Archive for 2018

Square Expands into Consumer Lending, Keeps Banking Hopes Alive

October 16, 2018 Square is no stranger to payments and is looking more and more like a bank every day. Square Capital already facilitates loans to small businesses, and now they’re expanding into consumer loans. Meanwhile, it’s been several months since Jack Dorsey’s fintech startup withdrew its application to become an Industrial Loan Company (ILC), but Square’s banking pursuits appear far from over.

Square is no stranger to payments and is looking more and more like a bank every day. Square Capital already facilitates loans to small businesses, and now they’re expanding into consumer loans. Meanwhile, it’s been several months since Jack Dorsey’s fintech startup withdrew its application to become an Industrial Loan Company (ILC), but Square’s banking pursuits appear far from over.

“With regard to charters, Square Capital is uniquely positioned to build a bridge between the financial system and the underserved, and we continue to work closely with the FDIC and Utah DFI on our ILC applications,” a Square spokesperson told deBanked.

In the interim, Square is making a push into consumer lending, giving small businesses the opportunity to capture big-ticket sales that might otherwise slip away. After testing the feature for about a year, Square Installments has now been rolled out across 22 states with plans for a nationwide expansion.

“Historically, offering financing options for customers has only been available to larger businesses. For many Square sellers, providing a payment option like this to customers has either not been possible, or has been too complicated or time/labor intensive to set up. We are focused on expanding access to financial services for both businesses and individuals, and Square Installments sits at the intersection of both,” the spokesperson said.

Square Installments will further diversify the company’s revenue stream and build on the momentum that they have been experiencing with business loans. The new product offers customers more flexibility for purchases between $250 and $10,000, giving them the option to pay over three, six or 12-month installments at an APR of up to 24%.

“We noticed there were a lot of very high-ticket purchases on Square and sellers were saying that they might lose a sale because a national chain might offer financing,” according to the spokesperson. Over the past year, Square facilitated tens of millions of transactions for purchases of more than $250.

And it isn’t just merchant demand. Small business customers similarly are hunting greater flexibility and more financing options for budgeting purposes, according to a survey of American consumers done by Square over the summer.

Square Installments works at both the point-of-sale for brick-and-mortar businesses as well as with Square Invoices for e-commerce companies. Other fintechs that offer similar consumer lending solutions include Affirm, GreenSky and Klarna, as Reuters pointed out.

For sellers, Square Installments can be integrated into their existing Square offerings. The seller is not engaged in the credit decision process and is paid for the sale up front.

By giving customers the ability to pay in installments, small businesses can increase their sales, bolstering growth in the process. Square gives the example of Fly1 Motorsports, whose sales increased between 20%-30% while order values increased by more than 50% as a result of Square Installments.

Square has a history with the sellers on its platform, which delivers greater transparency to the credit decision process. The loans, however, will be added to Square’s balance sheet, a risk that was reflected in declines in Square’s stock price on the heels of the announcement. Square (SQ) shares are down 22% so far in October. The declines also coincided with the departure of Square’s CFO, Sarah Friar.

“From a risk perspective, we look at two types of risk — fraud and credit. At Square, we start with an advantage since we know the sellers we are bringing on to the Square Installments program given they are already processing with Square. We have visibility into what they sell, their average ticket size, and any chargebacks,” the Square spokesperson explained.

On the consumer credit risk side, Square uses machine learning and other tools to provide what it describes as a “holistic view of our borrowers.”

OnDeck Launches New Subsidiary

October 16, 2018 OnDeck announced today that it has created a new subsidiary, called ODX, which will help banks become more efficient online lenders. OnDeck’s CEO Noah Breslow told deBanked that ODX is an expansion of OnDeck’s successful partnership with JPMorgan, which started in 2016.

OnDeck announced today that it has created a new subsidiary, called ODX, which will help banks become more efficient online lenders. OnDeck’s CEO Noah Breslow told deBanked that ODX is an expansion of OnDeck’s successful partnership with JPMorgan, which started in 2016.

“We created what at the time was I think a pretty groundbreaking partnership with the largest bank in the country,” Breslow said. “Now today, we’re funding loans very efficiently using our platform and [Chase’s] marketing and their balance sheet. And it really is sort of the promise of a fintech working with a bank. So we decided strategically this year to really make a big bet in this area…[and create] a company that’s going to support many banks.”

