Related Headlines

| 12/11/2023 | Cross River: $150M facility to Best Egg |

| 01/03/2019 | Best Egg, SuperMoney strategic partners |

| 04/11/2018 | Best Egg exceeds $5B in loans |

| 04/09/2018 | Best Egg exceeds $5B |

Stories

Best Egg Exceeds $5 Billion in Loans

April 11, 2018 Now four years old, the consumer-lending platform Best Egg has delivered more than $5 billion in personal loans. The Wilmington, DE-based lender does not offer business loans. However, Best Egg CEO Jeffrey Meiler told deBanked that they are increasingly making loans to people who are self-employed.

Now four years old, the consumer-lending platform Best Egg has delivered more than $5 billion in personal loans. The Wilmington, DE-based lender does not offer business loans. However, Best Egg CEO Jeffrey Meiler told deBanked that they are increasingly making loans to people who are self-employed.

“Structurally, one of the things that has really been a tailwind to this industry is the whole move to the gig economy and people having income that is less regular,” Meiler said. “It has increased demand for what we provide.”

Meiler is referring to, among others, freelancers, who are essentially one-person businesses. Best Egg specializes in personal loans with repayment periods of either 36 or 60 months. Some loans are used for large purchases while the majority are used for consolidating debt or refinancing.

“We mostly cater to people who want to get out of debt,” Meiler said.

Best Egg does all of its marketing internally and has 280 employees.

Meet the CAFE That Can Accelerate Your Fintech Startup

October 14, 2024 Newer fintechs on a mission to advance financial health and wellness for low-to-moderate income individuals and underserved populations may not have to weather the startup journey alone. Inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus, is the non-profit Center for Advancing Financial Equity (CAFE). Supported by numerous partnerships including the Small Business Administration, Discover, the Small Business Development Center (SBDC), the American Bankers Association, and more, one of its signature initiatives is its bi-annual fintech accelerator, which aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort of the accelerator. One of those selected this past Spring, Parlay, offers a powerful tool to improve small business loan applications. Another, Stratyfy, offers interpretable AI solutions that enable financial institutions to make more accurate, efficient, and fair financial decisions in credit risk, fraud, and compliance.

Newer fintechs on a mission to advance financial health and wellness for low-to-moderate income individuals and underserved populations may not have to weather the startup journey alone. Inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus, is the non-profit Center for Advancing Financial Equity (CAFE). Supported by numerous partnerships including the Small Business Administration, Discover, the Small Business Development Center (SBDC), the American Bankers Association, and more, one of its signature initiatives is its bi-annual fintech accelerator, which aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort of the accelerator. One of those selected this past Spring, Parlay, offers a powerful tool to improve small business loan applications. Another, Stratyfy, offers interpretable AI solutions that enable financial institutions to make more accurate, efficient, and fair financial decisions in credit risk, fraud, and compliance.

Being accepted into CAFE requires a startup to already be up and operating.

“[These companies are] in market, the products are built already,” said Kristen Castell, Managing Director of CAFE. “They do have some customers, some of them are enterprise customers like banks, a full time team, and many of them have raised money already.”

Castell tells deBanked that the companies applying to the accelerator still need a lot of help in terms of making industry connections, scaling distribution, and developing the right partnerships. It’s an eight-week program, some of which takes place on location at the Fintech Innovation Hub in Delaware. The rest is virtual. Applicants and those selected can be from anywhere in the US. The founders, all connected by some level of common interest, are bound to form a bond throughout the unique experience. Last week for example, the members of the Fall cohort went on a field trip to the Wilmington, Delaware headquarters of Best Egg (F/K/A Marlette), an online lender, and got to learn about their path from being a startup in 2014 to the fintech stalwart they are today.

“This time, we have some opportunities to meet the American Bankers Association in Washington, DC,” Castell said. “We also meet the regulators at CFPB in Washington, DC. There’s some other conference opportunities like another accelerator called RevTech Labs that has an investor conference in Charlotte. So there’s an opportunity to pitch there to investors.”

The learning curve for any company coming through the accelerator is dramatically shortened by the access and guidance they get, whether that be from other fintechs, from bankers, from regulators, or the largest fintech trade association, the American Fintech Council.

At the end of it all there’s a demo day in person at the Fintech Innovation Hub in Delaware, where they present to investors, bankers, academics, industry and community leaders, non-profit organizations and entrepreneurs alike to show what they’re made of.

Castell, a former banker herself that previously worked for JPMorgan and BlackRock, also experienced a taste of being a fintech entrepreneur when she became interested in impact investing. It’s a scene she loves. When the plan for CAFE was in development, the opportunity to be involved with financial inclusion, technology, and startups all in one was something she really wanted to take on.

