Archive for 2017

Funding Circle Rebrands

August 10, 2017Funding Circle is ditching their old circular logo with arrows in favor of a more modern purple logo. The website has also undergone a redesign as well.

On the new website, the company states that they are “revolutionising a broken system” and emphasize that “we believe in those made to do more.”

In a recent interview with deBanked, Sam Hodges, a co-founder and U.S. managing director of Funding Circle said, “We are focused on building a world-class technology platform that can handle millions of transactions daily and deliver a best-in-class customer experience for borrowers and investors,” Hodges told deBanked.

PayPal Scoops Up Swift Financial

August 10, 2017

Online lending M&A is under way. PayPal is bolstering its merchant lending capabilities with the addition of Swift Financial. While the deal was kept under wraps, some industry participants heard some buzz about a possible combination.

PayPal has been investing in its lending arm of late, evidenced by the addition of former Amazon executive Mark Britto as senior vice president and general manager of global credit in July.

Noah Grayson, South End Capital managing director and founder, weighed in on the deal.

“A merger of two industry leaders like this is not surprising. As the economy continues to improve and small business owners have access to more financing options, alternative business lenders are going to continue to consolidate to stave off competition, retain deal flow and secure profitability,” said Grayson.

Dave Girouard, founder and CEO at Upstart, a consumer lending platform that uses machine learning, reacted to the deal:

“I expect to see more consolidation in online lending across both consumer and small business in the next year. Platforms with either giant balance sheets or proprietary technology will likely stick around, but others will struggle to compete,” Girouard told deBanked.

Alternative lender LendUp was a recent recipient of a PayPal investment. Sasha Orloff, LendUp’s CEO, had this to say about the deal:

“I’m not surprised to see an acquisition in the fintech credit space and expect this will kick off a wave of acquisitions. PayPal is a force to be reckoned with and we have seen them lead the industry again and again. Whether it is the partner model like with Synchrony, the acquisition model like Swift, Braintree/Venmo, Xoom, or the investment model like LendUp, they are proving again and again why they are leading innovation in financial services decade after decade,” said Orloff.

Meanwhile don’t expect to see a PayPal/LendUp pairing anytime soon.

“For our part, we’re going after a very different market and we’re focused on driving consumer financial inclusion — and we’re very focused on remaining an independent company and helping companies like PayPal and banks offer better products for millennials and the emerging middle class,” Orloff added.

PayPal was already working with Swift on a white-label basis for one of its products, PayPal Business Loan, which is a term loan with structured repayments.

“Swift Financial offers complementary business financing solutions and advanced underwriting capabilities that accelerate our ability to acquire new merchant partners with business financing solutions and to deepen our relationships with existing merchants and channel distribution partners,” said Darrell Esch, VP and Commercial officer, Global Credit, PayPal, pointing to Swift’s advanced underwriting and product capabilities and seasoned management team.

Swift was launched just over a decade ago and has extended loans to 20,000-plus merchants.

Company Founded By LendIt’s Co-founders Has Acquired LendingRobot

August 10, 2017 NSR Invest has acquired LendingRobot to become the largest robo-advisor in the alternative lending space, according to an announcement made by both companies.

NSR Invest has acquired LendingRobot to become the largest robo-advisor in the alternative lending space, according to an announcement made by both companies.

Of note is that three of NSR Invest’s co-founders, Peter Renton, Bo Brustkern, and Jason Jones, are also co-founders of the LendIt Conference.

The acquisition is a reminder that the conference founders are also significant players in the alternative lending space itself. According to the announcement, the new combined parent company, Lend Core, LLC, serves over 8,000 clients and manages over $150 million in assets.

For those not familiar with LendingRobot, deBanked started reporting on the company more than two years ago as a tool for investors to automate their investment picks on marketplace lending platforms like Lending Club and Prosper. I eventually became an individual paying customer of the service, using it to automate the purchase of nearly $30,000 worth of tiny $25 and $50 notes that fit within the parameters I had set. LendingRobot’s classic service can also automate investments on the Funding Circle platform, though I have never signed up with Funding Circle or invested in their loans.

