Archive for 2020

Deloitte Sued Over Audits of Failed DLI Fund

May 7, 2020Those affected by the failure of Direct Lending Investments (DLI) have added a new target to blame, Deloitte & Touche LLP and related entities.

A lawsuit filed last week in the Superior Court of California says that Deloitte was engaged by DLI to audit the Funds’ financial statements and accompanying footnotes in accordance with GAAP for the years ending 2016 – 2018 and issued clean unqualified audit reports that “negligently ratified and confirmed the false valuations contained in the financial statements and footnotes disseminated to the Plaintiffs.”

Interview With Polling Expert Scott Rasmussen

May 7, 2020On Tuesday, I interviewed nationally recognized public opinion pollster Scott Rasmussen, who is the publisher of ScottRasmussen.com and is the editor-at-large for Ballotpedia, about the trajectory of the presidential race and how the current environment is affecting how people think.

Mr. Rasmussen will be a guest speaker at Broker Fair 2020 Virtual on June 11, 2020. You can watch the video interview below.

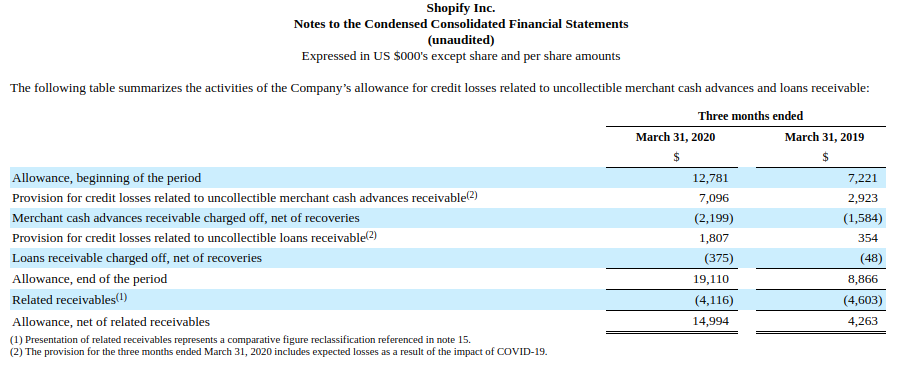

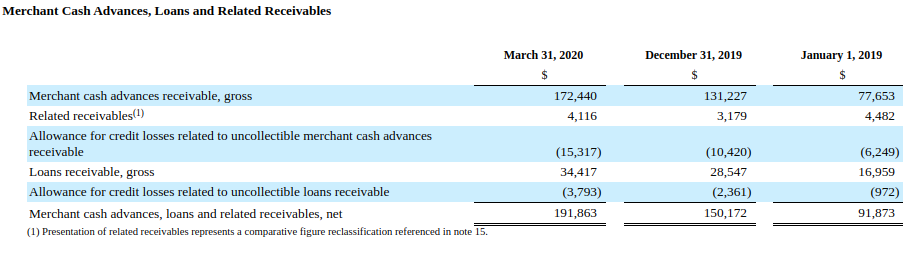

Shopify Shows Strength in Q1 Results, Issues $162.4M in MCAs and Loans

May 6, 2020eCommerce platform Shopify, 2nd only to Amazon in retail eCommerce sales, issued $162.4M in merchant cash advances and business loans in Q1, up from $115.9M in the previous quarter. The statistic pushed them past the $1 billion threshold of funds cumulatively issued since inception.

The company’s provision and allowance for loan losses ticked up from significantly from the same period the prior year but Shopify at that time was originating 50% less volume.

The company reported a GAAP net loss of $31.4M on $470M in revenue. Shopify also has approximately $2.36B in cash and cash equivalents on its balance sheet.

The company reported an increase of monthly recurring revenue, thanks to an increase in the number of merchants joining the platform, strong app growth, and Shopify Plus fee revenue growth.

Shares of Shopify (NYSE: Shop) jumped by more than 5% after the announcement.

