Archive for 2017

New FCC Chairman Ajit Pai Has Been Critical of Serial TCPA Plaintiffs, Record Shows

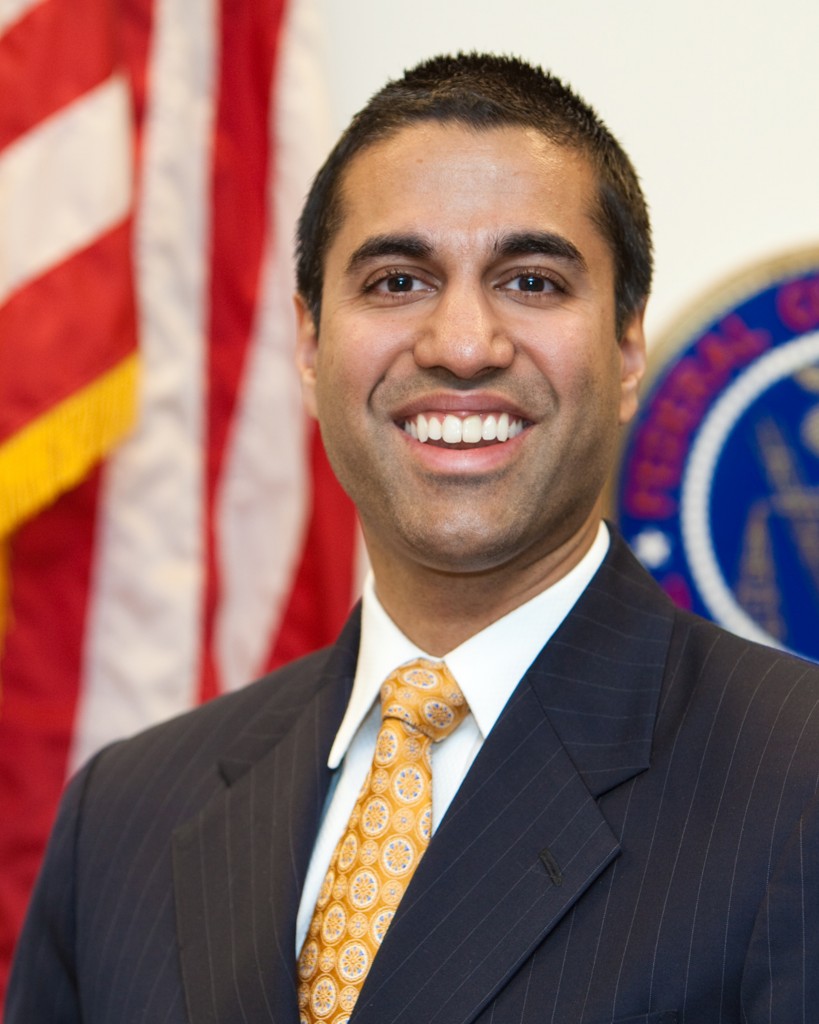

January 24, 2017 FCC Commissioner Ajit Pai is the commission’s new chairman, thanks to President Trump. A republican who believes free markets are better for American consumers than highly regulated ones, Pai is likely to offer a sympathetic ear to companies besieged by serial TCPA plaintiffs, a problem that has reached epidemic proportions in the small business finance industry.

FCC Commissioner Ajit Pai is the commission’s new chairman, thanks to President Trump. A republican who believes free markets are better for American consumers than highly regulated ones, Pai is likely to offer a sympathetic ear to companies besieged by serial TCPA plaintiffs, a problem that has reached epidemic proportions in the small business finance industry.

In 2015, when the FCC announced a broader definition of an autodialer under the TCPA, Pai strongly dissented.

Instead, the Order takes the opposite tack. Rather than focus on the illegal telemarketing calls that consumers really care about, the Order twists the law’s words even further to target useful communications between legitimate businesses and their customers. This Order will make abuse of the TCPA much, much easier. And the primary beneficiaries will be trial lawyers, not the American public.”

– Ajit Pai, 2015

If you’ve been threatened or sued by someone for violating the TCPA, you’re not alone. When we researched Smile, Dial and Trial, we reviewed dozens of lawsuits filed against small business finance companies and have since even discovered new ones filed since then.

Why Banks and Alternative Lenders Will Play Ball in 2017

January 23, 2017 The economic recession over the last decade significantly slowed banks’ willingness to approve small business loans, and the impact on small businesses’ ability to get loans from banks is still being felt today. According to the Wall Street Journal last year, big banks have decreased the number of loans to small businesses by more than 38 percent since 2006.

