Archive for 2020

Stavvy Co-Founder Kosta Ligris on Navigating Real Estate Loans in a Contact-less world

September 18, 2020 How does real estate loan signing work in a contactless world? One company offers a solution.

How does real estate loan signing work in a contactless world? One company offers a solution.

Stavvy, a platform that empowers businesses and lenders to close real estate loans digitally, has seen a dramatic change in their business landscape since the launch of their E-signing platform in March.

“Over the course of literally a couple of weeks, [states] realized that they had to empower people to be able to do business as usual, despite what was going on,” Co-Founder Kosta Ligris said. “We were able to put all the necessary tools in one platform to empower these title companies, law firms, notaries to have identity solutions when we went live in March.”

Right when the platform came live, contactless signing became a necessity. Kosta Ligris, a co-founder of Stavvy, said his team worked hard to include emergency digital notarization options in states that had not allowed it yet before. The market went from about 20 states with legalized digital signing to 48 that had legalized or created a temporary law.

Stavvy also reached out to engineers and employees who were losing their jobs during the first wave and picked up new hires while many firms were downsizing.

“The pandemic is a once in a lifecycle opportunity,” Kosta said. “I hope that we don’t see anything that resembles COVID again. But this opportunity has given us the chance to get in front of people that we otherwise would not have been able to hire.”

Unlike competitors, Stavvy does not get involved in signing or notarizing themselves, but instead offer a digital platform for both lenders, signers, and state compliance checking. The platform is somewhat like the Uber app Ligris said- they don’t bring a car to you, but they give you a digital way to connect to people who can pick you up.

In many states, especially in New York and New Jersey, complete digital signing is still not allowed. Instead, Stavvy encrypts film of the “wet signing” -ink pen on a document- and sends the encrypted data and other identification guarantees in a live “Zoom-like experience” to the county registry.

Ligris said Stavvy is very passionate about empowering both lenders and signers. As an MIT entrepreneurship resident who looks at student companies and ideas every year, he knows about barriers to entry. He said one such barrier to digitalized innovation is a simple fear of change.

Ligris said Stavvy is very passionate about empowering both lenders and signers. As an MIT entrepreneurship resident who looks at student companies and ideas every year, he knows about barriers to entry. He said one such barrier to digitalized innovation is a simple fear of change.

“Change in and of itself is always frustrating and scary, but it doesn’t necessarily mean that it’s bad,” Ligris said. “In so many industries where people regard technology, they look at it as this is the next thing that’s going to take my job away from me.”

That’s the concept Stavvy is fighting- that digital innovation is not automating away livelihood, but further connecting people. Ligris said that the one thing technology could not replace: broker buyer relationships.

“When it comes down to making one of the largest financial decisions of their life, they want a trusted professional,” Ligris said. “If we’re going to provide the technology, we want to empower the stakeholders that know best to be more efficient and better at what they do.”

Square Makes Jeopardy’s Daily Double

September 17, 2020“What is Square?”

That was the right question to the answer read by Jeopardy host Alex Trebek during an episode that aired this week. Contestant “Beth” hit a Daily Double and waged $2,000 to try and take the lead over “David” and “Joe.”

@Jack, hello pic.twitter.com/zwIzdAyTVT

— Nick D 👨👧 (@ndimichino) September 17, 2020

Square employees reacted on twitter by pointing out that the quoted transaction cost was a little out of date, but mostly took the honorable mention in stride.

We've made it! https://t.co/MZoZofrsno

— Jackie Reses (@jackiereses) September 18, 2020

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

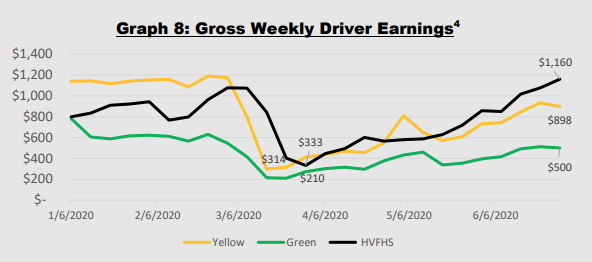

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.

