sales

Learn From Josh Feinberg and Will Murphy in Person at Broker Fair

April 16, 2019You’ve seen them on social media. Now you can see them in person. Josh Feinberg and Will Murphy of Everlasting Capital will be doing a joint presentation on how to scale your broker shop at Broker Fair on May 6th at The Roosevelt Hotel in New York City.

Limited tickets are still available. Register now at Brokerfair.org

The Everlasting Capital co-founders will be presenting at 3:15pm on May 6th in the Promenade Suite. To view the full agenda, CLICK HERE.

-

Brokers

Access to the conference as a broker - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop of The Roosevelt Hotel

- Your conference badge will identify you as a broker

-

Funders/Lenders

Access to the conference as a capital provider - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop of The Roosevelt

- Your conference badge will identify you as a direct capital provider

-

General Admission

Access to the conference as a third party - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop at The Roosevelt

What Am I?

Broker

- You are employed by a non-bank business financing Broker/ISO — OR — You are an independent sales agent

- You are NOT employed by a direct lender or direct funder

- Broker Fair reserves the right to verify your selection.

- Your conference badge will identify you as a broker

Funder/Lender

- You are employed by a direct capital provider whether it’s loans, merchant cash advances, factoring, or other products

- Your conference badge will identify you as a direct capital provider

General Admission

- You are not employed by a broker/ISO or direct capital provider

- Your conference badge will not display a specific business model designation

- You will have the same conference access as a funder/lender does

LinkedIn Posts Are Turning Into Deals & Dollars

March 14, 2019

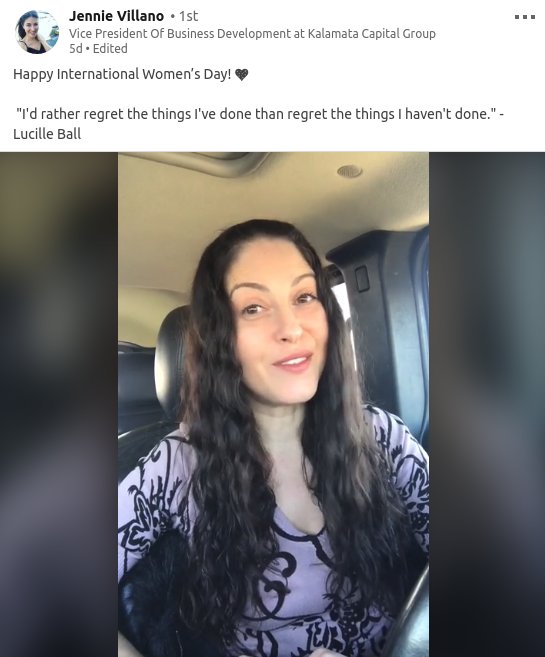

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

Villano is among the growing crowd of industry insiders attempting to convert social media posts into measurable business. With more than 600 million users on LinkedIn, there is no question about the potential to reach clients. The prevailing wisdom is that you need to be on social media and sharing, but share what exactly?

New Hampshire-based Everlasting Capital is building a window into the business lives of co-founders Josh Feinberg and Will Murphy. One of their recent social media posts focused on their search for a new office lease, while another was a video stream of Feinberg making a real live cold call. The rewards span the gamut, from merchants seeking funding to offers to speak professionally in front of large audiences. And it’s not just about them. “We have worked with our employees to get confident on camera which is making them a lot more comfortable on the phone,” Feinberg said.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

For Jennie Villano, it’s not always a sales pitch. She has posted about being a single mom and about how to keep an upbeat attitude. “Your co-workers, your friends. Are they positive, or are they always complaining?” Villano asks in the video. “Try to surround yourself with positive people who see the best in everything.” She’ll typically extend the offer to do business in the videos that she makes and shares, but not all of them. She shares 2-3 videos a week and her posts typically receive thousands of views.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Though other social networks are being used in full force by many industry players, LinkedIn is definitely a platform to consider. “We’ve gotten tremendous value from posting to LinkedIn,” Smart Business Funding’s Collin said.

Storytelling Sales Expert Kindra Hall to Keynote Broker Fair 2019

March 7, 2019 Sales expert Kindra Hall will present at Broker Fair 2019 to teach attendees about the irresistible power of strategic storytelling. If you want to learn to sell differently and use the power of storytelling, her keynote is something you won’t want to miss!

Sales expert Kindra Hall will present at Broker Fair 2019 to teach attendees about the irresistible power of strategic storytelling. If you want to learn to sell differently and use the power of storytelling, her keynote is something you won’t want to miss!

According to Hall, the shift from a transactional economy to a connected one has people scrambling; when surveyed, companies admit they believe a substantial portion of their revenue is under threat as a result. Businesses, brands, sales forces, marketing teams and leaders at all levels are desperately trying to capture attention and resonate with consumers who expect more. Is there a secret weapon? A silver bullet to humanize and connect? Yes. The answer is strategic storytelling.

