Archive for 2021

LoanMe Has Been Acquired Along With Liberty Tax By Canadian Listed SPAC

February 22, 2021 LoanMe has been acquired. The announcement was made by Nextpoint, a SPAC listed on the Toronto Stock Exchange that simultaneously acquired Liberty Tax.

LoanMe has been acquired. The announcement was made by Nextpoint, a SPAC listed on the Toronto Stock Exchange that simultaneously acquired Liberty Tax.

The combined company will be called NextPoint Financial.

NextPoint will acquire LoanMe at an enterprise value of approximately US$102 million, US$18 million of which is payable in cash, approximately US$49 million of which is payable in NextPoint common stock equivalents and with the balance of which reflects the assumption of existing corporate net debt at LoanMe.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses to get to the NextPoint in the financial futures,” the company said of its newly formed self.

The company says that LoanMe had originated $2 billion since inception, 340,000+ borrowers since inception, and has a $200 million loan portfolio. Liberty Tax, meanwhile, processes 185,000+ SME tax returns, 1 million+ US consumer tax returns, and 400k+ Canadian tax returns.

Combined, the company projects $317M in revenue in 2021.

“NextPoint has obtained a commitment for a new US$200 million revolving credit facility, advances under which may be used for NextPoint’s general corporate purposes, including to fund the Liberty Tax and LoanMe cash purchase prices, and to fund potential future acquisitions,” the company said in a public release.

Game Stopped? Short Selling, Social Media, and Retail Investors Collided in House Hearing

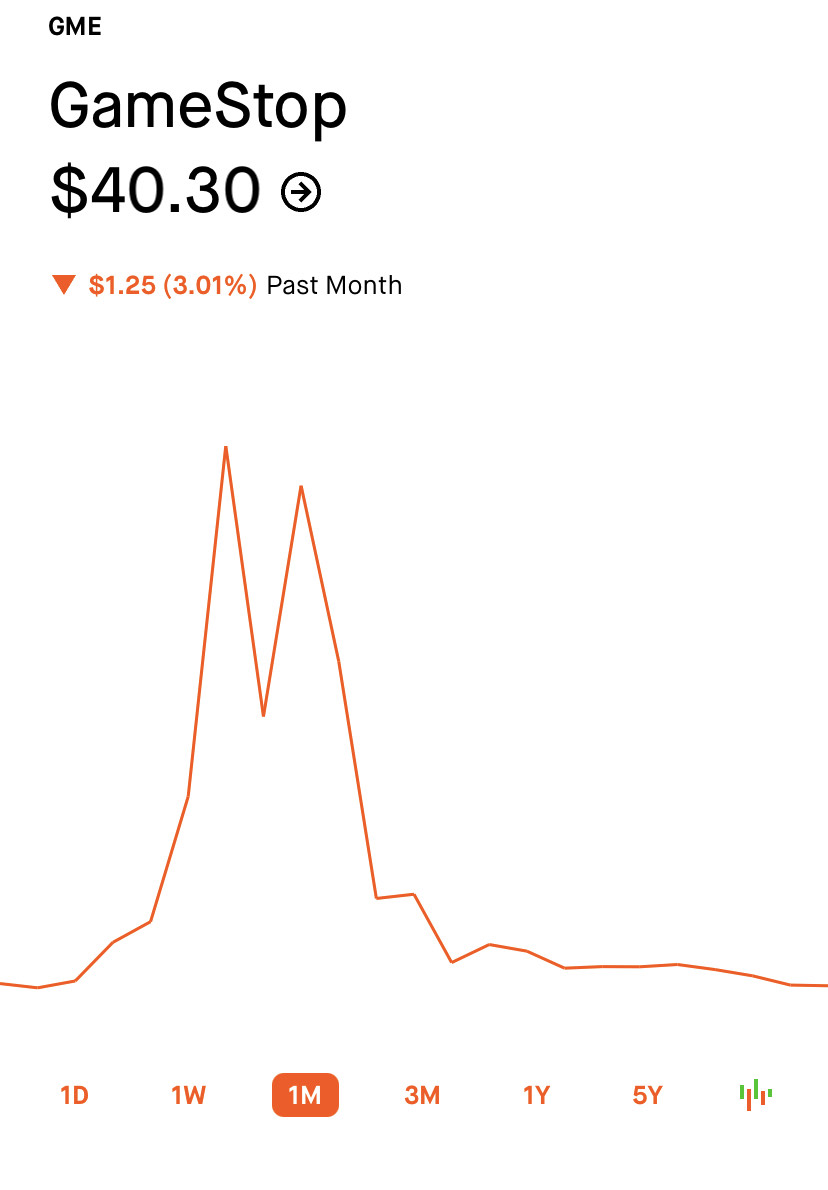

February 21, 2021 Nearly a month after the GameStop (GME) stock price shot halfway to the moon, the House Committee on Financial Services gathered representatives from the trading conflict in a hearing to examine what happened.