Dwolla Introduces New Push-to-debit Platform

September 17, 2020 Dwolla, an online payments platform, released a Push-to-Debit functionality that they said will allow faster payouts to a debit card and give clients additional flexibility.

Dwolla, an online payments platform, released a Push-to-Debit functionality that they said will allow faster payouts to a debit card and give clients additional flexibility.

“We have been moving money for quite some time,” VP of Product Ben Schmitt said, “In doing so, we’ve learned a lot about what our customers want.”

Founded in 2008, the Dwolla team has worked to incorporate many different ways for their users to move money. They offer same day, next day, and other payment types, but said customers were always looking for ways to transfer funds faster. Now with Press-to-Debit, Dwolla offers a way to shift funds instantaneously, a product that they say fits many use cases.

“It could be the gig economy, it could be online marketplaces, but people want to move funds faster,” Schmitt said. “And I think especially during a pandemic, getting funds quickly adds a lot of value.”

Dwolla wanted to offer the platform’s simplicity with debit speed. Schmitt said the process is PCI security compliant and nearly instantaneous, though it might take up to 30 minutes.

“The value of instant payments is in getting the funds now when you need them, but there’s an emotional response,” Schmitt said. “When you see the funds hit and they’re instant- when you push a button and show up just like that, it’s fascinating.”

It works not just for debit, but prepaid cards, meaning businesses paying employees or customers don’t need a relationship with a bank to get funds transferred.

“If you’re a gig worker and do some work during the day and finished your shift, you can use an app or website and clock out,” Schmitt said. “Then a business has a record of the work performed, and say ok, here’s the agreed-upon payment and issue that to you right away.”

Peter Ribeiro, CEO of US Business Funding – Talks About Experience and Success in 2020

September 17, 2020I recently caught up with Peter Ribeiro, CEO of US Business Funding, based in Santa Ana, California. US Business Funding is quite well known on social media for their company culture.

I asked Ribeiro about what 2020 has been like as a broker in this wild year of 2020 and you can watch it in full below:

Puerto Rican Businesses & People Resilient In Spite of Pandemic and Challenges, Says Alvelo

September 16, 2020 While the US economy slowly opens back up to careful in-person commerce, the territory of Puerto Rico is still facing rising case numbers- So how is business in the “Island of Enchantment?”

While the US economy slowly opens back up to careful in-person commerce, the territory of Puerto Rico is still facing rising case numbers- So how is business in the “Island of Enchantment?”

“I don’t think there’s anything that will shake the confidence of our small business owners in Puerto Rico,” said Sonia Alvelo, CEO of Latin Financial. “Businesses and the people of Puerto Rico are the most resilient I have ever known: I know that as I am one of them.”

Alvelo, a native to the island, has won awards as a top entrepreneur of the year for her business financing partnerships in the US and Puerto Rico. She said that even as the island faces its hardest challenges, the spirit of entrepreneurship remains unbroken.

Puerto Rico has been hit by irregular misfortune in the past couple of years. Destruction from Hurricane Maria and Irma damaged the 2017 infrastructure of the island immeasurably, and the response of the US government was painfully lacking. Commerce continued with caution, seeming to rebound. Then this year, earthquakes and aftershocks punctuated January and February, foreboding the coming storm.

The pandemic was slow to reach the island; Puerto Rico was the first US state/territory to impose a quarantine, banning business and all travel March 15th. The region is a territory of the United States, so it could not directly enforce control over its borders. Recently, Puerto Rico made the news with an increasing case count.

There’s also been the troublesome search for a new governor. After a mass protest, Governor Ricardo Rosselló stepped down last year. After his successor ‘appointment’ was deemed unconstitutional by the Supreme court of Puerto Rico, Wanda Vazquez, the former Secretary of Justice, took office.

