Archive for 2017

BFS Capital Appoints Michael Marrache as CEO

August 17, 2017Coral Springs, Fla.—August 17, 2017—BFS Capital Inc., a leading small business financing company, announced that it has appointed Michael Marrache as Chief Executive Officer to succeed outgoing CEO and co-founder Marc Glazer. Named President in September 2016, Marrache previously served for more than three years as the company’s Chief Operating Officer. He also will join the company’s Board of Directors. Marc Glazer will continue to serve as Chairman of the BFS Capital Board.

“Michael has been invaluable in enhancing operations and driving sales. As CEO, he will lead our strategic direction both domestically and internationally, and spearhead initiatives that will continue to improve our loan portfolio metrics and strengthen our reputation among customers and partners as a premier small business lending organization,” said Glazer.

Over recent months, Marrache has built a management team that will execute on a long-term strategic plan to guide the company’s future and reach new milestones in the areas of origination, ISO partnerships and customer experience.

“I began work with BFS Capital nearly four years ago because I thought the company had enormous potential, and I’m even more certain of this today. I’m honored to have been asked by Marc and the Board to lead the company’s next phase of growth,” said Marrache.

“Our business has experienced great momentum over the last year and we’re setting a course for continued growth and leadership. We have a strong, committed management team and together, along with our employees, we’re primed to execute on our priorities, including upgrading the customer experience, investing in our product offerings and leveraging our data science to drive insights for our customers and partners,” Marrache added.

In April, BFS Capital reached a milestone of $1.5 billion in financing—a 50% increase over the $1 billion the company generated from inception through July 2015, led by loan portfolio growth in both new and repeat customers.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS Capital’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund businesses in all 50 states and Canada, and through its affiliate, Boost Capital, in the United Kingdom. Since 2002, BFS Capital has provided more than $1.5 billion in total financing to more than 18,000 small businesses across more than 400 industries. Headquartered in South Florida with offices in New York, California and the United Kingdom, BFS Capital is an accredited BBB company with an A+ rating. To learn more, please visit: www.bfscapital.com.

Go West, MCA Broker

August 16, 2017

If you check out the deBanked forum, one of the latest discussions originated from a self-described newbie business owner who wants to know, ‘What separates a successful ISO from the rest?’ The user, who calls himself jellyfish capital, asks the deBanked universe:

“I’m trying to figure out what the variables are that would dictate a successful brokerage/ISO vs. a shop that has a ton of turnaround and doesn’t make any money and ultimately ends up shutting its doors.”

The answer just might lie in the types of financial products the broker can sell.

MCA Broker Shift

Noah Grayson is managing director and founder of South End Capital, a commercial and investment residential real estate lender launched in 2009 that also started doing SBA loans and MCA consolidation loans in recent years to help out merchants with stacked MCA positions. Grayson pointed to a shift in the types of brokers signing up with the Encino, Calif-based lender.

“We’ve noticed a large number of brokers signing up with us are coming over from the MCA space. They’ve relayed to our staff that competition is too stiff to make enough money only originating MCAs, and they are looking for other avenues to bring in revenue,” Grayson said.

Indeed, South End Capital has seen an influx of brokers from the MCA industry gravitating their way. In fact, there has been more than a 10 percent spike year-to-date versus the same period last year in the number of brokers that discovered South End Capital through some form of Internet origin, such as deBanked, versus a targeted ad in a real estate related publication or through more traditional real estate origination means.

“What we’re hearing from our MCA industry referral partners is that their[customers] now want any option other than an MCA. These brokers are coming to us now because they are trying to evolve their businesses to stay afloat. Offering real estate or SBA loans has proved to be the next logical step for these brokers and it has provided a big bump to our business,” said Grayson.

As in any industry, making a career change can introduce unexpected challenges. A hurdle for the brokers, particularly as it relates to making the jump to commercial real estate lending, has been unrealistic expectations.

“Many MCA brokers have an expectation that real estate or SBA loans will work similarly to an [MCA], but it’s a more involved process. There’s more documentation and more moving parts to understand. There has been a big learning curve for a lot of these brokers — some have been willing to learn and are excited about the opportunity. However, many MCA brokers have proven extremely resistant to change and unable to adapt” noted Grayson.

There are hurdles facing the MCA industry, too.

Merchant Motivation

Merchant Motivation

So what’s driving the shift? Small businesses, some of which are saddled with short-term obligations, have begun to realize that thanks to the rise of alternative lenders they have more options. Meanwhile unscrupulous collection agencies are throwing a monkey wrench into the situation, making it trickier for merchants to gain access to cash advances.

David Soleimani, CEO of LendFi Corp, said a major setback for the MCA industry has been the interference of collection companies convincing good paying merchants to default and cut their payments in half. By negotiating payments with a third party, merchants essentially become blacklisted from receiving any further MCAs.

LendFi senior account rep Jonathan Meyer specializes in cash advances, term loans, equipment leasing and lines of credit. He’s noticing a trend of more MCA brokers expanding their line of business in the last year.

“Companies are overextended [with cash advances.] It’s a problem,” said Meyer. “If everything is perfect, we can do a term loan or a line of credit if it falls under certain criteria.”

