Archive for 2017

DataMerch.com Surges Past 10,000 Records

November 28, 2017 Tampa, FL, November 28, 2017 – Today, DataMerch.com, an online underwriting database for the alternative financing industry, announced that they have surpassed over 10,000 records in their database. After creating the online database only 2 years ago, DataMerch has experienced rapid growth in users and records to reach this milestone.

Tampa, FL, November 28, 2017 – Today, DataMerch.com, an online underwriting database for the alternative financing industry, announced that they have surpassed over 10,000 records in their database. After creating the online database only 2 years ago, DataMerch has experienced rapid growth in users and records to reach this milestone.

Director of Credit Risk Management at 1 st Merchant Funding LLC Dylan Edwards commented, “DataMerch has been an excellent resource for 1 st Merchant. We’ve been able to get additional information on potential clients that we wouldn’t have had otherwise. This really helps our underwriting decisions and adds another layer of safeguard. It’s something our industry needed for a long time.”

“DataMerch has been an excellent resource for 1st Merchant. We’ve been able to get additional information on potential clients that we wouldn’t have had otherwise.”

– Dylan Edwards, Director of Credit Risk Management at 1st Merchant Funding

“We make it easy for our members to search and enter records on our platform,” said Co-Founder Scott Williams. “Members can easily enter records manually, send us an excel spreadsheet for mass uploads, or they can integrate their underwriting software using our API to automate the process.” Scott added, “We are thrilled to see the enthusiasm and positive feedback we have received. Funders see the value DataMerch brings by revealing if a future client has a bad track record in the alternative funding industry. DataMerch can literally save a funder hundreds of thousands of dollars; that’s why we have been able to grow so much in the first few years. We expect the growth of members and records to continue to grow at a rapid pace.”

DataMerch’s leadership said they plan to continue to add new features and improvements to their platform. DataMerch currently offers members fraud alerts, API access, unlimited searches and uploads, personal support, and more. They plan to offer data reporting and analytics for trends within different categories soon.

About DataMerch

DataMerch LLC was founded in 2015 and is designed to help Funders determine if a future client of theirs has a bad track record in the alternative finance industry. DataMerch members can scrub their files using DataMerch’s specifically designed FEIN search and enter unsatisfactory businesses into the database. DataMerch currently has over 40 industry-leading subscribed members working together as a community. DataMerch continues to grow subscriber base and record count daily. DataMerch can be accessed at https://www.datamerch.com and contacted at support@datamerch.com

Source: DataMerch LLC

ISO Roadmap For 2018

November 26, 2017ISOs, as you finish out a wild year of funding, we’ve put together a roadmap to prepare you for a very successful 2018!

1. Educate yourself. Litigation in the MCA industry skyrocketed in 2017. That means as a salesperson you’re  more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

more accountable than ever to communicate the products and services you sell in a succinct and truthful manner. Case in point, MCAs are offered by funders, not lenders. Using lending-related terminology at any point during the sales process for non-lending products can open yourself up to both legal or regulatory consequences, even if you’re just an employee. As these fundamentals apply to industry veterans as well as newcomers, your top priority in the new year should be to get a certificate in Merchant Cash Advance Basics.

2. Source your own leads. Sneaking deals out the backdoor or being on the receiving end of ill-gotten leads may yield a couple bucks but it may ultimately come at the expense of your reputation and career. It could also be against the law. The surefire way to become a legitimate top performer in the industry is to generate your own deals. How else do you expect to build a book of business that’s truly yours and relationships with clients that are built on trust and integrity? Need help getting started? Check out this list of lead sources!

3. Participate in industry events. In 2018, it will pay to truly  know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

know who you’re working with. Sending your deal off to some random person you’ve never met claiming to be a funder or lender is a great way to increase the odds that your deal and potential commission will disappear. Fortunately in the coming year, there are great opportunities to network with industry colleagues. Here’s a link to one deBanked hosted this past August at Marine Park Golf Course in Brooklyn. If you’re a sales rep in the South Florida area, you should attend deBanked’s FREE cocktail networking event in South Beach on January 25, 2018. And if you want to better your skills, discuss the issues, and connect with the industry, you should register for Broker Fair 2018 right now! Check out the list of companies that have signed on to sponsor it already. Broker Fair 2018 is the number one don’t-miss event of the coming year.

4. Keep up on the news. Keep up on  developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

developments taking place across the entire alternative finance spectrum. The best part about deBanked magazine is that it’s free to subscribe. We publish six issues a year. Copies can be mailed to your home or office in print free of charge. Magazine content is typically distributed in print before it ever comes online so don’t miss out. Make sure the next deBanked magazine will be coming your way in 2018!

5. Choose your partners wisely. In the same way that it’s probably not a good idea to send your deal off to a random funder that cold called you, using old-fashioned methods like Google to discover who’s who can be onerous. That’s why we’ve segmented our sponsor directory by business type so that you can narrow down the right partner to fit your needs fast. While it’s true that these companies pay to advertise here, it’s an excellent starting point. So check out our list of sponsors!

Canadian Merchants Show An Appetite For Capital

November 25, 2017In Canada, the average deal size for a merchant is anywhere between $20,000 and $30,000 in funding, depending on who you ask. That’s why when one startup recently funded a $300,000 CAD advance from its balance sheet to a Canadian merchant, the deal turned some heads. While it’s unclear whether this amount could be indicative of a trend unfolding at our neighbors to the North, Canadian small businesses are preparing for some changes in the industry landscape in 2018.