Study Finds Vulnerable Canadians Ill-Equipped Against Coronavirus

May 4, 2020 Last week Loans Canada, a loans comparison platform, released a survey of over 900 financially vulnerable Canadians. These being defined as those Canadians who rely on low income, who have limited access to credit, and who have little to no savings available, the study found that many of the respondents were at risk of financial troubles from covid-19 due to their restricted means and ineligibility for government welfare programs.

Last week Loans Canada, a loans comparison platform, released a survey of over 900 financially vulnerable Canadians. These being defined as those Canadians who rely on low income, who have limited access to credit, and who have little to no savings available, the study found that many of the respondents were at risk of financial troubles from covid-19 due to their restricted means and ineligibility for government welfare programs.

30% of those surveyed reported that they are unable to access the Canadian Emergency Relief Benefit, a program that offers CAD$500 a week to those whose finances have been negatively affected by covid-19, due to the terms of the package. In order to qualify, one must earn less than CAD$1,000 over the four week period that the claim is for, leaving many who work part-time or who have had their hours cut unable to access the money.

As well as this, the survey recorded that many of these individuals are having difficulty accessing credit, as nearly 50% said that their bank has denied them funding. This coupled with the fact that 80% have experienced a loss of income due to the novel coronavirus, as well as only 12% of respondents having the government-recommended three months of living expenses saved up, paints a grim picture for the future finances of those vulnerable Canadians.

Beyond immediate finances, 73% of those surveyed believed that the pandemic would negatively affect their credit scores, 63% expect to miss paying at least one bill over the next six months, and 78% claim that they will struggle to finance their necessary expenses if the covid-19 situation continues through the summer.

Altogether, the study indicates a need for more financing amongst those likely to be hit hardest by the economic knock-on from covid-19. What remains to be determined however, is whether it will come in the form of governmental relief, credit from their banks, or funding from the non-bank lenders.

Round Two of PPP Is Targeting Much Smaller Businesses

May 4, 2020 $79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

$79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

Though the pause button for big lenders was only in effect for eight hours that day, it was recognition that the playing field had not been level in the first round. JPMorgan Chase, the largest lender in round 1, for example, had an average PPP loan size of $515,304 in that round.

It’s a competitive process for limited dollars. 5,400 direct PPP lenders have already participated in the second round. More than 80% of those have less than $1 billion in assets. Senator Marco Rubio, a champion of PPP, called the latest figures released by the SBA as “all good news.”

Square Capital, meanwhile, has taken small to the extreme. Their average PPP loan approval as of April 29th was just $16,000, according to stats published by Square Capital head Jackie Reses on twitter. But only 2,711 of the 38,000+ approved had received the funds so far.

Still, that average is significantly smaller than the average loan size of $73,000 approved by Ready Capital in Round 1, a non-bank lender that got widespread attention for approving more PPP loans than any other lender in the country. Those record-breaking numbers, however, led to delays in borrowers receiving their funds to the point where as of April 30th, the responsibility of funding those loans had reportedly transferred to Customers Bank.

OnDeck has also played a role in the PPP, though only as an agent despite being approved by the SBA to lend. That news, which was revealed last week in the company’s quarterly earnings call, is likely due to the company’s current predicament brought on by government-mandated shutdowns.

Enova On Their Small Business Lending Exposure

April 30, 2020Enova’s exposure to the small business lending crisis is limited, the company said during its earnings call yesterday. The Business Backer and Headway Capital are two of the international consumer lending company’s small business lending divisions.

In terms of their overall loan book, small business loans only make up a percentage worth in the teens. “It’s very much manageable for us,” CEO David Fisher said. Fisher also said that they did not have large exposures to entertainment, hospitality and restaurants in their small business loan portfolio and were well diversified.

“Defaults […] have not increased anywhere near as much as we would have expected. Lots of payment deferrals and modifications, but with the PPP checks coming in and states opening back up, we are somewhat encouraged that we haven’t seen very high levels of default yet.”

