Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

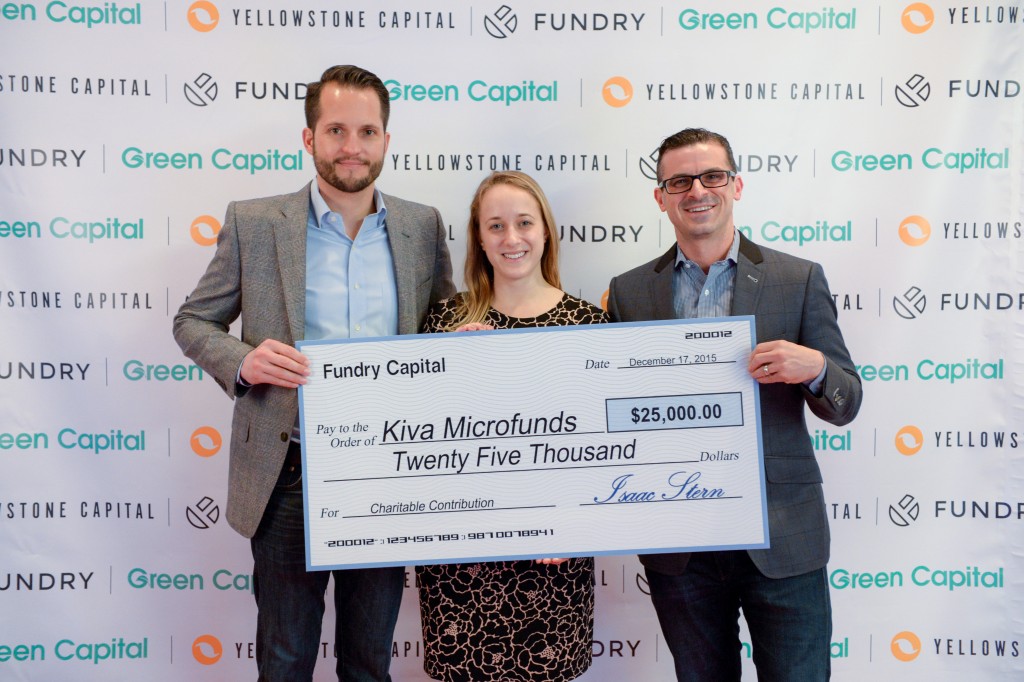

Fundry Donates $25,000 to Kiva at Red Carpet Event

December 22, 2015Fundry, the parent company of Yellowstone Capital and Green Capital, hosted a red carpet event last Thursday evening in New York City where they presented a donation of $25,000 to Kiva. Kiva is a non-profit organization with a mission to connect people through lending to alleviate poverty.

The event, which also celebrated their 2015 success, was attended by more than 300 people. All told, Fundry originated nearly half a billion dollars in small business funding for the year.

Brooklyn Eyeglass Merchant Defrauds Business Lenders

December 22, 2015 It’s another case of bad merchants. In this instance, Maksim Grinberg, the owner of D&M Optical and 9th Street Vision in Brooklyn have been charged with defrauding lenders out of $3.4 million. According to an article in the New York Times, Grinberg, along with two co-defendants, used false documents and guarantors to obtain numerous business loans over the last five years. He then used those funds to gamble, shop with his girlfriend, and pay his rent. The charges have resulted in a 148-count indictment filed by the Brooklyn district attorney’s office.

It’s another case of bad merchants. In this instance, Maksim Grinberg, the owner of D&M Optical and 9th Street Vision in Brooklyn have been charged with defrauding lenders out of $3.4 million. According to an article in the New York Times, Grinberg, along with two co-defendants, used false documents and guarantors to obtain numerous business loans over the last five years. He then used those funds to gamble, shop with his girlfriend, and pay his rent. The charges have resulted in a 148-count indictment filed by the Brooklyn district attorney’s office.

Brooklyn District Attorney Ken Thompson is quoted in the official report as saying, “this long-running scheme allegedly took advantage of banks and leasing companies as well as of hard-working doctors whose identities were stolen so they could be listed as loan guarantors. We investigated this brazen scam, put an end to it and will now hold those responsible accountable.”

