Archive for 2016

Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

November 29, 2016Update 11/30 7:30 pm: CAN says they are still open for business and still providing access to capital for current customers and renewal business. They are not actively seeking new business at this time, but will evaluate it as it comes in.

CAN Capital has confirmed that CEO Dan DeMeo has gone on a leave of absence. The company’s chief financial officer Aman Verjee and chief risk officer Kenneth Gang have also reportedly stepped down. Parris Sanz, the company’s Chief Legal Officer, has been made acting head of the company, while Ritesh Gupta has been promoted to COO.

A statement from CAN Capital is below:

“As the board and our leadership team conducted our business reviews and looked at how we can best position the firm for future growth, we self-identified that some assets were not performing as expected and that there was a need for process improvements in collections. It became clear that our business has grown and evolved faster than some of our internal processes. As we work to improve these processes, the Board has named twelve-year CAN Capital veteran and senior executive, Parris Sanz acting head of the company and promoted Ritesh Gupta to COO, while Dan DeMeo, CEO, and two other members of his team are on a leave of absence. Over the past 18 years CAN Capital has consistently made decisions to position ourselves for growth and leadership in the industry and we look forward to helping small businesses succeed for many years to come.”

Some of CAN Capital’s referral partners have reported to us that the funding of new deals has been put on hold until January 2017. This could not be confirmed, however. (Update: This was later confirmed)

More than just an industry leader, CAN was founded in 1998 and is widely regarded as the first merchant cash advance company. A year ago, deBanked featured Dan DeMeo and CAN in a story to mark their success. As of April this year, they had funded more than $6 billion since inception. In August, they secured a coveted partnership with Entrepreneur Magazine.

Having secured a $650 million credit facility last year led by Wells Fargo, they are the second largest player in the alternative business finance industry behind OnDeck.

Sanz joined the company in 2004 with more than 12 years of experience as a corporate, securities, and transactional attorney. Before joining CAN Capital, he was a senior executive and General Counsel of a specialty pharmaceutical company, the successful sale of which he led in 2003. Prior to that, Sanz was an attorney in private practice at the law firms of Latham & Watkins in Los Angeles and Paul, Hastings, Janofsky & Walker in San Francisco, where he handled a wide variety of M&A transactions, securities offerings including IPOs, and other corporate transactions, and acted as outside general counsel to a number of technology start-ups.

Sanz received his J.D. from Harvard Law School in 1993 and a Bachelor of Arts degree from U.C. Berkeley, High Honors and Phi Beta Kappa, in 1990. Sanz is admitted to practice in California and Washington, D.C., is a registered In-House Counsel in New York, and is also admitted to practice before the United States Court of Appeals for the Federal Circuit.

Q3 2016: Confidence in the Small Business Financing Industry’s Success Down Slightly

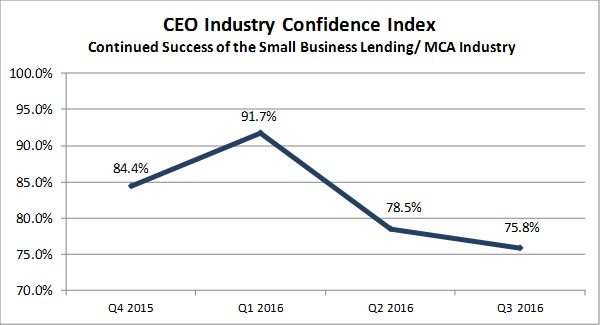

November 29, 2016Confidence in the industry’s continued success was down among small business financing CEOs in the third quarter, according to the latest survey conducted by Bryant Park Capital and deBanked. At 75.8%, it’s the lowest level recorded since surveying began late last year.

Respondents were not asked the reasoning for their confidence score, but the sentiment may have been influenced by what seemed like an impending Clinton presidency at the time and the 4 more years of regulatory pressure on financial services that would’ve continued as a result. The survey was conducted before the election. Also, the correction taking place in the consumer space with companies like Prosper and Avant have allowed a general feeling of pessimism to waft through the alternative financing universe.

Still, at 75.8%, which is still well into positive territory, the mood is probably best described as cautiously optimistic. The euphoria in Q1 at 91.7%, preceded the resignation of Lending Club’s founder and CEO, which symbolically burst alternative lending’s bubble.

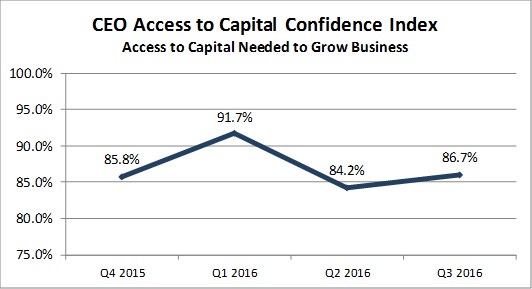

Curiously, industry CEOs were slightly more confident in their ability to access capital needed to grow their business. Respondents were not asked what their capital source options were or the respective costs, but it signals that there are still plenty of investors interested in the space.

