Articles by Gerelyn Terzo

Creating a Credit Standard for Canadian Merchants

December 26, 2017

The Canadian alternative lending market is in earlier innings than the US market, which creates unique opportunities for funders and merchants alike. Indeed, the Canadian market is one comprised of nuances that distinguish it from the lower 48, which we have spotlighted before, and 2018 is shaping up to be a year that could redefine the parameters as we know them. One of the companies that is positioned at the forefront of this expansion is Montreal-based Thinking Capital

Jeff Mitelman, Thinking Capital’s chief executive, explained the company existed for about eight years before somebody called the industry fintech. “Rather than think of ourselves as a large funder in the context of the Canadian market, I like to think of us as having the greatest opportunity to get this new way of lending into the mainstream,” said Mitelman.

The challenge, he says, has moved away from ‘does this have a place in the market and do people want this’ (evidenced by the fact that Thinking Capital has funded thousands of businesses and deployed hundreds of millions of dollars) and shifted toward establishing a standard for business credit underwriting.

There are more than 1 million small businesses in Canada with no formal method to evaluate them. One of the most notable differences in the Canadian small business landscape is that there are no FICO scores for credit underwriting.

“The FICO score doesn’t exist in Canada. We have other similar measures of credit, but they are all very much consumer measures. They all fail to accurately reflect the credit worthiness of the small business,” said Mitelman.

Language & Education

The new face of credit for Canadian merchants, one in which Thinking Capital is positioned at the forefront, surrounds language and education and it is now taking shape.

“Interestingly the opportunity we have is around creating the language of credit and educating the market to say that there is a measure of small business credit that exists far beyond how credit used to be adjudicated,” he added.

This language would communicate to borrowers what their score looks like and how they should think of their own credit as it relates to their ability to borrow.

“There is no universal measure of credit that exists in Canada that says , ‘this business has great credit and this one has less than great credit.’ The opportunity that we have both as an organization and an industry is to establish a language on which credit can be offered to small businesses going forward,” said Mitelman.

One of the industries that is poised to benefit is restaurants, which historically has had a tough time accessing financing based on the belief that they’re a bad credit risk. “It’s an amazing industry that by default is just considered risky. Just saying ‘restaurants are risky’ full stop is an exclusive way to think about. The idea here is to be inclusive and say, ‘let’s find the right way to communicate credit worthiness back to the restaurants and help those that are doing great,” Mitelman explained.

Attention Small Businesses

Partners are a cornerstone to the Thinking Capital business model, including key relationships with the likes of Staples, CIBC, Moneris and Money Mart. The lender will rely on this model for its campaign to touch and educate small businesses about credit worthiness.

“What we are looking to do is really partner with brands that already have the attention of small businesses and in their messaging out to their customers let small businesses know that there is a better way to borrow; there is a bigger market for credit that is available through this new methodology than there was in the old way of thinking about credit,” Mitelman said.

Thinking Capital exclusively targets very large brands as partners. The lender has not taken the agent route and they’ve very much adopted a “lending as a service” approach with partners.

“2018 will be a big year of major partnership announcements for us,” said Mitelman. “Lending is being made easier and the addressable market for small business lending is being expanded.”

Mitelman went on to explain that small business demand for capital has always been there. “The ability to access working capital from brands that are trusted is something that’s changing and giving small businesses a whole lot of comfort around tapping the credit markets rather than bootstrapping themselves through vehicles that aren’t intended to finance small businesses, such as friends and family loans, personal loans and credit cards.”

MCA’s Top Social Media Voice

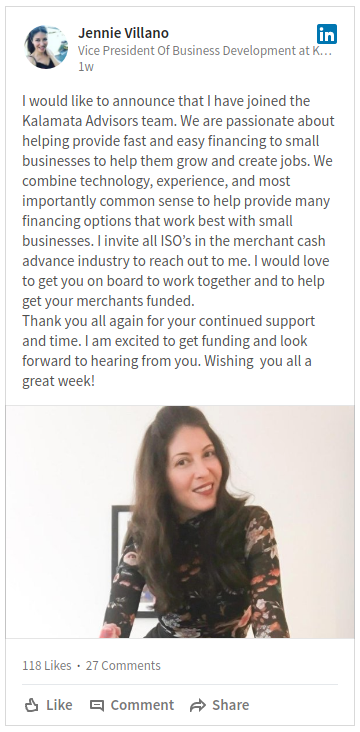

December 18, 2017 LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

By most standards she’s a newbie to fintech, having joined her previous employer Pearl Capital only two years ago. But that hasn’t prevented her from making her social media presence known. And while she reserves Facebook for her personal life, if you know Villano then you wouldn’t be surprised at her success on LinkedIn, as she seems to have a knack for social media.