The roster of victim lenders which included names like Wells Fargo, noticeably did not list any alternative lenders. While a UCC search revealed his D&M Optical Store used a merchant cash advance 10-years ago, Grinberg’s scam was directed at what was apparently an easier target, traditional lenders. “To secure the loans,” according to the DA’s report, “the defendants submitted fraudulent documents, including applications, lease agreements and delivery acceptance forms as well as forged signatures of loan guarantors, according to the indictment.”

It is perhaps another sign that lenders need to move away from paper statements and to tools that can be verified electronically through third parties in an automated fashion. According to the Times, the scheme only began to unravel once a guarantor whose identity had been stolen was contacted to make a payment on their $1 million loan.

World Business Lenders Rings in 2016

December 18, 2015On December 8th, World Business Lenders (WBL) wrapped up 2015 and prepared for the coming new year at their annual shareholder meeting hosted at the Waldorf Astoria in New York City. The event, which was mostly restricted to company employees, referral partners and shareholders, featured some out-of-town guest speakers including BFS Capital CEO Marc Glazer and RapidAdvance Chairman Jeremy Brown.

On a panel moderated by WBL Managing Director Alex Gemici, Brown and Glazer expressed their optimism for the industry’s future, but to some extent heeded caution. Brown specifically made reference to his prediction of a bursting bubble but conceded that he might have been off by a year or two. Glazer reminded the audience that both executives had weathered the financial crisis so that they had witnessed firsthand how a recession can affect their businesses, and made them stronger because of it.

WBL CEO Doug Naidus made a similar admission in his presentation, in that he thought that the bubble of unsecured lending would burst in 2015 but that it hadn’t happened yet. Still, he thinks it’s right around the corner. One of their primary hedges against a correction is that they secure their loans against real estate. Naidus has a background in mortgage lending so it’s a market they’re familiar with.

Another one of their key strategies is the franchise model. Over the last two years, WBL has acquired commercial finance brokerages and converted them into originating houses for their collateralized loan program. It has had a really positive impact on their growth and on their margins, according to information disclosed at the event. It’s expected that they will continue to pursue more acquisitions.

The sentiment of the event was rather festive and optimistic, with WBL enjoying a positive trajectory of growth and success.

National Security Could Prove to be Alternative Lending’s Achilles Heel

December 11, 2015 While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

House Financial Services Chair Jeb Hensarling said on Thursday that, “clearly the financing link to terrorism is a critical one.” As quoted by Politico, “everything’s on the table,” he said when asked about further scrutiny of online lenders.

His sentiment echoes other responses, some of which are clearly emotionally charged and accusatory. LendAcademy’s Peter Renton for example wrote, “I have had to answer such ridiculous questions as, is P2P lending going to become the new way for terrorists to get funding?”

With so much misinformation now floating around out there about online lenders, conspiracy theorists are even claiming that it would be impossible for someone earning $53,000 a year (As Syed Farook did) to get an unsecured loan for $28,000, the implication being that there is something more sinister going on. Of course those that work in the alternative lending industry, including myself personally as someone who invests on the Prosper Marketplace, know that’s not true.

But before the experts can be called on to answer the questions, those motivated to protect this country at all costs (with noble intentions) are rallying around swift and immediate consequences for online lenders such as Prosper.

“The issue may end up being whether marketplace lenders are too easy of a source of cash to finance terrorist attacks,” said Guggenheim Partners analyst Jaret Seiberg in a research letter.

In an article published by The Street, writer Ross Kenneth Urken basically likened Prosper Marketplace to Silk Road where bitcoins were used to buy drugs, weapons, and killers for hire.

Breitbart News, a right-wing news website, led in with an even bigger headline, San Bernardino: Has Islamic State Hijacked Consumer Loans?. It quickly sums up the story by insinuating that online lenders will become the funding tool of choice for ISIS. “The San Bernardino terrorists, Syed Rizwan Farook and his wife Tashfeen Malik, funded their killing spree with a debt consolidation loan, raising questions about whether terrorists might use popular consumer loans to fund their activities,” Breitbart wrote.

And the International Business Times argued that Utah industrial banks are aiding terrorism. “Meanwhile, industrial banks in Utah are taking full advantage of the lack of regulation in the peer-to-peer lending market while they still can, aiding potential terrorists along the way,” author Erin Banco concluded.