In the August primary, thousands of ballots got stuck in delivery trucks that did not move, never reached polling locations. The candidates are now petitioning for a re-vote and the counting of the votes that were cast. The courts are still deciding, so even the election is facing challenges in Puerto Rico.

Besides that, the tourism industry has been devastated. Though the early shut down saved lives, the island saw an unemployment rate of up to 23% in July alone. That could be a low estimate, considering that half of the Puerto Rican workforce hold a job in the “informal economy.” The New York Times reports that the real unemployment rate in the middle of the summer could have reached close to 40%.

Even so, Alvelo conveyed the enduring willpower of the Puerto Rican people, that there was still confidence things would turn around.

Alvelo is partnered with more than 97 pharmacies in Puerto Rico as an MCA provider, as well as with gas stations and other small businesses. She said that she has been receiving calls for business financing options non-stop, on a day-to-day basis. Alvelo shared information she learned from one of her clients.

“They suffered the most at the beginning, but you know only 5-10% of pharmacies in the islands are open,” Alvelo said. “But even still, and we’re talking a hurricane, earthquakes, a pandemic, everything- I still don’t think that anything will change the confidence of business owners in PR.”

Alvelo is standing right next to Puerto Rican business owners, talking to them through their increasing needs during this time, she said. Latin Financial facilitated almost $2 million in PPP loans and $2 million in EIDL loans in the US and PR.

“That was the best experience- when they got the PPP funds,” Alvelo said. “They were crying over the phone; it was incredible.”

Brendan Lynch, Alvelo’s fiancé and business partner, said that the program had a rough rollout. It was unclear how long the Fed money would last, but PPP ended up working well for Puerto Rican businesses. He even saw BlueVine begin funding Loans in PR for the first time.

“One of our finders here in the US was approved for the program, and we were able to use their online platform,” Lynch said. “And normally they don’t really fund in Puerto Rico, but they did allow Puerto Rican businesses to apply for funding; which is great because they had the technology to make it so simple and quick.”

Lynch said Latin Financial was sure to share links to a PPP loan application with every client to make sure aid funds were as accessible as possible.

“Businesses are probably still down-scaled somewhere between 60 to 70% of their total revenue,” Lynch said. “they’re still working shorthanded with less people in the office, and regulations on how many people you can have in your business are making it harder.”

Alvelo and Lynch are no strangers to environmental forces affecting their plans- the pair were planning on getting married in PR in 2017 before the hurricanes hit.

“We started actually looking [for a venue] again, and then COVID happened,” Alvelo said. “Clients were going to be invited and are always asking how they can help, just like when everything happened with COVID, the pharmacies all got together, and said if you need this let us know. Businesses are really working together because they know that they need each other.”

“We started actually looking [for a venue] again, and then COVID happened,” Alvelo said. “Clients were going to be invited and are always asking how they can help, just like when everything happened with COVID, the pharmacies all got together, and said if you need this let us know. Businesses are really working together because they know that they need each other.”

Maria Barzana, the owner of Farmacia Asturias, has been a longtime client of Latin Financial, one of the first dating back to 2015. Barzana went to Alvelo for help. She said the island did not feel an economic impact until this August. Businesses, including most medical offices in the country, have been closed for the past five months. Pharmacies are finally feeling it.

“At the beginning of COVID-19, we were able to manage the economic factor by invoicing refills of prescriptions and the sale of basic necessities related to COVID,” Barzana said. “Due to social distancing, the flow of clients/patients has decreased, concentrating on items necessary to combat COVID-19 and maintenance medications.”

Latin Financial is almost back to regular funding after rushing to help complete PPP and EIDL stimulus loans. Sonia Alvelo will be a panelist speaker this Sept. 24, for the annual Latinas & Power Symposium.

Upstart Welcomes Policy Head Nat Hoopes

September 15, 2020 Upstart, an AI lending platform, welcomed longtime industry advocate Nat Hoopes to the team this week, to lead as Head of Government Policy and Regulatory affairs. Hoopes previously served as the Marketplace Lending Association executive director (MLA), where he grew the trade group and advocated on behalf of its members.

