MPR Authored

The Funders of Summer

August 2, 2012What’s new? Who funded? What happened? Merchant Processing Resource will try to give you a glimpse into the Merchant Cash Advance (MCA) universe:

We all know salespeople love to fund, but underwriters?!! This banner hangs on the wall of the underwriting department at mid-sized MCA firm, Rapid Capital Funding:

Holy Moses Batman! $10 Million in a month?! Yellowstone Capital is reporting a new personal monthly funding record of $10,245,000.

There has been an influx of really creative instructional/promotional videos about MCA lately. Cartoons are really “in” right now:

PayPal white labeled a Merchant Cash Advance program in the U.K.

Will the mega banks be next?

It feels like 2006 all over again says First Annapolis Consulting in a recent article:

This seems to be the same bullish sentiment that surrounded the industry in 2006, when there was a constant influx of new MCA providers into the industry and what appeared to be unlimited financial sources. What might be different now is the experience accumulated in the industry during the recession. In the last few years, and as a result of the mounting losses that the industry suffered during the economic crisis, MCA players have implemented more conservative risk management practices and procedures.

Underwriters industrywide are also reporting that stacking, splitting, double funding, and fake statements are on the rise. It certainly brings back some nostalgia for veterans and not the good kind. A screenshot of a current ad on craigslist that is directed at bad apple merchants:

A new chapter opened for Merchant Cash Advance (This is soooo last month but a great read if you missed it).

http://greensheet.com/emagazine.php?issue_number=120602&story_id=3088

Is the loan shortage a banking problem or a merchant problem? Ami Kassar makes the case in his New York Times column.

“Where are the leads? I need the leads. Can you tell me where the leads are?” We literally get asked daily where to get leads from. We recommend:

http://SmallBusinessLoanRates.com

http://meridianleads.com

By the way… for every company that says cold calling doesn’t work, there’s a company getting rich doing just that. Same goes for SEO, mailers, e-mail blasts, PPC, and so. Marketing is an art form. Just because it doesn’t work for you, doesn’t mean it doesn’t work period. Keep doing what you’re doing. Too many ISOs/agents/marketing directors abandon campaigns after 30-60 days. Practice makes perfect!

Have you abandoned social media? We ask this question: What looks worse to a prospect?

Not having a business twitter account or having one but failing to tweet at all in the last 8 months?

Not having a business blog or having one but failing to add any new blog posts in over a year?

We didn’t spend much time researching hard data but we would surmise that freshness is a psychological component to a prospect’s shopping experience. If a business blogged regularly on their site up until May, 2011 and then stopped, might a merchant think the entire business itself is abandoned or gone? Is a facebook fan page with 1 post from 8 months ago a positive or negative selling point? WE SAY: If you build it, maintain it. Nothing brings down your presence on the Internet like abandonment. We understand that smaller companies might not have the manpower, time, or creative energy to write informative articles or engage people through social networking, especially when it’s hard to measure the results and value it creates. Consider the value you might actually be losing by projecting to the world that you have given up. It’s like operating a store with a sign out front that says “THIS BUILDING HAS BEEN CONDEMNED” even though you are actually open for business. If WE stopped posting articles for a year, would you still come back several times a month?

Here are two examples of MCA firms that keep it FRESH!:

http://unitedcapitalsource.com/blog/

http://takechargecapital.com/category/blog/

Don’t you just love MCA? We do! Visit our site again soon.

– Merchant Processing Resource

https://debanked.com

The Other 93%

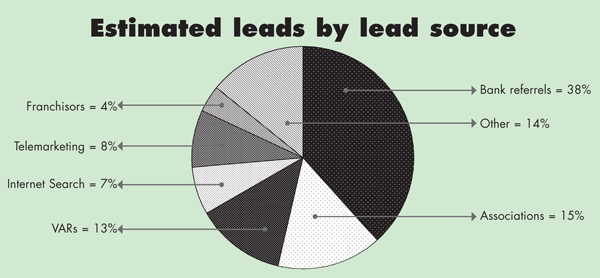

July 13, 2012The SEO war rages on for Merchant Cash Advance providers, ISOs, micro lenders, and other financing firms, but just how much real estate is everyone really fighting over? According to data recently provided in The Green Sheet by First Annapolis Consulting, only 7% of all merchant account leads are generated via the Internet. So if your business plan’s success hinges on getting to page 1 of Google search, you might be shutting yourself out from nearly the entire marketplace. Don’t get us wrong, there’s a lot of money to be made and business to be acquired via the Internet, but even the big firms get roughed up from time to time by competition, new algorithms, and SEO companies that promise the world but deliver few results.

So if not the Internet, then what else is there besides cold calling? That’s a question that tons of small ISOs ask themselves when they realize that competing online isn’t easy. It just so happens that the “what else” comprises of 85% of all generated leads in the payments industry. More than 50% are derived from bank referrals and associations alone.

Has anyone ever wondered why companies like AdvanceMe (Capital Access Network) are still number one in the Merchant Cash Advance arena? They’ve managed to defy Darwin’s theory of evolution. In every industry, there is a pioneer that leads the way, gets too comfortable, stops innovating, and is systematically made irrelevant by fresh thinking competition. There was MySpace until there was Facebook. There was Yahoo until there was Google. There was AOL until…there was just everything else.