According to the WSJ, the House Financial Services Committee will examine whether new legislation is needed in online lending. They’ve also made inquiries to the Treasury Department about existing online lending regulations. Treasury Counselor Antonio Weiss’s previous remarks hinted that the Treasury up until recently was concerned about discriminatory lending practices more than anything else, but stressed that they were not a regulator in this area. Terror financing was not something they even addressed.

According to many sources, lawmakers are drafting up legislation on terrorism financing and expect to have something ready early next year. As for how that will impact online lenders is unknown. Right now, everyone’s still trying to figure out what just happened. Hopefully whatever is ultimately done is done intelligently.

CFPB Track Record on Anti-Discrimination Analyses Show Malfeasance

December 11, 2015Congressman David Scott (D), the same congressman that said, “God Bless the online lenders” back in October had some choice words for the Consumer Financial Protection Bureau recently after learning they manipulated data to falsely support evidence of racial bias in lending. According to the Wall Street Journal, Scott called their data “shamefully flawed.”

As explained by the WSJ:

The bureau has been guessing the race and ethnicity of car-loan borrowers based on their last names and addresses—and then suing banks whenever it looks like the people the government guesses are white seem to be getting a better deal than the people it guesses are minorities. This largely fact-free prosecutorial method is the reason a bipartisan House supermajority recently voted to roll back the bureau’s auto-loan rules.

The House of Representatives responded on November 18th by voting 332-96 in favor of stripping some powers away from the CFPB. In a bill, that hopes to be known as the Reforming CFPB Indirect Auto Financing Guidance Act if it is also passed in the Senate and signed by the President, attacks the CFPB’s guidance of the Equal Credit Opportunity Act as it applies to auto lending.

The House of Representatives responded on November 18th by voting 332-96 in favor of stripping some powers away from the CFPB. In a bill, that hopes to be known as the Reforming CFPB Indirect Auto Financing Guidance Act if it is also passed in the Senate and signed by the President, attacks the CFPB’s guidance of the Equal Credit Opportunity Act as it applies to auto lending.

“Bulletin 2013-02 of the Bureau of Consumer Financial Protection (published March 21, 2013) shall have no force or effect,” the bill states outright.

Bulletin 2013-02 addressed the auto lending industry by saying, “the ECOA makes it illegal for a ‘creditor’ to discriminate in any aspect of a credit transaction because of race, color, religion, national origin, sex, marital status, age, receipt of income from any public assistance program, or the exercise, in good faith, of a right under the Consumer Credit Protection Act.”

The CFPB reviewed loan data as expected to see if there were racial disparities but disturbingly did not actually know the race of the borrowers in many cases. So they guessed, according to the WSJ, by reviewing the last names and addresses of the borrowers. When being shown the results of their guesses against a sample of data for which they actually had racial background data, the CFPB only successfully guessed correctly 54% of the time. Despite being aware of this, the CFPB sued Honda, Fifth Third Bank, and others for discriminatory lending practices. Honda was pressured into settling for $24 million and Fifth Third for $18 million even though the CFPB’s data and methodology were false.

The House bill also requires that the CFPB publicly disclose the methodologies and analyses used to assess discrimination in auto financing, lest they continue to manufacture their own data, draw conclusions based on that, and then extort corporations for tens of millions of dollars through lawsuits, investigations and public shaming.

88 Democrats in the House joined their Republican colleagues in passing this bill.

This kind of blatant malfeasance is especially alarming considering the CFPB is already licking their chops to collect data on small business lending so that they can test it for racial and gender disparities as well.

As small business underwriting is markedly different from the commoditized world of consumer lending, it would be near impossible for a pious, law-abiding, and even omnipotent CFPB to make meaningful determinations. Considering that the CFPB we have acts in a manner as described above, small business lenders have a lot to worry about over the implementation of Dodd Frank’s Section 1071.

Dan DeMeo is deBanked’s November/December Magazine Cover

December 10, 2015Meet Dan DeMeo, his story, and the rise of CAN Capital in this November/December issue of deBanked. Researched and written by Ed McKinley, we’ve got the scoop you haven’t read anywhere else. If you’re not already subscribed to the magazine, you can SIGN UP HERE.