Enova reported a consolidated Q1 net income of $5.7M.

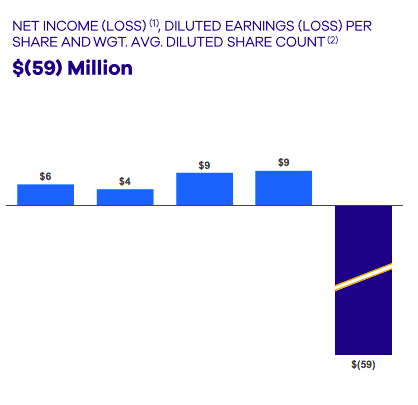

OnDeck Reports Q1 Net Loss of $59M, Suspends Non-PPP Lending Activities

April 30, 2020O nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

The company has also suspended its pursuit of a bank charter. The company has instituted a 15% pay reduction for its full-time employees, a 60% pay reduction for part-time employees, and furloughed additional employees that will receive benefits but no salary. OnDeck CEO Noah Breslow and members of the Board took a 30% pay reduction.

The company said that PPP funding has not really reached real small businesses like the ones they serve and as such only a handful of their customers have received PPP funds. While OnDeck is approved to operate as a PPP lender themselves, they have been acting as an agent of them in the interim and will dedicated their resources almost entirely to this endeavor. The company anticipates that originations of its own products could contract by 80% or more in Q2.

The company has not tripped any covenants or triggers with its own lenders as of yet but is currently in discussions with them on a path forward in this environment.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

Noah Breslow, chief executive officer, is quoted in the announcement:

“In the span of several weeks, the spread of COVID-19 led to government-mandated lockdowns for small businesses both in the US and globally, placing our customers under unprecedented economic stress.After a successful and rapid transition to remote work, we effected immediate changes to our business to preserve liquidity, support our customer base, manage our loan portfolio and reduce costs. With an uncertain timetable for the reopening of the economy, and the effectiveness of government stimulus for small businesses unclear, we will be reducing debt balances in the second quarter and focusing on managing our portfolio, delivering government stimulus to our customer base and ensuring the company has the runway to scale operations again when the economy reopens.”

The company fully utilized its initial $50 million share repurchase authorization in the first quarter of 2020. On February 10, 2020, the Board authorized the company to repurchase up to an additional $50 million of common shares, and the company has approximately $23 million of remaining capacity under that authorization. The company suspended share repurchases late February but maintains authorization to resume purchases at its sole discretion.

For 2020, OnDeck expects:

- Portfolio contraction reflecting an 80% or more reduction in second quarter origination volume

- Increased delinquency and charge-offs stemming from COVID-related economic deterioration

- Reduced Net Interest Margin reflecting a lower portfolio yield

- Reduced operating expenses, on pace to cut second quarter expenses by approximately 25%.

The company had been on a modestly positive trajectory as of year-end 2019.

The company’s stock had a somewhat minor rally on Wednesday, closing at $1.61. That’s still substantially down from where it stood on February 20th at $4.22. It hit a low of 66 cents on March 18th. The share price dropped by nearly 19% after earnings were released on Thursday morning.

This story will be updated as the information becomes available.

Fundry Donates $25,000 to Community FoodBank of New Jersey

April 29, 2020Jersey-City based Fundry made a $25,000 donation the Community FoodBank of New Jersey this week. CFBNJ is an organization that “fights hunger and poverty in New Jersey by assisting those in need and seeking long-term solutions.” In addition to the over 40 million Americans who struggle with hunger every day, an estimated 17.1 million more people will experience food insecurity during this crisis, the organization says on its website.

Thank you, @FundryC, for such a generous donation! Support like this is essential as we continue to meet the growing need. https://t.co/kLhDxn5orJ

— Comm. FoodBank of NJ (@CFBNJ) April 28, 2020