One small business came to LendFi’s Meyer recently and as a result saved himself a lot of cash. “I consolidated someone’s loan recently. I got him a term loan and saved him $14,000 a month. He had two loans at $110,000. I got him a term loan for $165,000 and he saved $14,000 a month. He was paying $22,000 per month,” said Meyer, adding that he also consolidated the payments from a daily to a monthly schedule. “That’s a huge savings,” he said.

For all of the twists and turns that may be up ahead for brokers and merchants alike, one thing seems clear. The MCA industry isn’t going anywhere.

“There will always be a [customer] whose only option is an MCA, and it has its benefits for many. For example, the only way to get business funding in one or two days is with an MCA. However, I think the reasons why someone would need an MCA are becoming fewer and fewer as other more viable financing options emerge,” said Grayson.

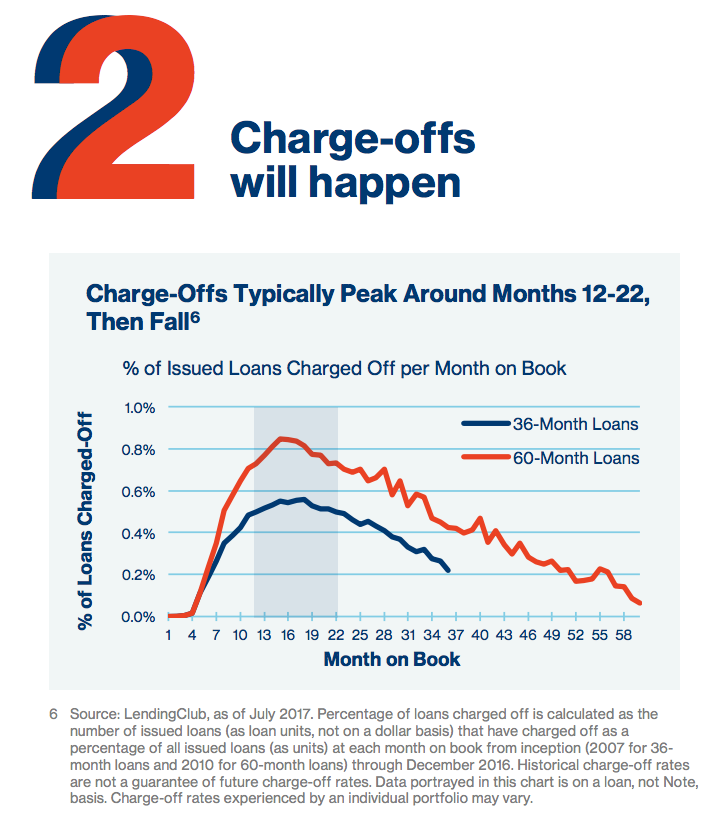

Lending Club: Charge-offs will happen

August 16, 2017 A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

1. Focus on net returns

2. Charge-offs will happen

3. Diversification is key

4. Monthly payments include principal and interest

5. Reinvestment is critical for consistent returns

Lending Club has gradually drawn more attention to the effect of prepayments on loans and this guide is no different.

“Prepayments impact returns because they reduce the amount of principal earning interest from Notes. A Note is considered prepaid when the dollar amount received is greater than the amount due for any given month,” they say. “It is inevitable that certain loans will charge-off or prepay and result in a loss of investment capital.”

Not mentioned however is that investors are charged a 1% fee on all outstanding principal if a borrower pays off their entire loan early despite it being no fault of the investor. And investors are less likely to monitor the impact of these fees if they keep reinvesting their cash which of course Lending Club advises investors to do.

The guide is still helpful in setting expectations for retail investors who ignored or did not understand all the fine print when they signed up. Quoted below about charge-offs:

“It’s inevitable that some borrowers will get behind on their loan payments. Some of these borrowers will get back on track and others will stop repaying their loans. After it’s clear that a borrower won’t make any more payments a loan is considered ‘charged-off.’ All investors in consumer credit experience some charge-offs, so it’s important to understand them and consider how they might impact your investment strategy.”

Overall, the guide is a nice way of keeping retail investors engaged. As someone who invested on the platform for a few years, one of the biggest disappointments I found was that the platform did not feel like a “club” at all. There was no sense of peer community and there was almost no communication whatsoever from Lending Club about anything other than requests to deposit more money.

But lately, peer funding has been dropping off the platform after reaching an all time high back in the first quarter of 2016. In Q2 of this year, only 13% of loans were funded by peers. 44% of loans were funded by banks. Maybe they’re not entirely ready to see individuals disappear completely or maybe they just want those that remain to keep the faith as returns slide. Hopefully, they continue to supply interesting and helpful materials in the future.

The Employee Suing SoFi Only Worked There for Three Months

August 15, 2017On Monday, several news outlets reported that a former employee of SoFi was suing for wrongful termination after he not only reported sexual harassment in the workplace, but also exposed an internal loan cancellation scheme designed to pad the bonuses of certain employees.

According to the complaint, which you can read for yourself here, plaintiff Brandon Charles learned of the loan scheme within 2 weeks of being hired and was fired only 3 months later in June of this year.

According to The New York Times, Charles’ attorney said he expects to bring another lawsuit, a class action, against SoFi next week for broad mistreatment of employees.