The economic recession over the last decade significantly slowed banks’ willingness to approve small business loans, and the impact on small businesses’ ability to get loans from banks is still being felt today. According to the Wall Street Journal last year, big banks have decreased the number of loans to small businesses by more than 38 percent since 2006.

But the recession helped pave way for another industry – alternative lending – which has significantly improved access to capital for small businesses. According to the Small Business Administration (SBA), the 2016 fiscal year was a record setting year for loans, with more than 70,000 approved that totaled $28.9 billion and supported nearly 694,000 jobs.

The success of alternative lending showed banks the importance of expanding their offerings, particularly with online loans and small businesses. Over eight years removed from the recession, banks are taking notice and rebounding to grant more small business loans and release new financial services. More and more headlines show that banks are shifting their strategies to keep up with America’s technology and alternative lending habits, making 2017 the year banks finally get back into the fray and play ball with alternative lenders to improve the lending process.

For one, banks already have built-in advantages to accomplish this:

- an extremely low cost of capital

- a built in customer base that can be targeted

- visibility into accounts and access to a treasure trove of key data

In 2016, we saw large banks explore three key strategies: build, buy or partner. Let’s look at a few examples of each:

In 2016, we saw large banks explore three key strategies: build, buy or partner. Let’s look at a few examples of each:

Build: Wells Fargo went to market with its own technology in 2014, called Wells Fargo FastFlex for Small Businesses. Opening access to lines of credit, term loans, and SBA loans, Wells Fargo set a five-year goal to extend $100 billion in loans to small businesses. In December 2016, Citizens Bank announced plans to start offering its own digital small-business loans by the middle of 2017.

Buy or License: Instead of building infrastructure, banks can acquire or license off-the-shelf technology. This route is for the financial institutions that don’t believe in building tools themselves or want to move more quickly than their internal development resources will allow. Instead of expanding its suite of offerings on its own, they would rather acquire an existing infrastructure and focus on the top end of the lending market. Kabbage has led the way on the licensing deals by announcing partnerships with ScotiaBank, Santander, and ING.

Partner: Through partnerships, banks can expand their loan offering and quickly leverage other’s technology. Through licensing deals or white-labels, banks can send businesses they decline to work with to alternative lending options to give their customers additional access to small business loans. In December 2015, JPMorgan Chase took this route and partnered with On Deck Capital to provide alternative lending and small businesses loans to its customers. JPMorgan Chase also partnered with LiftFund in October 2016 to fill the remaining gaps in its small business lending services.

It was a resurgent year for banks’ ability to offer small business lending. In fact, going into 2016, American Banker predicted that banks would set their sights on online lending by signing strategic partnerships with the leading platforms. That came true to an extent, but based on recent trends, 2017 will really be the year that banks and alternative lenders start to work together.

No longer content to be sidelined, banks are starting to play ball, and they will continue to do so at an even faster pace. The fact that banks are moving in now and increasing small business loans validates alternative lending. As JPMorgan Chase has showcased, partnerships between banks and alternative lending can offer channels of sales for both parties and improve the small business lending process. The next step is for banks and alternative lending to work together.

New Regulations, Section 1071 of Dodd-Frank Among Them, Temporarily Frozen By Executive Order

January 23, 2017

Update 2/1/17: Disagreements abound over whether or not Trump’s recent regulatory freeze can affect the CFPB. According to the WSJ, part of this stems from the CFPB’s uncertain status as an independent agency after the the recent court decision in PHH Corp v. CFPB. “The CFPB is following a hiring freeze ordered separately by the Trump administration,” the WSJ states. This may be a signal that they do not feel totally insulated.

Section 1071 of Dodd-Frank had expanded Reg B of The Equal Credit Opportunity Act and granted the CFPB the authority to collect data from small business lenders. It’s all-encompassing considering that it oddly defined a small business lender as “any entity that engages in any financial activity.”

Although Dodd-Frank was passed in 2010 and the CFPB created in 2011, Section 1071 has been lying in wait. But just a month ago, the Federal Register said that its implementation was under way, with a pre-rule timetable of March 2017. “The Bureau is starting its work to implement section 1071 of the Dodd-Frank Act, which amends the Equal Credit Opportunity Act to require financial institutions to report information concerning credit applications made by women-owned, minority-owned, and small businesses,” it says.

And that work is no doubt a big undertaking, especially if it is really supposed to cover any entity that engages in any financial activity.