When I last met with Emmanuel Marot, LendingRobot’s CEO, in person, he was launching a new hedge fund dubbed the LendingRobot Series that would be managed with robo-advisor technology. The hedge fund was included in NSR Invest’s acquisition.

NSR Invest CEO and LendIt co-founder Bo Brustkern will lead the combined entity as CEO. In a prepared statement he said, “We have long respected the work of the LendingRobot team and recognize that our companies are pursuing a common goal. That is, to provide a unifying investment solution for the millions of investors worldwide who seek the attractive, uncorrelated, diversified returns that alternative lending can provide. With this combination of our firms, we are bringing enhanced capabilities to our combined client bases today, and big plans for the future. A shining example of the kind of innovation that we will emphasize is the Lending Robot Series Fund, which provides customization, liquidity and diversification to investors through a novel, elegant, low-cost fund structure.”

Meanwhile, Marot will continue on only as a special advisor to the company. In a prepared statement, he said, “NSR and LendingRobot have taken different tracts to provide similar services. Now is the perfect time to combine our complementary strengths. The combination of LendingRobot’s advanced technology and NSR’s extensive knowledge of this industry puts us in the best position to provide superior investment advice in the alternative lending space for both individual and institutional investors.”

On Bloomberg: Watch Lending Club CEO Scott Sanborn Talk Q2

August 9, 2017On Bloomberg, Lending Club CEO Scott Sanborn said that banks were a critical piece of their platform. In Q2, 44% of all originations were funded by banks. Watch below:

Video not loading? Click here

Breslow: The Advantage Goes to Scale Players

August 8, 2017

OnDeck’s recent quarter answered a host of questions that surrounded the online lender, touching on everything from market share gains, to year-end profitability, to double-digit loan origination growth on the horizon. Another major growth driver that took the spotlight was the partnership between OnDeck and JPMorgan Chase, which has been cemented with expanded terms.

Noah Breslow, OnDeck’s CEO, told deBanked the partnership, which is bigger than any other relationship the online lender has formed, is firing on all cylinders.

“Ever since the product was introduced in April 2016 we’ve seen nice growth, incredible customer satisfaction and sound credit performance,” said Breslow.

In fact, the Chase partnership has been not only a flagship deal for OnDeck but very possibly the online lending community as a whole.

“We think it’s a harbinger of what’s to come in the space. Chase took a very forward thinking move a year and a half, two years ago when it decided to work with us to build a product,” said Breslow, adding that OnDeck remains in discussions with a number of large financial institutions about providing similar services and capabilities for online business lending.

The partnership, which started off as a pilot program between OnDeck and Chase, is a testament to JPMorgan’s commitment not only to OnDeck but also small business lending, which has taken it on the chin since the financial crisis. Under the new terms the relationship will continue for another four years.

“A whole segment of small businesses doesn’t want to borrow $5 million or $500,000. They want $50,000. The traditional bank lending process is not set up to make loans very efficiently,” said Breslow, pointing to the costs and time involved that cause banks to shy away from doing this.

OnDeck uses a score, dubbed the OnDeck score, that Breslow likens to a FICO score for small businesses. “The OnDeck score is built for our population. It looks at cash flow, personal and business credit, the industry and geography of the business, other debt, taking a holistic view of performance of the business than only FICO and cash flow,” he said.

JPMorgan Chase sets how much risk they want to take or not take with the loans they issue on the OnDeck platform, leveraging both their own data as well as data OnDeck has collected over the past decade of lending. Chase’s small business lending program remains invite-only.

“Small business owners will receive an email or phone call or some other form of solicitation, and then they can come to the website and get approved. We think over the next couple of years Chase will expand the scope of the program, but we’re not talking about how and when they are going to do that,” Breslow said.

OnDeck has taken a series of steps to strengthen the company’s balance sheet in recent months, not the least of which has been to tighten lending standards, which admittedly led to lower loan originations in Q2. Nonetheless the company expects to rebound with double-digit growth in loan originations in 2018, albeit off a low base.