“It’s really been an incredible opportunity to build the organization, to build the program, to work with all these partners, to bring all these stakeholders that I had mentioned earlier in and we’re not done,” she said. “We’re just getting started.”

The six members of the Fall cohort are Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm. Sponsors include the American Bankers Association (ABA), Siegfried Advisory, Delaware Prosperity Partnership (DPP), Wolf & Co, Delaware Tech Park, deBanked, and Discover Financial Services.

deBanked is expected to attend the demo day in November.

Cross River Bank Raises $100 Million

December 11, 2018Cross River Bank, which provides banking services to fintech companies, announced last week the completion of a funding round of roughly $100 million. This was comprised of a $75 million equity investment from KKR, along with capital from Andreessen Horowitz, Battery Ventures, Rabbit Capital, and funding from new investors CredEase and Lion Tree. This adds to a $28 million raise a little over two years ago.

Cross River, which originated more than $5 billion in loans as of the end of August 2018, has developed partnerships with fintech leaders to build fully compliant and integrated products within the lending marketplace and payment processing spaces. They have about 15 lending platform partners, including fintech clients Affirm, Best Egg, RocketLoans, Coinbase and TransferWise.

According to the announcement, this new capital will be used to allow Cross River to continue building a complete banking platform where fintech companies can leverage best-in-class banking technology coupled with compliance.

“Cross River offers solutions to fintech companies by giving them access to a full suite of banking solutions and services in a single, fully compliant and innovative platform, making it an increasingly attractive and valuable franchise in a dynamic marketplace,” said Dan Pietrzak, Member and Co-Head of Private Credit at KKR, Cross River’s leading investor.

According to its website, Cross River was named “most innovative bank” by LendIt in 2017 and 2018. Founded in 2008, the Fort Lee, NJ, business-oriented bank has more than 180 employees.

Marlette Closes Proprietary Securitization Deal Worth $205 Million

August 3, 2016After a personal-loan bond sale last month, marketplace lender Marlette Funding closed its first proprietary securitization worth $205 million. “MFT” consists of Best Egg collateral financed via three classes of Notes and one class of Certificates.

Best Egg is Marlette’s personal loan platform with $2 billion in originations since 2014. This transaction, done through Goldman Sachs was the second securitization of unsecured consumer loans originated by Cross River Bank on the platform. In July, Marlette securitized personal loan bonds worth $180 million in Single A notes rated by Kroll Rating Agency.

This news comes at a time as online lenders and marketplaces alike feel the need to diversify sources of capital. “Accessing the securitization markets represents the third major component of a diversified funding plan, which also includes building strong relationships with institutional investors and developing on-balance sheet asset backed credit facilities,” said Paul Ricci, CFO of Marlette Funding.

5 Tips for Better MCA Collections

February 3, 2023Shaya Gorkin is an experienced attorney and the COO of Monetaria Group, a premier collections agency specializing in merchant cash advance and commercial debt recovery. To connect with Shaya, email shaya@merelcorp.com.

With the benefit of our collective decade of experience working in collections for the merchant cash advance industry, our team at Monetaria Group has come to understand all too well the importance of recovering funds for our clients and all the difficulties associated with that. The MCA sector poses distinct obstacles and challenges for collections; but, by implementing the correct systems and strategies, we’ve found that outstanding payments be recovered, without it having to be a painful and drawn-out experience.

Here are five key strategies for better MCA collections that we have implemented with our clients, that can help you too:

1. Be familiar with the industry you’re being asked to advance.

Often, MCA companies offer small businesses short-term funding in their moments of need. This means that the funders are betting on the business’s ability to take advantage of the opportunity being offered to them and turn the ship around, enabling them to repay the advance without any complications or issues.

To ensure you are giving your company the best chance of getting its money back, it is essential for funders to have an understanding of the industry and the businesses they are working with to be able to evaluate their advance worthiness and anticipate fluctuations in repayment ability.

2. Establish relationships and overcommunicate.

Having strong relationships goes a long way in MCA collections, for both the funders and their clients. Establishing trust and open communication with clients will inevitably lead to a better understanding of their specific needs and challenges. Additionally, it goes without saying that developing positive customer relationships can lead to more successful negotiations and repayment agreements.

3. Be proactive and offer solutions.

Instead of passively waiting for merchants to default, proactively reach out to them to check in and see if it’s time to discuss reconciliation and other solutions. This shows a willingness to work with them and allows for potential issues to be addressed before they become major problems.