These events come just as SoFi had started teasing about a possible IPO in the near future.

You can read Brandon Charles’ complaint here and reach your own conclusions.

LendingPoint: CAN Capital’s Close Neighbor in Kennesaw

August 14, 2017 LendingPoint, a consumer lender staffed largely by former CAN Capital employees, may have something to teach the alternative small-business finance industry about creditworthiness. Three-year-old LendingPoint claims to go beyond FICO scores to bring each applicant’s sense of fiscal responsibility into sharper focus.

LendingPoint, a consumer lender staffed largely by former CAN Capital employees, may have something to teach the alternative small-business finance industry about creditworthiness. Three-year-old LendingPoint claims to go beyond FICO scores to bring each applicant’s sense of fiscal responsibility into sharper focus.

But first, let’s examine the CAN Capital connection. Four or five members of LendingPoint’s top management team came to the company after lengthy tenures at CAN Capital, a LendingPoint official says. That includes Tom Burnside, LendingPoint’s CEO and founder, and Franck Fatras, the company’s president and chief operating officer. Both worked 13 years for CAN Capital, with Burnside leaving as chief operating officer and Fatras departing as chief technology officer, according to biographies posted online.

All told, about 30 of LendingPoint’s 100 or so employees – a total that includes outsourced positions – formerly labored at CAN Capital, according to Fatras. Many put in considerable time at CAN Capital, holding jobs there in management, corporate governance, legal affairs, risk, sales, operations, IT, marketing, analytics, design, customer service, partner success and success delivery, online reports say.

Geography no doubt encourages CAN Capital employees to consider LendingPoint when it’s time to move on to another job. Both companies maintain headquarters in office parks in the Atlanta suburb of Kennesaw. In fact, the two companies operate half a mile apart, both of them just off of Cobb Place Boulevard Northwest, according to Google Maps and Directions.

Great news! Our new logo has OFFICIALLY made it's mark on our new building. What do you think?#Finance #LendingPoint #Logo pic.twitter.com/cpUIQvLy2w

— LPLoans (@LPLoans) March 13, 2017

The way Fatras tells it, LendingPoint hasn’t raided CAN Capital’s workforce. “We post the job, and they end up responding,” he says. “When they’re known quantities and people we have a lot of respect for, we just end up making it work.”

Moreover, LendingPoint’s connections with other companies don’t begin or end with CAN Capital. Some of the people in top management met when they worked at First Data Corp. and Western Union, Fatras recalls. Juan E. Tavares, co-founder and chief strategy officer, and Victor J. Pacheco, chief product officer, came from those relationships, he says.

Regardless of where they became acquainted, Lendingpoint’s leadership team has come together to form a direct balance-sheet consumer lender specializing in what they call a “near prime” clientele. The company defines the phrase “near prime” to include personal-loan applicants with FICO scores from 600 to 700, Fatras says, adding that the segment’s not sub-prime and not prime. The company has even trademarked “NEARPRIME” as a single word in capital letters, and it appears that way on the company website. It regards those consumers as “deserving yet underserved,” Fatras notes.

To qualify those applicants for credit, LendingPoint considers “behavior,” such as work history, education, and timeliness with paying rent, utility bills and cell phone bills, Fatras says. “A lot of what we do is identify patterns,” he says. “It’s all about asking the right questions.” The process requires tapping into multiple sources to collect the data, he observes.

In a blog published online soon after LendingPoint was launched, executives Burnside and Tavares claim that most credit models search for ways to say no to applicants, while their company uses big data to find ways of saying yes. LendingPoint algorithms predict risk with great precision, they say.

In a blog published online soon after LendingPoint was launched, executives Burnside and Tavares claim that most credit models search for ways to say no to applicants, while their company uses big data to find ways of saying yes. LendingPoint algorithms predict risk with great precision, they say.

In a newspaper opinion piece that ran about the same time, Burnside and Tavares maintain that their model examines cycles in an applicant’s life to pinpoint upward and downward trends. A consumer on the way up deserves a loan, according to the theory.

The company’s willingness to study information that resides outside credit scores did not originate with the CAN Capital connection, Fatras says. “The model is unique and the data structure we are using is unique,” he says. “It’s all about understanding the credit story of the person.”

Latin American lending practices had some influence on LendingPoint, Burnside and Tavares write in one of their editorial pieces. Lenders there review factors other than credit scores because the scores aren’t readily available in some countries, they write.

To analyze that type of non-FICO information, LendingPoint has developed its own internal scoring model and then automated the process, spending a lot of time to develop the technology, Fatras continues. Once again, asking the right questions determines the meaning that the company can extract from the data, he emphasizes. Otherwise, the information’s just not that beneficial, he says.

When consumers come to the LendingPoint website and answer five or six questions, they can receive a firm offer of credit in an average of seven seconds and sometimes as quickly as four seconds, Fatras maintains. The offers are contingent upon the company underwriting department’s validation of income and other figures, ne notes, adding that “we’re pretty happy with the infrastructure we’ve built.”

LendingPoint collects on the loans with automatic payments from customers’ savings or checking accounts twice a month, according to the company website. Deducting the payments twice a month helps customers with budgeting, the site says. Consumers can borrow up to $20,000 and pay it back in 24 to 48 months.