OnDeck has largely completed a cost reduction plan that was started in 1H2017 and essentially removed $45 million in annual expenses from its P&L. “That was a lot of work to take on in a short period of time. We went heads down and got through it. In conjunction with that we rationalized our credit policy and our credit standards to be more conservative to reduce loss rates. The combination of those two moves set the business up to be profitable at the end of the year,” said Breslow.

These steps are resonating with institutional investors, including Mario Cibelli, managing partner at Marathon Partners Equity Management, which has an investment in OnDeck. He characterized the Chase extension as “good stuff.” “I think they had a solid quarter. They’re following through on some of their promises and I’m continuing to monitor our investment,” Cibelli said.

While OnDeck appears to be out of the woods, Breslow shared his perception of the industry.

“The advantages of online lending go to market leaders and scale players. Some folks with lower levels of scale can’t get credit performance right and don’t have enough capital to build out their business,” said Breslow.

With the expanded JPMorgan Chase relationship, gaining scale is on the horizon while some of the hard times appear to be in the rear-view mirror.

“The nice thing is we’re focused on growth again. The message we wanted to communicate yesterday is that we have all the capital we need to lend after the progress we made in the past year. We refinanced $850 million in credit facilities or added new credit facilities. So we have a great balance sheet that’s healthier than it’s ever been from a capital perspective. Now it’s about growing responsibly and profitably as we head into 2018,” said Breslow.