4. Utilize the best available technology.

Over the past decade, the merchant cash advance space has seen an explosion in the creation CRMs and softwares to service and assist the MCA businesses. Utilizing these technologies will greatly improve the efficiency and effectiveness of your business and will be a great asset in ensuring you are collecting all that is owed to you. Look for the services that offer the features you need, such as custom reports, client breakdowns, automated payment reminders, online portals for customers to make payments, and data analytics- they are all out there ready to assist you.

5. Have a contingency plan.

Despite your best efforts, some merchants will still default. Having a well-crafted contingency plan in place that doesn’t put all your eggs in one basket will minimize the potential negative impact on your business. This includes doing a very thorough underwriting of the merchant’s business. Additionally, be prepared to explore your options in terms of collecting what is owed to you. This may include selling the debt, restructuring the payment, hiring a qualified third-party debt recovery agency, or legal action.

Having all these in place will more than adequately prepare you for a successful MCA collections experience, and help you avoid all the stress and headaches it can present otherwise.

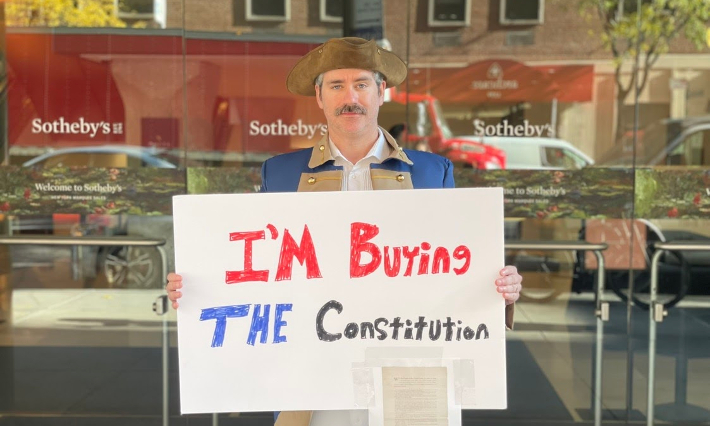

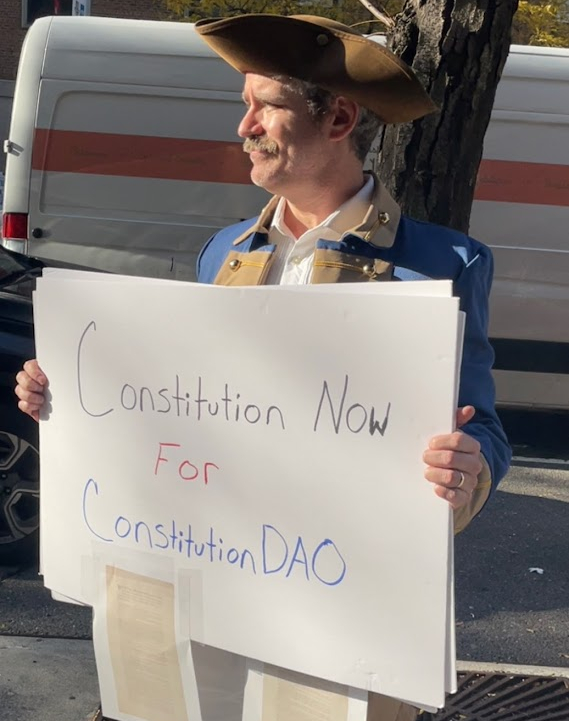

So We Didn’t Buy The Constitution

November 18, 2021 An internet movement started last week to buy one of the only remaining original copies of the United States Constitution reached a roaring climax on Thursday night and then descended into chaos and confusion as almost no one seemed to know what the outcome was, how auctions work, who was bidding on the movement’s behalf, or anything at all.

An internet movement started last week to buy one of the only remaining original copies of the United States Constitution reached a roaring climax on Thursday night and then descended into chaos and confusion as almost no one seemed to know what the outcome was, how auctions work, who was bidding on the movement’s behalf, or anything at all.

Several news outlets reported that the Decentralized Autonomous Organization, aka DAO (pronounced “Dow”), representing the internet movement, had won, including the crypto-focused outlet Coindesk. The DAO raised approximately $47 million via ethereum contributions in a matter of just days from a total of more than 17,437 people who joined in (yours truly included). Knowing that, most people were lured into believing that the winning bid of $43.2 million had to have been the DAO. Unfortunately, the contributors seemed largely unaware of the hefty fees charged on top by Sotheby’s, the 8.875% sales tax, and more. I wrote about this two days prior.