The system was devised by top management with combined experience of more than a century in credit and risk, Fatras says. When those executives with so much commercial lending experience gather around the conference table to talk about the business, the possibility of lending to small businesses occasionally comes up in the conversation.

But Fatras doubts the company will make that move to the commercial side anytime soon because companies in the alternative small-business finance industry are competing for 5 million to 6 million potential customers while the country has 50 million near-prime consumers. “The space is so big where we are,” he says. “The demand could be over a billion dollars a month. We have a lot of room in front of us for growth.”

With that seemingly infinite market, LendingPoint has been growing at a healthy pace, Fatras says. The company, which was self-funded for the first year, made its initial loan in January 2015. In 2016, it did $150 million in business, he notes. By the middle of this year, the company had made a total of $250 million in loans to 25,000 consumers, he says.

It’s a business model that members of the alternative small-business finance community might do well to emulate, Fatras suggests. “There could be a lot of cross-pollination,” between consumer and commercial loans when it comes to going beyond FICO, he says.

LendingPoint executives that were formerly at CAN Capital

Tom Burnside, CEO

formerly a COO and president at CAN

Franck Fatras, President and COO

formerly a CTO at CAN

Mark Lorimer, Chief Marketing Officer

formerly a CMO at CAN

Dave Switzer, Chief Analytics Officer

formerly a VP at CAN

Joe Valeo, EVP of Strategic Development

formerly an EVP at CAN

Catching Up With Marketplace Lending – A Timeline

August 13, 20175/17 – Funding Circle surpassed Zopa in cumulative lending to become the UK’s biggest marketplace lender

5/18 – Breakout Capital announced appointment of Douglas J. Lanzo as EVP and General Counsel

5/22 – The New York State legislature held a joint hearing on online lending

5/25

- OnDeck had the maturity date of its $100M credit facility extended

- China Rapid Finance reported Q1 net revenue of $10.5M

- Prosper Marketplace closed $495 securitization transaction

- SoFi co-founder Dan Macklin announced his departure from the company

5/31 – IOU Financial reported Q1 results, had $1M loss on $4.3M in revenue and lent (CAD) $22.1M

6/2 – Zopa began allowing investors to sell loans that have previously been in arrears

New York State legislators proposed the formation of an online lending task force

6/6 – deBanked and Bryant Park Capital published their Q1 confidence index in which industry CEOs scored their confidence in the continued success of the MCA and small business lending industry at 73.8%, the lowest level since the survey started in Q4 2015. It peaked at 91.7% in Q1 2016.

6/8 – Amazon surpassed $3 billion in loans made to small businesses since their lending program launched

6/9 – RealtyMogul announced that they had exited the residential fix-and-flip market

6/12 – The US Treasury published a report that called for the repeal of Section 1071 of Dodd Frank

6/13

- SoFi applied for a bank charter, specifically an Industrial Loan Company charter

- Lendio announced a pilot agreement with Comcast business

6/14 – Patch of Land expanded its debt facility from $10M to $30M

6/19 – Goldman Sachs’ online lender Marcus surpassed $1 billion in loans made since inception

6/20 – Former Lending Club CFO Carrie Dolan joined Metromile, an insurance company, as CFO LendingTree acquired MagnifyMoney

6/21 – Pearl Capital secured $15M in financing from Chatham Capital Management

6/27

- Square Capital announced that it will pilot a consumer loan program

- Former RapidAdvance CFO Rajesh Rao became the CFO at Beyond Finance, Inc.

6/29

- Funding Circle hired Joanna Karger as US Head of Capital Markets and Richard Stephenson as US Chief Compliance Officer

- Pave suspended lending operations

- Ron Suber, president of Prosper Marketplace, announced that he was stepping down from the company

- The SEC announced that all companies will now be able to submit draft IPO registrations confidentially, a perk previously only reserved for businesses designated as “emerging growth companies” under the JOBS Act.

6/30

- PayPal Holdings Inc announced that it had invested in LendUp

- Yellowstone Capital announced that they had funded $47 million to small businesses in the month of June

7/3 – Funding Circle announced that Sean Glithero had joined the company as its new global CFO

7/5 – Lending Club appointed Ken Denman to its Board of Directors

7/6

- CAN Capital announced that they had been recapitalized and were resuming funding operations

- Orchard Platform and Experian announced a strategic collaboration on data

7/7

- CFPB announced that it was extending the deadline of its small business lending RFI from July 14th to September 14th

7/10

- China Rapid Finance announced that they had made 20 million cumulative loans since inception

- CFPB announced new arbitration rule that effectively bans class action waivers from consumer finance contracts

- Former OnDeck VP of External Affairs and Associate General Counsel Daniel Gorfine, was appointed by the Consumer Future Trading Commission to be Director of LabCFTC and Chief and Innovation Officer

7/11

- dv01 and Upgrade (Former Lending Club CEO Renaud Laplanche’s new company) announced a strategic reporting partnership

- PayPal hired former Amazon executive Mark Britto to lead its lending business

- Fora Financial expanded its credit facility led by AloStar

See previous timelines:

4/6/17 – 5/16/17

2/17/17 – 4/5/17

12/16/16 – 2/16/17

9/27/16 – 12/16/16

Is The End Near For This Debt Settlement Firm?