“I felt like I needed a very strong presence in this industry to get anywhere,” Villano told deBanked. “It’s funny, I think a lot of people associate sales with a type A personality and being pushy. I’m not an aggressive, pit-bull woman. You don’t have to be that type of woman to get ahead. I thought about how am I going to show this to the industry? Social media was my answer. My Facebook and LinkedIn attract a lot of views.”

Indeed, it was because of her Facebook profile that Villano was featured by a famous painting by David Uhl. The painting, dubbed Steampunk Seduction, is the first in Uhl’s Steampunk series. “I got that through Facebook,” Villano explained. “Someone saw my profile on Facebook, reached out and said, ‘you should contact the artist.’ I told them they were crazy. They insisted, and he chose me. It’s been a blessing.”

Meanwhile, her LinkedIn posts designed for MCA ISOs have similarly caught on like wildfire, and she only “amped up” her activity on the site in July. Villano has been posting on LinkedIn once per week, and the proof is in the pudding. “Since then, in September, October, and November, we broke funding records every month. It works,” said Villano of her previous employer Pearl Capital.

Underpinning that deal flow has been a flow of new relationships she’s forming, evidenced by more than 500 ISOs having contacted Villano on LinkedIn via her previous employer’s Salesforce network.

“That was from posting one time per month and just educating; not posting pictures of me on a beach sipping a Pina Colada,” said Villano. Instead, she was educating them about Pearl’s funding options, the types of deals they wanted, their bonus structure, etc. “So, it’s very basic information. I was just letting them know what they can expect from Pearl, what kind of fundings we were doing, just being a constant reminder,” she added.

While Villano is no longer employed by Pearl Capital, her posts from her tenure there have had a lasting impact. “[Last month] I put up a post announcing that I was leaving Pearl Capital,” Villano said. “The post generated more than 35,000 views.” Meanwhile, since she’s been posting, she’s seen the number of LinkedIn connections skyrocket.

Villano is continuing her social media push at her new employer, Kalamata Advisors.

“Kalamata has a partnership-culture mentality. It’s an amazing opportunity to be elected a partner, like a partner at Goldman Sachs or McKinsey, here after a couple of years. Then you have a real stake in the company and work at a firm where everyone wants to pitch in,” she explained. “Second is their great reputation. The partners put their mission and values first. They’ve grown so fast; but they’ve grown with the purpose to genuinely help people. And lastly, they’re very respected in the industry. Everyone here is very responsive, honest and professional.”

And while she’s no longer employed by Pearl Capital, she has nothing but respect for her former employer as well. The feeling is mutual, evidenced by a going away party that they threw for her on her way to Kalamata.

Gender Gap

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

The other has to do with the fact that MCA is a male-dominated industry. “Women are more conversationalists through texting or social media. I find women are more intimate with it on a professional level. I have to say that I have the most active social media in our industry,” said Villano, who again only joined fintech two years ago. She’s inspired by the many women who are behind the scenes at ISO shops, many of whom she explained work as processors.

We asked Villano about whether sharing her trade secrets with competitors in the industry made her uncomfortable. “Not at all. I’m not made like that,” she said. “And Kalamata believes trust is the importance of every brand. With transparency, there is trust. Everyone is authentic and unique. Everyone should have the opportunity to share his/her own self in any industry.”

Hard Work, Big Success – The True Story of an MCA Broker

December 15, 2017Sales is a tough field for anyone to break into even if they come from the most ideal of circumstances. At some point, the rubber meets the road for every MCA broker, at which time they must decide whether they’ve got what it takes to make it in this business.

This is what makes Lerry Dore’s story so remarkable, as it seems that the more he got knocked down in life, the higher he was destined to rise. Today he’s employed as an MCA broker at Cresthill Capital. And while education has been paramount to getting him here, evidenced by the fact that during his entire employment he has been in college and he is still one of the funding company’s most successful brokers, Dore more than anything else was trained at the school of hard knocks.

Coming to America

Dore was born in South Florida, but he wouldn’t stay in the United States for long. After his parents split up, his mom was having a tough time making ends meet and made the impossible decision to send him to Haiti to live with extended family.

“My mom had a very hard time supporting us right out of the gate. Soon after I was born, I was sent to Haiti to live with my aunt and cousins,” he said, adding that this gave his mom a chance to get on her feet. “She needed to get a job so that she could provide for us at a basic level.”

Dore would remain in Haiti for the first three years of his life, where his first language would become Haitian Creole. But you wouldn’t detect a hint of an accent talking to him today at the age of 23.

Dore’s mom eventually found a job. She was only earning minimum wage at a hospital, but it was enough to get the wheels in motion to bring her son home.

“She was in a position to provide food, electricity and shelter for us. That’s why I came back,” said Dore, adding that he doesn’t remember much of Haiti with the exception of the plane ride home. “That’s where my memories start,” he said. Perhaps it was somewhere over the Caribbean that young Dore’s dreams began to form.

