah Breslow said the following:

Overall this market is still characterized by extreme fragmentation. The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.

Translation: Once merchants have an offer from somewhere, they go with it. There is no price-competitive marketplace on the macro level.

OnDeck has been undercutting the entire merchant cash advance industry for years. None of their competitors have gone out of business, at least not because of a profit squeeze. Instead, everyone is growing, OnDeck included.

So why lose money?

In the case of OnDeck, they can argue that growth has allowed them to expand into Canada and Australia. They’ve forged partnerships with Prosper and Angie’s List. They’ve acquired more data because they’ve done more deals than most. And who is another billion dollar company likely to partner with in the lending space? Probably the one doing 10x the volume of everyone else, the one whose name is all over the place. They have the advantage to win the partnerships.

Five years from now, when the competition is trying to catch up in volume, all the lucrative partnerships might be snatched up already. Maybe it really is about who can spend the most the fastest. It’s a depressing thought.

Some startup vets will you tell that the most important aspect is actually the team. The CEO of 140 Proof for example has written, “You succeed or fail not on the strength of your idea or your product, but on the strength of your team. Venture capitalists fund teams, not business plans.”

With that in mind, I tried to imagine how that meeting three years ago would’ve turned out had I showed up with OnDeck’s CEO Noah Breslow and Lending Club’s CEO Renaud Laplanche in tow. “We’re going to disrupt lending,” I imagine the three of us tell the fierce startup expert.

The expert knew nothing about me. As far as she knew, I was just some random guy off the street holding a stack of papers with an incredulous plot to dominate the lending industry. I had never worked for a bank. I was young. I had no partner. I didn’t graduate from Harvard or MIT. It probably looked pretty ridiculous. “Duhhh so whaddya think?” I imagined I appeared to her.

With her guard down, she had no reason to hold back from saying what she really felt, that the plan was the absolute dumbest thing she’s ever seen.

Might the dumbest guy in the room only be that because he believed what she said? Or did she have it right all along?

The OnDeck Hedge

May 6, 2015 Days after OnDeck went public in December 2014, a handful of their competitors licked their lips and said, “Perfect. Now we can hedge ourselves.”

Days after OnDeck went public in December 2014, a handful of their competitors licked their lips and said, “Perfect. Now we can hedge ourselves.”

But can they really?

OnDeck isn’t quite merchant cash advance and not quite Lending Club. They might be heralded in news media as the poster child for the non-bank business financing movement but one could hardly say that they typify the average company in the industry. They do things their own way and always have. It’s the very reason they are often criticized by their competitors. OnDeck doesn’t represent an industry but rather an antithesis to an industry they were borne out of.

That’s not to say there aren’t many common denominators between their products and others such as merchant cash advances. There are. But as an outside investor who wanted to be long on the success of the merchant cash advance industry, OnDeck isn’t a perfect match. And if they wanted to be long on non-bank business lending, the daily payment short term system at the core of the company probably isn’t what an investor had in mind.

OnDeck presents only one investment opportunity, themselves.

But what if you short them? That’s the trade some funders and lenders talk giddily about over drinks as the answer (at least hypothetically) to an eventual economic downturn. How do you hedge your own portfolio’s losses? Just short OnDeck! or so the theory goes.

I don’t doubt that some folks have secretly placed the OnDeck hedge in their back pocket as a legitimate possibility, but I’m not sure anyone has really thought this through.

First, many funders rely on credit facilities from third parties to fund deals and scale operations. That means restrictions and covenants on how the money is allocated. I don’t think taking a multi-million dollar short position on a single stock was what the institutional lenders had in mind. Business lenders and merchant cash advance companies are not hedge funds. The immediate reaction to a downturn (whether miniscule or massive) should be to reduce the default rate, tighten underwriting, and cut costs, not take huge positions in the securities markets.

The logic behind this trade is almost like realizing that the restaurant you own is on fire and instead of running for water to put it out, you call an insurance company and take out a policy on the neighboring businesses instead. If those businesses burn down, you get paid, and the loss from your own restaurant burning down will be offset. Except now your business is gone.