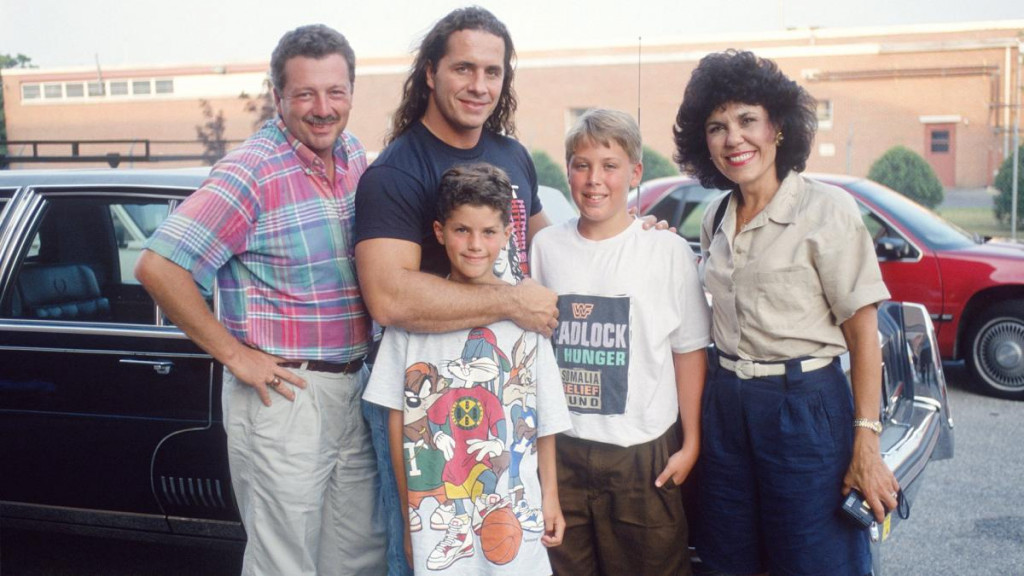

SharpShooter Funding, whose name depicts the famous wrestling move of the WWE’s Bret “The Hitman” Hart, was behind the $300,000 deal with an Eastern Canadian grocer.

If you’re wondering how a merchant funder and WWE legend became partners, chalk it up to a combination of fate and timing. Paul Pitcher, SharpShooter Funding managing partner, has been Hart’s biggest fan since he was a kid. Pitcher got the opportunity to meet his hero when was just 10 years old. It was then that the green shoots of friendship formed, and today the WWE’s Hart is acting commissioner of SharpShooter Funding, having helped to launch the business.

Canadian Merchant Landscape

To get a taste of the Canadian merchant financing landscape, consider that the three top Canadian funders deploy $20 million and $25 million per month combined, explained David Gens, president and chief executive of Merchant Advance Capital, which is included among the top three funders. That’s up from a range of $15 million to $20 million earlier this year.

And while a $300,000 advance may not seem like something to write home about for U.S. funders, it’s a big deal in the Canadian market. The culture among small businesses in the Great White North is different and more conservative than their US counterparts.

“It’s a function of the size of the merchant,” Gens explained. “The typical single-location storefront merchant is going to qualify for $30,000 to $50,000. It takes a larger and more established business, whether it’s a multi-location merchant or a business that is in the B-to-B space, a manufacturer, distributor or wholesaler to be large enough to qualify for large financing.”

Meanwhile there are some changes to small business taxation that are coming down the pike that may influence demand for credit, Gens noted, though the precise shape any changes to the tax law will take remains unclear.

“They will reduce the small business taxation rate on the face of it. But for businesses where they hold cash or need to hold cash, it’s a gray zone as to whether or not they will be able to hold financial assets in those businesses. The government is going after companies that are holding investments. But there’s a gray line as to what is a holding company that is holding an investment and an operating company holding a buffer because of seasonality or cyclical demand. We have yet to see what the rules end up being exactly,” Gens said.

Anatomy of the Deal

In the case of SharpShooter Funding, the grocer merchant originally came to the funder for less than $300,000 but qualified for more, bringing the funder’s tally for a single day’s deals to more than $500,000.

“We never thought we’d hit this milestone in the Canadian market. But the file was right, and the timing was great,” Pitcher told deBanked. Now that they’ve gotten a taste of it, SharpShooter Funding hopes to do more deals of this nature. “For a small funder like us to double the size of a big funder was a big moment for us, especially in the Canadian market,” Pitcher said.

Merchant Advance Capital’s Gens said his company is prepared to take on the risk for deals at even a higher threshold. “Our average is $35,000 to $40,000, and the largest deal we’ve ever done was $600,000. I don’t want to steal their thunder, but there have been larger deals,” said Gens. “A few funders may syndicate when deals get that big, but it’s not an inconceivable size.”

OnDeck, which similarly has Canadian operations, lends up to $250,000 CAD in Canada. OnDeck has extended more than $7 billion in online loans across 70,000-plus customers across the United States, Canada and Australia.

As for SharpShooter Funding, Pitcher said the funder has been on the sidelines for larger deals because they don’t want to grow too fast. He’s been turned off by other funders doing deals within a couple of months of launching and then being forced to close their doors.

“Our capital has always been strong. It’s not that we can’t afford to lend larger amounts. It’s because we want to make sure we’re doing it right from the start,” Pitcher said, adding that SharpShooter Funding has only had its doors open in Canada since June 2015, though its corresponding U.S. business, First Down Funding, has been around since 2012. “It’s been a work in progress, and I love every day of it! We’re only getting started, and I am 100% excited for the future,” he said.

The Canadian grocer reached out to SharpShooter Funding in response to Google advertising. The affiliation with the Bret Hart association didn’t hurt. Pitcher explained there is a seasonality tied to the merchant’s business, evidenced by a couple of months or more each year in which revenue is spotty, that made the grocer unattractive for banks to fund. “That’s why those sized deals are difficult to put out and banks won’t put out, because of seasonality,” Pitcher said.

SharpShooter Funding was not deterred by that. “We were really able to gain in-depth trust and visibility into this merchant from the first call to the last call. There was never a problem with him mixing up stories. Just the honest truth. From his references to his landlord, everyone involved made it clear he was here to work with us and not to play games,” Pitcher said.

Pitcher was impressed by the business owner’s work ethic. “He’s a roll-up-your-sleeves entrepreneur who didn’t borrow $1 million from his father. No bank loans. Six years ago, he rolled up his sleeves and made it work. Now he’s in a situation where banks won’t lend to him. But we will,” he said.

The merchant’s bank statements also made sense to the funder given their consistency, predictability and transparency. “Whenever we ask for finances from someone and that merchant can get them to us in an organized fashion in less than an hour, it speaks wonders. It means they’re honest and ready to play ball. And that’s what we want,” Pitcher exclaimed.