When he got back to Florida, Dore was able to meet his mom for what felt like the first time for him. He also met his brothers and sisters for the first time ever. He explained how at this point, his mom was still getting adjusted to life in America as an adult immigrant.

“There were a lot of things that I went through as a kid to this point that she couldn’t give me guidance on. She simply didn’t have that experience. That brought a challenge,” he said. Little did he know that these obstacles would help shape him into the resilient person and successful MCA broker he is today.

“There were a lot of things that I went through as a kid to this point that she couldn’t give me guidance on. She simply didn’t have that experience. That brought a challenge,” he said. Little did he know that these obstacles would help shape him into the resilient person and successful MCA broker he is today.

While getting used to the American culture was a challenge, something that his mother never lost sight of was the importance of education. “She was very big into education,” he said. Dore’s mom discovered Head Start, a government subsidized program that provided a pre-school education for families who couldn’t otherwise afford it. That was where it would all begin for Dore, and come hell or high water his mother was going to enroll him. Without the luxury of an air-conditioned vehicle to drive in the hot Florida heat, the pair set off on foot to sign up. Some 12-15 blocks later they arrived.

“Both of us were sweating bullets. She didn’t know it, but there was a small registration fee. At the time, she didn’t have it,” Dore explained. It was then that fate seems to have stepped in in the form of the woman who was handling registration. She pulled the pair aside and told them that after witnessing the dedication that this mother had toward her son, she was going to waive the fee. In return she only asked that they keep it on the down low.

“That small gesture made a dramatic difference in my life,” Dore said. “If I was not able to attend, I wouldn’t start school until I was seven or 10 years’ old. That was a very important moment in my life.”

Indeed, it was, as it would set in motion a series of events that would lead Dore to where he is today, a successful MCA broker at Cresthill Capital. But before he would join the firm, there were still more hardships waiting for him, not the least of which was the death of a friend in his teenage years. “That could have been me,” Dore exclaimed.

For the average person, life’s setbacks could have held them down forever. For Dore, they seem only to have propelled him further. “The reason why I stayed out of trouble was I was in school and my mother kept us grounded,” he said.

During his teenage years, Dore and his family lived in an apartment complex in a neighborhood of immigrant Haitians where he said the median income was $25,000 to $30,000 per year. He shared a room with his brothers and sisters.

“I focused on athletics,” he said, adding: “That’s where I got my competitive nature. Also, my thick skin,” both of which, incidentally, are characteristics that would serve him well as a broker later in life.

While he excelled at basketball at his Boca Raton high school, Dore wouldn’t be able to pursue those dreams for long. He and his family would be uprooted from their home time and time again amid landlord trouble. This series of setbacks, which involved him sleeping on his brother’s couch for a time, instilled a sense of maturity in Dore at a very young age.

He had a few Division II and Division III offers to play basketball in other states, but he turned them down. Instead of chasing his own dreams, Dore decided to focus on business and find a way to sustain and support his family “Once I graduated, I was not interested in basketball. I wanted to finish college,” said Dore, and lucky for the MCA industry he had his sights set on the field of finance.

Funding Merchants

After High School, the first thing that Dore did was to go online and look for a job. As it so happens, the first ad he saw was at a stock brokerage in Boca Raton. “That’s where I started, in phone sales. I didn’t have a Series 7 license at the time. I was just calling from the Yellow Pages. Once I got someone on the phone, I would transfer the call to someone who had a license,” he explained.

This went on for a couple of months until he heard about a startup company in nearby Delray Beach. “At the time, they were prospecting merchants. That’s how I got into the industry,” he said.

His first job in the MCA niche was with a very small ISO shop. But it was there that he would make a connection to change the course of his career. He was working on a deal that was hard to place and was only getting rejections. That is until he came across Mike Daniels, Cresthill’s No. 1 producer.

His first job in the MCA niche was with a very small ISO shop. But it was there that he would make a connection to change the course of his career. He was working on a deal that was hard to place and was only getting rejections. That is until he came across Mike Daniels, Cresthill’s No. 1 producer.

“I couldn’t get the deal done anywhere else. The merchant was getting frustrated with the process. I heard of a company that takes chances on merchants with imperfect credit,” he said. That funder was Cresthill Capital. Little did he know at the time, but they would eventually become his employer.

He sent the merchant file over to Daniels, who then reached out to the merchant and got the deal funded. It was at that point, Dore said, that he started to fall in love with Cresthill “because of how [Daniels] was able to treat the merchant with respect and get the deal done.”

For the next six months, Dore would proceed to trust all of his business with Cresthill. He was still employed by the small ISO shop, but he began to outgrow his environment and long for a platform that allowed him to explore his talent and excel. But his pursuit only left him frustrated and thinking about leaving the MCA industry, something he confided in Cresthill Capital’s Daniels, who was turning into a mentor, about.