“The amendments to ECOA made by the Dodd-Frank Act require that certain data be collected and maintained, including the number of the application and date the application was received; the type and purpose of loan or credit applied for; the amount of credit applied for and approved; the type of action taken with regard to each application and the date of such action; the census tract of the principal place of business; the gross annual revenue of the business; and the race, sex, and ethnicity of the principal owners of the business. The Dodd-Frank Act also provides authority for the CFPB to require any additional data that the CFPB determines would aid in fulfilling the purposes of this section.”

Fear exists in the commercial finance community that the CFPB will use such data in a misinformed way to levy penalties and exert control over business-to-business transactions even though its statutory power is limited to just the collection of information.

Although the CFPB is still in the information gathering stage on Section 1071, the President’s regulatory freeze is likely only the first step of many to delay or dismantle their rules. And that’s at a minimum. Presently, the CFPB is faced with the threat that Trump will fire its director or abolish the agency altogether. There is strong support for this among Republicans, especially given that a federal court recently held that the CFPB’s structure is unconstitutional. In PHH Corp v. CFPB, the court offered two ways for the agency to come into compliance with its order, either reconfigure into a multi-member directorship or yield the director’s power to the President of the United States. Sitting CFPB Director Richard Cordray rebuffed the order as “wrongly decided” and declined both. His term ends in 2018.

The CFPB’s brash refusal to make concessions or accept court orders has made it a prime target of Trump’s administration. Because of the battles with the agency still to come, it is possible that Section 1071 may not begin to see the light of day for at least another four years.

The Leads Are Weak, Court Rules

January 21, 2017 One disagreement that has come out of the Argon Credit bankruptcy case is the value of the consumer loan leads that the company has in its possession. Argon argued that it has 300,000 leads worth $5.5 million based on its alleged cost to acquire them.

One disagreement that has come out of the Argon Credit bankruptcy case is the value of the consumer loan leads that the company has in its possession. Argon argued that it has 300,000 leads worth $5.5 million based on its alleged cost to acquire them.

In a court filing, Fund Recovery Services, LLC (FRS), a creditor, called that valuation “absurd on its face,” explaining that these were prospects that Argon had already declined for a loan and that they had not been able to sell these leads previously. A representative for FRS testified that the leads might be worth somewhere between a 1/2¢ and 1¢ each, giving them a value of only $1,500 on the lower end.

Presented with two completely different valuations for the leads, one for $1,500 and one for $5.5 million, the court ruled that it did not find Argon’s valuation credible and could not attribute any significant value to the leads.

Argon had hoped to use the leads’ value as collateral to keep the creditor at bay so that it could continue to spend its cash while the proceedings play out. The bankruptcy has been changed from Chapter 11 to Chapter 7.

The court has yet to rule on the motion to preclude non-closers from drinking the coffee.

Fifth Third Partners with QED Investors to Advance Fintech Strategy

January 20, 2017 CINCINNATI–(BUSINESS WIRE)–Fifth Third Bancorp (Nasdaq: FITB) today announced an innovative partnership between Fifth Third Capital Holdings, LLC and leading financial technology (fintech) venture capital firm QED Investors. Under the exclusive partnership, QED Investors will advise on the continued development of Fifth Third’s strategy to leverage fintech innovation to bring new products and services to bank customers while promoting the growth of fintech companies in the U.S.

CINCINNATI–(BUSINESS WIRE)–Fifth Third Bancorp (Nasdaq: FITB) today announced an innovative partnership between Fifth Third Capital Holdings, LLC and leading financial technology (fintech) venture capital firm QED Investors. Under the exclusive partnership, QED Investors will advise on the continued development of Fifth Third’s strategy to leverage fintech innovation to bring new products and services to bank customers while promoting the growth of fintech companies in the U.S.

“There is an unprecedented amount of innovation emerging in all parts of the financial services ecosystem,” said Tim Spence, executive vice president and chief strategy officer for Fifth Third Bancorp. “Our partnership with QED should enable us to identify new, high-potential technologies to complement our internal R&D and innovation efforts.”

This partnership, in addition to prior fintech company investments such as GreenSky, Transactis and AvidXchange, supports Fifth Third’s NorthStar strategy of enhancing its products and serving its customers more effectively through technology. By delivering products and services that its customers can count on, Fifth Third can better help those customers achieve their financial goals.

“We are incredibly excited about partnering with Fifth Third, a bank that is at the vanguard of change in the fintech space,” said Frank Rotman, Co-Founder and Partner at QED Investors. “Fifth Third is a natural partner for QED, one that embraces innovation and shares many of our views about what the future will look like in the space. We are thrilled for what this unique partnership means for the future of fintech and financial services at large.”