The problem? In its rapid rise in popularity, “storytelling” has been reduced to in-actionable jargon. Every day businesses and individuals miss critical opportunities to connect with their elusive audiences in powerful and profitable ways because they lack a storytelling skill. Until now.

About Kindra Hall

Kindra Hall is President and Chief Storytelling Officer at Steller Collective, a consulting firm focused on the strategic application of storytelling to today’s communication challenges. Kindra is one of the most sought after keynote speakers trusted by global brands to deliver presentations and trainings that inspire teams and individuals to better communicate the value of their company, their products and their individuality through strategic storytelling.

What began as a storytelling assignment in 5th grade, grew into a passion for not only telling stories, but a mastery for teaching others the methods and science of storytelling so they can better tell their own.

She was a National Champion storyteller (yes, they have those), member of the Board of Directors of the National Storytelling Network and has her master’s degree in communications where she conducted original research studying the role of storytelling in defining and revealing organizational culture.

Kindra is a former Director of Marketing and VP of Sales. Today, Kindra’s work can be seen at Inc.com, Entrepreneur.com and as a contributing editor for SUCCESS Magazine. Kindra’s message spans all industries and her clients include Facebook, Hilton Hotels, Tyson Foods, Target, Berkshire Hathaway and the Harvard Medical School. Her much anticipated book will be released by Harper Leadership in the fall of 2019.

Selling a Home, Selling Commercial Financing – What’s the Difference?

November 16, 2018 Alternative funding brokers come from all different backgrounds, but for many them, being a broker is not their first job in sales. Some sold equipment, some sold cars and others sold homes. They were realtors. deBanked found two alternative funding brokers with a background in residential real estate and we asked them to compare the similarities and differences between selling a home and selling money.

Alternative funding brokers come from all different backgrounds, but for many them, being a broker is not their first job in sales. Some sold equipment, some sold cars and others sold homes. They were realtors. deBanked found two alternative funding brokers with a background in residential real estate and we asked them to compare the similarities and differences between selling a home and selling money.

Alex Alpert is the owner and CEO of Philadelphia-based Solomon Commercial Lending, which provides clients with a wide variety of funding from SBA loans, equipment leasing, factoring and some MCA. Before starting his company, he had worked as a residential realtor for about five years. When asked about his approach to selling a home versus selling money, he sees them as very different.

“When I consider non-investment home ownership, it is 100% emotional,” Alpert said. “If you think about it, the most expensive and most intimate and emotional purchase that you’re ever going to make is going to be your home. As people, we pour ourselves into our homes. Our homes speak so much about our personalities – what we like, what we don’t. It’s literally like a biography [of someone.]”

Alpert spoke about the intangibles involved in residential real estate, how a lot of it is about the feel of a home, which is highly subjective.

“Instead of you manipulating what they want, it’s just guiding them to reach that ‘ah-ha’ moment,” Alpert said. “I didn’t walk around the house with them and say ‘This is the bedroom and this is the bathroom.’ I would stay back and just say ‘Take a walk around, see how it fits, jump in the bed if you want to, and see how you feel.’ And when they came back down, one of my common first questions would be, ‘Can you picture yourself living here?’ Because that question makes you visualize yourself waking up there. If you can pick up on what the person is showing at that moment, you can guide them better…I think I’m successful because I’m honest, I’m transparent, and I will tell you things you won’t expect. And at the end of the day, that’s how you build referrals and address the needs of an emotional transaction.”

On the other hand, Alpert sees non-primary home deals as more transactional.

“When it comes to business, it’s much less personal,” Alpert said. “People will certainly do their research on who they engage with. Most all of my business comes from referrals. But still, you don’t know me from Adam, and you’re sending me over everything…With [business transactions,] it’s based on need and your ability to serve that need. The emotional part, just from the start, is not that present. It’s a need and solution type of approach.”

Alpert will work with clients with tens of millions of dollars in revenue. But he acknowledged that for some of his smaller “mom and pop shop” clients, transactions can be emotional, like with a small town dance studio client he is helping to secure a 7(a) SBA loan for.

James Celifarco, President of Horizon Financial Group in Brooklyn, which offers mostly small business loans and MCA, currently works as a realtor as well. He doesn’t see much of a difference in the way he approaches residential real estate clients versus small business merchants.

“I think they’re very similar in that if [people] are buying or selling a home, it’s their most coveted possession,” Celifarco said. “It’s what they’ve worked the hardest to obtain. It’s their biggest asset. And it’s the same thing when dealing with a business owner. Business owners are probably more passionate than a homeowner. Either way, if you’re dealing with a business owner or a homeowner, it’s their prized possession.”

While not using the word “emotional,” Celifarco seemed to suggest that non-residential real estate deals are just as emotional.

“[For both homeowners and business owners,] you really have to deal with kid gloves in that they play very close to the vest,” Celifarco said. “You have to have a certain approach where they feel comfortable speaking with you about their home and their finances or their business and their finances. They want to know that their information is protected.”