It was at this point in his life and career that instead of being the rock, Dore needed to lean on someone else. Daniels and Cresthill Capital were there for him. He was invited in for an interview, and as they say the rest is history.

“I was shocked at how diverse the workforce is. There were different types of people with different backgrounds. I liked it right off the bat. And then everyone was very friendly to me from the moment I walked in,” he said. He was greeted at the front door by Cresthill Capital’s Mike Marano, who then proceeded to interview him.

“I’ve actually interviewed and sat with every single person at my company and hired them personally. What I can say about Lerry is that from the moment I looked at his face and saw his eyes, I knew intuitively that he was a good person. And responsible. I had no idea how deep of a person he was, how much humanity he would show. He was a willing student, and we were happy to teach him. And he continues to soak it up like a sponge,” Marano told deBanked.

“I’ve actually interviewed and sat with every single person at my company and hired them personally. What I can say about Lerry is that from the moment I looked at his face and saw his eyes, I knew intuitively that he was a good person. And responsible. I had no idea how deep of a person he was, how much humanity he would show. He was a willing student, and we were happy to teach him. And he continues to soak it up like a sponge,” Marano told deBanked.

Dore was convinced Cresthill Capital was the right place for him when Marano insisted that Dore stay in school and continue his education. “They said, ‘we will work around your schedule,’ and that really drew me in,” he said, adding that the dog-friendly environment was a bonus.

Dore has been employed by Cresthill Capital for the past 18 months and is graduating from college this week. He is not only supporting himself, but he’s the highest earner in his family, which has allowed him to help support them.

Paying it Forward

As if on cue from the mystery lady that paid his school tuition when he was just a child, Dore is now interested in paying it forward in life. He said that similar to how Cresthill Capital is involved with philanthropy, he’d like to give back to the community. But his vision goes beyond his neighborhood.

“I want to help kids that are similar to me, who are in programs that try to help them excel in this country. I want at some point to work with immigrants that come in from Haiti and work with them to give them a platform, like the lady who gave us a chance,” said Dore.

Since the Haiti earthquake, his extended family has relocated north to Canada. “But I still feel to some degree a responsibility to try and help out the people in that country and the ones who come here through immigration,” he said.

As for Marano, he said all Dore needs to do is exactly what he’s been doing. “When he leaves me, he won’t have to work again. But knowing this kid, he probably will anyway,” Marano said.

Kabbage Crosses $4 Billion in Loans, Taps C-Suite Exec for Intl Expansion

December 6, 2017

Alternative lender Kabbage is exiting 2017 with a bang, having just crossed the $4 billion threshold for loans deployed across more than 130,000 small businesses so far. The latest milestone represents a 30% spike in both total funding and the number of merchants on its platform since April 2017, which is when they celebrated their previous new threshold. Victoria Treyger, chief revenue officer for Kabbage, took some time to talk with deBanked about the latest milestone, international expansion and mobile strategy.

“Our lines of credit and amounts taken continue to increase as we begin serving more and larger small businesses. We see great momentum across all industries in all 50 U.S. states,” Treyger said, adding that the momentum is particularly evident among the restaurant, construction, professional services and automotive industries for funding strategic investments such as new locations, specialty equipment, business expansion, etc. The $4 billion milestone is the result of the company’s direct business in America only.

According to recently released data by Kabbage cited in CrowdFund Insider, nearly three-quarters of 400 small business owners polled are forecasting higher revenues by year-end. More than 50% of those merchants are targeting a jump of at least 10%. Kabbage certainly appears to be benefiting from this optimism and an economy that is functioning on all cylinders. Treyger points to the lender’s “fully automated lending process and unique, live data connections with our customers.”

Fintechs & Banks

The relationship between alternative lenders and banks has been at the forefront, and Kabbage has been involved in some of the most high-profile pairings, evidenced by SoftBank’s famous investment. And while there’s no crystal ball, fintech and bank partnerships are one of the trends that will likely persist in 2018.

“Data will be at the heart of everything, how it’s shared, accessed, applied, protected and given back. Expect to hear more about the personalization of lending and to see stronger partnerships between fintechs and banks,” said Treyger. Consumer data, of course, is the Holy Grail for lenders, with banks having a tendency to keep that information close to the vest. And with the Equifax breach so recent in the rearview mirror, the importance of data security is certainly paramount.

“The CFPB recently published data-sharing guidelines between banks, their customers and financial services they choose to permission their data. Kabbage applauds the CFPB guidelines, small business owners should control how, where and with whom their data is shared to best serve their needs. Security is the primary concern, as it should when handling customers’ data. All entities, from fintechs to data aggregators should be held accountable to the same security standards as banks,” Treyger said.

She also pointed to a mobile push in yet another sign that the industry has turned a corner. “Anticipate greater adoption in mobile lending. Today, approximately 20% of Kabbage’s originations come from mobile. We’re the only provider that allows its customers to apply, qualify and draw funding from a mobile app; we have seen growth and expect to see more in 2018,” she said.