Fifth Third Capital and QED Investors led ApplePie Capital’s Series B capital raise in the fourth quarter of 2016. Fifth Third Capital and QED are also investors in GreenSky and AvidXchange. Fifth Third Capital continues to seek strategic investments in Fintech companies in the US market.

About Fifth Third

Fifth Third Bancorp is a diversified financial services company headquartered in Cincinnati, Ohio. As of Sept. 30, 2016, the Company had $143 billion in assets and operated 1,191 full-service Banking Centers, including 94 Bank Mart® locations, most open seven days a week, inside select grocery stores and 2,497 ATMs in Ohio, Kentucky, Indiana, Michigan, Illinois, Florida, Tennessee, West Virginia, Georgia and North Carolina. Fifth Third operates four main businesses: Commercial Banking, Branch Banking, Consumer Lending, and Wealth & Asset Management. Fifth Third also has an 17.9% interest in Vantiv Holding, LLC. Fifth Third is among the largest money managers in the Midwest and, as of Sept. 30, 2016, had $314 billion in assets under care, of which it managed $27 billion for individuals, corporations and not-for-profit organizations. Investor information and press releases can be viewed at www.53.com. Fifth Third’s common stock is traded on the NASDAQ® Global Select Market under the symbol “FITB.”

About Fifth Third Capital

Fifth Third Capital Holdings, LLC is a subsidiary of Fifth Third Bancorp. Fifth Third Capital seeks to invest in strategically relevant companies that support innovation across Fifth Third’s lines of business, bringing new solutions to bank customers and creating value for shareholders. Established in 2010, Fifth Third Capital has made numerous equity investments spanning the full company life cycle, from early to mature stage.

About QED Investors

QED Investors is a leading boutique venture capital firm based in Alexandria, VA. QED was co-founded by Nigel Morris, who also co-founded Capital One. They are focused on investing in early stage, disruptive financial services companies in the U.S., U.K. and Latin America. QED is dedicated to building great businesses and uses a unique, hands-on approach that leverages their partners’ and principals’ decades of entrepreneurial and operational experience, helping their companies achieve breakthrough growth. Notable investments include Credit Karma, SoFi, Avant, Remitly, Fundera and LendUp. For more information, please visit www.qedinvestors.com.

Contacts

QED

Frank Rotman, 804-445-2232

or

Fifth Third

Sean Parker (Media), 513-534-6791

Sean.parker2@53.com

or

Sameer Gokhale (Investors), 513-534-2219

The Top Small Business Lending Platform Finalists Named By LendIt

January 20, 2017The LendIt Industry Awards has named six finalists for the Top Small Business Lending Platform. They are:

- OnDeck

- Kabbage

- SmartBiz

- StreetShares

- Ascentium Capital

- iwoca

OnDeck you should know by now. They are publicly traded on the NYSE under ticker ONDK. We last sat down with them in October, shortly before they announced a $200 million credit facility with Credit Suisse.

Kabbage was one of the first online small business lenders to truly experiment with complete automation. In the last year the company has partnered with banking giants Santander and Bank of Nova Scotia.

SmartBiz ranked as the number one provider of non-Express, SBA 7(a) loans under $350,000 for fiscal year 2016. An online platform, they generated $200 million in funded SBA 7(a) loans through its bank lending partners during that period.

StreetShares has a strong focus on funding veteran small businesses. The company is also one of a very few to get approved for Reg A+ under the JOBS Act, which allows them to accept investments from unaccredited retail investors (with some limitations).

Ascentium Capital actually funded nearly $900 million to small businesses in 2016 and was acquired by PE firm Warburg Pincus just a few months ago.

iwoca is based in the UK but also operates in Germany, Spain, and Poland. They offer lines of credit to small businesses up to £100,000 with repayment terms of up to 12 months. Interest rates range from 2% to 6% per month. iwoca has raised £46 million through debt and equity.

According to LendIt, finalists for this category were awarded to the top small business lending platform based on a combination of loan performance, volume, growth, product diversity and responsiveness to stakeholders.

A similar category, the greatest Emerging Small Business Lending Platform also had six finalists. They include:

- ApplePie Capital

- Capital Float

- Credibility Capital

- Lendio

- Lendix

- Wunder Capital

More than 30 industry experts will judge and select award winners. You can view all categories, finalists and judges here.

You can also get 15% off the LendIt Conference registration with promo code: Debanked17USA.