Celebrity residential real estate agent Ryan Serhant, who spoke at Broker Fair 2018, said that he lives be three rules to successful in real estate: Follow up, Follow through and Follow back. The last refers to following back a client on social media. This part might not always apply, but Celifarco said that the same persistence is required regardless of the sales client.

“It’s all sales,” he said. “You eat what you kill. You close a deal, you make money. You sell a house, you make money. If you don’t, if you’re not reaching out to your clients, you’re not going to make any money. It’s the same in that you get paid for how hard you work.”

How to Use Your Clothes to Get Deals

September 17, 2018 Most people are always trying to find more business and make more money. But most of us don’t think of our wardrobe as a way to accomplish this. That is, except for Chief Marketing Officer at Quicksilver Capital Paul Boxer, who looks in his closet and sees business opportunity. Boxer is known for going to industry events wearing a suit with a pattern of $100 bills piled on top of each other. Not one for understatement, he pairs it with a similar tie, enveloped in cash.

Most people are always trying to find more business and make more money. But most of us don’t think of our wardrobe as a way to accomplish this. That is, except for Chief Marketing Officer at Quicksilver Capital Paul Boxer, who looks in his closet and sees business opportunity. Boxer is known for going to industry events wearing a suit with a pattern of $100 bills piled on top of each other. Not one for understatement, he pairs it with a similar tie, enveloped in cash.

“I’ve become known as the ‘Money Suit Guy,’” Boxer told deBanked, “and with that, so many people have found me and reached out to work with me. They have all said, ‘if you can wear that and rock it out, I want to work with you.’”

In addition to Boxer’s iconic money suit, he also wears a Quicksilver Capital baseball hat to promote his company and he often wears Quicksilver glasses and cash patterned shoes, which he said he got as a gift from his CEO. Even before his money suit, Boxer wore loud and unusual glasses to start conversations. He says he has over 100 pairs of prescription glasses and he put prescription lenses into his company’s promotional swag glasses.

“I feel that with the attire and suits that I’m known for, people are more prone to come up to me and strike up a conversation. It’s just that – a great conversation starter…And I found that I’ve built many business relationships at events with just the clothing I wear,” Boxer said.

The concept of wearing promotional clothing – namely a t-shirt – to promote a company has been around for years. In fact, in 2009, a young man named Jason Sadler started a company called iwearyourshirt.com, in which he filmed himself wearing a different company’s shirt everyday. He generated over $1 million within a few years, even though he started out with a virtually non-existent social media presence. (He moved on to start something new in 2013).

The concept of wearing promotional clothing – namely a t-shirt – to promote a company has been around for years. In fact, in 2009, a young man named Jason Sadler started a company called iwearyourshirt.com, in which he filmed himself wearing a different company’s shirt everyday. He generated over $1 million within a few years, even though he started out with a virtually non-existent social media presence. (He moved on to start something new in 2013).

The legendary golfer Greg Norman is never seen without his iconic straw hat which he built an apparel brand around that now includes golf shirts, shorts and pants.

And nonprofits have used apparel for years to spread awareness. Think of pink for breast cancer, the red bow for AIDS and Lance Armstrong’s yellow wristband for cancer awareness. But there is definitely opportunity for for-profits to use clothing to turn strangers into paying clients. Or if you will, into money.

deBanked’s San Diego event is also tapping into the creativity. The first 100 salespeople to check in on October 4th will receive a FREE t-shirt that says, “I Can Fund Your Business” and “Ask Me How” on the back. “There is no mention of deBanked anywhere on the shirt,” said deBanked president and event organizer Sean Murray. “We simply want to create opportunities for salespeople to do more business. They can wear it on Main Street, at the gym, or while patronizing small businesses. Someone is bound to ask them how to get funded.”

deBanked’s San Diego event is also tapping into the creativity. The first 100 salespeople to check in on October 4th will receive a FREE t-shirt that says, “I Can Fund Your Business” and “Ask Me How” on the back. “There is no mention of deBanked anywhere on the shirt,” said deBanked president and event organizer Sean Murray. “We simply want to create opportunities for salespeople to do more business. They can wear it on Main Street, at the gym, or while patronizing small businesses. Someone is bound to ask them how to get funded.”

“If we dress the way we want to be perceived, it will in turn be seen that way,” Boxer said. “Dress to impress, dress to rock it out and you will go in with that feeling that you can conquer everything…And you will! It will help you with your mindset which will lead you to close more deals and in effect generate more business.”

Grooming The Best Sales Reps

August 22, 2018The best sales reps have a lot in common – they’re smart, honest, likable, well-organized, thick-skinned and hungry for success. They navigate the difficult early days of their careers in the alternative small-business funding community by persevering despite long hours, countless outbound telephone calls and meager commissions.