Kabbage’s Global Ambitions

Meanwhile, as Kabbage sets its sights on global expansion, they’ve tapped a C-Suite executive from the consumer goods industry who has held leadership roles across North America, Europe and Asia. Robert Sharpe was tapped for the newly created position of COO at Kabbage. Most recently, Sharpe served as president and COO at National DCP, LLC, a supply chain management company. He has also led CSM Bakery Solutions and Spain’s Campofrio Food Group, serving as chief executive at both companies.

According to the press release: “Sharpe will be responsible for Kabbage’s continued growth and operational oversight as the company expands internationally and scales its services to serve more and larger small businesses.”

As Kabbage readies its 2018 roadmap, notwithstanding its $200 million revolving credit facility with Credit Suisse in November, don’t be surprised to see them revisit the capital markets.

“Continuing to diversify our funding options for small business lending is certainly of interest,” noted Treyger.

Canadian Merchants Show An Appetite For Capital

November 25, 2017In Canada, the average deal size for a merchant is anywhere between $20,000 and $30,000 in funding, depending on who you ask. That’s why when one startup recently funded a $300,000 CAD advance from its balance sheet to a Canadian merchant, the deal turned some heads. While it’s unclear whether this amount could be indicative of a trend unfolding at our neighbors to the North, Canadian small businesses are preparing for some changes in the industry landscape in 2018.

SharpShooter Funding, whose name depicts the famous wrestling move of the WWE’s Bret “The Hitman” Hart, was behind the $300,000 deal with an Eastern Canadian grocer.

If you’re wondering how a merchant funder and WWE legend became partners, chalk it up to a combination of fate and timing. Paul Pitcher, SharpShooter Funding managing partner, has been Hart’s biggest fan since he was a kid. Pitcher got the opportunity to meet his hero when was just 10 years old. It was then that the green shoots of friendship formed, and today the WWE’s Hart is acting commissioner of SharpShooter Funding, having helped to launch the business.

Canadian Merchant Landscape

To get a taste of the Canadian merchant financing landscape, consider that the three top Canadian funders deploy $20 million and $25 million per month combined, explained David Gens, president and chief executive of Merchant Advance Capital, which is included among the top three funders. That’s up from a range of $15 million to $20 million earlier this year.

And while a $300,000 advance may not seem like something to write home about for U.S. funders, it’s a big deal in the Canadian market. The culture among small businesses in the Great White North is different and more conservative than their US counterparts.

“It’s a function of the size of the merchant,” Gens explained. “The typical single-location storefront merchant is going to qualify for $30,000 to $50,000. It takes a larger and more established business, whether it’s a multi-location merchant or a business that is in the B-to-B space, a manufacturer, distributor or wholesaler to be large enough to qualify for large financing.”

Meanwhile there are some changes to small business taxation that are coming down the pike that may influence demand for credit, Gens noted, though the precise shape any changes to the tax law will take remains unclear.

“They will reduce the small business taxation rate on the face of it. But for businesses where they hold cash or need to hold cash, it’s a gray zone as to whether or not they will be able to hold financial assets in those businesses. The government is going after companies that are holding investments. But there’s a gray line as to what is a holding company that is holding an investment and an operating company holding a buffer because of seasonality or cyclical demand. We have yet to see what the rules end up being exactly,” Gens said.

Anatomy of the Deal

In the case of SharpShooter Funding, the grocer merchant originally came to the funder for less than $300,000 but qualified for more, bringing the funder’s tally for a single day’s deals to more than $500,000.

“We never thought we’d hit this milestone in the Canadian market. But the file was right, and the timing was great,” Pitcher told deBanked. Now that they’ve gotten a taste of it, SharpShooter Funding hopes to do more deals of this nature. “For a small funder like us to double the size of a big funder was a big moment for us, especially in the Canadian market,” Pitcher said.

Merchant Advance Capital’s Gens said his company is prepared to take on the risk for deals at even a higher threshold. “Our average is $35,000 to $40,000, and the largest deal we’ve ever done was $600,000. I don’t want to steal their thunder, but there have been larger deals,” said Gens. “A few funders may syndicate when deals get that big, but it’s not an inconceivable size.”

OnDeck, which similarly has Canadian operations, lends up to $250,000 CAD in Canada. OnDeck has extended more than $7 billion in online loans across 70,000-plus customers across the United States, Canada and Australia.

As for SharpShooter Funding, Pitcher said the funder has been on the sidelines for larger deals because they don’t want to grow too fast. He’s been turned off by other funders doing deals within a couple of months of launching and then being forced to close their doors.