This snafu seems to have been expected by those skeptical of an internet movement. Having actually stood outside of Sotheby’s earlier in the day in full George Washington-esque garb, I was asked by someone seemingly connected to a bidder if the DAO was aware of the added fees. I told them what I knew, but I couldn’t speak in the affirmative for the other 17,436 people.

Having also crossed paths with Julian Weisser, however, a Core team member and nice fellow, it was clear that he was extremely knowledgeable about all the details involved. Weisser was also the first team member to officially announce the loss on the discord.

“@everyone – We did not win the bid for the copy of the U.S. constitution.

While this wasn’t the outcome we hoped for, we still made history tonight with ConstitutionDAO. This is the largest crowdfund for a physical object that we are aware of—crypto or fiat. We are so incredibly grateful to have done this together with you all and are still in shock that we even got this far.

Sotheby’s has never worked with a DAO community before. We broke records for the most money crowdfunded in less than 72 hours. We have educated an entire cohort of people around the world – from museum curators and art directors to our grandmothers asking us what eth is when they read about us in the news – about the possibilities of web3. And, on the flip side, many of you have learned about what it means to steward an asset like the U.S. constitution across museums and collections, or watched an art auction for the first time.

We had 17,437 donors, with a median donation size of $206.26. A significant percentage of these donations came from wallets that were initialized for the first time.

You will be able to get a refund of your pro rata amount (effectively minus gas fees) through Juicebox. Please expect more details from us about this tomorrow – our team has not slept in the past week, and we are giving people the night to get some rest before we’re back at it tomorrow AM.

Every one of you were a part of this. We want to also thank our partners in this work: Alameda Research, Endoament, FTX US, Juicebox, Morning Brew, and SyndicateDAO”

Once the results finally started to kick in, feelings were mixed. Discord members were torn between feeling completely bamboozled or excited to use a DAO to make some other kind of meaningful purchase. The leadership behind the organization’s official twitter account signed off for the night early after working around the clock for about a week to even put the entire thing together.

Once the results finally started to kick in, feelings were mixed. Discord members were torn between feeling completely bamboozled or excited to use a DAO to make some other kind of meaningful purchase. The leadership behind the organization’s official twitter account signed off for the night early after working around the clock for about a week to even put the entire thing together.

gn everyone we’ll be back tomorrow

thanks for all your love and support. can’t wait to shape the next leg of this journey with you all 🙂 🌙 📜 https://t.co/Vhtiglpntg

— ConstitutionDAO (📜, 📜) (@ConstitutionDAO) November 19, 2021

By any measure, the dollars involved were astounding. This particular copy of the Constitution last sold in 1988 for the price of $165,000. Sotheby’s pegged the current value at $15 – $20 million. With $47 million in hand, winning seemed a strong possibility. The one major problem, however, is that with the blockchain being a public ledger, the rival bidder already knew the DAO’s best bid.

Overall, it was a rather strange experience, no doubt made more unusual by my throwing down eth and then donning a costume on the Upper East Side of Manhattan to the bewilderment of many locals.

Was this ultimately a loss for crypto or still a win? Only time will tell…

When The Music Stopped: How The Pandemic Threatened the History and Culture of Austin, Texas

November 15, 2020

In April of this year, Threadgill’s – a legendary Austin music venue and beer joint that, in the 1960s, famously launched the career of blues singer Janis Joplin — turned off the lights and pulled the plug on its sound stage.

A converted gasoline station, Threadgill’s had been a rollicking music scene since 1933 when musician and bootlegger Kenneth Threadgill secured the first liquor license in Texas after Prohibition. His juke box was crammed with Jimmie Rodgers songs and Threadgill himself famously sang and yodeled Rodgers’ tunes.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

“The first time I went to Threadgill’s was in the fall of 1968, when I was a freshman at UT,” recalls Perry Raybuck, a songwriter-folksinger and retired government worker who, as a member of the Southwest Regional Folk Alliance, played the stage in 2018. “It was the beginning of an education for me,” he adds. “I had been a Beatles and rock n’ roll kid and it opened me up to different music styles. I became a convert.”

In 1981, Threadgill’s was taken over by another acclaimed club owner, Eddie Wilson, who previously had been the proprietor of the Armadillo, a fabled music venue. Wilson began to actually pay musicians – Threadgill had compensated them mainly with free cold beer – and installed a circular stage.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

“Live music,” says Laura Huffman, chief executive at the Austin Chamber of Commerce, “is why people come here. It is a central component of Austin’s cultural and economic life.”

