Articles by deBanked Staff

Tiny Small Businesses Struggle More Than the Rest

March 28, 2019 The average credit score of the owner of a “mom and pop” shop (a business with four or fewer employees) is 30 points lower than the owner of a larger business, according to a recent study conducted by Lendio. (Lendio defined a “mom and pop” business and having four or fewer employees). Furthermore, the study says that, on average, mom and pop businesses require twice as many interactions with a lending expert, compared to larger small businesses. This is likely because of problems with credit and other financial challenges.

The average credit score of the owner of a “mom and pop” shop (a business with four or fewer employees) is 30 points lower than the owner of a larger business, according to a recent study conducted by Lendio. (Lendio defined a “mom and pop” business and having four or fewer employees). Furthermore, the study says that, on average, mom and pop businesses require twice as many interactions with a lending expert, compared to larger small businesses. This is likely because of problems with credit and other financial challenges.

Smaller mom and pop businesses are in greater need of capital, according to the study. These businesses represent 53% of the customers funded through Lendio’s online marketplace. And their loans account for 34% of the total loan volume funded, even though the average size of their loans is smaller. The average loan amount for a “mom and pop” business is less than half that of larger businesses. Specifically, the average loan amount for “mom and pop” businesses is $23,081, while the average loan amount for larger small businesses is $54,188. Of course, a larger company with greater sales can afford to borrow more. But the $54,188 average loan size for larger companies may be a smaller percentage of revenue for those larger companies.

Speaking of revenue, mom and pop businesses’ monthly revenues are on average $35,000 less than their non-mom and pop small business counterparts. The smaller mom and pop shops are also generally younger, according to the Lendio study. Their average time in business is 5.6 years compared to 7.4 years for the larger small businesses.

What Did Direct Lending Investments Invest In?

March 27, 2019 When Bloomberg News reported that Direct Lending Investments (DLI) had lost approximately 25% of its portfolio value from a deal gone bad, some were surprised to learn that it had nothing to do with its core competency of online lending. VOIP Guardian Partners I, which stuck DLI with more than $190 million in unpaid loans, was in the business of lending money to smaller telecoms against their accounts receivables, Bloomberg News reported. VOIP was then supposed to be repaid the money when larger telecom companies paid the smaller ones.

When Bloomberg News reported that Direct Lending Investments (DLI) had lost approximately 25% of its portfolio value from a deal gone bad, some were surprised to learn that it had nothing to do with its core competency of online lending. VOIP Guardian Partners I, which stuck DLI with more than $190 million in unpaid loans, was in the business of lending money to smaller telecoms against their accounts receivables, Bloomberg News reported. VOIP was then supposed to be repaid the money when larger telecom companies paid the smaller ones.

On March 11, VOIP filed for Chapter 7, and limited details behind these telecom borrowers became public.

VOIP’s largest loan default was to a Hong Kong-based company formed in 2015 named Telacme, Ltd. Records indicate that $1 billion overall had been loaned to Telacme through 30-day rolling advances but that they stopped making payments in October 2018, leaving a remaining balance to VOIP and in turn to DLI, of $101.1 million. Telacme’s official website no longer exists and only a holding page by Godaddy indicating that the page has been parked free remains. (Update 4/16/19 – The website has been restored)

The second largest default at $58 million was to a company named Najd Technologies, Ltd, headquartered in the United Arab Emirates. Like Telacme, Najd stopped paying in October 2018 and their website is also no longer accessible. Internet archives show it advertised itself as a global telecom company based in Bangkok, Thailand.

The other remaining telecom loan issues spanned companies all across Europe.

A lawsuit filed against DLI in 2017 complained that DLI falsely represented to investors that it typically made loans that ranged between $5,000 and $100,000 when in fact DLI had been financing multi-million dollar telecom deals as far back as 2014. The plaintiffs went so far as to claim that at one point up to 50% of DLI’s portfolio was invested in telecom receivables.