August 11, 2017 Corporate Bailout, a New Jersey based firm that purports to help businesses lower the monthly payments on their debts, is back in the news. This time it’s for allegedly running a sex-fueled office with stripper parties, sex dolls, and sexual harassment, according to the New York Post who published video footage of the debauchery. Warning: the New York Post link is not safe for work.

Corporate Bailout, a New Jersey based firm that purports to help businesses lower the monthly payments on their debts, is back in the news. This time it’s for allegedly running a sex-fueled office with stripper parties, sex dolls, and sexual harassment, according to the New York Post who published video footage of the debauchery. Warning: the New York Post link is not safe for work.

deBanked has written about Corporate Bailout previously, in one case recently where the company is alleged to be robo-dialing out of control. Corporate Bailout never responded to the lawsuit and the court entered a default against the company this past Monday, according to the docket.

Back in April, deBanked also received the recording of a call purportedly between a representative of Corporate Bailout and a small business owner. We had the lengthy dialogue transcribed and it appears below with the names between the parties changed.

Of note, the alleged Corporate Bailout representative in the call makes several references to a partner law firm named Protection Legal Group. There are several lawsuits pending against Protection Legal Group, one of which alleges the firm didn’t have a lawyer licensed to practice in the state they claimed to offer defense in. In that situation, a merchant had to hire another lawyer to sue his lawyer at Protection Legal Group.

| Person Answering Phone: | Hello. |

| Robo Agent: | Hello. How are you today? |

| Person Answering Phone: | I’m good. |

| Robo Agent: | Great! Can I speak to the business owner please? |

| Person Answering Phone: | Who is this please? |

| Robo Agent: | This is Alex from Corporate Bailout. Are they available? |

| Person Answering Phone: | Yeah. One second please. One second. |

| Robo Agent: | Thanks. |

| John: | Hello. |

| Robo Agent: | Can I speak to the business owner please? |

| John: | Speaking. |

| Robo Agent: | This is Alex from Corporate Bailout. I know your time is valuable. So, let me get straight to the point. We help small business owners eliminate their unsecured debts. If your business has taken a merchant cash loan or advance, a high interest credit card debt, accounts payable debt, or any other unsecured business debt, you are now able to settle your outstanding balances for just a fraction of what you owe. I just need to ask two qualifying questions. Okay? |

| John: | Sure. |

| Robo Agent: | What type of entity is your business registered as? LLC, Corp, etc.? Hello? |

| John: | LLC. |

| Robo Agent: | Do you have at least $25,000 in unsecured debt? |

| John: | Yes. |

| Robo Agent: | Great! It looks like you may qualify. Hold on one second while I get a specialist on the phone who can explain further. |

| [Phone Ringing] | |

| Derrick: | Hello. Hi. |

| Robo Agent: | Hi, I have someone here that is interested in moving forward. I will let you take it from here. |

| Derrick: | Thank you for that. My name is Derrick by the way. Who am I speaking with? |

| John: | John. |

| Derrick: | John, it’s a pleasure, John. So, John, go ahead and tell me a little bit. What kind of unsecured debt are you experiencing? Is this with cash advances? |

| John: | Yes. |

| Derrick: | All righty. And that’s our cup of tea. So, I wanna give you an example— |

| John: | What exactly— |

| Derrick: | …of exactly how this would work for you. |

| John: | Okay. Perfect. Yeah. |

| Derrick: | All right. Tell me how many advances do you have. Do you have one or a couple out there? |

| John: | I have 3. |

| Derrick: | 3. Okay. And what do you owe approximately in combined balances? |

| John: | About $85,000. |

| Derrick: | Okay. And lastly, what are they charging you daily? |

| John: | Total of about $2,000. |

| Derrick: | At this day? |

| John: | Yeah. |

| Derrick: | Okay. Obviously, they’re overextending you for sure. Now, you open these advances yourself? Is this your business, John? |

| John: | Yes. |

| Derrick: | Okay. What is it that you do? I just wanna get a better grasp of what’s going on. |

| John: | We’re a trucking company. |

| Derrick: | Oh okay. Yeah. Yeah. I work with a lot of trucking clients. All right. So, here’s the deal. I mean, at 85,000, knowing that these are cash advances, we’re able to reduce that down to about 63,000. Saving you well over 21,000 just on principal. |

| John: | How do I do that? |

| Derrick: | That’s very simple. I mean, what we do is we appoint you a power of attorney that represents the association. And what they’ll do is that by power of attorney they’ll contact your creditors in a form of hardship for you. Okay? And that’s the key word there because by law— And it doesn’t matter if it’s a cash advance or a Capital One Visa. Whoever that creditor is, whatever obligations you have to that creditor comes to an immediate halt. That means no more interest accruement. That means that whatever number I’m telling you by the time you hire us let’s say by today, that’s the number. Yeah. |

| John: | One second. Why does it come to a sudden halt if I have a contract with them? Like can’t they sue me for this? I mean, I signed a contract with them and everything. How is it legal to go and say that I can’t pay them? I’m not understanding you. |