New Industry Group Established to Support Consumers’ Right to Access their Financial Data

January 19, 2017The Consumer Financial Data Rights (CFDR) group defends consumers’ access to their data and fuels new innovation in fintech

REDWOOD CITY, Calif., Jan. 19, 2017 /PRNewswire/ — The Consumer Financial Data Rights (CFDR), a new industry group formed by some of the most recognized companies in the financial sector, officially launched today in support of the consumers’ right to innovative products and services that improve their financial well-being and are powered by unfettered access to their financial data. As fintech companies increasingly collaborate with banks around the world to provide innovative solutions through open application program interfaces (APIs), this right ensures a consumer can continue to give permission to third party companies to use that individual’s data for managing their personal finances, obtaining loans, making payments, and providing investment advice in addition to many other applications.

The CFDR brings together organizations from across the fintech ecosystem and includes some of the most influential and innovative companies in the financial sector, including the following founding members: Affirm, Betterment, Digit, Envestnet | Yodlee, Kabbage, Personal Capital, Ripple, and Varo Money among many other companies.

Section 1033 of Dodd-Frank codified the consumers’ right to access their personal financial data through technology-powered third party platforms. Together with promoting consumer choice and access to these consumer-first financial health tools, the CFDR is also committed to improving dialogue throughout the financial industry, actively engaging the government and working with banks, fintech innovators, and third party platforms. The CFDR aims to be a resource for policymakers, including the Consumer Financial Protection Bureau, as they determine how to best assist consumers in leveraging their own financial data.

“Each consumer’s right to their own financial data is vital in helping to understand their finances and make the best saving and spending decisions,” said Max Levchin, Founder and CEO of Affirm. “As a company we’re committed to helping customers make the best financial decisions and improve their financial lives through technology and improved flexibility, and having a complete picture of a customer’s financial picture is essential to achieving this. As a founding member of the CFDR, we’re committed to ensuring that all consumers have access to data which makes their financial lives better.”

“Consumers and small business owners need to be able to view their entire financial picture to make decisions that are truly in their best interests,” said Rob Frohwein, Co-Founder of Kabbage. “The ability to freely access financial data empowers customers to take actions to improve their financial lives, whether it’s accessing capital to grow a business or better understanding their income streams. Access to financial data is not just vital for customers wanting to enjoy financial health, but it also allows companies to provide better user experiences. Kabbage is thrilled to join other companies also committed to democratizing access to financial data.”

CFDR’s first action will be the submission of a joint comment letter in response to an advanced notice of proposed rulemaking on Enhanced Cyber Risk Management Standards issued by the Federal Reserve, Office of the Comptroller of the Currency, and Federal Deposit Insurance Corporation. The submission will encourage the regulators to establish a risk hierarchy with regard to cybersecurity risk in the fintech industry and will note the importance of continuing to allow consumers to access secure tools that enable their financial well-being.

“Consumers have the right to access financial solutions that allow them to improve their financial well-being,” said Anil Arora, CEO of Envestnet | Yodlee. “The CFDR is committed to initiatives that enable fintech innovation in the United States, much of which has transpired globally including recent open API initiatives in Europe, the Open Banking standard in the UK, and the commitment by the Monetary Authority of Singapore to create an open API economy and promote the secure use of cloud environments. The consumers’ right to unfettered access to their financial data will help enable the continued growth of innovative financial technologies and ultimately help consumers improve their financial health.”

About Consumer Financial Data Rights (CFDR)

The Consumer Financial Data Rights (CFDR) is a new industry group formed by some of the most recognized companies in the financial sector, launched to support the consumers’ right to unfettered access to their financial data. Open data acess is critical to enabling innovative tools that can help consumers improve their financial lives. CFDR members seek to: drive financial innovation in a collaborative ecosystem by bridging the needs of consumers, banks, fintech innovators, and regulators; partner with banks to support unfettered access to consumer and small business data through a secure and open financial system; and promote consumer rights to access and share their financial data with third party companies that provide tools to enable better financial outcomes.

SOURCE Envestnet | Yodlee

The NYDFS Opposes Fintech Charter Proposed by the OCC

January 19, 2017New York State regulators are not happy with the OCC’s willingness to grant bank-like powers to non-banks in the fintech movement.

“NY DFS disputes the OCC’s claim that it has the authority under the National Bank Act for this proposed new charter,” a letter by Superintendent Maria Vullo states. “Nonbank financial institutions are not banks nor are they similar to the entities encompassed by the National Bank Act.”

The letter goes on to make many points, one of which is the reminder of New York’s state sovereignty and another is the argument that such a regulatory experiment would lead to a financial crisis.

The letter follows similar concerns by Democratic members of Congress.