OnDeck has chosen Brian Geary to serve as president of ODX. Breslow said this is because Geary launched and oversaw the collaboration with Chase, whereby OnDeck built a digital bank originations platform for the bank.

“Geary has really been the focal point of that entire effort,” Breslow said, “so he was a very natural choice to head this up.”

OnDeck has drawn talent from among its existing employees to create this company, but it also hired Raj Kolluri to serve as Head of Product and Technology for ODX. And Geary said they are actively hiring to build the team. Kolluri comes from SS&C Primatics, a software company, where he served as Vice President of Product and Engineering, helping to build the company’s software as a service analytics platform for banks.

When asked if helping banks to become faster online lenders is a way of aiding OnDeck’s own competitors, Geary said he didn’t see it that way.

“We don’t view it as competitive,” Geary said. “The banks and OnDeck are playing in different segments of the market. [Banks] have a tighter risk tolerance and certain customers they can serve. So we’re enabling them to serve those customers more efficiently.”

Breslow said that ODX, which he described as “a company within a company,” will soon be announcing its next bank partnership.

ODX will operate within the offices of OnDeck, including its offices in New York, Arlington, VA and Denver, CO.

Sean Murray to Moderate Best Practices Panel at New York Institute of Credit Event

October 15, 2018deBanked President and Chief Editor Sean Murray will be moderating a best practices panel at the New York Institute of Credit Event on October 16th. The event is also supported by the IFA Northeast, the Alternative Finance Bar Association, and deBanked.

The subject of the panel is to discuss best practices when dealing with different financial firms, namely ABL, factoring, and merchant cash advance. The panelists are:

- Bill Gallagher, President, CFG Merchant Solutions

- Bill Elliott, President, First Business Growth Funding

- Raffi Azadian, CEO, Change Capital

- Dean Landis, President, Entrepreneur Growth Capital

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

Congressman Tom MacArthur Visits CFG Merchant Solutions’ NYC Office

October 15, 2018United States Representative Tom MacArthur, who represents New Jersey’s 3rd District, visited the NYC office of CFG Merchant Solutions on Monday. MacArthur has been in office since 2014.

CFG Merchant Solutions moved into the 180 Maiden Lane office earlier this year. The company is a member of the Commercial Finance Coalition (CFC). Adam Sloane of Cresthill Capital, another CFC member, was also in attendance.

NJ Legislature Aims to Classify Merchant Cash Advance as a Loan in New Disclosure Bill

October 15, 2018 S2262 in New Jersey, a bill to require disclosures in small business lending, was amended this afternoon to define merchant cash advances as small business loans for the purposes of disclosure.

S2262 in New Jersey, a bill to require disclosures in small business lending, was amended this afternoon to define merchant cash advances as small business loans for the purposes of disclosure.

Banks and equipment leasing companies are exempt from the bill.

You can listen to the hearing here. Debate on S2262 begins at the 6 minute, 12 second mark.

The bill’s author (image at right) is Democratic Senator Troy Singleton who represents New Jersey’s 7th legislative district.

Testifying on Monday’s hearing against the bill were Kate Fisher of the Commercial Finance Coalition and PJ Hoffman of the Electronic Transactions Association.

New Jersey Moves to Regulate Small Business Loan Disclosures and Brokers

October 15, 2018 A committee within the New Jersey State Senate convened today at 1:30pm to discuss S2262, a new small business loan disclosure bill. Similar to SB1235 in California, this bill would require all of the following on small business loan contracts less than $100,000:

A committee within the New Jersey State Senate convened today at 1:30pm to discuss S2262, a new small business loan disclosure bill. Similar to SB1235 in California, this bill would require all of the following on small business loan contracts less than $100,000:

The APR(This was removed during the committee hearing)- The annualized interest rate

- The finance charge

- The maximum credit limit available

- The payment schedule

- A list of all broker fees and a description of the broker’s relationship with the lender and any conflicts of interest the broker may have

- These terms must be presented before a business accepts a loan

In addition, any change to the terms that would significantly affect the responsibilities or obligations of the small business concern under the loan must be noticed 45 days in advance.

During the hearing, the bill was amended to define merchant cash advances as small business loans. Kate Fisher of Hudson Cook, LLP who represented the Commercial Finance Coalition (CFC) during the hearing, strongly opposed that amendment. The CFC is a trade association representing small business lending and MCA companies.

