Archive for 2018

War on Debt Settlement Continues: 16 Defendants Sued in RICO Case

September 6, 2018

Fourteen individuals and two companies (including Decision One Debt Relief) were sued by Funding Metrics in Federal court last month for allegedly “conducting a nationwide illegal debt restructuring scheme through numerous acts of mail and wire fraud.”

The suit, which stems from the defendants’ interference with Funding Metrics’ merchant cash advance customers, makes six claims, among them financial damages resulting from state and federal crimes. Per the complaint:

“Defendant Decision One (along with its affiliate/alter ego D1 Servicing) fraudulently presents itself as being able to renegotiate and restructure merchant agreements with Plaintiff and other funding companies. It has established a deceptive business practice of making misleading and often outright false representations to merchants under contract with Plaintiff promising that, with its help, these merchants will save money on those contracts by defaulting on them. Decision One tells merchants that they can safely stop paying cash advance funding companies like Plaintiff; that it will go to work for them promptly; that it can reduce their debt by 60-80% or more; and that they will be provided with a Veritas insurance plan to cover legal expenses arising from their defaults, once cash advance companies exercise their rights under agreements with their merchants, as they inevitably will. Based on these misrepresentations, the merchants default on their contracts with their funders – that is, at Decision One’s direction, they stop paying their funders and instead pay Decision One – although Decision One does not even expect to achieve results for the merchants. The result is a fraud on the merchants and tortious interference with the contracts Plaintiff have with them.”

The suit is just the latest bomb dropped on the exploding debt settlement industry. deBanked began covering the controversy surrounding debt settlement in late 2016 after the owner and employees of an upstate New York debt settlement company were arrested for charging merchants to restructure their merchant cash advances and then not actually performing any services. The owner, Sergiy Bezrukov, was charged with money laundering, bank fraud, mail fraud, wire fraud and conspiracy to defraud. Bezrukov has been locked away in jail for almost two years awaiting trial. He is facing a maximum of 30 years. Two of his employees pled guilty, Vanessa Cardona to bank fraud and Dustin Walker to conspiracy to commit bank fraud.

Since then, nearly a dozen major lawsuits have been filed by merchant cash advance companies against other debt settlement companies that are alleged to be carrying out similar schemes. One of those sued companies, NJ-based Corporate Bailout LLC, was featured on the cover of the New York Post last summer for being “the craziest office in America.” Corporate Bailout was sued by both Yellowstone Capital and Everest Business Funding which later resulted in a very public settlement agreement that forced Corporate Bailout to fork over $500,000 to the two MCA companies.

Decision One Debt Relief, sued now by Funding Metrics, was also originally a co-defendant alongside MCA Helpline in a lawsuit filed by Everest Business Funding earlier this year. In February, after determining the two were not related, Everest dropped the claims against Decision One only. The suit against MCA Helpline is still pending.

Around that same time, a representative for Decision One revealed to deBanked that the company was on track to be doing more than $100 million a year in business.

Bezrukov, by contrast, who currently resides in a Niagara County New York jail, is accused of having only obtained $1.2 million throughout his entire debt settlement venture’s existence. Although Decision One is not being charged criminally, the private civil suit alleges damages caused by a violation of criminal statutes including RICO.

The Funding Metrics suit against Decision One was filed in the Southern District of Florida under ID# 9:18-cv-81061.

CAN Capital to Grow Team and Business with New Facility

September 5, 2018 CAN Capital CEO Parris Sanz at Broker Fair May 2018

CAN Capital CEO Parris Sanz at Broker Fair May 2018CAN Capital announced today that it agreed to a financing transaction of up to $287 million, provided by Varadero Capital. This is CAN Capital’s second facility with Varadero Capital. The first one came in July 2017. This financing will be used to fund more small business loans and to invest in talent and technology to enhance customer experience. The company plans to grow the size of its team with this new facility.

“We look forward to utilizing this funding to expand our ability to provide access to capital for small businesses, enhance our technology stack, and continue to build a dedicated, customer-driven team,” said Parris Sanz, CEO of CAN Capital.