“Persistency is really, really the key – putting in the time,” says Evan Marmott, CEO of Montreal-based CanaCap and CEO of New York-based CapCall LLC. “It’s not always easy, but you’ve got to stay late, make the phone calls, send the emails and do the follow-ups. It’s a numbers game.”

Being relentless counts not only when pursuing merchants but also when matching merchants with funders, Marmott emphasizes. “If they can’t get an approval one place, they’re going to shop it out until they get approval someplace else so they can monetize everything that comes in,” he says.

“It’s all mindset and work ethic,” in sales, according to Joe Camberato, president at Bohemia, N.Y.-based National Business Capital. His company works to create a culture that supports the right mindset by working with a firm called “Delivering Happiness.” Together, they forge to a set of core values based on integrity, innovation, teamwork, empathy, and respect for fellow employees, clients and clients’ businesses.

National Business Capital employees learn to live those ideals by working and playing together on the company volleyball team, through work with local and national charities, and at company mixers and staff picnics, Camberato maintains. “We adapt and change, and we’re committed to helping small businesses grow,” he says of the company culture, “and we have fun while doing all that.”

Likeability helps build relationships with customers, says Justin Thompson, vice president of sales for San Diego-based National Funding. “People will do business with people they like and trust,” says Thompson. “It’s really about establishing a relationship first and then establishing quality discovery.” From there, presentation and execution become paramount, he says.

Methodology can make the difference between success and failure in sales, observes Justin Bakes, co-founder and CEO of Boston-based Forward Financing LLC. “Have a defined process and stick to it,” he advises. A well-organized approach inspires trust among clients, establishes and maintains a great reputation; and fosters understanding of the customers’ needs, wants and business operations that help the rep choose the right financing option and appropriate funder. Using technology to wrangle multiple leads and high volume counts for a lot, too, he says.

It’s all part of the consultative approach to sales, says Jared Weitz, CEO of Great Neck, N.Y.-based United Capital Source. Long ago, sales reps may have succeeded by mimicking carnival barkers, sideshow pitchman and arm-twisting medicine-show peddlers. Thankfully, those days have ended – if they ever really existed. Most of today’s successful salespeople earn clients’ respect by becoming knowledgeable, trusted business consultants, says Weitz.

THE CONSULTATIVE SALE

“Someone calls, and there are two ways of handling a deal, right?” Weitz asks rhetorically. Using one method, a salesperson can say, “We’ll fund you this much at this rate today – are we good?” he says. The other way calls for understanding the client’s business – how long has it been open, does it make more cash deposits or credit card deposits, would it be best-served by an advance, a loan, an equipment lease or a line of credit, how much can it afford in monthly payments?

Establishing how the merchant intends to use the funding plays a crucial role in the consultative sale, Marmott agrees. Objections can arise when a merchant learns that receiving $100,000 this week will require paying back $150,000 in four or five months, he notes. So it’s essential to demonstrate that using the money productively will more than pay for the deal. A trucking company can realize more income if it deploys two more trucks, or a restaurant can increase revenue by placing another bar outside for the summer, he says by way of example.

“A lot of salespeople ask a business owner what they need the money for,” observes Thompson. “The merchant says, ‘Inventory,’ and the rep stops right there. I train my reps at National Funding to go two or three clicks deeper.” Examples abound. When does the merchant need the inventory? From whom do they order it? How long does it take to ship? How long does it take to turn it over? What are the shipping terms?

The consultative approach can require salespeople to pose a lot of open-ended questions that can’t be answered yes or no, according to Thompson. Ideally, the conversation should adhere to the 80-20 rule, with the client talking 80 percent of the time and the sales rep speaking 20 percent, he asserts, adding that “a lot of times it’s reversed in this industry.”

Sometimes, however, salespeople should set aside the time-consuming consultative approach and instead find funding for a merchant as soon as possible. That’s true when the business owner can make an opportune purchase of inventory or when it’s time to acquire a competitor quickly. More often, however, it pays to take the time to understand the merchant’s needs and search out the best type of funding for that particular case, top sales people maintain.

Much of the alternative small-business finance industry has caught on to the importance of the consultative approach to sales as the array of available alternative financial products has grown beyond the industry’s initial offerings of merchant cash advances, according to Weitz. The days of scripted pitches and preplanned rebuttals to objections have ended, he says. Today, management trains reps for success.

THE RIGHT TRAINING

Are top salespeople born that way? “Some people hit the ground running, but sales can be taught – that’s for sure,” Weitz says. “The tougher thing to teach is integrity.” Much of the training process focuses on learning the products to enable a rep to make a consultative sale and shoulder financial responsibility, he maintains.

Believing that some people are born to sell provides a crutch to avoid learning what really works, according to Bakes. Training can teach a smart, motivated person how to succeed, he maintains. They don’t have to be born that way.