Also testifying against it was PJ Hoffman of the Electronic Transactions Association. Other Trade groups are gearing up to oppose the bill as well, deBanked has learned.

The bill was voted through the committee and will continue to move forward.

Kate Fisher’s testimony has been transcribed below:

Senator Pou and committee members: Thank you for the opportunity to present testimony today regarding business loan disclosures.

My name is Kate Fisher and I am here today on behalf of the Commercial Finance Coalition, a group of responsible finance companies that provide capital to small and medium-sized businesses through innovative methods. I also am an attorney who helps providers of commercial financing comply with state and federal law.

The Commercial Finance Coalition supports efforts to make business financing more transparent.

The problem is the proposed amendment would define a merchant cash advance as a loan. A merchant cash advance is not a loan.

We all know how a loan works – the lender advances money and the borrower promises to pay it back.

A merchant cash advance is a factoring transaction, in which a business sells a percentage of its future receivables at a discount.

Take for example, a pizza shop. The pizza oven breaks and the owner needs cash to replace it.

In a loan, the pizza shop borrows the money and promises to pay the money back to the lender with interest.

In a merchant cash advance, the pizza shop sells its future receivables to a merchant cash advance company. In exchange for the money to buy that pizza oven, the merchant cash advance company will take 10% of each dollar the pizza shop makes.

If the pizza shop’s sales go down, it will pay less. If the pizza shop’s sales go up, it will pay more. And if the pizza shop is damaged by a hurricane and has to close for repairs, it will pay nothing until it can reopen its doors.

This uncertainty of repayment is why a merchant cash advance is not a loan – the pizza shop in our example, only pays if it sells pizza. Courts have overwhelmingly agreed that a merchant cash advance is not a loan. To quote a recent court decision:

“Receivables purchasing is an accepted form of business transaction, and is not a loan.”

Because a merchant cash advance is not a loan, and there is no fixed payment term, requiring an APR or annual interest rate disclosure would be misleading. For a small business looking for financing, these types of disclosures would only add confusion.

I’m very optimistic that New Jersey can lead the way in providing businesses with disclosures that are helpful – and not misleading.

Thank you.

How Dealstruck Arrived, “Disrupted,” and Died – A Cautionary Online Lending Tale

October 14, 2018Dealstruck just wanted to be loved.

When Dealstruck popped up on the online lending scene in 2013 with promises of long term loans and low interest rates, some industry insiders rolled their eyes at the naïveté. “It’s not about disintermediating the banks but the very high-yield lenders,” Ethan Senturia, chief executive of Dealstruck, told the New York Times in March 2014.