The merchant plans to use the capital for an expansion into a new food product line. If he pays off the advance early the funder will lower the rate.

Take a Break From Funding This Thanksgiving

November 21, 2017This Thanksgiving…

Step back from the daily grind

Those merchants eager for your cold calls can wait

There’s no need to start worrying about next year just yet

It’s Thanksgiving

So hug an underwriter

Kiss a broker

Think about your favorite merchant

And pay no attention to the algorithms automating your job

Give thanks

Because nobody wants to hear you recap your holiday like this

Or this

Or this

Enjoy the Holiday!

You should also check out our 2016 Thanksgiving Day post and 2012 Thanksgiving Day post.

Cleveland Fed Retracts Their Report on P2P Lending

November 18, 2017Here’s something you don’t see every day. A paper published by the Federal Reserve Bank of Cleveland about peer-to-peer lending was so dubious, that it has been taken down.

Since working paper no. 17-18 and related commentary on peer-to-peer lending were posted on our website on November 9, the authors have received several questions about the composition of the underlying data set they used in their analysis. In light of the comments received, the authors are currently revising their paper to further clarify the data sample they used in the study. Their revised paper will be posted as soon as it is completed.

– Federal Reserve Bank of Cleveland after analysts poked major holes in their findings

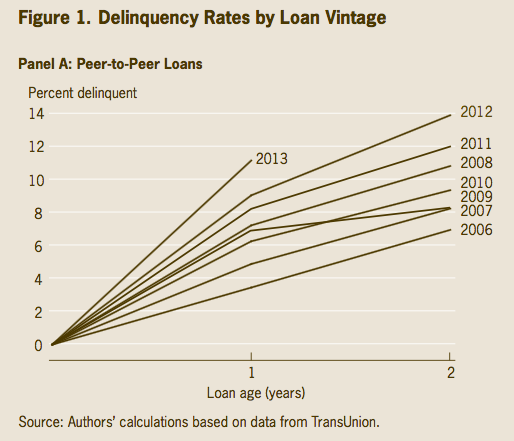

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

P2P Lending evangelist Peter Renton, a LendIt co-founder, was one of the first to challenge it. One issue was a chart purporting to plot delinquency rates in p2p lending going back to 2006.

“This chart shows that the lowest delinquencies from P2P loans occurred in 2006. Really?” Renton wrote on his blog. “I am sorry but this is just plain wrong and I challenge the authors to show me the actual data this is based upon. In 2006, the only consumer P2P lending (or any significant online lending) platform in existence in this country was Prosper and their 2006 vintage was terrible.”

Nat Hoopes, executive director of the Marketplace Lending Association (MLA), was even more vocal. In an op-ed he wrote for American Banker, Hoopes says, “In our view, this paper — ‘The Taste of Peer-to-Peer Loans’ — and its accompanying materials show that a lack of precision and understanding of subject matter can result in significant inaccuracies. The report’s authors presented findings that seemed to reflect issues with the P-to-P industry, but they actually relied on data from a much broader category of loans. The result was a misleading and brutally critical report about the P-to-P industry that was actually based in part on data from more traditional loans.”

Online lenders had reason to fret over the report as the Cleveland Fed did more than just publish charts. “P2P loans resemble predatory loans in terms of the segment of the consumer market they serve and their impact on consumers’ finances,” the Fed concluded. “Given that P2P lenders are not regulated or supervised for antipredatory laws, lawmakers and regulators may need to revisit their position on online-lending marketplaces.”

The worst offense, according to MLA’s Hoopes, was that the data the Cleveland Fed relied on was not even p2p lending data. A senior VP at Transunion had reportedly admitted that the data used comprised of both traditional loans and online loans that had been requested by the Fed a long time ago to use for a different study.

Oops.

Kabbage Taps Debt Capital Markets for a Cool $200 Mil

November 16, 2017 Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

With the Credit Suisse deal, the tally for Kabbage’s debt funding capacity reaches $750 million. “The new revolving credit facility will be issued by Kabbage Asset Funding 2017-A LLC, a wholly owned subsidiary of Kabbage Inc,” according to a press release.

Kabbage expects the credit facility will help them to scale faster. They plan to use the credit to add bigger small businesses to its client roster as well as extend higher lines of credit with longer durations.

“The new revolving credit facility with Credit Suisse is a debt round. Those funds are for our small business customers, and will be used to continue to provide them with easy access to working capital,” Deepesh Jain, Kabbage Head of Capital Markets, told deBanked.

It’s Kabbage’s maiden credit facility to be rated by credit rating agency DBRS. “The top two classes of the multi-class transaction earned investment-grade ratings of ‘A’ and ‘BBB’ and are collateralized entirely with assets originated through Kabbage’s fully-automated underwriting technology,” according to the press release.

Jain told deBanked the DRBS rating is highly significant. “It strongly demonstrates the proven success of Kabbage’s fully-automated platform and its data-driven risk analysis for small business lending. It speaks to the company’s leading position in the SMB-lending marketplace and Wall Street’s confidence in Kabbage,” he noted.

As Jain pointed out, Credit Suisse has been an early supporter of fintech. Indeed, the Swiss bank a year ago similarly provided a $200 million asset-backed revolving credit facility to another alternative funder, OnDeck.

Alternative Funders and Bank Partnerships in the Spotlight

Jain declined to comment on whether Credit Suisse might be interested in Kabbage’s lending platform for its own use. Alternative funder and banking partnerships were recently thrust into the spotlight with a lawsuit filed by a Massachusetts-based small business owner against Kabbage and Celtic Bank, which have had a partnership for at least several years.

The lawsuit alleges that the funding model of the defendants “was designed to evade usury laws,” according to The National Law Review. Apparently, the plaintiffs, which are listed in the public filing as Alice Indelicato and NRO Boston, had several small business loans and now accuse Kabbage of “renting” Celtic’s bank charter. Jain declined to comment on the lawsuit and the plaintiffs couldn’t be reached.

Capital Markets Pipeline

Meanwhile, at the rate they are going, we could see Kabbage tap the capital markets again in 2018. “Capital markets are something we will continue to explore to further diversify our funding options,” said Jain.