Nearly a month after the GameStop (GME) stock price shot halfway to the moon, the House Committee on Financial Services gathered representatives from the trading conflict in a hearing to examine what happened.

The focus was on a struggle between big institutional money and retail, everyday investors. Armed with nothing but zero-commission investment apps, government stimulus, and with nothing to do but sit at home waiting for a pandemic to end, retail traders exploded onto the securities markets. One of the results was a dramatic rise and fall of GME at the end of January.

Vlad Tenev, the Robinhood app’s co-founder, faced the highest number of questions after the firm blocked trading of GME on January 28th. Across the videocall-octagon was Keith Gill, a r/WallStreetBets retail investor long on GME since the summer, known by some as u/DeepFuckingValue.

With his signature headband hanging in the background, sitting in a gaming chair, Gill donned an uncharacteristic suit and tie while representing himself as a stand-in for the millions of retail investors who were along for the ride.

His message: he is no expert, is not responsible for the volatility of a multi-billion dollar securities market, and after everything, he still likes the stock.

“I support retail investors right to invest in what they want when they want to,” Gill said. “I do not have clients, and I do not provide personalized investment advice for fees or commissions. I am an individual investor.”

Gill went on in his testimony to state that his posts and video appearances about GME to other investors were not trading advice and no different than talking in a bar about a stock he liked.

Before the run-up of GME, Gill had a small audience of around 500 viewers. After GME started gaining ground, Gills’s online popularity exploded alongside the Reddit stock betting forum r/WallStreetBets.

Gill gained hundreds of thousands of followers, while WSB saw a rise of 8 million members in just one week. In the end, his positions in the stock earned him $22 million, as he shared with his extended family over the holidays, “we’re millionaires.” Many were not as lucky, and some have looked toward social influencers like Gill as speculators and market manipulators.

The Congressional Committee were light on their interrogation of Gill, acknowledging the importance of protecting retail investor rights. In challenging Tenev of Robinhood, Committee Chairwoman Maxine Waters set the tone, stating: “The market volatility around GameStop has highlighted how many people believe the cards are stacked against them.”

Waters asked numerous yes or no questions to Robinhood’s Tenev, who could only respond with drawn-out statements. Overall, the fintech founder was apologetic but still insisted Robinhood did nothing wrong and does not answer to hedge funds.

“Look, I’m sorry for what happened, and I apologize. I’m not going to say Robinhood hasn’t made mistakes in the past,” Tenev said. “We’re going to learn from this and make sure it doesn’t make the same mistake in the future.”

At the height of the trading frenzy Thursday, January 28th, Robinhood suddenly restricted the purchase of GME and other “meme” stocks and only allowed selling. Demand plummeted because, despite problems in the past, Robinhood is still a favorite in the r/WallStreetBets community. Prices roller coasted downward. From a high of $468/share, the GME price dropped down to trading in the $40 range in the month that followed.

Tenev was explaining his financial responsibilities to clearinghouses as a brokerage firm.

On the morning of January 28th, Robinhood suddenly received an email from a subsidiary of the DTCC, holder of all U.S. traded securities. It asked for an increase of $3 billion to ensure Robinhood could back the explosion of GME trading, an astronomical price. Robinhood complied by shutting down buying, offering sell-only, bringing the insurance price down to more than $700 million. The firm also reached out to existing investors to raise billions in capital, yet Tenev still insists there was never a liquidity problem.

Representing traditional, “smart money” investors was Ken Griffin of Chicago hedge-fund Citadel LLC and market-maker Citadel Securities, known for its short-selling positions. Alongside was Gabe Plotkin, the founder of Melvin Capital, a hedge fund with many short positions in GME, lost $6 billion in just 20 trading days. During the crazy trading week, Melvin was offered $2.7 billion in new investment from Citidel funds after losing 30% of its value.

Citadel is also a prime market maker for Robinhood, completing many of the app’s trades. Some, including those house members lobbing questions, saw a firm that self describes its mission as “to democratize investing,” cut out the poor and give to the rich. It looked like a collaboration between a major investor making up for losses due to app trading while retail investors were left out.

Chair member Blaine Luetkemeyer, a Republican from Missouri, expressed his concern that GME had been an over shorted stock and that “naked shorting” drove the price down.