The web-based version will be up on December 11th.

Prosper Loan Linked to Terror – A Preliminary Assessment

December 9, 2015By now you have probably heard that one of the San Bernardino terrorists received a $28,500 deposit from WebBank.com two weeks prior to committing the attack. After Fox News broke that story, I may have been the first to publicly connect it to an alternative lender which was later revealed to be marketplace lender Prosper about 12 hours later.

As a Prosper investor myself, here are some things you should know:

The $28,500 deposit (if that was the exact true amount) would have been net of the origination fees. In all likelihood this was a loan for around $30,000 and the borrower only netted $28,500.

Those that have speculated that it would be impossible for someone making $53,000 a year (as Syed Farook did) to qualify for an unsecured loan of this amount are wrong. There are loans on the platform right now that fit these parameters. Online Lenders like Prosper and Lending Club are pretty aggressive with their lending.

The notion that Prosper somehow could’ve detected what the borrower planned to do two weeks later just isn’t possible. In lending, this is known as the asshole factor, meaning that even if the applicant meets all the criteria, they could just decide to be an asshole, and there’s no way to predict that.

There are strict laws in place to prevent all kinds of discrimination, meaning that even if Prosper had formed some kind of suspicion about the borrower, it may have been illegal to act on that suspicion. Such is the hypocritical paradigm of fair lending where factors that are measurable predictors of negative performance (or worse) cannot be legally used. Federal laws have purposely tried to create an environment where lenders make decisions on an objective basis they consider to be fair. In business lending for example, there is a law within Dodd-Frank that has not been implemented yet, but seeks to prevent loan officers from knowing the gender or even the name of the prospective borrower to protect them from subconscious discrimination.

Investigators have publicly announced that the terrorists were not on any watch lists and therefore there are no systems or checks that Prosper could’ve plugged into to have gotten the information.

Prosper and other alternative lenders already have Anti-Money Laundering Policies. I know this because I complained about Lending Club’s over a year ago.

The Wall Street Journal stated, “Only some nonbank financial institutions, such as mortgage lenders, are subject to Treasury rules requiring lenders to report suspicious activity to the government under the Financial Crimes Enforcement Network.” Maybe that’s true, but there is nothing suspicious about someone applying for a loan online who is not on any watch lists. I can’t think of anything that could’ve been suspicious unless they submitted fake pay stubs or forged documents.

“There’s no due diligence that’s done into how these loans are actually going to be used,” said Brian Korn, a partner at the law firm Manatt, Phelps & Phillips, LLP in the WSJ. This is true and at the same time related to anti-discrimination laws. Judging a loan applicant by their detailed monetary plans could potentially induce gender or ethnicity bias, even if subconscious.

There will be plenty of questions in the coming days from Americans, the media, and government officials about what alternative lenders are doing to make sure they’re not funding terrorists. Part of what they may learn is that for all the data that alternative lenders have at their disposal to make intelligent decisions on an automated basis, some of them cannot be legally used. They’ll also find out that there’s only so much that predictive analytics can actually predict.

It’s very unlikely that Prosper could’ve handled anything differently…

Alternative Lender Likely to Be Questioned in San Bernardino Terror Tragedy

December 7, 2015Fox News has reported that terrorist Syed Farook received a $28,500 deposit two weeks before committing the terrorist act with his wife. The source of the money? WebBank.com, an FDIC-insured, state-chartered industrial bank based in Salt Lake City, Utah. Perhaps more notably, it’s the bank that originates loans for dozens of alternative lenders including Lending Club, Prosper, and Avant.

WebBank.com is reportedly refusing to comment but in all likelihood we are probably going to learn that the loan was made by an alternative lender.

As written on Fox News:

The loan and large cash withdrawal were described to Fox News by the source as “significant evidence of pre-meditation,” and further undercut the premise that an argument at the Christmas party on Dec. 2 led to the shooting.

If the loan was indeed originated on a marketplace lending platform like Lending Club or Prosper, hundreds of Americans could potentially face the horror of having bought shares in the loan and made it possible.

For now, all we know is that Farook got $28,500 through a WebBank.com deposit. I’ll post more as the story develops.