| Derrick: | Well, #1, these are cash advances, which is highly unregulated. Everyone knows if you look into it. Okay? Everyone knows— |

| John: | I did. |

| [Crosstalk] | |

| Derrick: | Okay. Yeah. There you go. Well, they’re tiptoeing the line of legalities here by pressing [0:04:55][Inaudible] laws. That’s why we’re able to snatch them and nip them in the butt. Okay? When you are charging on a daily basis an overextended amount way past 25% APR, this is abuse. This comes to abuse now and we have to come at them in a form of hardship. By law, that’s what happens and everything comes to a halt right then and there. Now, they have to settle. Now, here’s the thing. I know you’re saying can they sue you. You know, they can. They can. Probability is very low. |

| John: | Why would I take the risk of getting sued? I mean, I’m just trying to understand. Is what you guys doing also legal? I mean, no offense, it sounds a little— |

| Derrick: | Oh yeah. |

| John: | This sounds a little less legal. What you’re doing sounds a little more illegal than what they’re doing because I really have a contract with them that I signed and I notarized. I mean, that is like legal documents. |

| Derrick: | Yeah. We give you a legal contract. It needs to be notarized and all that too. Okay? But here’s the thing. It is legal here. You’re working with the law firm. Okay? The law firm will then take that responsibility and make sure that they do reduce your debt size. Okay? It’s a cash advance. It’s a slam dunk every time. Who do you work with by the way? |

| John: | [0:06:15][Inaudible] I’ll give it to you in a couple minutes. Where did you get my information from? ‘Cause I usually get calls from them. Like this is the first call I’m getting from this type of company. Where did you guys get my information from? |

| Derrick: | So, we essentially look through UCC filings and UCC filings are only liens that are basic entry companies that normally take out cash advances. Normally. |

| John: | Right. |

| Derrick: | 9 times out of 10 when I see a UCC file that looks like yours and, you know, I’m usually right it’s a cash advance, so yeah. |

| John: | Which business were you referring to though? |

| Derrick: | I don’t know. I don’t know. Your phone call got transferred to me. So, we have several ways of finding new clients and one of them is that we have a database. People make outbound calls. I’m the one on the receiving end. I work with my clients one-on-one to get them enrolled, have them feel good about the program, and then I pass them along to the law firm. That’s my role here. So essentially, it happens like this, John. Right? Let’s say hypothetically today you’re like “You know what? This makes sense. I am in a hardship. I need to get out of this crap. All right, what do I need to do today?” I get you on board today just hypothetically. By Thursday because today is Tuesday— We need at least 48 hours. By Thursday, the law firm contacts you and they say, “You know, John, we reviewed everything. You know, you’re good to go. Let’s now help you stop making those payments so that way your bank no longer honors the ACHs you’re making daily. So essentially, by Thursday, we’ll put a stop, a complete halt to your payments. And then we can culminate maybe a week to 2 weeks before there’s any expense. And by the way, it will be a fraction of that cost. We’re talking at least 50% less in those payments. That’s how overextended they have you on. We don’t have to have that start for at least 2 weeks from today or whenever— |

| John: | So, in essence, I will still have to pay them. Just in a longer period of time you’re saying? |

| Derrick: | Right. Yeah. Well, we can work that out, but the whole point of this program is not to stress anybody. And that’s where the idea of a scam needs to be thrown out of the window. Okay? |

| John: | So, they’re scamming me you’re saying? |

| Derrick: | Yeah. I would say so. You don’t feel like you’re being highway robbed right now paying 2,000 a day? And I can give you even better numbers if I look at— you know, if I take a peek at the contract just to see the real numbers ‘cause on average they’re charging anywhere from 30 to 60 percent on a borrowed amount. That’s an average. I know you’re in that category. |

| [Crosstalk] | |

| John: | I understand, but I didn’t know about it that’s why I’m saying if I knew about all this, I can’t deny in court if they sue me. They do have a legal document against me. I mean, it is an issue. |

| Derrick: | Right. Well, here’s the good thing. I mean, people are in such a worse shape than you, John, that they’ll hire any company who’s gonna promise them that they’ll be able to negotiate, but the greater thing why this is such a more wise decision for you is that you’re not hiring a middle man. As a matter of fact, I can show you, okay, any agreements that we have. We provide litigation defense services on top of the settlement. So, if ever anything should happen, which being at 85,000 likely not, but if ever anything should happen, you have attorneys there that will show up in court for you, that will battle, that will counter lawsuit if we have to, whatever, drag out the process, whatever it takes. Whatever it takes. But at the end of the day if they wanted to sue you, you know how long a sue takes place or takes to convert? |

| [0:09:59] | |

| John: | I know, but— |

| Derrick: | It takes a long time. |

| John: | At the end of the day, I would still be found guilty that I did sign the contract. What defense could I possibly have for that? I’m just trying to understand what the legality is. |

| Derrick: | The defense is #1 it’s a hardship. If you look into that, hardships create a big deal in the law system. So, that’s #1. Number 2 is that this is technically not even a debt that you have. Check in on technicalities. They only purchase future receivables at expect it let’s say 2,000 a day. |