“You have stated in your testimony that you had no intention of manipulating the stock,” he said. “If you’re short selling your stock 140%, for me from the outside, that looks like what you’re doing.”

Both Citidel and Melvin Capital representatives said there was no collusion to drive the price down, no over shorting, and no buy-out when the short positions failed.

The end of Gills’ testimony, read in front of a “hang in there” cat poster summed up the hearing well.

“It’s alarming how little we know about the inner-workings of the market, and I am thankful that this Committee is examining what happened,” He wrote. “I’m as bullish as I’ve ever been on a potential turnaround. In short, I like the stock.”

The MCA of the Major Leagues

February 20, 2021 It’s been said a million times. It’s not a loan. The seller receives an upfront payment in exchange for an agreed upon percentage of future earnings. If there’s no earnings, then nothing is owed.

It’s been said a million times. It’s not a loan. The seller receives an upfront payment in exchange for an agreed upon percentage of future earnings. If there’s no earnings, then nothing is owed.

No, it’s not a merchant cash advance, it’s a big league advance, a deal offered by a company named just that, Big League Advance (BLA) to baseball players.

“Players receive an upfront investment from Big League Advance in exchange for an agreed upon percentage of their future Major League earnings,” the BLA website says. “If the player never makes it to the Major Leagues, the player will never owe or pay any money back to Big League Advance.”

The company was founded in 2016 and recently made the news because of its success with Padres player Fernando Tatís Jr. Tatís recently signed a 14 year contract with the team worth $340 million, the third highest in history. And now BLA stands to get their cut, potentially as much as $30 million, according to the WSJ.

The BLA website explains it as such:

Players choose what percentage of their future career earnings they want to give Big League Advance. For example, Big League Advance may offer a player $50,000 for every 1% of his future professional earnings. If a player wanted to sign a deal for 5%, he would receive $250,000, or if he wanted to sign a deal for 10%, he would receive $500,000. While our offer amounts are non-negotiable, the percentage the player would like to give up is up to the player.

The average deal is for 8% and the underwriting performed is a combination of the players’ background, scouting, and statistics.

Michael Schwimer, a former Major League pitcher, is the founder and CEO. The WSJ says that the company has made advances to 350 players for a combined $150 million.

Fintech Lenders Did Better Job Meeting Intentions of the CARES Act, Study Finds

February 18, 2021 Fintech lenders doling out PPP not only reached smaller businesses on average but played an essential role in extending PPP loans to Black-and Hispanic-owned businesses, according to a study conducted by professors at the NYU Stern School of Business.

Fintech lenders doling out PPP not only reached smaller businesses on average but played an essential role in extending PPP loans to Black-and Hispanic-owned businesses, according to a study conducted by professors at the NYU Stern School of Business.

“Fintech lenders originated much smaller loans than other lenders, suggesting they served smaller firms on average,” researchers found. “Overall, we find that, relative to other lenders, [Minority Development Institutions] nonprofits, and fintech lenders make a substantially larger share of their loans to minority borrowers, particularly Black- and Hispanic-owned businesses.”

The team of economists looked over 3.4 million PPP transactions to determine what category of lenders had the highest minority share among their loans. Ryan Metcalf, Head of Public Policy for Funding Circle, member of the Innovative Lending Platform Association (ILPA), shared the full study on LinkedIn, pointing out that six ILPA members had contributed to saving jobs.

“(Funding Circle US, BlueVine, Kabbage, Inc, OnDeck, Fundbox, Lendio) provided more than 476,000 #PPP loans totaling $16.5 billion with an average loan size of ~$30,000, median loan size of $15,000, and helped save more than 2 million jobs,” Metcalf wrote. “And that was just in 2020.”

The study found that fintech lenders did a better job meeting the intention of the CARES act. While most lenders were giving out larger loans to large firms, fintech better reached actual small businesses with smaller loans on average.

“Section 1102 of the CARES Act explicitly specified that the program should prioritize ‘small business concerns owned and controlled by socially and economically disadvantaged individuals,'” they wrote. “However, the SBA did not issue specific guidance for distributing the loans, leaving private financial institutions administering the loans to independently determine which businesses to serve first or at all.”

Instead, as has become clear, many funds went to larger firms and seemed to miss minority communities. The team compared the mean and median loan amounts for different Lenders, finding the smallest in both types were fintech loans.

Researchers put first and last names through a mathematical model to predict race because that data was not available from the majority. Then predictions were compared to the sample borrowers that self-reported race. The algorithm was 78% accurate in guessing black names, 84% in guessing Hispanic, 95% for Asian, and 99% accurate for white names.