The logic behind this trade is almost like realizing that the restaurant you own is on fire and instead of running for water to put it out, you call an insurance company and take out a policy on the neighboring businesses instead. If those businesses burn down, you get paid, and the loss from your own restaurant burning down will be offset. Except now your business is gone.

Second, OnDeck isn’t a perfect match for this trade. In Barroom small talk, the hypothetical circumstances surrounding a hedge are less often an economic downturn and more often about everything going to hell. If everything goes to hell, we can just short OnDeck!

Except there are many sane reasons why OnDeck would soar in such a scenario. If purchases of future sales were interpreted to be usurious loans, well then that might cause everything to go to hell for merchant cash advance companies but boost the value of OnDeck who has been cognizant of state usury laws and the complexities of being an actual lender for some time now.

And if business lenders issuing 5 year loans with monthly payments are all falling apart, it’s possible that OnDeck with their 1-year terms and daily payment schedules would be a refuge.

Just yesterday, OnDeck beat the street’s expectations and then for some reason immediately lost more than 15% of their market capitalization. Bloomberg’s Zeke Faux ran the following headline, OnDeck Tumbles as Competition Forces Online Lender to Cut Rates, despite OnDeck’s execs specifying TWICE in the earnings call that competition had no bearing in their decision to cut rates.

While beating the street and subsequently getting clobbered may lend credence to the phrase, “buy the rumor, sell the news,” there wasn’t anything particularly jarring in the report to warrant such a huge sell-off. OnDeck doubled year-over-year revenues and they funded an astounding $416 million in loans in a single quarter.

The 15+ day delinquency ratio increased from 7.2% to 8.4% year-over-year however. CEO Noah Breslow and CFO Howard Katzenberg defended this as normal Q1 seasonality but were non-committal to the direction this would move in future quarters. Maybe that’s what spooked investors? It’s tough to say.

Had CAN Capital been publicly traded too, should OnDeck have taken a short position on them when they saw their own 15+ day delinquency rate spike? And should OnDeck buy put contracts on competitors that also eventually go public, you know… just in case everything goes to hell?

Probably not.

The only investment OnDeck should focus on making is in themselves. Leave the trades to the hedge funds who may actually be in the business of buying insurance contracts on a burning restaurant’s next door neighbors.

The only hedge to a failing business is to create a business built to last. Shorting OnDeck makes for entertaining barroom chatter, but it cannot be a serious fallback for a funding company worried about their portfolio.

Get Paid More in Alternative Business Financing

May 5, 2015Maybe you’re happy with your current job now.

Maybe you’re making a lot of money.

Maybe you’re not.

Or maybe you’re at least curious to see what’s out there?

This is an exciting time to be in the alternative business financing industry. The OnDeck IPO made several senior-level people in the company instant multi-millionaires, many of whom are only in their 30s.

Now is the time

Now is the time

Back in 2007, payment processing professionals thought that the age of merchant cash advance was over. A Green Sheet writer in August of that year actually wrote a story about cash advance and said, “I think that boat has come and gone, and I missed it.”

And yet there were 20-somethings making between $200,000 to $1 Million a year. I knew a few of them and for their sakes, I won’t name names. The industry has treated those who are good at it very well.

Not everybody got rich though.

The industry got corporate really fast in 2008 and 2009 when it became apparent you couldn’t run a funding company like it was Delta Tau Chi in the movie Animal House. Commissions and salaries shrank and then leveled off for a time. But then the ACH payment methodology renewed the industry’s wild growth and made every business owner in the country a potential candidate for funding, rather than just those processing more than $5,000 a month in Visa/Mastercard sales.

Commissions shot up, way up. Opportunities exploded.

Today, having experience in the merchant cash advance or alternative business lending space is extremely valuable. It’s a buyer’s market. Demand for qualified and experienced professionals by funding companies and brokers far outpaces those looking for work. There are 20-somethings making well into the six figures again, particularly if they’re good at sales.

Other positions are in demand too: Operations, Underwriting, Administrative, Collections and more. If you have experience in these areas, there are employers very eager to talk to you.

But maybe you’re 100% happy.

Or maybe you’re not.