| John: | Yeah. And they also have a judgment against me though. |

| Derrick: | That is all scare tactics. That’s all. Confession of judgments you’re talking about, right? |

| John: | Yeah. Yeah. |

| Derrick: | Confession of judgment that you signed. Yeah. Yeah. Almost everybody signs a confession of judgment now. They just started implementing that the last 3 years. |

| John: | They can’t do anything with that? |

| Derrick: | Not when you have a power of attorney reaching out to them for settlement against the hardship cost. They can’t do that. |

| John: | Oh. |

| Derrick: | And if they use that– |

| John: | And also like with this document, they can like freeze accounts and they can freeze assets and stuff like that. But if you guys trick them and they can’t do that– |

| Derrick: | Yes. They won’t be able to. But if we need to take any preventative actions, your law firm, your adviser there will tell you to possibly change. |

| John: | So, you guys have a lawyer? You are the lawyer then? |

| Derrick: | I’m not the lawyer. I’m not the lawyer. I don’t do the negotiation. I told you my role here is just to get you on board so I can pass you to the law firm. That’s it. That’s my role. Give you the information– |

| John: | what’s your charge? |

| Derrick: | Okay. Good question, John. So, let me look at this number here again. I wanna give you something real. So let’s say it’s 85, right? 85,000 you owe. That gets reduced down to $63,340. That 63,000 is going to cover absolutely everything. That covers paying back your cash advances. That will cover for our services and fees all inclusive. Okay? The only reason why we’re able to do that, John, is because we are a nationwide law firm that does negotiations for cash advances specifically. That’s what Protection Legal Group does. And so, are you familiar with a class action lawsuit? Are you familiar with that? |

| John: | Yeah. |

| Derrick: | Okay. So, we approach settlements in that same format. Class action settlement is what we call it. So, essentially you’re one drop in the ocean. Right? And that’s why I wanted to ask you who you work with so I can give you references. But guaranteed we have, you know, up in the hundreds of clients in those cash advances that we have already control such a large portion of their funds. So, because we’re going to– Who do you have? do you have Swift? [inaudible] |

| John: | I’m not gonna reveal that information yet until I look into your company a little more only because it’s my first time hearing about this. I will look into this. I wanna speak with my lawyer about it and everything. But you were telling me it would be lowered to 63,000. That’s fine. |

| Derrick: | Yeah. That’s at most. |

| John: | What’s your fee? |

| Derrick: | Our fees are inclusive, John. I can’t tell you what it is until we submit everything, until we submit all the hard copies into the law firm |

| John: | What’s the percentage range? I mean, there’s gotta be some sort of number that I can go by. |

| Derrick: | Yeah. Yeah. I can give you a percentage. So, let’s say we reduce it down to 70 cents on the dollar, right? 42 cents of the dollar will go to your creditors. Okay? |

| John: | And the 28? |

| Derrick: | And 28 cents gets [0:13:58][Inaudible] up between the law firm and your attorney. It’s like 4 cents in a dollar to the attorney, 24 cents to the law firm. So, that’s how it works. Normally, that’s what they look to negotiate. |

| John: | So, you’ll get the 24, they get the 4? |

| Derrick: | That’s if they agree to that term. Yeah. The whole point is for your attorney to figure that out with the lender. At the end of the day– |

| John: | Isn’t that 24% on the dollar also? |

| Derrick: | No. No. On the 70 cents on the dollar that we reduce it. So, you have 85,000. Reduce it to 70 cents on the dollar let’s say. In that 70 cents, 42 goes to them. The remainder of the 28 is split. Right? 4 cents to your attorney, 24 to the law firm. So that’s the numerology of how it gets distributed. |

| John: | That’s 40% |

| Derrick: | Right. That’s how it gets– What is? |

| John: | The 28 cents on the 70 cents is 40%. |

| Derrick: | 40%? |

| John: | Yeah. |

| Derrick: | No. No. It’s smaller than that. |

| John: | Do the math. |

| Derrick: | If it were 40%– |

| John: | Do the math. You said 28. Do 28 divided by 70. |

| Derrick: | 28 divided by 70, 0.4. Yeah. 40%. So, what are we getting off here? |

| John: | So basically, you’re charging me 40% and they’re charging me the same 40%. So what’s the difference? I’m just trying to understand why– |

| Derrick: | No. Yeah. We’re making 40– Hold on. We’re making 40% of that 70%. They’re making 60% out of that 70 cents. I mean, if you wanna get in detail, that’s what it works down to. At the end of the day, the whole program cost for you is only 63,000. So, you make the decision whether you pay 63,000 or 85,000. |

| John: | And run the risk of getting sued. |

| Derrick: | No one touches–. No. You have a law firm that will fight and give you the litigation defense. |

| John: | Right. That’s not a–I understand that. I understand they’ll give it to me. But I also run the risk of losing. And if I lose, I would have to pay all their legal fees and that extra money that I know, you know, what trying to get out of. So, here’s what I’m gonna do. I’m gonna have to look into this a little more ’cause I’m not just gonna give all my information in a second. Can you send me some– |