CAN Capital also announced today that it has now provided small businesses with access to over $7 billion of working capital through more than 190,000 funding transactions with over 81,000 small business owners.

“Reaching $7 billion in working capital is a significant milestone for us,” Sanz said. “We are excited to use our deep experience and data to enable even more small business owners to grow with streamlined access to capital.”

CAN Capital makes business loans from $2,500 to $250,000 that last between 6 and 18 months. And they provide merchant cash advance financing, also from $2,500 to $250,000. They also work with broker partners to fund deals.

Founded in 1998, CAN Capital is among the oldest alternative lending companies. After an issue plagued them in 2016, the continued growth and confidence in the company from Varadero Capital is noteworthy. The company is now growing when it was making layoffs less than two years ago. Currently, CAN Capital’s headcount is 142.

“Since our initial facility, we’ve been impressed by the work ethic and dedication of CAN Capital’s staff, which have driven consecutive quarters of business growth and boosted confidence in the company’s fundamentals,” said Fernando Guerrero, Managing Partner and Chief Investment Officer at Varadero Capital.

BFS Capital is a Sponsor of deBanked CONNECT – San Diego

September 4, 2018BFS Capital is a sponsor of deBanked CONNECT San Diego. The half-day event for funders, lenders, brokers and industry professionals is being held at the Andaz on October 4th!

Check out photos from deBanked’s past CONNECT event in Miami

Bitty Advance is a Sponsor of deBanked CONNECT – San Diego

September 4, 2018Bitty Advance is a sponsor of deBanked CONNECT San Diego. The half-day event for funders, lenders, brokers and industry professionals is being held at the Andaz on October 4th!

Check out photos from deBanked’s past CONNECT event in Miami

The Broker: How Copelon Kirklin Became a Dealmaker

September 3, 2018 Title: President of KPC Group, one man broker shop.

Title: President of KPC Group, one man broker shop.

Location: Kenner, Louisiana. Fifteen minutes outside of New Orleans.

What’s your morning routine?

I wake up at 6. I get a quick breakfast. I check my emails and then on to phone calls.

What keeps you going throughout the day?

My gasoline is my family. They’re my coffee, my 5-hour energy. They’re my motivation because I know what I want to give them. I’ve been able to accomplish some things in this business and [be able to] provide some of things for them… So no coffee here. Just the family. That’s my fuel.

Biggest deal?

$2.5 million deal. It was an SBA loan and I had 1 point in it. So I made a $25,000 commission.

What are a few of your biggest challenges as a broker?

If I’m dealing directly with a merchant, at the beginning, the way they represent themselves on paper regarding their revenue – everything looks good. And then when the actual bank statements come through, it doesn’t match up. I mostly work with construction contractors. It’s a niche and it’s pretty simple. But it’s only simple if [merchants] don’t misrepresent their financials, if they’re telling the true story.

Also, I don’t mind working with brokers…it doesn’t matter if you’re in the deal 50-50 or you’re just passing me a deal of a friend…I pay 50% every time, because I want to foster more relationships and get more deals that way. The challenge is when the co-broker can’t let go of the client to let me deal with them. It’s when they want to be the go-between. When they want to communicate through me to the client and it just doesn’t work that way. I haven’t closed any deals when another broker tries to work that way.

Could you tell me about your first deal?

Could you tell me about your first deal?

2014 was the first time I closed a deal in finance…and I only made $500. But I tell you, it was the best thing that happened to me because it let me know that it was possible. There was this one moment when I was really questioning “am I supposed to be doing this?” And I’ll never forget that day. I was sitting in my bed and I just had this look on my face and my wife asked me what was wrong and I told her “I don’t know if this is for me because I’ve been doing this for [a few] years and nothing’s happened yet.”

And to my surprise, she said “pick up that laptop, open it back up and you get back to work. It’s going to work out. You’re not doing this in vain.” And lo and behold, two weeks later, I closed that first deal at $500 [in commission], and the next week I closed two deals, one for $1,100 and one for $1,400. And I was just on my way from that point.

How did you learn to be a broker?