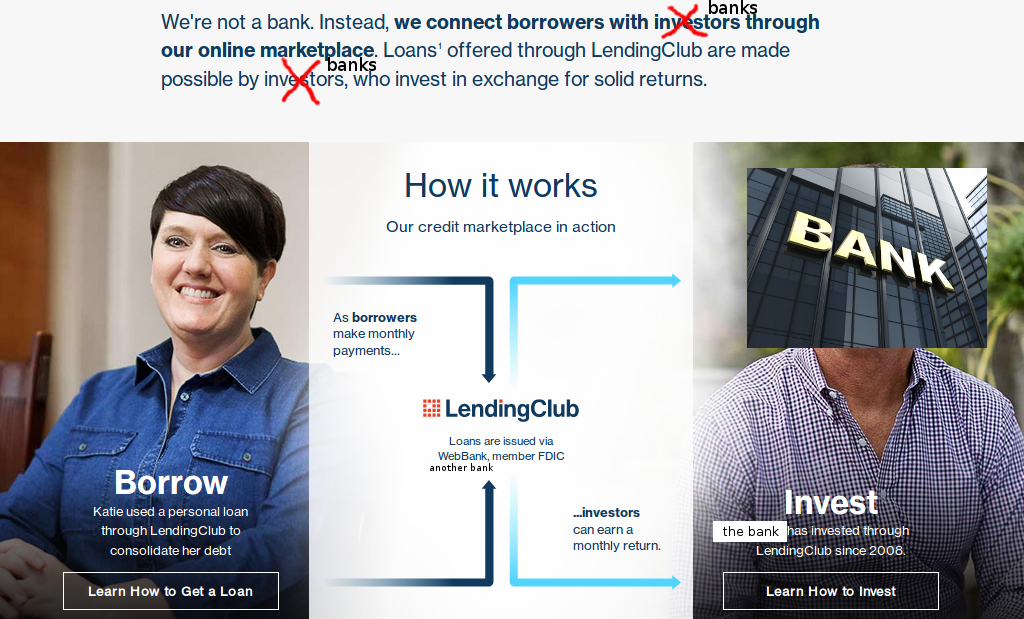

Lending Club Has Become the Domain of Banks as Peer-to-Peer Continues Decline

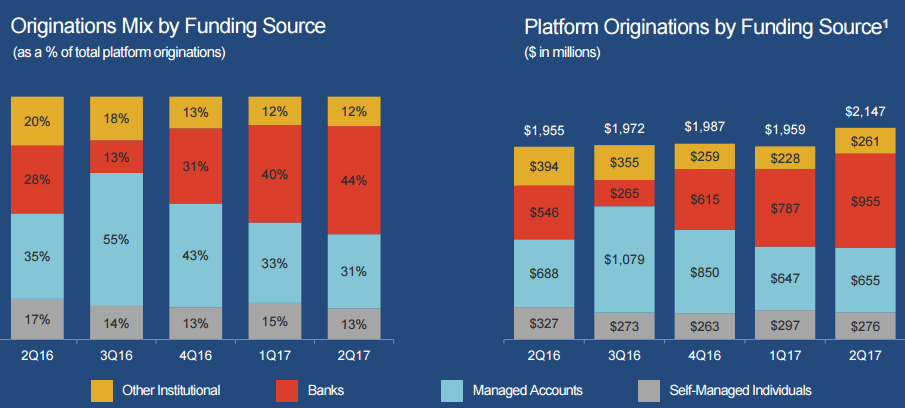

August 8, 2017Lending Club’s latest quarterly report revealed the future of their platform, as a conduit for banks to make personal loans. As illustrated below, banks have gone from funding only 13% of originations three quarters ago to 44% of all originations in the most recent quarter. That’s an increase from $265 million to $955 million.

Meanwhile, self-managed individuals, or the peers in the peer-to-peer aspect of the platform, only funded 13% of originations in Q2, a decrease from the previous quarter.

Lending Club refers to the breakdown as a “diverse” investor mix but it is obvious where the trend is leading.

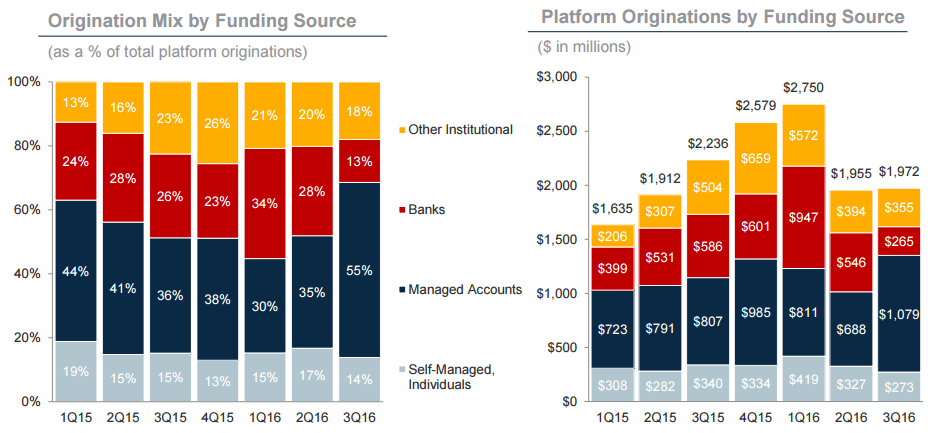

To be fair, Lending Club had previously depended on banks pretty heavily, as demonstrated by the chart that appeared in their Q3 2016 earnings presentation. Bank funding was at its highest point in Q1 2016 at $947 million, as was self-managed individuals at $419 million. Bank funding has since recovered and surpassed that record, but funding from self-managed individuals is still down by 34% (and shrinking).