Omar Lozano, director of music marketing for Visit Austin, the city’s main tourism organization, says: “We have close to 250 places in the greater Austin region where you can hear live-music, although it’s closer to 50-70 on any given night. During South by Southwest, no stone is left unturned — everything becomes a stage: parking garages, grocery stores, housing co-ops. There are also four or five stages at the Airport, which helps liven up the mood.”

But that identity is being put to the test. So far this year, Austin has lost a raft of live music venues. Among those joining Threadgill’s in honky-tonk heaven since the pandemic struck are Barracuda, Plush, Scratchhouse, Shady Grove, and Botticelli, all of which provided niche audiences to both established musicians and up-and-coming acts.

The roller-coaster ride of government mandated shutdowns followed by a limited re-opening in the spring and another shutdown since July fourth is making life miserable and untenable for both club owners and already hardpressed musicians and artists, says Marcia Ball, a piano player and blues singer.

Ball, who was named by the Texas Legislature as “2018 Texas State Musician” and whose musical style was once described by the Boston Globe as “mixing Louisiana swamp rock and smoldering Texas blues,” told deBanked: “There was already a limited amount of opportunity for musicians to perform and monetize their work in Austin, so it has always been necessary to travel to make a living. But we still depend on a thriving local scene, and we’re losing that when key venues like Threadgill’s disappear.”

Adds Graham Williams, a prominent Texas promoter of touring bands: “These venues and bars are vital to the music ecosystem. Local bands and cover bands need hangouts, even if people are not buying tickets. They’re places to play every night of week.”

While unheralded outside the Austin scene, the local music joints were often a port-of-call for out-of-town promoters and nightclub owners checking out Austin talent – “most notably Barracuda (which) had super-popular acts and was like a hipster garage venue,” says promoter Williams. “A lot of touring bands played there on their way up.”

A July study by the Hobby School of Public Affairs at the University of Houston found that the city’s live music industry is in desperate straits. Sixty-two percent of live music spots and 55% of the bar-and-restaurant businesses reported to researchers that that they can endure for no more than four months, making them the most vulnerable of 16 industries surveyed.

And the situation has become “even more ominous” since the report was published, explains Mark P. Jones, a political scientist at Rice University in Houston and a lead researcher on the Hobby study. “That survey finished polling two hours before all bars and restaurants closed back down,” he says. “Everything people were saying was when bars were at 50% capacity. That’s a best-case scenario.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

“He knocked down the rent a little bit,” Severin says of his landlord, but the situation is dire. “We just had a fifth venue, Re bar, close at the end of August,” he says. “It was a punch in the gut. This could be me.”

The Bitter End in Greenwich Village is also keeping its head above water despite not opening its doors since March. The nightclub has a storied past: owner Paul Rizzo recounts that it is where pop singer Neil Diamond got his start and where “everyone from Curtis Mayfield to Randy Newman” has performed since its opening in 1961. But the club is silent now since the pandemic overwhelmed the city’s hospitals and made New York the epicenter of sickness and suffering during the spring. So far the club is getting help from a landlord’s forbearance and loyal musicians.

Peter Yarrow (the “Peter” in the bygone trio Peter, Paul and Mary), donated a streamed concert to patrons who contributed to a fundraiser that raised more than $50,000. And grateful local musicians also put on a benefit directing people to a Go Fund Me page on the Internet that raised another $16,000. “We’re a major venue for local musicians,” Rizzo says. “We should pull through.”

It’s in their self-interest for artists to do whatever they can to keep the doors open at a club like The Bitter End. “These days because of the last two decades of declining record sales — live music is the bread and butter of a musician’s income,” says journalist Edna Gundersen, a recently retired, 28-year-veteran of USA Today. “That’s true whether it’s a local entertainer or an international superstar.” (Gundersen earned the reputation as Bob Dylan’s favorite journalist; it was she who scored his only interview after he won the Nobel Prize for literature in 2018, publishing his eccentric musings in the The Telegraph of London and breaking the news that he would indeed accept the prize.)

“Touring has been crushed,” Gundersen adds, “and festivals have been canceled. So people doing the circuit and clubs are gone for all intents and purposes. Streaming — while initially up — is down because people aren’t listening to music in the gym or in their cars. Physical record sales are also down because people aren’t going to stores. All of this is just killing musicians.”

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

Hoping to win attention and assistance for their plight from the federal government — “We’re the first to close and the last to reopen,” Severin says — live-music entrepreneurs like himself and Rizzo and more than 2,800 club-owners and promoters across the country have banded together to form the National Independent Venue Association.

Their membership includes independent proprietors (no corporate members allowed) of saloons, cabarets and concert halls as well as theaters, opera houses and auditoriums from every state plus the District of Columbia. To help plead their case with Congress, the organization hired powerhouse law firm Akin Gump Strauss Hauer & Feld, the largest Washington, D.C. lobbying firm by revenue.