However, some people do seem born to exert influence, which can translate into sales prowess, says Thompson. Still, those born with a strong work-ethic can overcome other deficiencies, he notes. The work ethic drives them to “come in every day,” he notes. “They’re organized and disciplined. They follow the National Funding philosophy, and they make a ton of money.”

National Funding trains salespeople to view their craft as being defined by two broad elements – art and science, Thompson continues. The science proves easier to master and includes asking the right questions to learn about the customer and the deal. The hard part, the art of the sale, consists of getting to know the business owner, building a relationship and demonstrating expertise. In one example, that’s based on learning how many trucks are in the fleet, whether they’re long-haul or short haul and whether they use dumpsters versus box trailers, he says.

Beyond those important basics, training should be ongoing because selling techniques change slightly as new products and systems emerge, according to Weitz. “One of the things I like about being a broker is the ability to pivot and add another arrow to your quiver,” he says.

Salespeople at United Capital Source talk sales among themselves almost nonstop, which amounts to daily sales training, Weitz observes. That can take the form of describing a challenge and explaining how to overcome it, he notes. A particularly good idea merits an email to the group to share the new piece of wisdom. It’s a matter of constantly refining the approach.

Training can help sales reps understand the businesses their clients run, according to Marmott. Knowing the margins in a restaurant, for example, can help the salesperson explain that the increase in revenue from an expansion will quickly pay the cost of capital, he notes.

Training should teach new employees how business works because common elements arise in enterprises ranging from dog grooming to asphalt paving, Thompson notes. There’s inventory, marketing, employee expense, payroll taxes, insurance and 401k’s in almost any business. “We teach all that to the reps,” he says. Then after conversations with thousands of merchants, reps have a solid foundation in the workings of businesses.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

New hires spend much of their time working with mentors for the first six months and a team leader who works with them indefinitely, Camberto continues. The company sometimes hires in groups and sometimes hires individually, he notes.

National Funding provides three eight-hour days of regimented classroom training on the fundamentals to each of the four groups of 12 to 17 hired each year, says Thompson. The classes cover processes, sales strategy, marketing and the lender matrix. Next comes three months of working with a sales manager dedicated to working with the class. After a total of nine to 12 months, management knows which reps will succeed.

Some shops operate on the opener-closer model, with less experienced salespeople qualifying the merchant by asking questions like how long they’re been in business and how much revenue they bring in monthly, Marmott says. If the merchant qualifies, the newer salesperson who’s working as an opener then hands off the call to an experienced closer to complete the deal. Good openers become closers, but opening isn’t easy because it requires lots of calls, he notes.

National Funding doesn’t use the opener-closer approach because the company believes reps should Participate “from cradle to grave,” Thompson says. “They hunt the business down, build the relationship and handle the transaction from A to Z.” East Coast shops often focus on cold calling and use the opener-closer model, while West Coast shops tend to invest more in marketing and reject the opener-closer method, he noted.

But where do these top salespeople come from?

THE RIGHT BACKGROUND

Prospective sales reps who have just finished college should have a grounding in communications or business, Weitz believes. Experience in sales and a familiarity with dealing with merchants helps prepare reps, he notes. Job history doesn’t have to be in the finance industry. Someone who’s sold business services in a Verizon store or worked for a payroll company, for instance, has been dealing with small-business owners and may succeed more quickly than those without that background.

Sales experience in other industries counts, Bakes agrees, especially in businesses that require dealing with a large number of leads. “Organization and process is just as important as being born with the traits of a salesperson,” he opines.

Life experience that breeds a positive attitude can prove vital, says Marmott. That’s especially important in the beginning when a new rep might take home a paltry $300 in the first month. Later, when the rep has a $50,000 month, he or she will see that their optimism wasn’t misplaced, he declares.

GUYS WHO ARE HUNGRY”

“The biggest thing I look for is guys who are hungry,” Marmott maintains. I don’t need somebody with a doctorate or a master’s degree or even a degree,” he says. “I need somebody who is going to put the work in.” Of a roomful of 25 new reps, two or three will succeed and stay on the job, he calculates. “You get to eat what you kill. If you’re not killing anything, you don’t get to eat.”

“We look for potential candidates who come from backgrounds of rejection,” says Thompson. Their previous sales experience has taught them not to take the answer “no” personally. “It’s part of the business and you continue to move on.”

Although most regard the financial services industry as a white-collar pursuit, “it has blue collar written all over it,” Thompson says, referring to the work ethic required for success. But it’s not just the volume of work. Sixty good phone calls generate more business than 300 mediocre calls, he emphasizes.

GETTING UP TO SPEED

Succeeding at sales requires taking the time to form relationships, understand guidelines, become familiar with lenders and acquire a working knowledge of how clients’ businesses operate, Camberato says. How long does it take? “It’s a solid year,” he contends while conceding that most who succeed operate at a fairly high level before then.

Others disagree about what constitutes being up to speed and how much time’s necessary to achieve it. “I’ve seen it take 30 days, and I’ve seen it up to 120 days,” says Weitz. “The hope is that it’s within 60.”