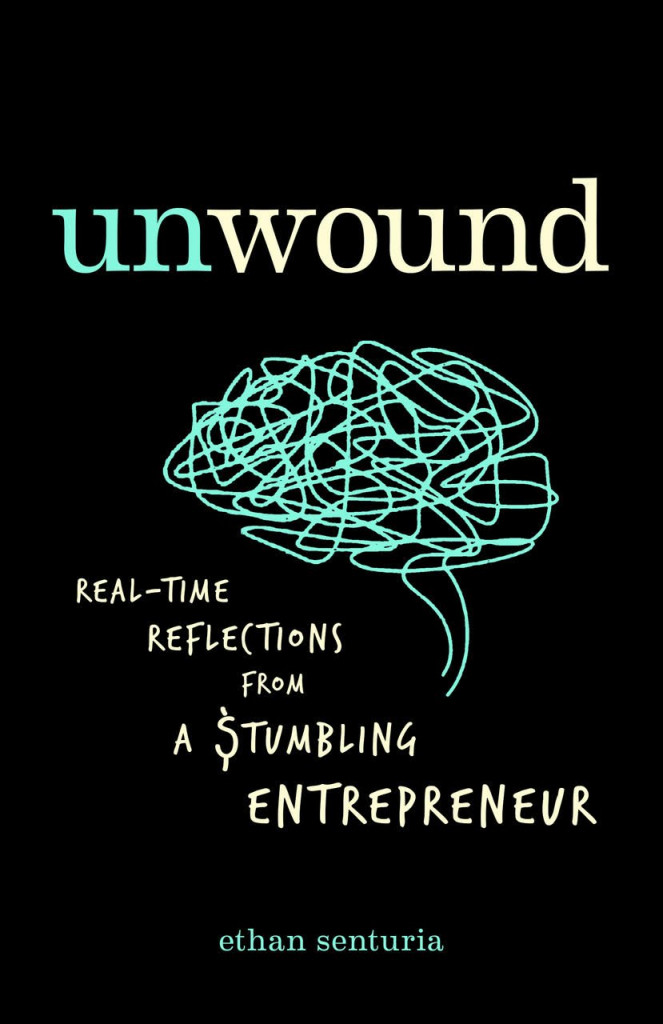

A self-described member of the “lucky sperm club,” a not-even 30-years-old Senturia went on to successfully raise $30 million of investor capital to fund his business, enough to fuel his rise and price-shame his competitors for years. But it wouldn’t last, as he detailed in book, Unwound, about the behind-the-scenes chaos that ravaged Dealstruck until the company closed for good in late 2016.

A self-described member of the “lucky sperm club,” a not-even 30-years-old Senturia went on to successfully raise $30 million of investor capital to fund his business, enough to fuel his rise and price-shame his competitors for years. But it wouldn’t last, as he detailed in book, Unwound, about the behind-the-scenes chaos that ravaged Dealstruck until the company closed for good in late 2016.

“We had taken to the time-honored Silicon Valley tradition of not making money,” Senturia recalls. “Fintech lenders had made a bad habit of covering out-of-pocket costs, waiving fees, and reducing prices to uphold the perception that borrowers loved owing money to us, but hated owing money to our predecessors.” The use of italics are his own.

During Dealstruck’s rise and fall, a journey that reads like an ever-frantic race to raise more money before collapsing, Senturia actually pauses to self-reflect if Dealstruck was becoming a Ponzi scheme. “When does a business go from legitimate but unsustainable to being a Ponzi?”, he pondered before rationalizing that he had not and would not cross that threshold.

At times, the company resigned itself to being a technology play for would-be-acquirers, one of whom included CAN Capital in 2014 when Dealstruck was only originating $3 million a month in loans. Senturia recalls, “For an unprofitable company that had raised $3.5m of equity and whose systems capabilities hadn’t evolved far beyond processing payments on term loans, it would have been tough to make a financial argument that we were worth much more than the capital we invested–$10m soaking wet. But CAN was doing different math. They were trying to go public.”

In Senturia’s view, CAN was trying to check the technology box on the way to an IPO. The offer was $33 million, $13 million in cash and $20 million in pre-IPO stock. Dealstruck first accepted the offer and then ultimately turned it down. CAN never had their IPO.

Dealstruck continued on, rapidly expanding while dealing with major defaults, one of which included an $800,000 loan, the largest deal they ever did at the time, that turned out to be completely fraudulent. One of their early investors never forgave the hiccup and by May 2016, when the online lending bubble was bursting, due in part to the Lending Club scandal, Dealstruck became a poster child for the overheated market.

Case in point, Senturia was mocked during an investor presentation as one individual stood up and asked who in the room would even invest $10,000 into Dealstruck let alone the millions they were seeking. Nobody raised their hand. It was a sign of the times.

At the end, Dealstruck’s dire situation had become entwined with a hedge fund that could not afford to let Dealstruck fail. Senturia referred to their predicament as “mutually assured destruction.” When Senturia warned the hedge fund manager that the game was finally over, it did not go well. “I am like, literally staring over the edge. My life is over,” the hedge fund manager tells him. Dealstruck died. The hedge fund survived.

What Senturia left in his wake were dozens of lost jobs, unpaid vendors, and a cautionary tale he feared nobody would even remember. His book makes sure that nobody will forget.

Though Dealstruck’s failed business could be summed up by bankers as an 180-page “I told you so,” Senturia, concedes throughout that he was learning major lessons along the way. After all, he was only in his twenties and all too self-aware that his family relationships, education (Wharton), and luck played a role in making Dealstruck possible in the first place. Besides, Senturia could easily be telling the tale of many other online lenders of that generation; Lose money, scale, raise capital, shame the competition for their high rates or slow speed, and hope that someone buys you up or you go public.

While it’s a quintessential Silicon Valley story, there are plenty of nuggets of wisdom Senturia sprinkles in along the way that would be valuable to any entrepreneur. It’s also a must-read for anyone interested in lending or fintech. If you were in the business during those years, you probably know some of the characters firsthand. You can buy the book on Amazon here.