“Our capital has always been strong. It’s not that we can’t afford to lend larger amounts. It’s because we want to make sure we’re doing it right from the start,” Pitcher said, adding that SharpShooter Funding has only had its doors open in Canada since June 2015, though its corresponding U.S. business, First Down Funding, has been around since 2012. “It’s been a work in progress, and I love every day of it! We’re only getting started, and I am 100% excited for the future,” he said.

The Canadian grocer reached out to SharpShooter Funding in response to Google advertising. The affiliation with the Bret Hart association didn’t hurt. Pitcher explained there is a seasonality tied to the merchant’s business, evidenced by a couple of months or more each year in which revenue is spotty, that made the grocer unattractive for banks to fund. “That’s why those sized deals are difficult to put out and banks won’t put out, because of seasonality,” Pitcher said.

SharpShooter Funding was not deterred by that. “We were really able to gain in-depth trust and visibility into this merchant from the first call to the last call. There was never a problem with him mixing up stories. Just the honest truth. From his references to his landlord, everyone involved made it clear he was here to work with us and not to play games,” Pitcher said.

Pitcher was impressed by the business owner’s work ethic. “He’s a roll-up-your-sleeves entrepreneur who didn’t borrow $1 million from his father. No bank loans. Six years ago, he rolled up his sleeves and made it work. Now he’s in a situation where banks won’t lend to him. But we will,” he said.

The merchant’s bank statements also made sense to the funder given their consistency, predictability and transparency. “Whenever we ask for finances from someone and that merchant can get them to us in an organized fashion in less than an hour, it speaks wonders. It means they’re honest and ready to play ball. And that’s what we want,” Pitcher exclaimed.

The merchant plans to use the capital for an expansion into a new food product line. If he pays off the advance early the funder will lower the rate.

Kabbage Taps Debt Capital Markets for a Cool $200 Mil

November 16, 2017 Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

With the Credit Suisse deal, the tally for Kabbage’s debt funding capacity reaches $750 million. “The new revolving credit facility will be issued by Kabbage Asset Funding 2017-A LLC, a wholly owned subsidiary of Kabbage Inc,” according to a press release.

Kabbage expects the credit facility will help them to scale faster. They plan to use the credit to add bigger small businesses to its client roster as well as extend higher lines of credit with longer durations.

“The new revolving credit facility with Credit Suisse is a debt round. Those funds are for our small business customers, and will be used to continue to provide them with easy access to working capital,” Deepesh Jain, Kabbage Head of Capital Markets, told deBanked.

It’s Kabbage’s maiden credit facility to be rated by credit rating agency DBRS. “The top two classes of the multi-class transaction earned investment-grade ratings of ‘A’ and ‘BBB’ and are collateralized entirely with assets originated through Kabbage’s fully-automated underwriting technology,” according to the press release.

Jain told deBanked the DRBS rating is highly significant. “It strongly demonstrates the proven success of Kabbage’s fully-automated platform and its data-driven risk analysis for small business lending. It speaks to the company’s leading position in the SMB-lending marketplace and Wall Street’s confidence in Kabbage,” he noted.

As Jain pointed out, Credit Suisse has been an early supporter of fintech. Indeed, the Swiss bank a year ago similarly provided a $200 million asset-backed revolving credit facility to another alternative funder, OnDeck.

Alternative Funders and Bank Partnerships in the Spotlight

Jain declined to comment on whether Credit Suisse might be interested in Kabbage’s lending platform for its own use. Alternative funder and banking partnerships were recently thrust into the spotlight with a lawsuit filed by a Massachusetts-based small business owner against Kabbage and Celtic Bank, which have had a partnership for at least several years.

The lawsuit alleges that the funding model of the defendants “was designed to evade usury laws,” according to The National Law Review. Apparently, the plaintiffs, which are listed in the public filing as Alice Indelicato and NRO Boston, had several small business loans and now accuse Kabbage of “renting” Celtic’s bank charter. Jain declined to comment on the lawsuit and the plaintiffs couldn’t be reached.

Capital Markets Pipeline

Meanwhile, at the rate they are going, we could see Kabbage tap the capital markets again in 2018. “Capital markets are something we will continue to explore to further diversify our funding options,” said Jain.

The Bad Broker And Merchant Due Diligence

November 15, 2017 There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

deBanked was contacted by a victim of the fraud, Noah Grayson, managing director and founder of Encino, Calif.-based South End Capital. Grayson said the real victims are the merchants who get taken advantage of by these scams. In this case it was a New York-based small business owner who took on too many MCAs.

Grayson is quick to point out the MCAs were not at fault and each may have even thought they were the first position funder since it all unfolded so quickly. “They’re just trying to do business and provide financing to businesses, and they got burned as well. They’re going to take some degree of financial loss because of this and maybe more,” Grayson said.

False Pretenses

When Grayson reviewed an email that he received from the borrower, which included a copy of the LOI, he knew immediately that it was fraudulent and the borrower had been misled. “It was a fraudulent LOI and we had no record of the borrower or the brokers who provided it in our system,” Grayson exclaimed.