| Derrick: | Yeah, that’s fine. |

| John: | …information so I can look it over? |

| Derrick: | What’s your best email, John? |

| John: | It’s [address redacted] |

| Derrick: | @gmail.com. Do you happen to be in front of a computer now? |

| John: | I do. Yeah. |

| Derrick: | All right. I just wanna make sure that you at least get it. I’m putting in the subject heading, ATTENTION John. This should be easy to find. So, you know, you can loo at– |

| John: | I just wanna make sure what it’s about. what is this for? What’s it called? |

| Derrick: | Debt relief I can put in there. Is that okay? |

| John: | Yeah. That’s fine. |

| Derrick: | I’ll put debt relief as well. Yeah. |

| John: | And this is from Mason & Hanger? |

| Derrick: | Mason & Hanger? |

| John: | Yeah. That’s where you’re calling from? |

| Derrick: | What’s that? No. No. Protection Legal Group is the name of the law firm. Protection Legal Group. |

| John: | Oh, it’s not Mason & Hanger? |

| Derrick: | No. I don’t know where you got that name. |

| John: | From the caller ID |

| Derrick: | Really? Mason & Hanger? I don’t know. That’s strange. You know, when I make calls out of the office, sometimes it comes out like– |

| John: | Are you gonna have your contact number over there or no? |

| Derrick: | Yeah, it’s in the email. Tell me if you have it now ’cause it says that it’s sent |

| John: | [Name redacted]? |

| Derrick: | [Name redacted]. Yup. that’s me. All right. So, there’s a summary of what we went over and then those things in bold would be what we need in order— if you wanna proceed forward, but the very first thing you’ll see in bold is the current cash advance agreement signed or unsigned. Very important. That’s what’s gonna help us approve you or not and see if we can fit you in the program. We have to look over the verbiage in there. You see one document attached. Right? |

| John: | Right. Right. |

| Derrick: | Do you see what’s in bold? Yeah, I have a few things in bold there that we require from you. Okay? The hardship letter is one of them that’s attached in there. But before all of that, we wanna take a look at a copy of the agreements you have with the 3 cash advances. It could be signed or unsigned. Your personal information is not gonna do us any good. We wanna see if we can approve you first. Okay? That’s all. It’s just by procedure. And then what we find in there, which only takes about 20 to 30 minutes to approve you, I can tell you, “Hey, John, you know, here are the real numbers, what we found based on your contract. Here’s what we can offer and here are your options.” And then we can come into an agreement together. The whole point of this is to get you off from paying— You’re paying 10 grand a week, man, you know. To get you off of 10 grand. Maybe down to 5,000. Whatever that number is that’s more comfortable for you and obviously is realistic for the law firm. Okay? |

| John: | You are basically just the broker for the law firm? |

| Derrick: | I’m their spokesman, you know. I’m their marketing arm. Not a broker or anything. If I were a broker, I’d have countless sources of different law firms that does this. |

| John: | I assume you have one law firm that you work with? |

| Derrick: | I only represent them. |

| John: | Who do you work with? |

| Derrick: | What was that? |

| John: | Who is the law firm that you work with? |

| Derrick: | Protection Legal Group. Protection Legal Group. You can put that down. |

| John: | Can you email me that information? I wanna make sure. It is in the email? |

| Derrick: | Yeah. It’s in the email. Yeah. Yeah. It’s all in there. |

| John: | Okay. Protection Legal Group |

| Call trails out into goodbyes… |

In the follow up email that came up from a corporatebailout.com address, Derrick said, “We have teamed up with nationwide law firm, Protection Legal Group, who will negotiate with lenders on your behalf. By enrolling in our program, we would reduce the total advance balances down to 70 cents on the dollar! But more importantly, we turn your daily payment into a ONCE a week payment, and reduce that amount by up to 50%!”

Damage From the Nulook Capital Bankruptcy Shows Up In GWGH Earnings

August 10, 2017In April, we reported that Nulook Capital, a boutique merchant cash advance funder on Long Island had declared Chapter 11. The move was seemingly a response to a lawsuit filed against them by a secured creditor, GWG MCA, a subsidiary of publicly traded financial services company GWG Holdings Inc. (NASDAQ: GWGH).

In that bankruptcy, a merchant cash advance marketplace known as PSC also filed a claim against Nulook Capital to the tune of $400,000 in outstanding debt. In a sudden twist, however, a court saw enough evidence to believe that Nulook and PSC had an interwined relationship that jeopardized GWG MCA’s collateral, and ordered that PSC, who was supposed to just be a creditor with a secured claim, be put into receivership.

While the battle between all of the parties is still playing out in court, GWG Holdings Inc. disclosed the damage in their latest quarterly earnings report.

The secured loan to Nulook Capital LLC had an outstanding balance of $2,060,000 and a loan loss reserve of $1,478,000 at June 30, 2017. We deem fair value to be the estimated collectible value on each loan or advance made from GWG MCA. Where we estimate the collectible amount to be less than the outstanding balance, we record a reserve for the difference. We recorded an impairment charge of $870,000 for the quarter ended June 30, 2017.

Also notable in the earnings statement is that GWG MCA funds merchants directly. The company booked $133,583 in revenues attributed to MCAs in Q2. The amount was negligible compared to their core life insurance business. Their stock is up more than 30% YTD.