A salesperson should start feeling better after 30 days and should start feeling good after 60 days, Marmott says. Management can usually identify the strong and the week reps within two to three weeks, he says. “You get the lazy ones that drop out, the guys who aren’t making any money, the ones who aren’t putting the effort in,” he says. “The first two weeks are the toughest because you’re learning the product and how to sell it.”

“It depends on the person,” Bakes says of the time needed to begin selling successfully. “It takes time. It is not something that will just happen overnight.” About six months should suffice to become confident as a closer, he estimates.

Even when sales reps hit their stride, some outsell others, Marmott notes, citing the 80-20 rule that 80 percent of the business comes from 20 percent of the salesforce. Outbound sales to merchants who may feel beleaguered by offers of funding requires more effort than when a merchant makes an inbound call to seek funding, he adds.

And even the best salespeople need great marketing and tech support from the their companies, sources agree.

INVESTING IN SALES

A shop just starting out might have a marketing budget as low as $2,500 a month, which won’t do much more than pay for direct mail pieces that might prompt a few potential clients to pick up the phone, Weitz says. With a little more money to spend, a shop can begin buying leads, he notes. “Don’t break the bank before you understand what formula works for you,” he advises.

“The key to sales is marketing,” says Marmott. “You can be the best sales guy but if you don’t have anything qualified to call or follow up with, it’s a waste of time.” Social media doesn’t work as well for business-to-business contact as it does for business-to-consumer marketing, he says. Pay per click and key words have become more expensive and isn’t as cost-effective as it once was, especially for smaller shops, he contends. Mailers can work but require heavy volume and repetition, he says, adding that could mean at least 25,000 pieces and at least three mailings.

Besides allocating marketing dollars, companies can invest in sales by paying new sales staffers a salary instead of forcing them to rely on commissions to eke out subsistence during the tough early days. National Business Capital pays a salary at first and later switches reps to commissions and draw, Camberato says. “An energetic person interested in sales can plug into our platform, get trained and do very well,” he continues. “We believe in you, as long as you believe in us.”

National Funding provides recruits with a salary and commissions so that they have enough income to get by and still reap rewards when they help close a deal, Thompson says.

Investment in technology can help salespeople set priorities, eliminate some of the drudge work in the sale process, measure the sales staff member’s success or lack of success, and provide a consistent experience for customers, notes Bakes. “Because of the way our technology is set up we can hold people accountable,” he adds.

Every salesperson and every shop should organize the workflow by using a lead-management system or customer relationship management tool (CRM) – such as Zoho or Salesforce –instead of operating with just a spreadsheet, Weitz says.

Brokers can invest in sales through syndication, which means putting up some of the funds involved in a deal. Forward Financing favors syndication in some cases because it aligns the salesperson and the funder, thus demonstrating the sales rep’s belief in the validity of the deal and ensuring a willingness to continue servicing that customer, Bakes says.

Some shops offer monthly bonuses for outstanding sales results, but Weitz believes awarding incentives weekly makes more sense. With a monthly cycle, some reps tend to slack off for the first week or so because they believe they can make up for lost time later. With weekly rewards, there’s not much room for downtime, he notes.

Whatever form investment takes, it can help build a sterling reputation and a free-flowing “pipeline.”

THE RIGHT REPUTATION

“Reputation is huge,” especially for repeat business and referrals, Marmott says. Once a merchant has received funding, a blizzard of sales call can follow. Treating customers right by maintaining ethical standards and helping them during hard times can guard against defection to a competitor touing low prices, he says.

Reputation requires differentiation, which usually occurs online, by email or over the phone, notes Bakes. Factors that enhance reputation include referrals by satisfied customers and real-world testimonials from actual customers and good ratings on social media sites, he says.

While it’s still uncertain what role social media plays in the industry’s reputation-building efforts, it appears that text messages elicit quick responses if the client has agreed to communicate with the company via that format, Bakes says. He notes that unwanted text messages won’t work. Email messages provide more information than text messages but seem less likely to prompt response, he says.

THE RIGHT GOAL

So, where does the effort to succeed at sales lead? It’s the foundation for building “the pipeline” – the name given to the flow of renewals, referrals and leads that makes every day not just busy, but busy in a productive and profitable way. As a rep’s pipeline takes shape, the cost of acquiring new business also goes down, Marmott says. “It just grows from there,” he says of the successful salesperson’s endeavors at building a pipeline of business. It’s what successful salespeople seek.

9 Real Industry Stories To Get You Fired Up

March 7, 2018 Whether you’re working from home as an independent agent or you’re the owner of a young alternative funding startup, here are nine deBanked stories that are guaranteed to inspire. For those of you that haven’t been in the industry very long, you’ll definitely want to read some of the older ones!

Whether you’re working from home as an independent agent or you’re the owner of a young alternative funding startup, here are nine deBanked stories that are guaranteed to inspire. For those of you that haven’t been in the industry very long, you’ll definitely want to read some of the older ones!