Upstart, an AI lending platform, welcomed longtime industry advocate Nat Hoopes to the team this week, to lead as Head of Government Policy and Regulatory affairs. Hoopes previously served as the Marketplace Lending Association executive director (MLA), where he grew the trade group and advocated on behalf of its members.

“My hope is to bring the energy that I did in growing the organization [MLA] and also just in tackling a lot of different workstreams to Upstart,” Hoopes said. “But also, deepen their ties with the DC policy community.”

Hoopes is excited to join the Upstart team and advocate for the company to state and federal legislators. Hoopes intends to address the development of two main issues as he enters his new office: facilitating better credit reporting with the help of AI, and using better credit to bring financing options to disenfranchised minority communities.

Upstart uses non-traditional data like a college education, job history, and residency to evaluate borrowers for personal loans. The company recently introduced an AI-powered Credit Decision API to deliver instant credit decisions. Upstart added auto loans to the platform in June, so the new API works with personal, student, and auto loans.

Hoopes said he and Upstart shared a similar motivation: to provide credit to people and improve financial futures, especially to people unfairly blocked from receiving credit.

“I think because of the structural inequality that we have in our society, a lot of minority groups get really left behind and stuck in a low credit score environment,” Hoopes said. “By using more data, and using it in new ways with artificial intelligence we can really level the playing field.”

Hoopes said that he has already seen Federal regulators in the FDIC and the OCC, and the CFPB working on using AI learning in credit underwriting. He said the Fed is planning out how to help banks adopt more of these models to approve more people.

“I think that’s a key initiative,” Hoopes said. “A key area where I’ll be working for Upstart: Engaging with regulators on how to help banks get more comfortable in serving more customers,”

While advocating for banks to use the credit capabilities of partners like Upstart, Hoopes said he would be devoted to ensuring decisions are made with equality and inclusion in mind. Hoopes will stay on as a member of the MLA board, and working in concert with his responsibilities advocating at Upstart.

“At MLA, I helped develop the diversity and inclusion strategies for our part of the fintech industry,” Hoopes said. “I’ll remain active on those issues at Upstart both collectively with other members of the industry as a member of the MLA.”

Hoopes referred to the Diversity and Inclusion strategy released by MLA last month. Board members signed off on the paper, written with the help of the National Urban Leauge. League president and CEO Marc Morial and Representative Gregory Meeks (D-NY) to create a vision of an inclusive fintech industry.

Hoopes addressed what he said was the failure of the American credit scoring system. For instance, according to Upstart’s study in 2019, 80% of Americans have never defaulted, yet only half have a prime credit score. It’s a problem he says disproportionately affects minority borrowers.

According to a Federal Reserve study, more than three times as many Black consumers (53%) and nearly two times as many Hispanic consumers (30%) as White consumers (16%) are in the lowest percentiles of credit scores.

Hoopes said Upstart does not collect racial data from applicants but cites a CFPB test that found Upstart’s platform increased access to credit across race and ethnicity by 23-29% while decreasing annual interest rates by 15%-17%.

University of Delaware, Other Universities Going Long on Fintech

September 15, 2020The University of Delaware recently received a $9 million tax incentive to construct a new Fintech Center on its premier Science, Technology, and Advanced Research (STAR) campus, with help from a community-building company Cinnaire. Slated for completion in 2021, the building marks yet another fintech-focused resource for higher education.

Financial technology programs have long been offered at prominent business schools such as Harvard, Stanford, and Columbia, international schools such as Oxford, and research institutions like MIT since the late 2000s.

Now that fintech has become a long term value creator in the financial world, other institutions such as the University of Michigan, Fordham, and Delaware are excited to implement fintech opportunities on campus for undergraduate and graduate students alike.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

Discover Bank and Cinnaire jointly funded the building, a $39 million project. According to Delaware plans, it will create a space on the Delaware STAR campus to host a new Financial Services Incubator to encourage research and collaboration between students and industry leaders.