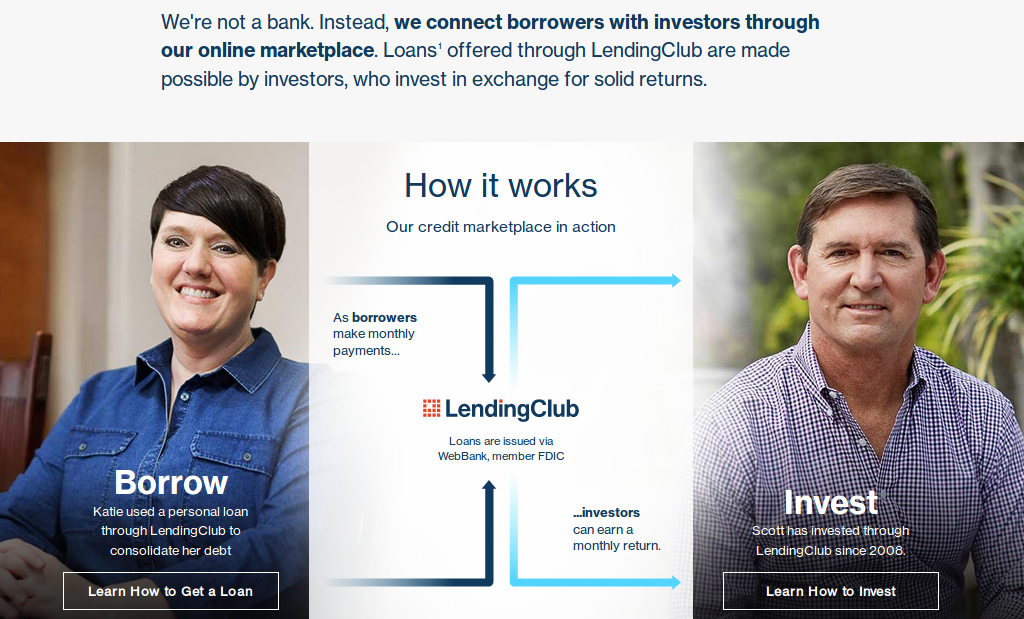

Despite these trends, Lending Club still explains their lending service as peer-to-peer on the homepage. In the example that explains how Lending Club works, “Scott” is investing on the platform to make a loan to “Katie.”

But it’s often more like this:

Lending Club had a $25.4 million loss in Q2. They’re projecting a loss of $61 million to $69 million for the year on revenue of $585 million to $600 million. Expect them to become more dependent on banks in the future.

Has OnDeck Turned The Corner?

August 7, 2017

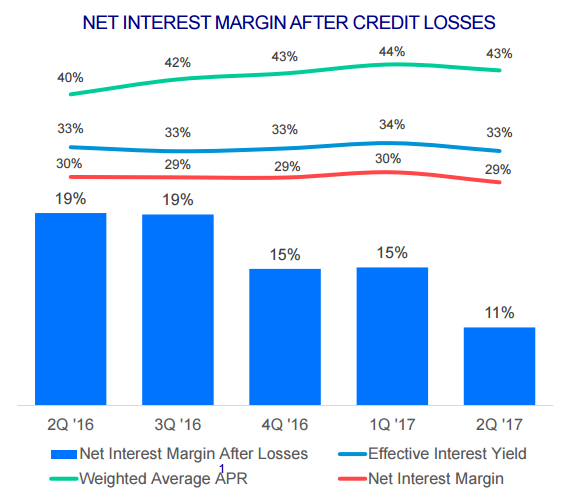

OnDeck’s loan origination volume declined by approximately 20% in the second quarter to $464.4 million but more importantly the company only recorded a GAAP net loss of $1.5 million. That’s down from the $11.1 million loss recorded in Q1 and in line with the company’s plan to achieve profitability in the second half of the year. OnDeck predicts that sequential originations growth will resume in Q3.

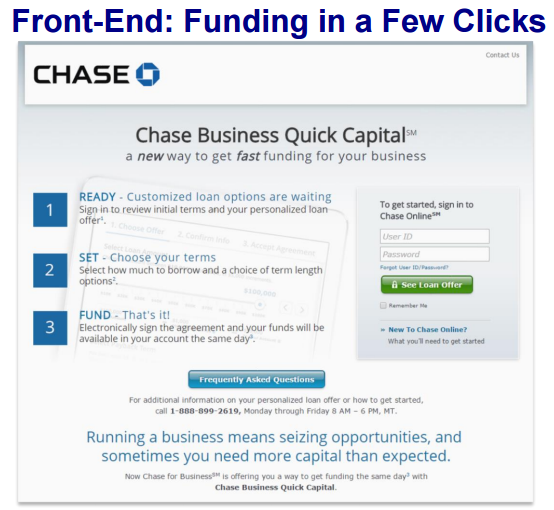

OnDeck also announced that it has expanded its collaboration with JPMorgan Chase for up to four years to provide the underlying technology supporting Chase’s online lending solution to its small business customers, according to the release. “Chase plans to continue to refine the offering, including expanding access and enhancing features throughout next year.” The image at right is from their Q2 earnings presentation demonstrating the front-end collaboration.