The Bad Broker And Merchant Due Diligence

November 15, 2017 There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

deBanked was contacted by a victim of the fraud, Noah Grayson, managing director and founder of Encino, Calif.-based South End Capital. Grayson said the real victims are the merchants who get taken advantage of by these scams. In this case it was a New York-based small business owner who took on too many MCAs.

Grayson is quick to point out the MCAs were not at fault and each may have even thought they were the first position funder since it all unfolded so quickly. “They’re just trying to do business and provide financing to businesses, and they got burned as well. They’re going to take some degree of financial loss because of this and maybe more,” Grayson said.

False Pretenses

When Grayson reviewed an email that he received from the borrower, which included a copy of the LOI, he knew immediately that it was fraudulent and the borrower had been misled. “It was a fraudulent LOI and we had no record of the borrower or the brokers who provided it in our system,” Grayson exclaimed.

As it turns out, the borrower was tricked by the fake LOI that sought to leverage the reputation of South End Capital’s brand to coerce him into taking out $260,000 of MCAs from four separate funders. They did it under the false pretense that South End Capital would then consolidate those positions in 10 days and extend as much as $900,000 more in working capital to grow the business.

To be clear, South End Capital does offer a genuine MCA consolidation loan program. Grayson had never agreed to consolidate the business owner’s MCA positions, however, or provide an additional $900,000. That part was fabricated. This left the merchant holding the bag for more than a quarter of a million dollars in MCAs, placing his business, which has been successful since the 1960s, on the brink of bankruptcy protection in the interim because of the crippling weekly payments.

Fraud Prevention

Andi McNeal, research director at the Association of Certified Fraud Examiners, or ACFE, said she has seen this before, only on the consumer side of the industry. “Loan consolidation fraud for credit card debt is very common in the consumer space, and it’s not surprising to know that similar schemes are popping up in the small business space, too,” she said.

She went onto explain that because a small business is typically run by a small management team who typically aren’t trained in fraud prevention, they often adopt the same mindset as they do in personal finances. They don’t always have the necessary checks and balances in place, which can place them at risk of being victimized by such schemes.

“Sometimes they’re not savvy enough to detect those types of scams coming at them,” she noted. “Certainly, big businesses can fall prey to this, but it’s less common.”

Staying on Defense

The recent saga unfolded over a period of six weeks. Meanwhile Grayson has outlined some red flags for small businesses to watch out for to prevent becoming the next victim to a new fraud.

“If what you’re being told seems suspicious or doesn’t make sense, question it. Ask questions and get more information,” said Grayson.

Another rule of thumb is to stick to the document in front of them. Again, this may just be a case of a few bad apples spoiling the bunch, but sometimes brokers tell small businesses something contrary to what appears in front of them on the official document. “The LOI spells it out,” said Grayson, adding that when in doubt the borrower should defer to the document.

The merchant should also take it upon themselves to call the lender whose name is on the LOI to verify its authenticity before signing it or providing any upfront fees.

“In this case, it was a fraudulent document and it didn’t help out the borrower but calling us to confirm it initially would have. Most of the time, looking at what’s written out on paper from the verified source will help and getting a verbal or email confirmation from the actual lender, certainly will,” Grayson said.

Another defensive step merchants can take is to simply review the website of the brokers and funders and look for names, press releases and past closings, details which Grayson noted were all missing from the broker in question’s site.

“Anybody can say they make loans and provide financing. They could tomorrow put up a website for a couple bucks and say they’re a lender and start taking applications. But just because there’s a website doesn’t mean they’re legitimate,” Grayson said.

He’s suggesting merchants check out the names of the principals and employees on the site. Google is their friend to check for any history of loans closing. Look for closing announcements and any complaints tied to the entity in question. Call the Secretary of State Department and inquire about any complaints.

At the end of the day, it comes down to the merchant doing their homework. “A lot is on him. He should have done more research, absolutely. But anybody can be coerced or tricked if the right things are said,” said Grayson.

If a merchant does find themselves in a situation where they fall victim to a fraud, there are steps they should take. McNeal said that while each situation is unique, a good first step is always going to be to reach out to a trusted legal counsel.

“They can help guide you through the process of what the options are. Do you have recourse? Does the situation call for insurance to help cover the losses? They also can advise on which law enforcement or government agencies are the most helpful – should the case be referred to the local authorities or do they need to bring in the FBI,” the ACFE’s McNeal advised.

More Pervasive

Grayson’s fear is that this is not an isolated incident. He has reason to be cynical, as this was the second incident this year resembling the most recent situation that they have experienced.

The first incident was relayed to South End Capital by a handful of borrowers about one specific MCA broker. No fraudulent documents were ever recovered, but the borrowers recalled the harrowing details of the incident

“Per the multiple borrowers, the broker used our real LOIs and lied to borrowers about how to interpret them to coerce tens of thousands of dollars in upfront fees from them. For example, for an LOI we issued for our SBA loan program that listed what SBA guarantee fees would be due at closing, he would convince them that that fee was his and they needed to pay it to him upfront to proceed,” Grayson explained.

The small business owner at the center of the scandal declined to comment, and it’s unclear whether they were the one to initiate the original communication with the broker or vice versa.

Lights, Camera, Crypto-Transaction – How a Lending Journalist Raised Millions to Build Magic Lamps Through the Murky World of Initial Coin Offerings

November 15, 2017

This past July, the winner of the Best Journalist Coverage category at the 2017 LendIt Conference Awards, announced that he would be stepping outside of his journalistic endeavors to raise money for a futuristic lamp company. The product, dubbed Lampix, is described as a lamp with a projector, a camera, specifically placed light-emitting diodes (LEDs), and a cloud-enabled computer. On the company’s “Medium” blog, Lampix promises that the product is “designed to transform any flat horizontal surface into an interactive computer.”