But the claims were removed in a subsequent amended version of the lawsuit after the judge ordered them stricken because the plaintiffs themselves were not aggrieved investors, but instead unhappy former business partners alleging violations of a non-compete.

“I don’t understand why it’s in the complaint,” the judge said. “Particularly, when [DLI] says it is impacting their ability to raise money.”

The decision was prescient as DLI would not only go on to raise more money but also lose more than $190 million of investor money in telecom deals that weren’t overtly advertised.

A March 2017 DLI investor presentation obtained by deBanked touts its focus on underserved Main Street USA businesses. There is no mention of international telecom lending, nor any plans to finance telecom businesses for hundreds of millions of dollars, let alone do so in the Middle East, Asia, and Europe.

In VOIP’s bankruptcy filing, DLI is the primary secured creditor. DLI’s chief executive recently resigned and the fund has been sued by the Securities & Exchange Commission for issues unrelated to VOIP and is being placed under receivership.

The 2017 lawsuit against DLI and VOIP can be found under Index #650973/2017 In the New York Supreme Court.

Yalber Announces $20 Million Credit Facility

March 26, 2019

Yalber announced today that they have obtained a new $20 million credit facility from Park Cities Asset Management. Brean Capital served as exclusive financial advisor to Yalber on the transaction. This follows an earlier $20 million credit facility in December 2018 from a different investment fund.

“The small business funding space has drastically changed in the past two years,” said Yalber CEO Amir Landsman. “We see more and more sophisticated players in the space and to me, it’s a sign that the industry is on the right track to be the major funding source of businesses in America. Being able to close two facilities within 15 months is strong evidence that Yalber has a lot to offer.”

Yalber provides American small businesses with royalty-based investments. They can fund small businesses with up to $500,000. Founded in 2007, the company is an early player in the alternative lending space and is unique in that it generates 90 percent of its business in-house. Less than 10 percent of their leads come from ISOs, although they do look to build relationships with high quality ISOs, according to Yalber COO Amotz Segal.

Segal said that, aside from business with ISOs, all of their marketing efforts are internal and span from social media to local advertising on radio, TV and in newspapers. Yalber does not use direct mail and does not pay for leads.

“It makes the job for our salespeople a little easier because they’re not making cold calls,” Segal told deBanked. “We [mostly] get incoming calls.”

As of the beginning of last year, Yalber had funded more than 5,000 business with over $300 million, and Segal said that they had funded approximately $65 million in 2018. On the subject of regulation, Segal said that they remain very aware of regulatory changes and they don’t necessarily see regulations as a negative thing.

Headquartered in New York, Yalber employs about 25 people and has two very small offices in Dallas and Los Angeles.

Direct Lending Investments Charged With Fraud by the SEC

March 25, 2019 Update: DLI has agreed to the appointment of a receiver to marshal and preserve the assets of Direct Lending and the funds. The SEC has also published a press release on the matter.

Update: DLI has agreed to the appointment of a receiver to marshal and preserve the assets of Direct Lending and the funds. The SEC has also published a press release on the matter.

One of the biggest online lending hedge funds has been accused of fraud by the SEC. On Friday, the SEC sued Direct Lending Investments (DLI) with perpetrating a multi-year fraud that misrepresented the value of loans in a segment of its portfolio.

A DLI employee told the SEC that CEO Brendan Ross helped engineer loans to be valued at par when they should’ve been valued at zero. Emails between Ross and the online loan platform suggest that this was intentional, the SEC argued. The effect of this was that between 2014 and 2017, DLI overstated the valuation of one of its loan portfolio positions by approximately $53 million and misrepresented the fund’s performance by about 2-3% annually.

The SEC seeks a preliminary injunction and appointment of a permanent receiver; permanent injunctions; disgorgement with prejudgment interest, and civil penalties.

You can download the full SEC complaint here.

Below: DLI’s stated monthly returns 2013-2016

A 2017 DLI investor presentation touted “double-digit returns with no down months since inception” and a portfolio that has “exhibited little volatility.”