It’s a buyer’s market

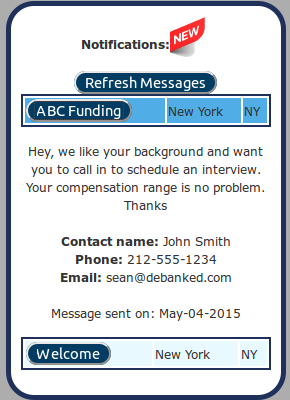

Because the demand for experienced individuals is so overwhelmingly high, we’ve created the deBanked Jobs network and put the ball fully in the court of the job candidates. That means you can fill out a blind profile that details your background, but keeps your identifying information away from employers. Employers can view the background but they won’t be able to see your name, email address, or username. If they like your profile, they can contact you through the site.

You’ll be able to see who the employer is and their message when you log on. Only if you choose to email them or call them to schedule an interview will they ever know who you are. If you don’t do either, they’ll never know who you were. Like I said, the ball is in your court. Why not see who comes knocking once they’ve seen a little bit about you?

Initially, we’re only allowing a handful of vetted employers on the network to prevent abuse and solicit feedback. As of now an employer can only send you one message.

We’re also not sending email notifications so if you’ve registered with your work email address, job notifications will not be sent there. They can only be viewed by logging on.

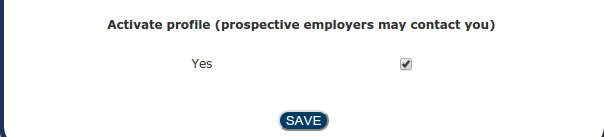

If you no longer want your profile to be discoverable by employers, just untick this checkbox and click save. It’s unticked by default so if you’ve already set up a profile but forgot to tick the box, you won’t be receiving any messages anytime soon.

Anyone can create a jobs profile so long as they have a deBanked forum account. If you don’t have one, register here. Then just log on to create a profile on the network at https://debanked.com/jobs/.

Have feedback? Notice a bug? Are you an employer looking to hire that wants access to this? Email sean@debanked.com.

The industry’s growth is on fire. Are you happy with your place in it???

OnDeck Q1 2015 Earnings Call

May 4, 2015OnDeck (ONDK) is scheduled to release Q1 2015 earnings today at 5pm EST. Anyone can register to listen to the call via web HERE or by dialing in through (877)201-0168 with conference ID 23530259.

OnDeck closed Friday at $19.29, just 8 cents below where it closed leading up to the 2014 Q4 and year-end earnings call on February 23rd. By that measure, the stock has been relatively flat.

Recently, the company announced expansions into Canada and Australia, though analysts such as Henry Coffey of Sterne Agee remain skeptical.

“If the opportunity is so large in the U.S., why go halfway around the world to lose money?” Coffey told the Wall Street Journal.

The Street doesn’t see eye to eye on OnDeck. Compass Point issued a sell rating with a price target of $14 while Deutsche Bank issued a buy rating with a price target of $28. Meanwhile, news media continue to disseminate incorrect information about the company by often times referring to them as a peer-to-peer lender.

OnDeck has never been a peer-to-peer lender.

In April, the company announced a strategic partnership with Prosper, though the extent of their collaboration is uncertain.

OnDeck predicted a net loss for all of 2015 in their 2014 year-end report. Consequently, it is likely OnDeck will report a loss today for Q1, though analysts expect year over year revenue growth of almost double.

Wasted Leads, a Plague in the Business Financing Industry

May 1, 2015Many people don’t know this, but a few years ago I dabbled in online lead generation for business lenders and MCA companies. I did online marketing, captured prospects, qualified them using a very simple algorithm, and then directed them to the appropriate companies for a fee. I don’t do this anymore.

One of the first features I added to boost conversion rates of the recipients was auto-phone connect. It worked like this:

- Prospect fills out a web form with their phone number

- Algorithm qualifies it

- Data is sent to appropriate lender/funder via API or email

- My phone system dials the recipient’s live sales line

- Sales rep picks up

- My phone system then dials the applicant’s phone number and if they answer, they’re immediately connected to the sales rep on the other end

The entire process was fully automated. An applicant could fill out a form and be called with a live sales rep on the other end in literally 3 seconds. Basing the idea on studies performed by experts like Dr. James Oldroyd, who believes the odds of reaching a lead declines exponentially after the first five minutes, I thought my system was pretty damn brilliant.