“The FinTech building will bring together computer science, engineering and business experts in cybersecurity, human-machine learning, data analysis, and other emerging financial technologies,” said Levi Thompson, Dean of the College of Engineering. “These collaborations will allow us to provide our students with a very unique experience that prepares them to excel in the workforce. Furthermore, our Fintech discoveries will benefit people throughout Delaware and the world.”

Cinnaire is a national nonprofit that focuses on improving communities’ financial health by creating capital solutions to revitalization projects: lending funds, managing, and building housing structures.

Funding communities is what Cinnaire does best: in this case, utilizing a New Markets Tax Credit to fund an addition to the Delaware campus.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The nearby University of Fordham at Lincoln Center has also been trending toward preparing students for a fintech world. Undergrad and graduate students pursuing an MBA through the Gabelli School have the option of a fintech concentration.

The course work not only incorporates data science and machine learning skills into the worlds of credit lending and risk management but facilitates relationships between students and a wealth of industry partners.

Sudip Gupta, professor, and Director of the MS Quantitative Finance program, spoke about the courses’ popularity there. The program is ranked in the top 20 of its kind in the world by Risk Magazine.

He has seen a revolution in fintech in the past few years that has recently received a big push by pandemic forces, introducing the wholesale adoption of fintech techniques into traditional financial institutions.

“The fintech revolution in the industry- big data, machine learning techniques, storage capacity, and cloud computing has been going on for the last couple of years,” Gupta said. “The pandemic provided the big push to move toward that direction.”

Gupta has been following the development of alternative credit closely, recently publishing an award-winning paper studying machine learning to create alternative consumer credit scores using mobile phone and social media data.

“The idea of my research- let’s look at people who do not have a credit history or enough traditional credit you could get from a FICO score,” Gupta said. “Using this data, it turns out they are better predictors, and better to judge than FICO, and can reach out to more people.”

Gupta is excited for the adoption of big data techniques into alternative and traditional consumer loans because it offers a win-win for consumers and institutions alike, he said. Echoing the findings of many successful alternative finance companies, Gupta said his research showed that collected data could offer better insight for lending than “stale FICO scores.”

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Up north at the Univerisity of Michigan, Professor Robert Dittmar at the Ross School of Business heads the Fintech Initiative. He is working on adding even more fintech classes. Recently, through a partnership with PEAK, a Chicago fintech lending company, Michigan launched a fintech initiative that incorporates undergrad and grad classes, faculty research, and a fintech entrepreneurial club that connects students to industry leaders.

Michigan Ross is adding fintech classes for a variety of reasons.

“The simplest reason: students are interested in learning more about this kind of space,” Dittmar said. “And we’re seeing more demand from the industry side for students that know more.”

For years Dittmar said tech companies and startups in silicon valley were pioneering innovations in the industry. Through talking with alumni and contacts in the industry, Michigan found that fintech has gotten to the place where there is an excellent supply of data engineers. Still, there is a demand for professionals with the financial business expertise to implement these technologies.

“What we are trying to do at Ross is fill in that gap,” Dittmar said. “what we’d like is for [students] to know enough about the technology that they can provide the insights of finance and business to the people that are doing that technical work.”

At Ross, they are organizing what will one day be like a fellowship program. The program will feature a combined learning experience: students will learn data analytic finance, apply their computing skills in credit decision making classes, and then connect with the industry in experiential learning classes.

“In the last couple of years, I have been taking students to London to work at fintech startups in the UK,” Dittmar said. “And we are hoping to expand that program so that most or all graduate students have the opportunity to participate in something like that.”

Last year Ross hosted a “Fintech Challenge” competition to design a banking service to reach customers in a “banking desert” in rural Michigan. The program is hoping to host another challenge this year, despite complications of COVID-19.