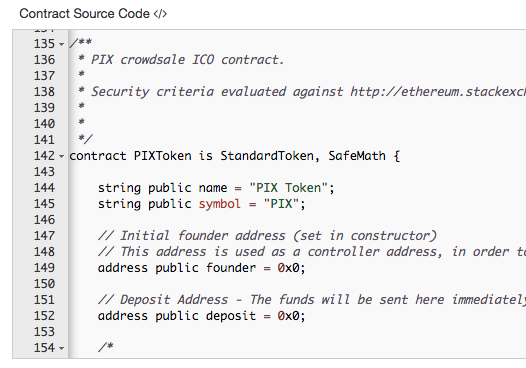

The man behind Lampix, George Popescu (whose Lending Times news site competed against and beat out fellow finalist deBanked at the LendIt Awards), makes for an interesting case study in alternative finance. That’s because Lampix shunned traditional capital-raising methods by relying on an Initial Coin Offering (or ICO), an unregulated blockchain-based corporate event which is similar to an initial public offering. Rather than purchasing shares, as is the case in an IPO, investors in an ICO receive digital tokens instead of shares. In August, Lampix raised $14.2 million through its ICO*.

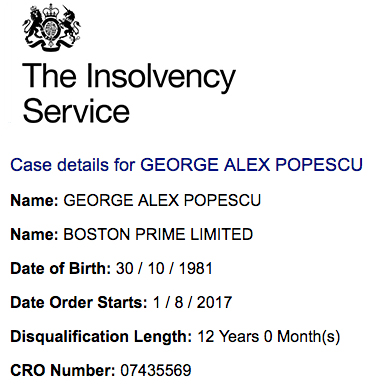

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

In case details published by the UK’s Insolvency Service on August 1st, the agency announced that Popescu was disqualified from serving as a company director.

Mr Popescu breached his fiduciary duties to act in the best interest of Boston Prime Limited (“Boston Prime”) and/or failed to ensure that both Boston Prime, as the regulated firm, and him individually, as the approved person, complied with the Financial Conduct Authority (“the FCA”) rules and guidance.

$6.2 million was transferred out of the company to a company named FXDD. Boston Prime’s receiver is presently suing FXDD seeking the return of the funds to the company. Proceedings are ongoing. Mr. Popescu is not under investigation and there are no legal proceedings at this time against Mr. Popescu.

It’s an inauspicious beginning for someone financing the “lamp of the future” using an unregulated and controversial strategy. Even so, when its ICO concluded on August 19, Lampix declared its gambit a success after raising $14.2 million through the sale of its digital tokens, which are known as PIX.**

By mid-November, the market value of those digital tokens, which exist on the Ethereum blockchain, had dropped by 50%, causing Lampix investors to suffer losses of $7 million. Unlike shareholders in publicly traded companies, token buyers have few investor protections. It’s not clear they are even considered to be actual investors at all. Buried in the fine print of Lampix’s 85-page “white paper” – a convenient way to avoid the label of prospectus – is a disclaimer. “Buyer should not participate in the [PIX] Token Distribution or purchase [PIX] Tokens for investment purposes. [PIX] Tokens are not designed for investment purposes and should not be considered as a type of investment.”

Additional disclaimers, moreover, declare that the white paper is not a prospectus, that the tokens “are not securities, commodities, swaps on either securities or commodities, or a financial instrument of any kind.”

But the distinction has not deterred people from joining in the frenzy of buying digital tokens like PIX. So much so, TechCrunch reports companies employing this strategy had raised nearly $800 million by means of ICOs in the first half of 2017.

And the SEC is not exactly excited about ICOs. “Fraudsters often use innovations and new technologies to perpetrate fraudulent investment schemes,” a July 29 directive by the SEC states. “Fraudsters may entice investors by touting an ICO investment ‘opportunity’ as a way to get into this cutting-edge space, promising or guaranteeing high investment returns. Investors should always be suspicious of jargon-laden pitches, hard sells, and promises of outsized returns. Also, it is relatively easy for anyone to use blockchain technology to create an ICO that looks impressive, even though it might actually be a scam.”

On September 29, moreover, the SEC brought an enforcement action against REcoin Group, charging Los Angeles businessman Maksim Zaslavskiy and two companies he controls with defrauding investors “in a pair of so-called initial coin offerings (ICOs) purportedly backed by investments in real estate and diamonds,” an SEC press release said.

The SEC alleges that Zaslavskiy and his companies –REcoin Group Foundation and DRC World (also known as Diamond Reserve Club) — have been selling unregistered securities, and that “the digital tokens or coins being peddled don’t really exist.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Deborah Meshulam, a partner in the Washington office of law firm DLA Piper and a former SEC enforcement official, told deBanked: “Regarding the lack of equity ownership, Lampix is seeking to establish that the tokens are not securities. Whether the SEC would agree should it decide to look into the offering depends on the facts and circumstances. The SEC staff would look past form to substance to assess whether the sale of the tokens constitutes an investment contract under legal standards. If so, then the SEC would view the Lampix offering as a securities offering. It may be that Lampix (or its lawyers) already vetted the offering with the SEC but I don’t know the answer.”

Popescu tells deBanked in an e-mail interview, “We had to respect all securities rules and regulations of course, respect the Howey test and so on. There were no hoops to jump through as we are not trying to avoid anything or prevent anything. We honestly built a token to build a community to help us crowdsource (mine) pictures for all applications among which, Lampix.”

“Each PIX token,” the Lampix website explains, “will be used as a form of payment to picture image miners, voters and app developers or to purchase a Lampix, cloud computing and apps.”

Meshulam also notes that the June, 2017, date of the Lampix white paper pre-dates the SEC’s enforcement activity in this area. She adds, “The statement that ‘token sales or ICOs are not currently regulated by the U.S. Securities and Exchange Commission may be very literal in the sense that there is not a specific regulation, but the SEC has stated that, in the right situation, ICOs are subject to the US federal securities laws.”

Erin Fonte, an attorney in the Austin, Texas, office of Dykema Cox, and the leader of the firm’s regulatory & compliance group, says, “The ICO stuff is so up-in-the-air. The SEC is looking at it closely. But it’s fairly new. And some of them (ICO’s) have been tied to fraud and Ponzi schemes. If a client came to us (seeking advice), we’d want to vet the people behind the offering.”

But what of Lampix, the company that won the Augmented and Virtual Reality category of the South by Southwest (SXSW) Accelerator Pitch Event earlier this year in March – and put a pretty feather in the cap of Popescu?