The company has also implemented stricter underwriting standards which includes lower loan amounts, shorter loan terms and stronger credit metrics.

Sales and marketing expenses actually increased from $14.8 million in Q1 to $15.3 million in Q2 but that was inclusive of $1.4 million in severance charges. The high cost of marketing is consistent with anecdotal reports obtained by deBanked regarding market saturation. Just recently, a small business owner told us in an interview that she has received so many mailed advertisements for working capital that she has a pile of them that’s now four inches thick.

OnDeck recorded a significantly higher charge-off percentage in Q2 at 18.5% up from 14.9%, which the company partially attributed to a contracting portfolio. However, the raw dollar amount grew substantially as well. The 15+ day delinquency ration dropped from 7.8% in Q1 to 7.2% in Q2

During the Q&A session of the earnings call, CEO Noah Breslow said he believed the company was positioned well to gain some market share due to the shakeout occurring in the industry.

Breakout Capital Expands Senior Leadership Team

August 6, 2017Breakout Capital – a leading small business lender – announces the hires of Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. These key additions position the small business lender for continued growth.

McLean, VA, August 7, 2017 – Breakout Capital announced today the appointments of Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. Both Mr. Fleischmann and Mr. McCammon bring a wealth of knowledge and small business lending experience that can accelerate Breakout Capital’s rapid growth.

“Breakout Capital’s growing employee base shares the same passion and commitment to advancing the Company’s mission to provide transparent working capital solutions, educate small businesses, and promote industry-wide best practices. We are thrilled with the additions of Robert and Tom to the leadership team,” said Founder & CEO, Carl Fairbank.

“Breakout Capital impressed me with its outstanding commitment to educating and advocating on behalf of small businesses,” said Fleischmann. “The innovative loan products combined with the impressive team of professionals make me extremely excited about the opportunity.”

Mr. Fleischmann will lead Breakout Capital’s efforts to expand and diversify its channels through strategic partnerships. Prior to joining Breakout Capital, Mr. Fleischmann was Director of Strategic Partnerships at RapidAdvance where he worked with a diverse group of partners, including banks and commercial finance companies, to help meet the financing needs of their business clients.

Mr. McCammon joins Breakout Capital with direct industry experience as he was formerly Director of Portfolio Management and Credit Operations at OnDeck. Prior to OnDeck and his recent move to the Breakout team, Mr. McCammon was involved in two de novo banks and was a consultant to the FDIC during the financial crisis. He will be a central figure in continuing to build Breakout Capital’s stature as both a credit-and customer-centric enterprise.

“Having worked in both retail banking and fintech, I was drawn to Breakout Capital as they have successfully combined strong credit and ethics fundamentals from traditional banking while still efficiently delivering capital to small businesses,” said Mr. McCammon.

Breakout Capital has quickly established a reputation as one of the most trusted and respected lenders in the market with a focus on product innovation, transparency, responsible lending and a partnership-based approach that extends beyond providing capital. Additionally, Breakout Capital is a Principal Member of the Innovative Lending Platform Association (ILPA), the leading trade organization representing a diverse group of online lending and service companies serving small businesses.

About Breakout Capital

Breakout Capital, headquartered in McLean, VA., is a technology-enabled direct lender which has provided a wide range of working capital solutions to small businesses across the country. In addition to becoming one of the fastest growing companies in the market, Breakout Capital is a leading advocate for small business. Its CEO, Carl Fairbank, is a Board Member of the Innovative Lending Platform Association. Breakout Capital has produced a highly regarded “educational series” through its blog, Breakout Bites, that helps small businesses better understand the technology-enabled lending market and how to avoid the hidden fees and debt traps that are prevalent in the industry. With a laser focus on educating small businesses, advocating for industry-wide best practices, and providing diverse, transparent working capital solutions, Breakout Capital is changing the financial landscape for millions of small businesses in need of funding. For more information, visit http://www.breakoutfinance.com.