Nest Planner: The Story Of A Startup MCA Broker | 3/4/18

Hard Work, Big Success – The True Story of an MCA Broker | 12/15/17

A True Rapid Advance For Mark Cerminaro | 12/16/16

Can an ISO “Excel” in 2016? | 8/26/16

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True? | 4/28/16

The Dual Aura of Fora – How Two College Friends Built Fora Financial and Became the “Marketplace” of Marketplace Lending | 2/16/16

The Closer – Meet the Yellowstone Capital Rep That Originated $47 Million in Deals Last Year | 2/10/16

Meet the Source: How Jared Weitz and United Capital Source became one of the industry’s fastest growing shops | 10/23/15

From Lowes to Loans: Meet William Ramos | 4/12/15

Ready to network with your industry peers in person? Register For Broker Fair! coming on May 14 in Brooklyn, NY.

Hard Work, Big Success – The True Story of an MCA Broker

December 15, 2017Sales is a tough field for anyone to break into even if they come from the most ideal of circumstances. At some point, the rubber meets the road for every MCA broker, at which time they must decide whether they’ve got what it takes to make it in this business.

This is what makes Lerry Dore’s story so remarkable, as it seems that the more he got knocked down in life, the higher he was destined to rise. Today he’s employed as an MCA broker at Cresthill Capital. And while education has been paramount to getting him here, evidenced by the fact that during his entire employment he has been in college and he is still one of the funding company’s most successful brokers, Dore more than anything else was trained at the school of hard knocks.

Coming to America

Dore was born in South Florida, but he wouldn’t stay in the United States for long. After his parents split up, his mom was having a tough time making ends meet and made the impossible decision to send him to Haiti to live with extended family.

“My mom had a very hard time supporting us right out of the gate. Soon after I was born, I was sent to Haiti to live with my aunt and cousins,” he said, adding that this gave his mom a chance to get on her feet. “She needed to get a job so that she could provide for us at a basic level.”

Dore would remain in Haiti for the first three years of his life, where his first language would become Haitian Creole. But you wouldn’t detect a hint of an accent talking to him today at the age of 23.

Dore’s mom eventually found a job. She was only earning minimum wage at a hospital, but it was enough to get the wheels in motion to bring her son home.

“She was in a position to provide food, electricity and shelter for us. That’s why I came back,” said Dore, adding that he doesn’t remember much of Haiti with the exception of the plane ride home. “That’s where my memories start,” he said. Perhaps it was somewhere over the Caribbean that young Dore’s dreams began to form.

When he got back to Florida, Dore was able to meet his mom for what felt like the first time for him. He also met his brothers and sisters for the first time ever. He explained how at this point, his mom was still getting adjusted to life in America as an adult immigrant.

“There were a lot of things that I went through as a kid to this point that she couldn’t give me guidance on. She simply didn’t have that experience. That brought a challenge,” he said. Little did he know that these obstacles would help shape him into the resilient person and successful MCA broker he is today.

“There were a lot of things that I went through as a kid to this point that she couldn’t give me guidance on. She simply didn’t have that experience. That brought a challenge,” he said. Little did he know that these obstacles would help shape him into the resilient person and successful MCA broker he is today.

While getting used to the American culture was a challenge, something that his mother never lost sight of was the importance of education. “She was very big into education,” he said. Dore’s mom discovered Head Start, a government subsidized program that provided a pre-school education for families who couldn’t otherwise afford it. That was where it would all begin for Dore, and come hell or high water his mother was going to enroll him. Without the luxury of an air-conditioned vehicle to drive in the hot Florida heat, the pair set off on foot to sign up. Some 12-15 blocks later they arrived.

“Both of us were sweating bullets. She didn’t know it, but there was a small registration fee. At the time, she didn’t have it,” Dore explained. It was then that fate seems to have stepped in in the form of the woman who was handling registration. She pulled the pair aside and told them that after witnessing the dedication that this mother had toward her son, she was going to waive the fee. In return she only asked that they keep it on the down low.

“That small gesture made a dramatic difference in my life,” Dore said. “If I was not able to attend, I wouldn’t start school until I was seven or 10 years’ old. That was a very important moment in my life.”

Indeed, it was, as it would set in motion a series of events that would lead Dore to where he is today, a successful MCA broker at Cresthill Capital. But before he would join the firm, there were still more hardships waiting for him, not the least of which was the death of a friend in his teenage years. “That could have been me,” Dore exclaimed.

For the average person, life’s setbacks could have held them down forever. For Dore, they seem only to have propelled him further. “The reason why I stayed out of trouble was I was in school and my mother kept us grounded,” he said.

During his teenage years, Dore and his family lived in an apartment complex in a neighborhood of immigrant Haitians where he said the median income was $25,000 to $30,000 per year. He shared a room with his brothers and sisters.