Popescu’s resume is no doubt impressive. He holds a trio of master’s degrees in various scientific and technological disciplines, including one from Massachusetts Institute of Technology. And he is a serial entrepreneur who lays claim to having founded 10 companies: they include, according to his LinkedIn profile, online lending, a craft beer brewery, an exotic sports car-rental space, a hedge fund, a peer-reviewed scientific journal, and a venture-debt fund.

He’s charmed journalists like Forbes contributor Roger Aitken, who declared: “The founders (of Lampix)…believe that Lampix will impact humans as much as computers or smart phones in the future…Think Tom Cruise in Minority Report. Imagine your room in five years: you will be able to use any surface around you as if it was a computer. The ability to transform any surface into an interactive computer (augmented reality) is going to unleash applications we have not even conceived of.”

The Lampix website hyped its ICO with the aid of an infographic listing “active product inquiries” the company has in its pipeline, the likes of which includes Amazon, Apple, Samsung, Microsoft, Sony, IBM, BMW, Bloomberg, PwC, and the Aspen Institute. With all of these names seemingly lining up, it begs the question: Why did Lampix choose the controversial route of an ICO to raise capital?

But it’s hard to determine the seriousness of these corporate relationships. Florin Mihoc, Lampix’s Strategic Partnerships & Development Advisor, said he could not assist us with confirming any of them, citing the slow and cumbersome bureaucracy of dealing with Fortune 500 companies. He did invite us to try reaching out to some of them on our own, which we did.

Bloomberg is one of the few acknowledging a relationship with Popescu’s company. Chaim Haas, head of innovative communication at Bloomberg, told deBanked that the New York-based media and financial communications company “collaborated” with Lampix. Bloomberg, he says, “has used Lampix hardware in its fellowship program (Bloomberg AR Fellows) as a prototype for augmented reality applications.” But Haas declined to elaborate on whether Bloomberg’s relationship with Lampix was more than an experimental one.

Edward Caldwell, director of public relations for East Coast markets and sectors at Pricewaterhouse Coopers, the Big Four accounting firm, declined to comment about Lampix. “We can’t discuss individual companies, clients or engagements,” he reports.

Douglas Farrar, senior manager for communications and public affairs at the Aspen Institute, told deBanked that he could find no business relationship between Aspen and Lampix. “I have gone down quite a few rabbit holes here,” he said in an e-mail, “But I’m coming up empty.”

When Popescu was directly confronted about this, he wrote, “The companies would only figure [in the infographic] if they actually themselves reached out to us and we exchanged emails with somebody from that entity. Most of these entities have many people and most of the companies’ people will have no idea [that] somebody else in the company is talking to us.”

Telephone calls and e-mail requests for comment to Microsoft were not returned.

A spokesperson using BMW of USA’s official twitter account, however, responded to an inquiry by saying they were a customer of Lampix, “but only for office usage.”

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Balina asked Popescu the softball question, could he show viewers a demonstration of the product? Popescu admitted he wasn’t prepared to do that and when he attempted to set one up on the fly, it didn’t work. The incident is notable because Lampix has been promoting the video through its social media network.

Popescu corroborates a number of details about the ICO, however. He confirmed the ICO price of a PIX token to be 12 cents, the US dollar price people had to pay per token. Cryptocurrency exchanges, where token speculators can buy and sell tokens online, show the trading value of a PIX token currently hovering around 6 cents, which translates into roughly a 50% loss in value.

Investors feeling hurt by such a loss can’t contest the purchase of PIX tokens with their credit card issuers. That’s because of a requirement that token sales had to be purchased with ether (ETH), the currency of the Ethereum blockchain. While ether is arguably similar to Bitcoin, it operates on an entirely different blockchain.

To participate in the ICO, in a Youtube video, Lampix also explained to purchasers, for example, how they could first buy ether with dollars through an online exchange known as Coinbase** before forwarding the ether to a digital wallet. Next, investors were instructed to send the ether from the digital wallet to a specially designated PIX address. An automated “smart contract” would then release the appropriate amount of tokens to the buyers’ digital wallets 31 days after the ICO was consummated.

It’s a byzantine procedure. And for investors – especially for those who are not exactly tech-savvy – the rigmarole makes it nearly impossible for them to recover their money should they feel buyer’s remorse. Neither the video nor the Lampix white paper mentions any buyer restrictions. Indeed, Lampix’s white paper specifies that “anyone” in the global market can participate. That means that an investor could theoretically be underage or a citizen of Iran or North Korea. (When asked what steps Lampix took with regards to KYC/AML, Popescu said, we “implemented the standard ones with partners specialized in it.”) Investors could even be citizens of the UK where Popescu is banned from being a company director.

And global they are. deBanked interviewed Rudy (whose last name we are withholding), a graduate student who lives in Singapore that says he bought approximately $2,200 worth of PIX tokens during the ICO. The drop in value has gotten him so frustrated that he’s contacted securities regulators in the United States to investigate Lampix. Despite the caveat in the white paper that tokens are not an investment and should not be used for investment purposes, Rudy said he considered himself to be an “investor” and that his reason for buying the tokens was to sell them in the future for a profit.

Popescu, who wasn’t asked about Rudy’s experience specifically, told deBanked that Lampix is not selling PIX tokens as an investment but rather to primarily build a community. “What people do with the tokens is their choice and we cannot prevent them,” he asserted.

English is not his first language but Rudy said, “I think that [the] SEC should regulate ICOs in the USA. There are no rules currently, teams can promise anything before the ICO and forget everything after the ICO. Things have to change, there should be legal pressure on crypto teams.”

Rudy added that he was “so enchanted” by Lampix’s ideas that he had promised himself not to sell the tokens for at least two years even if they were losing value. He conceded that he was not a tech expert. But, he says, the award at the SXSW competition was an important milepost to him.

deBanked found 700 more people interested in Lampix on the company’s official Telegram channel. The chat history since September 20, which we were able to obtain, has been dominated by talk of the PIX token’s trading value. Those bemoaning the low price regularly use the term “investors” to describe themselves – never mind that the white paper specifies that PIX tokens are not supposed to be an investment or to be used for investment purposes.