Bryant Park Capital and deBanked also produce a comprehensive full-year industry report, available to anyone for $495. To purchase the 2015 report, you can contact me at sean@debanked.com

Brief: LendIt Brings First Fintech Awards to the Industry

November 28, 2016

Marketplace lending conference LendIt, has announced the first fintech industry awards and is inviting nominations to recognize top-performing companies and executives.

Nominations are now being accepted (closes December 21st) for 18 different categories including executive of the year, fintech woman of the year, emerging consumer lending platform and most innovative bank. The award ceremony will be held during LendIt’s 2017 conference in March.

“The lending industry is entering its 2.0 phase, after maturing in 2016,” said Peter Renton, co-founder and chairman of LendIt in a statement. “As we seek to connect the global online lending community and foster innovation and industry growth, we must recognize those that are making the biggest contributions and innovations and moving our industry forward.”

The entries will be judged by a panel of 30+ industry experts including Gilles Gade, CEO of Cross River Bank, Glenn Goldman of Credibly, and Angela Ceresnie, COO of ClimbCredit.

CapFundNow Launches Funding Platform for ISOs and Agents

November 27, 2016Hauppauge, NY – November 28, 2016 – CapFundNow.com has launched an online platform and portal that is bringing Funders and their offers direct to the ISO and Agent. This concept is taking the funding industry by storm. The platform was created to help streamline the funding industry by allowing the ISO and Agent to submit a deal through an online platform and have the industry’s top funders make offers through the portal.

According to managing partner Elliott Levine, “you spend countless hours submitting deals to funders through multiple platforms and email addresses. You become exhausted and it’s grueling wasting valuable time submitting deals to multiple funders. It’s impossible to keep up to date with each funder’s niche and guidelines as they can be revised and modified daily. CapFundNow was designed specifically with the ISO community in mind, giving them large-scale access to the industry’s best funders with a simple one-click platform. Our intention was to allow a seamless transaction approach from ISO to funder, allowing them to communicate directly while retaining their full commission.”

Why spend your valuable time submitting deals to multiple funders when CapFundNow will do it for you? CapFundNow has teamed up with the industry’s best to bring you a seamless funding experience. CapFundNow will submit your deals instantly to the industry’s top funders allowing them to compete for your business. You will have the capacity to review and compare multiple offers within the portal. This will allow you to concentrate on the most viable part of your business; sales and servicing your clients. CapFundNow will do the rest by bringing the funders and offers direct to you.

CapFundNow is a completely free service exclusive to the ISO and Agent. You receive the same commission as if you were working hand in hand with the funder. Your full commission is paid directly from the Funder.

Contact Information

CapFundNow – Where Funders Compete!!

Clientservices@capfundnow.com

300 Wheeler Rd.

Hauppauge, NY 11788

(888) 285-6665

Goldman Sachs Goes After Online Lenders With Video Ads

November 25, 2016“No fees. Ever,” states one of Marcus’ new video ads. Marcus is Goldman Sachs’ new online consumer lending division and the value proposition is pretty compelling. Most other online lenders for example, strongly rely on origination fees, but Marcus doesn’t charge them nor any other kind of fee. View their four campaign videos below:

It’s Here: Artificial Intelligence Changes MCA Broker’s Business, Improves Bank Underwriting and Debt Collection

November 22, 2016In this age of man versus the machine, the case for artificial intelligence and machine learning does not need many vociferous advocates.

Some predict that revenues from fintech startups using AI and predictive models is set to jump by 960 percent or to $17 billion by 2021. We might be closer to that number than we think, considering 140+ AI startups raised a total of $958M in funding in Q3’16, alone.

While healthcare, cybersecurity and advertising are frontiers of AI innovation, the growth and momentum of big data in finance (spurred by online lending) is fast bringing fintech to the forefront. In lending, specifically, data has become the new currency. It’s not so much that lenders didn’t use data for decision making earlier, but the data available then, wasn’t as rich or as extensive. A loan approval decision that just required a decent FICO score and assessment of character has expanded to include data points like a business’ social media presence, reviews, and owners’ background history.

Today, artificial intelligence in fintech has grown to tackle cybersecurity threats, act as a personal assistant, track credit scores and perform sentiment analysis to predict risk — making automated underwriting just the tip of the iceberg for what artificial intelligence and machine learning can do for the financial services industry. deBanked spoke to three fintech upstarts that have taken AI beyond underwriting.

AI Assist

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

“I hadn’t heard anything like an artificial-intelligence sales assistant,” said Vinfield. “The results we got within a month of using it were unbelievable.” Within the first month, Vinfield made $35,000 in revenues by spending just $4,000 and eventually reduced his staff of 24 to 4 people. He was so sold on its potential for the merchant cash advance industry that after prolonged negotiations, he secured the rights to be the exclusive reseller of the software, and called it AI Assist. The software is now used by leading MCA companies like Yellowstone, Bizbloom and GRP Funding.