“I focused on athletics,” he said, adding: “That’s where I got my competitive nature. Also, my thick skin,” both of which, incidentally, are characteristics that would serve him well as a broker later in life.

While he excelled at basketball at his Boca Raton high school, Dore wouldn’t be able to pursue those dreams for long. He and his family would be uprooted from their home time and time again amid landlord trouble. This series of setbacks, which involved him sleeping on his brother’s couch for a time, instilled a sense of maturity in Dore at a very young age.

He had a few Division II and Division III offers to play basketball in other states, but he turned them down. Instead of chasing his own dreams, Dore decided to focus on business and find a way to sustain and support his family “Once I graduated, I was not interested in basketball. I wanted to finish college,” said Dore, and lucky for the MCA industry he had his sights set on the field of finance.

Funding Merchants

After High School, the first thing that Dore did was to go online and look for a job. As it so happens, the first ad he saw was at a stock brokerage in Boca Raton. “That’s where I started, in phone sales. I didn’t have a Series 7 license at the time. I was just calling from the Yellow Pages. Once I got someone on the phone, I would transfer the call to someone who had a license,” he explained.

This went on for a couple of months until he heard about a startup company in nearby Delray Beach. “At the time, they were prospecting merchants. That’s how I got into the industry,” he said.

His first job in the MCA niche was with a very small ISO shop. But it was there that he would make a connection to change the course of his career. He was working on a deal that was hard to place and was only getting rejections. That is until he came across Mike Daniels, Cresthill’s No. 1 producer.

His first job in the MCA niche was with a very small ISO shop. But it was there that he would make a connection to change the course of his career. He was working on a deal that was hard to place and was only getting rejections. That is until he came across Mike Daniels, Cresthill’s No. 1 producer.

“I couldn’t get the deal done anywhere else. The merchant was getting frustrated with the process. I heard of a company that takes chances on merchants with imperfect credit,” he said. That funder was Cresthill Capital. Little did he know at the time, but they would eventually become his employer.

He sent the merchant file over to Daniels, who then reached out to the merchant and got the deal funded. It was at that point, Dore said, that he started to fall in love with Cresthill “because of how [Daniels] was able to treat the merchant with respect and get the deal done.”

For the next six months, Dore would proceed to trust all of his business with Cresthill. He was still employed by the small ISO shop, but he began to outgrow his environment and long for a platform that allowed him to explore his talent and excel. But his pursuit only left him frustrated and thinking about leaving the MCA industry, something he confided in Cresthill Capital’s Daniels, who was turning into a mentor, about.

It was at this point in his life and career that instead of being the rock, Dore needed to lean on someone else. Daniels and Cresthill Capital were there for him. He was invited in for an interview, and as they say the rest is history.

“I was shocked at how diverse the workforce is. There were different types of people with different backgrounds. I liked it right off the bat. And then everyone was very friendly to me from the moment I walked in,” he said. He was greeted at the front door by Cresthill Capital’s Mike Marano, who then proceeded to interview him.

“I’ve actually interviewed and sat with every single person at my company and hired them personally. What I can say about Lerry is that from the moment I looked at his face and saw his eyes, I knew intuitively that he was a good person. And responsible. I had no idea how deep of a person he was, how much humanity he would show. He was a willing student, and we were happy to teach him. And he continues to soak it up like a sponge,” Marano told deBanked.

“I’ve actually interviewed and sat with every single person at my company and hired them personally. What I can say about Lerry is that from the moment I looked at his face and saw his eyes, I knew intuitively that he was a good person. And responsible. I had no idea how deep of a person he was, how much humanity he would show. He was a willing student, and we were happy to teach him. And he continues to soak it up like a sponge,” Marano told deBanked.

Dore was convinced Cresthill Capital was the right place for him when Marano insisted that Dore stay in school and continue his education. “They said, ‘we will work around your schedule,’ and that really drew me in,” he said, adding that the dog-friendly environment was a bonus.

Dore has been employed by Cresthill Capital for the past 18 months and is graduating from college this week. He is not only supporting himself, but he’s the highest earner in his family, which has allowed him to help support them.

Paying it Forward

As if on cue from the mystery lady that paid his school tuition when he was just a child, Dore is now interested in paying it forward in life. He said that similar to how Cresthill Capital is involved with philanthropy, he’d like to give back to the community. But his vision goes beyond his neighborhood.

“I want to help kids that are similar to me, who are in programs that try to help them excel in this country. I want at some point to work with immigrants that come in from Haiti and work with them to give them a platform, like the lady who gave us a chance,” said Dore.

Since the Haiti earthquake, his extended family has relocated north to Canada. “But I still feel to some degree a responsibility to try and help out the people in that country and the ones who come here through immigration,” he said.

As for Marano, he said all Dore needs to do is exactly what he’s been doing. “When he leaves me, he won’t have to work again. But knowing this kid, he probably will anyway,” Marano said.