The chat’s administrator, who uses the nickname Chester, identifies himself as a “community manager” at Lampix. At one point he too refers to PIX holders as investors. “Hey guys,” he wrote in the channel on October 1, “Lampix is a company, not a single person, we don’t do things that quick, but pretty quick and we try not to confuse our investors by telling you unconfirmed news. Be patient, things will be just fine.”

Laura Toma, another community manager for Lampix, responded to complaints about the depressed price in the channel by saying, “The issue is that people want to get rich in a month.”

Indeed, investors hound not only the community managers, but also Popescu himself, who frequently joins in on the chat and fields questions about the trading price of PIX. “You should care more about the company revenue, clients, users.” Popescu replied to one user.

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

Others keep the faith. “PIX will be the real Aladdin’s magic lamp,” writes one user. Another hyperbolically predicts the price will “fly out of the earth, fly to the moon, and finally fly out of the galaxy.”

There is very little discussion about the use of the product itself while numerous inquiries are written in Mandarin. “Lampix has a lot of Chinese investors,” writes one. Other users self-identified as citizens of Russia, Romania, and France. Meanwhile, Toma writes, “Yes, there are investors from USA as well.”

Despite the losses that investors have so far experienced with Lampix, among other concerns, Popescu isn’t limiting himself to just one ICO. According to his online statements, Popescu is connected as an “advisor” to another company engaged in an ICO. AirFox, a Boston-based start-up launched by two Google alumni, provides free data to mobile phone users in return for eyeballing advertising. In early October, Airfox’s ICO raised $15 million. But a month later its AIR tokens, which sold for two cents apiece during the ICO, had lost 75% of their trading value. That means investors in AIR, the company’s ICO ticker symbol (which is becoming an increasingly ironic moniker) have seen more than $11 million go up in smoke almost overnight.

Popescu says in their defense, “The AIR tokens are meant to solve a real problem, of remunerating people who watch ads in exchange of getting more data and minutes on their mobile phone. The ecosystem is still being worked upon, the product is not live. Once the ecosystem is live we will see what really happens. Until then the token is mostly being handled by speculators. The price can therefore vary widely and it doesn’t reflect their true value.”

Even as Lampix and AirFox have been racking up massive losses for investors, Popescu announced on November 5 in a LinkedIn post that he would be involved in five more ICOs.

Among them is DropDeck Technologies, at which Popescu is listed as the chair of the advisor board; its ICO is scheduled for November 21. Another company, Factury, for which he is listed as an advisor, is initiating its ICO on December 15.

He’s an ambitious man.

And his ICO familiarity hasn’t escaped the scrutiny of PIX investors. “I find it strange that you are directing 5 other ICOs,” writes one user in the Telegram chat on November 4. “To make Lampix big, this will require a CEO [who is working] full time working on the project.”

Popescu responds personally. “I am working full time on the project but people have asked me to advise on their ICOs and this grows Lampix’s notoriety a lot in the crypto space,” he writes. He offered further assurances that he wouldn’t be advising those companies’ projects beyond their ICOs.

In an email to deBanked, he writes, “I run right now Lending Times, Lampix and Block X Bank only. The ICOs are just customers of Block X Bank. I have built about a dozen companies in 9 years, sold a few, closed a few. Each company has a team to help me, I am not doing this alone. For the ICOs I am more or less involved as an advisor / helping them project-manage their ICOs. How to run 3 companies? It’s about being effective, organized, delegating, partnering and being productive. Oh and I don’t watch TV, so maybe I have a few more hours per day than the average person. I do work long hours.”

Block X Bank, through which Popescu extends his efforts toward other ICOs, is described on the company website as “a boutique investment consulting company specializing in connecting blockchain projects with funding.”

In all of these ICOs, money is seemingly being created out of thin air. A consultant who was hired by deBanked to help analyze the technical aspects of both ICOs and smart contracts determined that Lampix raised much more than just the $14.2 million in token sales. In addition to the 114 million PIX tokens sold to investors, our consultant explained, the company also issued 220 million tokens to itself. At the ICO price of 12 cents apiece, those tokens would theoretically be worth $26.4 million – a huge piece of the total ICO pie that Lampix could sell on cryptocurrency exchanges if it wanted to rake in even more money.

There’s a kicker too. At scheduled intervals over the next four years, the smart contract that made PIX tokens possible in the first place is slated to automatically create – and allocate – 330 million new tokens to Lampix. Thus, when Lampix raised $14.2 million in August, the company reserved $66 million worth of PIX tokens for their corporate use.

Popescu said in his e-mail to deBanked that these company tokens are for “corporate usage like employee incentives, M&A, other company investments…etc.”

It’s a mind-boggling sum of money for the development of a futuristic lamp whose followers mostly seem to reside on internet chats like Telegram, reddit, and bitcointalk.org.

And this has occurred despite the company’s withholding any information regarding Popescu’s status in the UK. Balina, who interviewed Popescu on Youtube, told deBanked he wished he had known about his disqualification in the UK. “This is definitely a big issue and I wish I would have known about it so that either my audience or I could have asked him this directly on the live stream,” he said.

deBanked asked Paul Savchuk, Co-founder, CEO, and Chief Product Officer at Cryptocurrency Capital LLC, a US-based hedge fund that only invests in utility tokens as commodities, if Popescu’s ban in the UK would have been relevant information in the Lampix ICO. “Yes, that might be a red flag for us in some cases and require us to perform additional research,” he wrote in an emailed response. “We look at management very seriously – especially since a lot of projects are treated like startups and management is a key component to whether or not many of these ICOs can make it. We try to find such events and spot red flags whenever we conduct our due diligence research on ICOs. The reason: each project has something that needs to be improved. ‘Red flag’ – sometimes conversely can lead to a great opportunity when other market participants ignored it or were too skeptical.”

Mr. Savchuk further said, “Lampix is a perfect example of a coin that on the surface looks very promising, but when you dig a little deeper, you do find red flags that can dampen the excitement for this investment.”