As it turns out, the borrower was tricked by the fake LOI that sought to leverage the reputation of South End Capital’s brand to coerce him into taking out $260,000 of MCAs from four separate funders. They did it under the false pretense that South End Capital would then consolidate those positions in 10 days and extend as much as $900,000 more in working capital to grow the business.

To be clear, South End Capital does offer a genuine MCA consolidation loan program. Grayson had never agreed to consolidate the business owner’s MCA positions, however, or provide an additional $900,000. That part was fabricated. This left the merchant holding the bag for more than a quarter of a million dollars in MCAs, placing his business, which has been successful since the 1960s, on the brink of bankruptcy protection in the interim because of the crippling weekly payments.

Fraud Prevention

Andi McNeal, research director at the Association of Certified Fraud Examiners, or ACFE, said she has seen this before, only on the consumer side of the industry. “Loan consolidation fraud for credit card debt is very common in the consumer space, and it’s not surprising to know that similar schemes are popping up in the small business space, too,” she said.

She went onto explain that because a small business is typically run by a small management team who typically aren’t trained in fraud prevention, they often adopt the same mindset as they do in personal finances. They don’t always have the necessary checks and balances in place, which can place them at risk of being victimized by such schemes.

“Sometimes they’re not savvy enough to detect those types of scams coming at them,” she noted. “Certainly, big businesses can fall prey to this, but it’s less common.”

Staying on Defense

The recent saga unfolded over a period of six weeks. Meanwhile Grayson has outlined some red flags for small businesses to watch out for to prevent becoming the next victim to a new fraud.

“If what you’re being told seems suspicious or doesn’t make sense, question it. Ask questions and get more information,” said Grayson.

Another rule of thumb is to stick to the document in front of them. Again, this may just be a case of a few bad apples spoiling the bunch, but sometimes brokers tell small businesses something contrary to what appears in front of them on the official document. “The LOI spells it out,” said Grayson, adding that when in doubt the borrower should defer to the document.

The merchant should also take it upon themselves to call the lender whose name is on the LOI to verify its authenticity before signing it or providing any upfront fees.

“In this case, it was a fraudulent document and it didn’t help out the borrower but calling us to confirm it initially would have. Most of the time, looking at what’s written out on paper from the verified source will help and getting a verbal or email confirmation from the actual lender, certainly will,” Grayson said.

Another defensive step merchants can take is to simply review the website of the brokers and funders and look for names, press releases and past closings, details which Grayson noted were all missing from the broker in question’s site.

“Anybody can say they make loans and provide financing. They could tomorrow put up a website for a couple bucks and say they’re a lender and start taking applications. But just because there’s a website doesn’t mean they’re legitimate,” Grayson said.

He’s suggesting merchants check out the names of the principals and employees on the site. Google is their friend to check for any history of loans closing. Look for closing announcements and any complaints tied to the entity in question. Call the Secretary of State Department and inquire about any complaints.

At the end of the day, it comes down to the merchant doing their homework. “A lot is on him. He should have done more research, absolutely. But anybody can be coerced or tricked if the right things are said,” said Grayson.

If a merchant does find themselves in a situation where they fall victim to a fraud, there are steps they should take. McNeal said that while each situation is unique, a good first step is always going to be to reach out to a trusted legal counsel.

“They can help guide you through the process of what the options are. Do you have recourse? Does the situation call for insurance to help cover the losses? They also can advise on which law enforcement or government agencies are the most helpful – should the case be referred to the local authorities or do they need to bring in the FBI,” the ACFE’s McNeal advised.

More Pervasive

Grayson’s fear is that this is not an isolated incident. He has reason to be cynical, as this was the second incident this year resembling the most recent situation that they have experienced.

The first incident was relayed to South End Capital by a handful of borrowers about one specific MCA broker. No fraudulent documents were ever recovered, but the borrowers recalled the harrowing details of the incident

“Per the multiple borrowers, the broker used our real LOIs and lied to borrowers about how to interpret them to coerce tens of thousands of dollars in upfront fees from them. For example, for an LOI we issued for our SBA loan program that listed what SBA guarantee fees would be due at closing, he would convince them that that fee was his and they needed to pay it to him upfront to proceed,” Grayson explained.

The small business owner at the center of the scandal declined to comment, and it’s unclear whether they were the one to initiate the original communication with the broker or vice versa.

From Ineligible to 0% APR – Los Angeles Company Monetizes Startup Leads, Combats Stacking

November 10, 2017 Merchants have no shortage of options when it comes to accessing funding in today’s climate. And while MCAs and loan products have become more pervasive, one company’s solution is to reintroduce traditional financing in a strategic manner. Seek Business Capital finds credit card offers and credit lines for the credit-worthy who may not be eligible or ideally suited for a business loan.