Maryland MCA Prohibition Bill Morphs Into MCA APR Limit, Broker Licensing, Double Dipping, Uniform Disclosure, and Go to Jail Bill

February 18, 2021Update: A Recording of the Hearing is Here

Plans to enact “prohibition” in Maryland on merchant cash advance transactions abruptly came to a halt last year, but the legislature there has brought the issue back front and center in 2021, designing a system of prohibition while dropping the actual word from the name.

Plans to enact “prohibition” in Maryland on merchant cash advance transactions abruptly came to a halt last year, but the legislature there has brought the issue back front and center in 2021, designing a system of prohibition while dropping the actual word from the name.

No MCA transacted in the state would be permitted to have an estimated APR that exceeds 24%, for example. The penalty for violating such a statute can be imprisonment for up to 3 years.

Newly introduced House Bill 664 (SB0532) would “prohibit a person from engaging in the business of making or soliciting a sales-based financing transaction unless the person is licensed by the Commissioner of Financial Regulation” and would require that an applicant “for a license having $20,000 in available liquid assets and to have demonstrated a sufficient level of responsibility to command public confidence and warrant faith in the honest operation of the business.”

The 26-page bill includes a laundry list of requirements and restrictions like specific disclosures, how to calculate a forward-looking estimated APR on an MCA, and a limitation of 24% on that APR.

The bill draws heavily from the recently passed law in New York, going so far as to copy and paste the section requiring MCA funders to disclose if there is literally any “double dipping” in the contract.

The Commissioner of Financial Regulation would retain sole authority to judge compliance with the law.

A House committee hearing on the bill was conducted yesterday and a subsequent one in the Senate is scheduled for February 23rd at 1pm.

You can read the full version of the Maryland House Bill here.

Shopify Originated $226.9M in MCAs and Business Loans in Q4, Close to $800M For the Year

February 17, 2021 Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

That is a posted increase of 96% over the same quarter in 2019 but was down 10% from q3. The full year 2020 originations of $794M were nearly double the $430M in 2019.

“Products like Shopify Capital are increasingly sought out by entrepreneurs and small businesses that face unnecessary barriers to access from traditional banks,” Shopify President Harley Finkelstein said in the quarterly earnings call. “Merchant empathy runs deep at Shopify. When traditional businesses were turned away, for the perceived high risk, we financed a record number of merchants when they needed it most.”

“We also introduced Shopify Capital to Canada and to the U.K. in 2020,” Finkelstein said. “To expand where we could help merchants.”

Shopify Capital still lagged behind rival OnDeck in origination volume, who reported a little over $1B in originations for the year.

CFPB’s Reach May Extend to PPP Lending

February 16, 2021 The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The foray into non-consumer finance was instead driven by PPP lending.

“Consistent with its authority to ensure compliance with the Equal Credit Opportunity Act (ECOA), the Bureau conducted [Prioritized Assessments] to assess potential fair lending risks attendant to the institutions’ participation in the [PPP] program,” the report said.

Accordingly, the CFPB determined that small business lenders that restricted or limited eligibility such as banks who only permitted applications from existing customers, for example, “may have a disproportionate negative impact on a prohibited basis and run a risk of violating the ECOA and Regulation B.”

The CFPB conceded that it had not actually investigated if violations occurred and noted that the majority of institutions had argued that such limitations were either in place to comply with Know Your Customer legal requirements, to prevent fraud, or both.

The CFPB did not say that it had supervisory authority over non-banks that participated in PPP, but it did signal that its purview was larger than just consumers when it came to the institutions it supervised.

The report can be viewed here.

The CFPB is expected to have more proactive involvement in small business finance under its new incoming director, Rohit Chopra. Chopra’s nomination was formally submitted on February 13th. Dave Uejio, the Bureau’s Chief Strategy Officer, has been serving as Acting Director since President Biden took office.

Lawsuit Against Former MCC Executives Dismissed

February 12, 2021A lawsuit brought by various investment vehicles of Atalaya Capital Managment LP against former officers and/or senior management of Merchant Cash and Capital (later known as Bizfi), was dismissed on Tuesday.

In the judge’s decision, the Hon. Jennifer Schecter said that “plaintiffs seek to hold defendants, former officers and managers of Merchant Cash & Capital, LLC, liable for money plaintiffs lost by investing in the Company. […] Plaintiffs do not sue the Company for breach of contract; instead, they seek to hold the individual defendants liable for the Company’s deficient underwriting through causes of action for negligent mispresentation and fraud. Those claims fail.”

Bizfi failed in 2017 after a long run of being among the largest and earliest merchant cash advance funders in the US.

The case was in the NY Supreme Court under Index No: 655593/2019