And yet Savchuk spoke rather positively of the Lampix product after reading their white paper. “We believe the project is looking to change the current AR/VR tech industry,” he said, referring to augmented reality/virtual reality. “The project is promising for two reasons. First, they have multiple companies in their pipeline. Second, they have a legitimate product which they will manufacture and sell. They are one of the few blockchain products to offer a tangible product with the ability to disrupt the market.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

With regard to the price drop, Savchuk said, “This is a danger for all purchasers of ICOs. Sometimes it’s caused by token purchasers (swayed by) fear and greed and (hoping for) easy money and fast money. I doubt somebody sold Apple Inc.’s stock right after its IPO. It is also very difficult to restrict exchanges from allowing massive pump and dumps. That’s not even mentioning the difficulty of measuring the value of tokens,” Savchuk concluded. “Consequently, such projects are struggling with low credibility. However, it also creates a possibility for those who believe in the idea and product on a long-term run.”

Popescu downplays the significance of the UK issue. The root of the debacle, he says, is the result of Boston Prime – the company he previously ran – being forced into bankruptcy by the actions of a company he is now suing called FXDD. “FXDD bought the companies and then bankrupted them and that’s why Boston Prime [went bankrupt],” he writes. “Myself personally and each company separately are suing FXDD for this. UK has archaic laws where if you are a director of a bankrupted company you get disqualified from being a director again for a time. Attorneys charge about 40,000 GBP to defend this automatic case and I weighed the pros and cons and decided to ignore it as I have no plans to be a director in the UK for time being.”

Investors unhappy with underperforming ICOs may be willing to challenge their legality. On October 25, for example, a class action lawsuit was filed against Tezos, a computer networking project that raised $232 million in one of the largest ICOs ever. In a complaint, the lead plaintiff alleges that, among other things, Tezos unlawfully engaged in the unregistered offer and sale of securities and fraud in the offer or sale of securities. “In July 2017, Defendants conducted an ICO in which they sold 607,489,040.89 tokens (dubbed ‘Tezzies’ or ‘XTZ’) in exchange for digital currency worth approximately $232 million at the time,” the complaint reads. The plaintiff, who purchased 5,000 Tezzies, feels he was misled about the company and the offering.

Internal squabbling at Tezos which has delayed the release of its product and the sheer amount of money at stake have put the company on the map with the mainstream media and business press. The New York Times, Wall Street Journal, and Fortune as well as news services Reuters and Bloomberg have all covered the allegations of fraud.

The day before the class action lawsuit was filed, moreover, a deBanked reporter attended an explosive session at Money2020 in Las Vegas that saw Tezos co-founders, Arthur and Kathleen Breitman, attempting to give a status report of the company. A crowd that had gathered outside prior to the doors opening had attendees speculating whether the Breitmans “would actually show their faces” in the midst of all the drama.

To date, no lawsuits have been filed against Lampix despite the drop in the token’s value.

At a cryptocurrency/ICO meetup in NYC in October, a deBanked reporter met with executives at one company preparing an ICO who said they would not allow American investors to participate because of securities-enforcement fears. Pressure is mounting in the Far East as well. Citing their illegality, Chinese regulators in September issued a blanket cease-and-desist order on all ICOs in their country. What that means for Lampix’s Chinese investors bears watching.

Popescu says that Lampix supports regulation in China. “Of course, all Chinese people have to follow Chinese regulation,” he writes.

Meanwhile, on the product front, Popescu says that right now a Lampix lamp can be purchased for $10,000, a tidy sum because they must be hand-made. “We plan to improve the manufacturing costs and then we’re planning to do a kickstarter early next year for around $500 [per] Lampix,” Popescu told deBanked in his e-mail interview.

But for investors, it always comes back to the trading value of PIX. On October 25, one investor asks Popescu if the company will buy back its own PIX tokens at the ICO price to pump up their market price. “If you want a pump and dump please go to other companies,” Popescu responds. “We are here for 5-10 years to build a $100 billion dollar company and compete with Apple.”

And it all began with an ICO.

“ICOs also help with bootstrapping the user base – breaking the chicken and egg problem,” Popescu also explains in his e-mail to deBanked. “In addition, given that Lampix is looking to crowdsource images, we prefer many different people hold PIX tokens rather than 2-3 VC funds. And last but not least I think tokens are better rewards for the community (liquid, mark to market, etc.) than illiquid instruments.”

Not everyone agrees that PIX is the most liquid instrument to grow the community. US Dollars come to mind, for example. “Let’s say I’m a customer,” one investor poses to Chester, a Lampix community manager. “I want to use the cloud computing service but then I see I have to pay with PIX. I have no experience in crypto and have no idea how to do that. I just want to use your service fast and don’t want to buy PIX coins first before I can make use of it. Will there be a fiat option?”

Chester is awed by the idea. “Well, you are so professional,” he writes. “Man, you are good. You are good, the question you threw just hit the spot seriously. I guess there is always something Lampix needs to figure out and choose the best solution. Technically speaking they are jolly good at this point, but it doesn’t mean it’s perfect.”

Chester, who assures him that he isn’t being sarcastic, goes on to refer to the investor who asked that fairly elementary question as a “big shark” that is “born to bite.”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

The responses fly in:

“Buying my Lambo”

“Travel to Paris”

“Buy an island”

“Buy my mum her dream home”

“Quit my job and start up something for me”

“Pay off mortgage and be financially free”

“Buy house in Miami, buy Lambo, enjoy life”

“Retire”

“Easy. Buy more crypto”

Meanwhile on Telegram, where investors continue to engage Lampix management on a daily basis, Dante offers a sobering reminder of what they’ve bought into, “We don’t have equity, we only have tokens,” he writes. “And we are taking a big risk.”

* The amount of tokens sold multiplied by the 12 cent ICO price doesn’t exactly match the dollar amount Lampix says they had raised. That’s because Lampix not only issued bonus tokens to buyers at each stage of their ICO but also because the market value of ether, which users had to convert to from dollars to buy PIX, had fluctuated when they reported how much they raised. Like Bitcoin, the value of ether is volatile.

** The smart contract Lampix wrote to launch Lampix’s tokens into existence specifically named them PIX tokens and dubbed their publicly identifiable symbol to be PIX.

*** Coinbase is a respected digital currency wallet platform based in San Francisco.