NIVA also blanketed Congressional offices with two million letters, e mails and correspondence generated from hordes of fans and performers. Among the many scriveners are a slew of boldface names: Mavis Staples, Lady Gaga, Willie Nelson, Billy Joel, Earth Wind & Fire, and Leon Bridges. Comedians Jerry Seinfeld, Jay Leno and Jeff Foxworthy have also penned notes to lawmakers championing NIVA’s cause.

Their message: without federal funding, 90% of independent stages will go under over the next few months. “The heartbreak of watching venues close is that once a building is boarded up, it’s not going to be a music venue any more,” warns Audrey Fix Schaefer, communications director at NIVA. “They operate on thin business margins to begin with and they’re too hard to develop.” For touring acts, each city stage is “an integral part of the music ecosystem,” Schaefer explains. “When artists finally do get back on the tour bus, they might have to skip the next five cities and go on to the sixth.”

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

The legislation would provide grants up to $12 million for live entertainment venues to defray most business expenses incurred since March, including payroll and employees’ health insurance, rent, utilities, mortgage, personal protection equipment, and payments to independent contractors.

NIVA’s chief argument for the legislation is coldly economic rather than sentimentally cultural. The organization cites a 2008 study by the University of Chicago that spending by music patrons produces a “multiplier effect” for the broader economy. For every dollar spent by a concert-goer at a live performance, the Chicago study determined, $12 in downstream economic activity occurs.

Explains Scott Plusquellec, nightlife business advocate for the City of Seattle: “You buy a ticket to a show and the direct economic impact of that purchase is that it pays the artist, bartender and the club itself as well as the band, advertisers, and promoters. The indirect economic impact,” he adds, “is that after you bought the ticket, you went to a barber shop or a hair salon to look good that night. You might also have dinner, go to a bar for a drink and tip the bartender. That’s the whole the idea of a ‘multiplier.’”

In Austin, that economic logic is an article of faith with city burghers, asserts Lozano of Visit Austin, who reports that live music in the capital city is roughly a $2 billion industry. To promote live music, the tourism bureau sponsors such endeavors as “Hire an Austin Musician.” That program, Lozano says, “sends musicians around the U.S. to represent us during marketing season.” In another promotional campaign, Visit Austin arranged for singer-songwriter Julian Acosta to play a gig at travel agents’ offices in London when Norwegian Air inaugurated direct flights between London and Austin in 2018. “The U.K. is one of our best markets,” he reports.

Even so, efforts by the business community and the City of Austin have failed to stanch much of the industry’s bleeding. According to its website, the city has disbursed $23.7 million in loans and grants to small businesses and individuals, but slightly less than $1 million of that has gone to live-music and performance venues, entertainment and nightlife, and live-music production and studios.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

The Continental Club on South Congress – a key fixture in the hip “SoCo” strip just over the Colorado River from downtown – appeared to do best. It picked up $79,919 from two programs: $40,000 in the CARES-backed small business grants program, and $34,919 from the city’s Creative Space Disaster Relief Program. Other clubs receiving $40,000 in the small business grants program included Stubbs, The Belmont, Cheer Up Charlies and the White Horse. (For a full list go to: http://www.austintexas.gov/edims/document.cfm?id=347299)

Joe Ables, owner of the Saxon Pub, a major Austin venue for jazz – blues singer Ball hailed it as one of several important Austin clubs “that sustains creative endeavor, especially for songwriters” – was vexed that his grant application was denied by the city “with no explanation.” Ables also voiced dissatisfaction that the city paid the Better Business Bureau a 5% administration fee to handle $1.14 million in relief funds, including determining which applicants were approved. “What would they know about live music,” he says.

Even for clubs that received city largesse, it hasn’t been nearly enough to sustain them. The North Door, which got $15,240, closed for good on September 11 (an ominous day — the anniversary of the attacks on the World Trade Center and the Pentagon.)

Meanwhile, enough clubs and venues were left out in the cold that club owner Stephen Sternschein could tell deBanked just before the slide show was released: “I’ve heard talk of a $21 million grant program but most people I know haven’t seen a dollar of that.”

Sternschein is managing partner of Heard Presents, an independent promoter and operator of a triad of downtown clubs that includes the spacious Empire Garage, which features hip hop and urban jazz, and has space for 1000 music-goers. A member of NIVA, Sternschein describes efforts by both the state and local governments as “woefully inadequate.” Says he: “People are looking to the federal government for answers.”