Not quite. Every single company that tried it hated it. There were problems on all sides. The receiving companies would be too busy on other calls to answer the auto-connects, they’d be out to lunch, or the calls would come after working hours. Some receiving companies felt they didn’t have time to digest the lead they were being auto-connected to since the call was being connected before their CRM or email was even processing the data. That meant right after the merchant had just filled out a web form with all the necessary information, the sales rep being auto-connected to them didn’t have it yet and thus the merchant had to frustratingly state it all again.

Even worse, sales reps would answer the call and wait to be auto-connected to the applying merchant, but many merchants wouldn’t answer the phone on their side even though they had just literally filled out a form seconds ago requesting somebody call them. That meant sales reps were often answering dead calls. Doh!

Technological flaws aside, some of the casual feedback I got was that seasoned sales reps preferred to contact leads at their own pace anyway, with the belief that it improved their closing percentages. Why go into a call completely unprepared in seconds or minutes when you could mentally digest the prospect’s application and possibly do a little research on them online before reaching out?

But Oldroyd’s research would argue that it was better to reach out as soon as possible because waiting a span of mere minutes exponentially increases the likelihood the prospect will not even pick up the phone when you call.

So what was the happy medium or best method? It’s hard to say since I didn’t continue to evolve it or test further. I bowed to the pressure of the lenders and funders, all whom wanted it gone and I disabled the automatic phone connects for good.

Meanwhile in 2015

Meanwhile in 2015

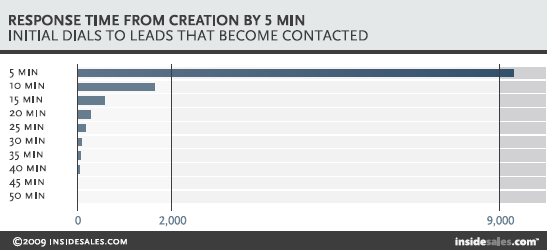

An experiment conducted early this year by FinServ’s Steve Conner found that 100% of sampled business financing brokers/ISOs in the industry waited longer than five minutes to call an inbound web lead. That’s a long enough delay by Oldroyd’s standards to infer that many merchants will no longer be interested by then to even accept the call.

Conner pretended to be a merchant and completed web forms on the websites of 52 brokers and funders in the industry. The fastest broker called in 6 minutes, but the average (for those that actually called) was an astoundingly slow 742 minutes, MORE THAN 12 HOURS LATER! More than half never even called at all. What the heck?!

Back in September I said that lenders will pay as much as $200 for an exclusive inbound lead in this industry. The kicker? Conner’s experiment and Oldroyd’s data say that brokers are waiting until the lead is already pretty much dead by the time they finally attempt to make their first contact.

No wonder costs per acquisition are so high?

The numbers were better for direct funders even though more than half of them never called the prospect at all. For those that did call, the average time to make contact was 17.5 minutes, far better than the average of 12 hours for brokers.

While I do not know specifically which websites were sampled, Conner’s full report (which you can download online) says that they researched the companies beforehand.

One has to wonder what happened to the leads for which nobody called. Were they filtered out and rejected by an algorithm? And if so, shouldn’t the prospect deserve to know?

While receiving a phone call from a sales rep literally seconds after completing a web form may seem creepy or overly ambitious, there’s nothing more disconcerting than complete silence. Where exactly did your information go then?

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

“I’m still shopping around,” I tell them.

The periodic emails don’t bother me. Many years ago, they paid for my contact information, possibly as high as $200 for it. They might as well keep trying.

1-call-close or bust

Ken Krogue, the CEO of InsideSales and a Forbes Contributor, discovered after his research that sales reps only make 1.3 call attempts on average to a lead before giving up. He tested over 10,000 companies in fifteen secret shopper studies. “We fill in a lead on their Web site with a real phone number and email address and track how fast they respond and how many calls or emails they make,” he wrote on Forbes.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

In off-the-record conversations I’ve had with a handful of lead generators in this space (companies that are neither brokers or funders), a leading challenge they face with buyers obsessed with costs and closing ratios is that the buyers don’t always end up calling all the leads or they call them once and never call them again.