I learned from the internet. I found leads organically because I didn’t have any money for leads. LinkedIn was my best friend at the time and it’s still my go-to. It was where I learned that people are willing to do business with you without meeting you. I got hooked on it – developing my profile, adding to it, learning, making mistakes, chasing pipe dreams. [Those many months] before closing my first deal were just a lot of growing pains.

How do know when something isn’t real on LinkedIn?

It’s really about learning to do due diligence and not taking people at their word, even though you would love to. You check out their background. Do they just have a personal email address? That’s not always a killer, but it does help if they have a corporate email address if they’re telling you that they’re a lender. Learning that someone is actually a broker when they’re saying that they’re a lender. Checking Ripoff Report, seeing if [someone] has a website, learning to tighten my filter. In the beginning, you want it to be easy. You want to take people at their word. And I fell for [tricks]. But you have to do your homework.

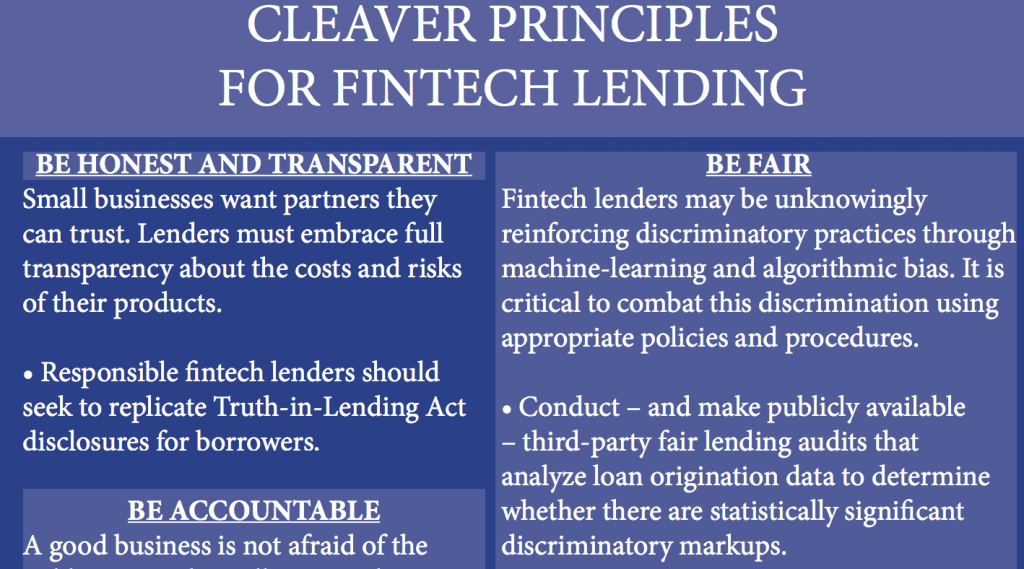

Congressman Cleaver’s Findings on Fintech Lending Mixed

August 30, 2018 Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Cleaver concluded that some common practices in non-bank underwriting processes lend themselves to discrimination against minority business owners. One such practice is using a merchant’s personal credit score to determine a business’ credit worthiness, which the report maintains is unfair because “a personal credit score has little bearing on a business model or the owner’s business acumen, and using it unfairly punishes minority business owners who may not have had the same opportunities to build credit.” Another complaint is the common practice of having merchants sign forced arbitration clauses that forbid the borrower to take the lender to court.

The companies that he surveyed included OnDeck, Kabbage, Fora Financial, Lending Club, Biz2Credit and LendUp, even though Lendup only does consumer lending. And OnDeck, Kabbage and Lending Club don’t offer a cash advance product. Still, they make non-bank business loans.

The report also mentioned that algorithms used by some of these companies could inadvertently be discriminatory. That’s because they have the ability to incorporate the number of criminal records and bankruptcies in the merchant applicant’s zip code when making a funding decision. And these numbers tend to be higher in minority neighborhoods.

However, the report also highlighted some good practices, such as including a third party in the lending process to protect from engaging in unintentional discriminatory behavior.