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

“You can go out to dinner in Waco,” he observes, referring to the mid sized Texas city between Austin and Dallas best known as home to Baylor University and its “Bears” football team, fervent Baptist religiosity, and unremarkable night life. “Music brings in revenue to Austin and to Texas that wouldn’t otherwise come here.”

In addition, Jones says, the large presence of “artists, creative types, and freelancers” helps make Austin a strong selling point for “brain industries” to attract talent from the East and West Coasts. “It supports the technology industry by making it easier to recruit employees to live there,” he says. “Austin is an alternative to Silicon Valley. People who are progressive might be hesitant to come to conservative, red-state Texas from California but they’ll come to Austin because it’s culturally cool.”

Austin, which embraces the slogan “Keep Austin Weird,” is on the verge of becoming just like every place else in Texas. Should it relinquish its flavor and charm, it could discourage many of the assorted business groups and professionals from keeping Austin on their dance card as a popular destination for meetings, conferences and get-away trips.

Howard Freidman, managing director at Bluechip Jets, a broker of private luxury aircraft, had an earlier career as a technology industry executive. Partly drawn by his previous experiences with the city, Freidman moved to Austin earlier this year. “It had the same coolness and weirdness of New Orleans — but also with the professionalism of a tech city,” he says.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

Many of the technology firms – including such needy companies as Samsung, Intel, Rackspace, Facebook, and Apple – have each received tax breaks, grants and subsidies worth tens of millions of dollars from a variety of local jurisdictions. Not only have the city of Austin and Travis Country been beneficent, but adjacent county governments and the state of Texas have provided abundant support. A 2014 study by the Workers Defense Project, in collaboration with UT’s Lyndon B. Johnson School of Public Affairs, reported that the state of Texas showers big business with $1.9 billion annually in state benefits. Most recently, officials with Travis County and a local school district granted Tesla more than $60 million in tax rebates to build a massive “gigafactory” southeast of town near Austin-Bergstrom International Airport.

To house the burgeoning cohort of “knowledge workers,” there are condominium conversions, tear-downs, high-rises and other forms of frenetic real estate development which, in their train, bring higher property taxes, steeper rents, and unaffordable housing.

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

The drop-off in live music and the belt-tightening by musicians is causing third-party pain for people like veteran Austin journalist and publicist Lynne Margolis, whose national credits include stories for Rolling Stone online, and radio spots for NPR. “The public relations aspect of my work has dropped away because artists can’t afford to pay,” she says, “and music journalism is falling by the wayside. It’s hard not to feel to like a double dinosaur.”

Led by bars, restaurants and music venues, on many days the solemn departure of small establishments has the business news sections of Austin newspapers reading more like the obituary page. One hardy survivor is Giddy Ups – a throwback honky-tonk on the town’s outskirts that advertises itself as “the biggest little stage in Austin” – promising “just about everything,” says owner Nancy Morgan, including “country, blues, rock, bluegrass, and soul.” For the past 20 years Giddy Ups has developed a devoted following of musicians and patrons while fending off hyper modernity.

“It has an untouched, back-to-the-seventies, cosmic cowboy vibe,” says local musician Ethan Ford, a guitarist and bass player whose trio, The Slyfoot Family, has graced its stage. “It’s a time capsule,” Ford adds.

Morgan declined to disclose her annual receipts but in 2019, she reports paying out $188,000 in wages to employees, $72,000 to musicians, and $185,000 in combined sales taxes to the city of Austin and to the state. Despite her status as a taxpayer, employer and entrepreneur, she has received no state aid and is disqualified from receiving city pandemic assistance programs, meager as they may be, because she’s located in an extra-territorial jurisdiction.“

Nancy still bartends most nights and does all of the booking,” says Ford. “Her knowledge of the Austin music scene could fill a couple of books. I know a decent fistful of Austin venue owners and she’s about the only one that hasn’t given up, been forced out, or just retired. She’s a dynamo.”

Unless the cavalry arrives for Morgan and other holdouts, though, their musical days may be numbered.

Editors Note: Threadgill’s didn’t make it. The venue “has closed for good, the property has sold, and the building will eventually be torn down,” according to information disseminated for its Last Call Music Series. Its November 1st grand finale show featured Gary P. Nunn, Dale Watson, Whitney Rose, William Beckman, and Jamie Lin Wilson.

The building will be replaced with apartments.

To Niche or Not to Niche, That Is the Fintech Question

October 1, 2019 A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

In the past decade, the fintech industry has followed this model to a tee. Whether it was B2B or B2C, fintech startups broke the banking business into narrower segments, offering singular niche services for various finance needs, e.g. credit card refinancing, small business loans, student loans, P2P payments, mortgages and more. From this model, big banks became the TGI Fridays of financial offerings (where you go to experience a full spread of financial services), and fintech platforms became the speciality grilled cheese shops (where you go to get the one thing you really crave).