While Conversica’s clientele includes auto and tech giants like Oracle, Fiat, Chrysler and IBM, for the financial services industry, it’s marketed and sold to MCA and lending companies through AI Assist. It integrates easily with CRM software like Salesforce and creates a virtual sales assistant avatar that tracks old leads and reestablishes engagement. In the lead generation race, where a 3-5 percent response rate could be considered good, the response rate for Conversica has been 38 percent.

Designed to be akin to a human sales assistant, Conversica’s technology can determine a lead’s interest based on the response and set up a conversation with the sales department to follow up. “Your Conversica virtual assistant is an extremely consistent, personable and tireless worker. She doesn’t get sick and never needs a break. She never gets discouraged, and she improves with each engagement,” says the AI Assist website.

True Accord

True Accord

Personal chat assistants for money management and sales is one of the popular modes of AI implementation in fintech, given it’s scalability in lending for functions like debt collection. One company that does this, is True Accord. True Accord, similar to AI Assist uses automation software to schedule and send messages to customers by the company’s “Automated Staff”

The San Francisco-based company was founded by Ohad Samet who has over 11 years of machine learning experience in finance. The idea came to Samet while he was working as a chief risk officer at payments and e-commerce company Klarna, underwriting loans worth $2 billion. “While working at Klarna, I realized how big a piece debt collection is and I did not like the way it was done,” said Samet. “I needed machine learning to change it.”

Samet founded True Accord in 2013 to develop a debt collection AI assistant and today the company works with leading banks, credit card companies and food delivery services and has collected over half a billion dollars. It establishes targeted communication with the customer less frequently than traditional collection agencies and allows customers to pay their dues over mobile, which accounts for 35 percent of collections for the company.

“We humans don’t want to accept it but the reality is that, when it comes to scale, machines make better decisions than humans,” said Samet. “Machines are consistent, they are not tired, not angry, don’t fight with the significant other and all of this makes for better accuracy, better cost structure and better returns of scale.” While this might be true, building an efficient, compatible and compliant model is harder than it might seem.

James.Finance

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Recognizing this opportunity, James.Finance, a Portugal-based startup is using artificial intelligence to help financial institutions like banks build their own credit scoring models. Founder and CEO Pedro Fonseca, describes James as a “narrow AI” for a specific purpose of guiding risk officers to build machine learning models that follow regulatory compliance.

The startup works with consulting agencies or partners to reach out to banks. It offers a trial run of the software, which it calls a ‘jumpstart,’ where a risk officer is provided with James’ technology and in 24 hours, he or she will have to beat it with their in-house AI software.

“And we are consistently able to beat the models,” said Fonseca. The company won the startup pitch at Money 20/20 in Copenhagen earlier this year after receiving an uproarious response in Europe. Fonseca wants to divert his attention to the US’s fragmented banking market, which is dotted with smaller banks and credit unions. “The US is a perfect target for us. We are looking to work with local consultancies that know the problems of a bank intimately.”

As these entrepreneurs vouch for it, the current state of AI use in fintech is just the tip of the iceberg. And anything man can do, machines can do faster and better, right?

Online Loan Middleman Just As Culpable As the Lenders, Federal Court Rules

November 21, 2016A CFPB lawsuit against a payday loan lead generator survived dismissal last week, despite the US Court in the Central District of California acknowledging the company’s role as a “middle man” in the lending process. T3Leads and several people connected to the company are alleged to have deceived consumers, in part such that “they allowed consumers to be exposed to lenders that could cause them substantial harm.”

The court ruled that T3Leads was a service provider as contemplated by the Consumer Financial Protection Act and is therefore bound to the laws therein. The case will now proceed to discovery.

Notably, the court also agreed with the recent opinion of the D.C. Circuit in finding the CFPB’s structure unconstitutional. Nonetheless they did not believe the remedy was to toss this case or prevent the CFPB from carrying out its operations. Instead, they ruled that the CFPB’s director must report to the President of the United States to come into compliance with Article II of the US Constitution. The CFPB has refused to comply and is already appealing the D.C. Circuit’s decision.

The CFPB’s quest for power however, may come at a cost. That’s because President-elect Trump has pledged to repeal and replace the Dodd-Frank Act, the law through which the CFPB’s power is vested.

Despite the Consumer Financial Protection Act’s exemption on vendors that simply provide advertising space, a decision Google made earlier this year to ban all payday lenders could have something to do with their fear of being labeled a middle man and covered service provider.

The History of Alternative Finance (As Told Through Memes)

November 21, 2016Exactly four years ago, I honored the Thanksgiving holiday by slightly exaggerating the industry’s history in a blog post. And every year around this time since, I’ve reposted it to the home page for all the newbies to enjoy. But in 2016, it just doesn’t seem as applicable. Too many things have changed, especially compared to when I first joined the industry.

The technological experience I remember as an underwriter back in 2006 might as well have been the 1700s. From my perspective, here’s how things have changed:

I don’t know about you, but I am afraid to see where we will be in 2026.

Happy Thanksgiving! 🙂