New Jersey Bill Seeks to Eliminate Quick Easy Access to Small Business Loans

March 21, 2019 The speed at which a small business owner can access capital to grow and create jobs in New Jersey is too dangerous and must be stopped. This is the takeaway from a bill (S3617) proposed by New Jersey State Senator Nellie Pou that calls for a minimum 3-day waiting period between when contract terms are disclosed to an applicant and when they can actually go through with getting a business loan or merchant cash advance. If the transaction does not fund within 10 days of the terms being disclosed, it implies that the waiting process must start over if the applicant wishes to still go forward.

The speed at which a small business owner can access capital to grow and create jobs in New Jersey is too dangerous and must be stopped. This is the takeaway from a bill (S3617) proposed by New Jersey State Senator Nellie Pou that calls for a minimum 3-day waiting period between when contract terms are disclosed to an applicant and when they can actually go through with getting a business loan or merchant cash advance. If the transaction does not fund within 10 days of the terms being disclosed, it implies that the waiting process must start over if the applicant wishes to still go forward.

The motivation behind the bill is to presumably force small business owners to think about the terms for awhile. It would apply where the payment frequency is greater than bi-weekly or the maturity is less than two years. There’s other little caveats too. If it passed, funding small businesses same-day or next-day would effectively become illegal.

In addition, the bill calls for detailed contract disclosures, proof that the funds will be used to economically benefit the small business applicant, lenders to set up their own complaint departments, licensing, bonding requirements for brokers & lenders, a minimum net worth for a broker of $100,000, background checks, written examinations, and ethics classes as part of continuing required education.

Pou’s bill, which at this point has not had the opportunity to get traction yet, is separate from another bill, S2262, which in addition to disclosures, calls for merchant cash advances to be defined as loans in the state. S2262 passed the Senate in February and is now under consideration in the Assembly.

Direct Lending Fund CEO Resigns, Investigation

March 20, 2019

Direct Lending Fund CEO Brendan Ross, has resigned, according to Bloomberg News and numerous individuals identifying themselves as investors on an industry blog. The fund not only lost nearly 25% of its portfolio in a single sour investment, but it’s reported that they may have overvalued its investments in QuarterSpot’s small business loan platform.

The fund was reputed as one of the largest funds in the online lending industry and one that “historically earned investors unlevered double digit returns” by investing in online loan marketplaces.

Were there signs of problems?

In a tell-all book published by DealStruck founder Ethan Senturia in late 2017, Senturia describes how Ross’s fund had been overly dependent on his company’s success. “I am like, literally staring over the edge. My life is over,” Senturia quotes Ross as saying in Unwound when he became aware of DealStruck’s downward spiral*. Despite this characterization, Ross’s fund continued to grow relatively unscathed.

Meanwhile, James R. (“Jim”) Hedges, IV wrote an op-ed in Mid-2017 on Lend Academy of a mystery fund he refused to identify that had a Bernie Madoff-feel to it. In the comments, users point out that the monthly returns matched the ones on Direct Lending’s investor letters.

“When I first saw these returns, I instinctively thought of Madoff,” Hedges wrote. “The narrow band of returns is, in my experience, highly unusual and inconsistent with the returns of investments being marked-to-market. To be clear, I am not saying that this fund is a fraud. I am stating that the performance they’ve reported is, in my experience, unlikely indicative of a valuation methodology that accurately reflects the month-to-month performance of the underlying assets.”

*DealStruck announced a restructuring in December 2018

Business Loan Brokers Indicted

March 16, 2019 Five business loan brokers were named in a federal indictment in Ohio for defrauding a 69-year-old business owner out of his money and cars. In addition to being asked for hundreds of thousands of dollars in upfront fees to apply for the loan, the victim signed over the title of 55 vehicles to a broker to serve as the collateral. The vehicles included a Ford Mustang, several dump trucks, several tractors, several restored classic vehicles, a Freightliner motor home, and trailers.