Merchants have no shortage of options when it comes to accessing funding in today’s climate. And while MCAs and loan products have become more pervasive, one company’s solution is to reintroduce traditional financing in a strategic manner. Seek Business Capital finds credit card offers and credit lines for the credit-worthy who may not be eligible or ideally suited for a business loan.

Roy Ferman is an Australia transplant who runs the company out of the Los Angeles headquarters, miles from the usual domicile for alternative funders of Silicon Valley, New York and Austin.

“We liked LA from a perspective of the sunshine, but we also like being away from the rest of the funding industry. It gives us the ability to put our heads down and focus on what we’re doing and not worry about what anybody else is doing,” Ferman told deBanked.

Seek Business Capital partners with MCAs and brokers on leads and recently expanded with a new hire in New York. Kunal Bhasin joined the company over the summer as vice president of business development. “We were traveling out there to meet with partners and doing redeye flights. Now someone is on the ground there training partners on how to better find opportunities to use our product,” Ferman said.

Basically, the company tells MCAs and brokers that the startup leads (those that are trying to start a business or have just started one), to send those deals to Seek Capital, instead of throwing them in the trash.

They recently adopted a fully automated underwriting product that delivers an instant decision for merchants though there’s an element of the human touch on the services side of the transaction.

“For us, the biggest driver is FICO. We take someone with a good FICO score but just started their business and we are still able to offer this person funding,” said Ferman, adding that the sweet spot is a credit score of 680 or higher. “Cash flow is always going to be a factor. For us, we’re predominantly based on FICO. Even still, FICO is one thing. That’s the body of the car. Sometimes we want to look under the hood and see what’s really going on,” said Ferman.

Economic Indicator

Seek Business Capital is industry agnostic though some of the more common sectors they work with are retail, restaurants and trucking. “What’s really interesting is we get a little bit of a sneak peek into emerging industries and local economies,” Ferman said.

For instance, when cannabis was legalized for recreational use in Colorado, they saw a spike in demand from “peripheral businesses” such as contractors that were building out the storefronts, security companies and restaurants amid a rise in tourism to the area.

A similar boom is expected in California when cannabis for recreational use becomes legal in the state in 2018 via Prop 64.

Zach Lazarus, CEO of San Diego-based A Green Alternative, a cannabis dispensary and delivery service, said: “You name it, it’s going up in California right now,” in response to Prop 64. He added there are desert towns and farm communities looking to embrace the boom, which he compares to the gold rush of 1849.

Zach Lazarus, CEO of San Diego-based A Green Alternative, a cannabis dispensary and delivery service, said: “You name it, it’s going up in California right now,” in response to Prop 64. He added there are desert towns and farm communities looking to embrace the boom, which he compares to the gold rush of 1849.

“It’s the service providers, architects, contractors, all these different niche needs are the people who are really going to benefit from the boom,” Lazarus said. Contractors especially need access to capital right away; they don’t generally get fully compensated until once the job is complete, and they need to purchase materials in the interim.

Lazarus said banks won’t loan to cannabis businesses and in his experience other lenders have been predatory in nature. He may just not have come across the right funder yet.

Anti-Stacking Tool

One of the problems that Seek Business Capital seeks to solve is that of merchants taking on too many positions. “We found two ways to provide our services. Our bread and butter and our historical performance has always been in startup funding. We’ve evolved to move more upstream with lenders and we’ve become an anti-stacking tool, if you will,” Ferman noted.

The problem with stacking is that it can put a major strain on the cash flow of the merchant and it put the first position funder at additional risk than what they originally agreed to underwrite.

“We offer 0% for the first 12 months. It’s very advantageous and we’re not crushing cash flow. We view it as an anti-stacking tool. There are few lenders and ISOs who use it, taking both our credit card position and the original term loan but protecting the merchant. The merchant gets all the money they need so they’re not interested in stacking,” said Ferman.

Seek Business Capital charges merchants a success fee of 9.9% of whatever funding they receive for them. Payment is made once the small business receives their funding and the merchant will typically choose to pay Seek Business Capital with the capital they receive from the credit extended to them.

Now they’re taking things to the next level with a data product that they plan to license to third party credit aggregators next quarter.

“We’ve seen everything from the credit profile, to income, to the approval rate, the approval score and the amount. We’ve taken all that data and analyzed $150 million worth of credit card approvals for big clients. We now have a strong indicator of which profile is going to get approved from which bank and how much,” Ferman explained.

A customer submits their details into Seek Business Capital’s decision engine, which generates an estimated approval or decline rate in real time. For instance, they might see that their approval likelihood is 25% for one card and 86% for another along with the estimated approval amount. It’s a soft credit pull so customers don’t have to worry about harming their credit. In addition to the decision engine there’s a recommendation engine that makes credit card suggestions to merchants.

Ferman said the biggest competition the company faces is a potential customer taking out a home equity line, dip into their 401(k) or borrow from friends and family.