“From the responses gathered,” the report reads, “it has become increasingly clear that a majority of the companies have taken some measure to prevent blatant discrimination. Nevertheless, additional protections are very much needed.”

“The initial findings are clear as day, Congressman Cleaver said in a statement about the report. “We need to further understand how lenders may be intentionally or unintentionally offering higher interest rates to minorities and underserved communities, and work to implement industry-wide best practices.”

The California Business Loan & MCA Disclosure Bill Has Passed

August 30, 2018The bill has passed. With the governor’s signature, all business loan contracts and merchant cash advance contracts in California will soon require a uniform set of formal disclosures including an annualized rate of the total cost. The precise formula for that rate will be determined by the state’s regulatory agency, the Department of Business Oversight.

Update: The bill’s death in committee was challenged by the bill’s author, Senator Steve Glazer, and ultimately allowed to come up for a vote after he complained to the senate majority leader that a committee’s decision is merely a recommendation, not a deciding factor on the bill itself. At 2:10 AM EST, it passed.

Update: The bill has died in the Senate Banking Committee. Daniel Weintraub, who serves as chief of staff to the bill’s author, tweeted after midnight eastern time that the bill was not moving forward.

Thanks to all who supported small business and #SB1235. Unfortunately the Senate Banking Committee killed the bill tonight. We fell one vote short of the four we needed to send the bill to the Senate floor. https://t.co/30ztdW2LbD

— Daniel Weintraub (@DMWeintraub) September 1, 2018

Update: The bill passed the Assembly unopposed and is slated for a late night vote by the Senate Banking Committee.

Update 8/31/18: Today is the last day for the legislature to pass this bill. We will keep you updated

California’s bill to mandate certain disclosures on business loan and merchant cash advance contracts is looking a little bit worse. The Annualized Cost of Capital method (Explained here) that some folks in the industry were accepting of, has been scrapped in favor of whatever formula a state regulator decides to pick. That means if the Commissioner of Business Oversight decides on an APR disclosure, which many industry trade groups believed they had already successfully lobbied against, all loans and non-loans alike would have to report an APR, a mathematical impossibility for a product like merchant cash advance. At present, however, all that is known is that the Commissioner’s choice must be an annualized metric.

According to Bloomberg, the amended version of the bill needs to get approval in both the Assembly and the Senate by Friday before the legislative session ends.

Trade associations that have weighed in on this bill include the Electronic Transactions Association, Commercial Finance Coalition, Small Business Finance Association, and the Innovative Lending Platform Association.

You can view all of our previous coverage about the bill here.

1 Global Capital Charged With Fraud by SEC

August 29, 2018

The Securities & Exchange Commission unsealed a 10-count complaint against 1 Global Capital LLC (“1st Global Capital”), its owner Carl Ruderman, and related parties on Wednesday.

The South Florida firm “fraudulently raised more than $287 million from more than 3,400 investors to fund its business offering short-term financing to small and medium-size businesses,” the complaint begins.

Investors were offered low-risk, high-return investments that 1st Global would use to fund merchant cash advance deals. Ruderman, who owned the company through a trust, misappropriated $35 million of the funds, paying a lot of it to himself and companies he controlled that had nothing to do with MCA, the SEC alleges. Beyond that, millions more went towards other pet projects like a $50 million purchase of distressed credit card debt.

But the deception went deep, the complaint lays out. 1st Global touted a default rate of only 4% despite the fact that 15-18% of their deals over the last 2 years had resulted in collections lawsuits.

By October 2017, the statements investors received showing their monthly performance were faked with the value and performance significantly inflated. By June 2018, one line item on monthly statements (labeled “cash not deployed”) reported that investors collectively had $70 million in idle cash ready to be put into deals. Meanwhile, the company itself only had about $20 million in all of its bank accounts combined, money that was being used for everything including operating expenses, salaries, and commissions.

1st Global’s alleged auditor, Daszkal Bolton, LLP, says they never audited 1st Global’s statements and haven’t had anything to do with the company since 2016. Nonetheless, 1st Global placed Daszkal Bolton’s name on statements given to investors and stated on their website that investor balances were validated by an accounting firm quarterly.