Five business loan brokers were named in a federal indictment in Ohio for defrauding a 69-year-old business owner out of his money and cars. In addition to being asked for hundreds of thousands of dollars in upfront fees to apply for the loan, the victim signed over the title of 55 vehicles to a broker to serve as the collateral. The vehicles included a Ford Mustang, several dump trucks, several tractors, several restored classic vehicles, a Freightliner motor home, and trailers.

In reality, there was no loan.

Text messages quoted in the indictment indicated that one of the defendants traveled from New York to Youngstown, Ohio by Greyhound Bus to begin driving the vehicles back to New York one-by-one, but their scheme faced challenges when they could not afford the gas to drive all of the cars. By the end, the victim was cooperating with the police and one of the defendants was lured back to Ohio in September to pick up a payment where he was then arrested.

deBanked discovered a message board post that appears to be published by one of the defendants months after the alleged crime. In it, she attempts to recruit other brokers to send her business with promises of high commissions, same day approvals, free leads, and a policy of no backdooring.

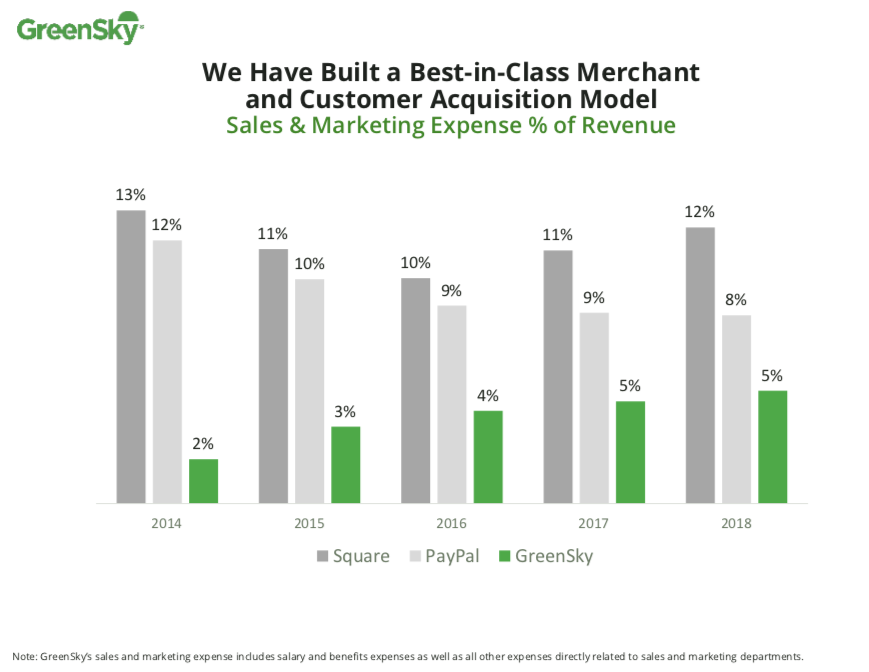

Acquisition Costs Compared for GreenSky, Square, PayPal, OnDeck, Lending Club, and Prosper

March 5, 2019 Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

deBanked examined three additional fintech lending companies and ranked them as follows:

| Company Name | 2018 Sales & Marketing Ratio | 2017 |

| GreenSky | 5% | 5% |

| PayPal | 8% | 9% |

| OnDeck | 11% | 15% |

| Square | 12% | 11% |

| Lending Club | 39% | 40% |

| Prosper Marketplace | 76%* | 72% |

*indicates an estimate

The closeness between Square and OnDeck is notable in that Square markets its payment services first and then offers loans (and other products) as an add-on, while OnDeck only offers loans. Despite that, sales & marketing as a percentage of revenue are still virtually the same for each of them. Square is outspending OnDeck on marketing by more than 10:1, however, and is on pace to surpass OnDeck’s annual loan volume.

Prosper, meanwhile, is doing just as poorly as its wacky ratio looks. The company is losing tens of millions of dollars a year with no end in sight.