There’s pressure on lead generators to provide 1-call-close quality leads. If the merchant can’t be closed on the first call, some reps are just throwing them in the trash, never to be remarketed to ever again.

“Spoiled,” was the word used by one industry veteran to describe the newer generation of sales reps who have walked into an industry growing by leaps and bounds. So many leads are coming in, that they don’t even know what to do with them all.

Research argues however they should be calling them inside of five minutes and of course following up. And there’s no reason that so many are never called at all.

One issue Conner discovered in his experiment is that several companies in this industry had broken websites. The HTML or javascript wasn’t set up right and the forms couldn’t even be submitted. :::face palm:::

A lot of money might be pouring into this industry, but a lot of money may also be getting flushed down the tubes.

Do you know your Web form-to-call response times? You should…

Letter From the Editor – May/June 2015

May 1, 2015 Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

New financial products can be just as intimidating to the professionals working within the wider industry as they are to the customers they’re being offered to. I’ve blogged often of my experience investing in Lending Club and Prosper notes, something I assumed everyone in the business finance world could relate to. Alas, I find that usually raises more questions with readers than it does answers.

Are you just nodding your head and smiling when your peers talk about their alternative lending portfolios? There’s no better way to understand today’s loan marketplaces than being an investor in them, even if it’s just a small amount. Whether it’s merchant cash advances, real estate loans, student loans, or credit card debt, there are plenty of opportunities and worlds to explore. You should conduct research, diversify, and be smart of course. You don’t want to be trapped in a bubble.

Outside the knowledge bubbles, we have regional enclaves. There are entire city neighborhoods being overrun by small business financing startups. In New York City, it had long been Midtown, but some shops started moving south and before anyone realized what was happening, Wall Street had been overrun by a new breed of broker. The culture in lower Manhattan is different than you might find in Midtown or in the next two largest industry hubs, Miami and San Francisco.

In this issue, we’ll begin to explore the industry’s bubbles, both geographically and structurally.

–Sean Murray

Defraud Merchant Cash Advance Companies, Go to Jail

April 27, 2015 We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

Just two months ago, the Essex District Attorney’s office in Massachusetts announced that, “six people were arraigned in Haverhill District Court on numerous counts of larceny, money laundering and fraud following a three-month investigation involving local, state and federal authorities into a false invoice scheme.”

But invoice factoring wasn’t the only thing on the crew’s hit list. Sources and research revealed that among the victims were at least five merchant cash advance companies, the names of whom we won’t mention.

At least one funding company’s UCC was filed two weeks after the defendants had been arrested, alluding to the possibility that they had obtained one last merchant cash advance in the days prior.

The Salem News reported that the group is alleged to have netted at least $700,000 over a five year period.

47-year old Susan Yerdon was fingered as the mastermind and was sentenced to three and a half to six years in state prison.

According to The Salem News, “she pleaded guilty to money laundering and other charges, will be required, in exchange for her sentence, to testify against some of her codefendants.”

“Police seized a Mercedes Benz E Class AMG, a GMC Yukon Denali, a BMW 328i, a Cadillac DTS, and a Pontiac Solstice.”

Rand Paul Speaks at Bitcoin Event

April 20, 2015 Yesterday, Senator Rand Paul spoke at a private Bitcoin event produced by Blockchain Technologies Corp in Midtown Manhattan. It was a gathering of monetary technophiles dressed in their Sunday best.

Yesterday, Senator Rand Paul spoke at a private Bitcoin event produced by Blockchain Technologies Corp in Midtown Manhattan. It was a gathering of monetary technophiles dressed in their Sunday best.

Paul’s main reason for supporting the Bitcoin movement/technology/currency was the ability to bypass the expensive fees tacked on by credit and debit card issuers. A business that only had a 3 or 4% profit margin could double its profits by eliminating merchant processing fees, he said.

The event lasted for about two hours with Paul only making an appearance for about 15 to 20 minutes.