Fintech Niches Fill Big Gaps

Many startups went niche not only because it was a business model that worked, but because the legacy banking industry model was out of date and there was room for true disruption. With these opportunities, niche fintechs could hone in on services that fulfilled singular needs, and they could do it with a focus, passion and dedicated customer service that most general banks couldn’t provide—and the results of this have been mostly positive. Globally, financial inclusion of unbanked people has improved. According to The World Bank, 69 percent of adults or 3.8 billion people now have an account at a bank or mobile money provider. In the U.S., niche fintechs made it easier for small businesses to get a loan post-recession. A host of online lenders stepped in to fill the gap, understanding that without access to relevant capital, small businesses struggle, which ultimately affects economic growth, jobs and inflation.

Can Fintechs Stand up to Tech Giants?

Tech giants thrive when users treat their platforms/offerings as a one-stop shop, something that is already commonplace in China, where millions of people use Tencent’s WeChat app to do almost everything—pay bills, book medical appointments, chat, play games, read news and pay for meals. Although this is not at the same level of activity in the U.S., it is a trend likely to continue.

The winds have been shifting as fintech companies question whether it makes sense to stay true to their niche or offer additional services as a path to scalability and profitability. By taking the latter path, former niche startups are now either a) building out and offering more financial services or b) partnering with more established companies/banks. Some recent examples include eBay and Square Capital, Venmo and Uber and KeyBank and HelloWallet. These partnerships seem to be a win-win—for the niche companies hoping to solve for scale and revenue stream issues, and for the established companies looking to offer complimentary services their core customers already use—but they also have fintech startups standing at a crossroads. Will working a niche be sustainable in 2020 and beyond, or is becoming a jack of all trades the only means of survival?

Beware of Diluting the Brand

For starters, the only means of survival for any fintech company is to solidly define what the company brand is and what it stands for. For example, many small business lenders are deeply passionate about fueling the American dream through helping business owners unlock their financial potential. Supporting small business is key to our country’s economic fabric. Dynamism and the ability to recover from an economic downturn are both dependent on startups’ ability to grow quickly, and in most cases, the only way for them to do so is through access to capital. For a fintech lender to become a trusted brand to small business owners, it must remain devoted to them as a company that has the financial wellbeing and vitality of small businesses in mind. This means facilitating the right loan for them, right when they need it.

The key for fintech companies is to be careful about diluting the brand. When companies stray too far from what they are passionate about, their core audiences suffer. Tech giants enter new spaces every day, whether from R&D or acquisitions. A strong brand (and the loyalty its customers have to it) will not only insulate a fintech company from the tech giant threat, but make its mission and voice stronger by comparison. Think about this the next time you are eating at In-N-Out Burger (sorry, East Coasters!). The humble hamburger shop became a cultural phenomenon through its razor-sharp focus on simplicity, quality and consistency.

Always Consider the Human Factor

Innovation and automation are both critical to survival in the fintech space. But how much tech can a fintech leverage in its solutions to avoid becoming too niche? The answer lies in understanding the core customers’ needs and how much technology can be used to fulfill those needs. For an e-wallet app, the key needs of customers are frictionless payments and transfers happening in real time; it is not a solution (when it’s working) that needs a lot of human interaction. A fintech company such as this can use technology and machine learning to automate most of its services.

Conversely, the human factor is still a huge part of the equation in some fintech services. For example, a person’s livelihood is at stake when a small business takes on a loan or another capital solution for its growth needs. This is a very personal and consequential decision for a business owner. In fact, in the majority of cases, they don’t want to rely solely on a technology-powered platform to deliver the most appropriate loan options for their needs, not to mention address their specific concerns and questions. A fintech lender can leverage technology at every touchpoint to optimize the application and loan approval process; but ultimately, many business owners will desire interaction with a live representative, not a chatbot. The human factor is crucial in business lending, and something that could become lost as a result of brand dilution. While scalability is important, customer service is equally so.

In the end, the decision to offer niche services or to go wide will depend on what’s at the core of a fintech company. Indeed, the pressures to scale, grow and earn returns for investors are huge for any business, but decision-makers must keep their perspective on the market they serve and the problems they solve best. If expanded offerings and partnerships with other service providers enhance your brand and what it stands for, then this approach makes sense for growth and customer satisfaction. If not, then serving up the best grilled cheese sandwiches around, to the folks who really crave them, may well be the best path.