So one would expect that in 2012, the mere mention of AdvanceMe would be part of a requiem for the founding fathers of the Merchant Cash Advance industry. That isn’t the case and is quite the opposite considering they are on pace to fund at least $700 million this year. So they must be #1 on Google, right? Nope. For all of the main keywords that people are fighting over, they rarely if ever, even show up on the first page of the results.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

All the sales pitches in the world about lower rates and free POS systems aren’t going to compete with a merchant who has just been given a referral by a company they already have a relationship with. Hell, even you have probably enlisted an insurance company, wedding vendor, or mortgage broker because someone you trusted said they were great.

This isn’t another lecture about how referrals are crazy good and that cold calling is wicked bad, especially since we don’t even necessarily feel that way. The point is really to highlight just how much more potential there is out there for small funders and ISOs. You can actually be successful with a sucky website and no SEO if you can just solidify some key relationships.

If you want to be around 14 years later, you can’t ignore the other 93% of the market. The volume of Internet leads will probably increase in the future as more computer savvy people become small business owners. But it’s way too easy to set up a website, hire an SEO guy, and throw money at Pay-Per-Click. Anyone can do it and everyone is doing it. That means most companies are losing the battle and tons of you are saying “what else is there?” Fortunately, the lead generation pie chart offers unlimited hope. You just need to think bigger and try harder.

If the other categories seem too ambitious, well then you’ll never make it in this biz kid…

The American Obsession With Startups

June 20, 2012Hi, I was just driving down 3rd Street and I saw an old building that had a For Sale sign on it. So I was just thinking it would be a great place to open a restaurant. It would have a really big outdoor eating area and I’ve always dreamed of owning my own restaurant. Lord knows I love food. I can’t talk long but I Googled loans on the Internet and you guys came up so I wanted to know if I could get a $4 million loan or line of credit to buy the building, fix it up, and make it into a Mexican restaurant, or maybe even Italian! Is that something you could do? I would need the money by friday…

This is the real transcript of a call to a Merchant Cash Advance brokerage. Don’t let anyone tell you that the U.S. is not a capitalistic society. Opportunity and entrepreneurship is so ingrained into the very fabric of our being that even self-proclaimed communists and socialists cast away their utopian worker ideals for the chance and self-satisfaction of turning something small into something big. We’re also an impulsive society, a trait partially due to our obsession with immediate self-gratification, but more to do with the fact that opportunities come and go in the blink of an eye. It is for these reasons that an individual who was taught to do market research, create a business plan, and mull things over is instead flying down the road with one hand on the wheel while the other hand is furiously applying for a $4 million loan to finance an opportunity he thought up 7 seconds ago.

How many other people driving down this road thought the same thing? How many of them have access to that kind of capital? Some might and so for the ones that don’t, the fear that someone is going to beat them to it turns them into unrealistic cash demanding lunatics. It’s true. The full service Merchant Cash Advance shops should probably offer John (the name we’re going to assign to the guy driving down the road) a proposal to help him create a business plan, form an LLC, and obtain the necessary licenses. These services would come with a price, a price that many people like John misinterpret as obstacles to be handled once he’s received the $4 Million. As John continues driving down the road, the dream of starting a restaurant is repeatedly crushed as he makes phone call after phone call to business lenders he found on the Internet. “There’s just no help for startups,” he concludes, and decides to hold off until the economy gets better before giving it another shot.

For 37 minutes that day, John was one of the many millions of startup businesses searching for capital. For the Merchant Cash Advance brokerage, he may have been one of the few hundred phone calls an account rep was bogged down with, while trying to help businesses that have been open for at least 1 year. The account reps have probably heard it all. “I want to start a home-based gas station“, “I need twenty million dollars for a good idea that I can’t tell you what it is because I don’t want anyone to steal the idea“, “I just got an LLC and I need $100,000 to come up with some business ideas“, “I’m gonna start an online shoe store and I need money to buy my first computer so I can get on the Internet.” We’re not poking fun at entrepreneurs since there are plenty of those who are really serious. But for the millions that call first and think second, they’re creating a disease unique to the U.S. It’s called startup fatigue. Business lenders are losing so much money by just talking to non-business owners, that they’ve taken to putting up big signs to ward them off.

The Internet is a great example because the cost of one click to the lender’s website can reach as high as $20. So how then does one tactfully express that their financing programs are for existing businesses only? It’s an art form that many have difficulty mastering. Advertisements, which are usually created to rope people in are instead being crafted to keep people out. “Hey Startups, GET OUT AND STAY OUT!” is the marketing campaign some lenders might be considering rolling out next quarter.

We expect that at this point in our post, startup specialists have already stopped reading and have instead taken to writing us long e-mails explaining how ignorant we are.

“DEAR MPR,

You are dumb. There are tons of startup lenders out there just begging for business.”

We’ll welcome any e-mails like this. Maybe these companies will stop hiding in the shadows and we can finally start helping people.

Raharney Capital, the organization that owns Merchant Processing Resource has a division that connects existing small businesses with financing companies. Coincidentally, they encounter a lot of pre-operational startups and continuously face the dilemma of how to service them.

Their first attempt to refer them out was with Go Big Network, a gargantuan networking service specifically for startups to obtain capital. Their homepage touts:

We help entrepreneurs find funding.

Over 300,000 Startups Have Used Go BIG to Connection with Millions of Dollars in Funding. Join today to connect with our network of over 20,000 investors.

They’ve been around for years and their advertisements can be seen all over the web. Inquiries about referring startups to them for a fee went nowhere as Go Big Network made abundantly clear that they did not want affiliates. Further attempts to refer them the business (even free of charge) went unanswered. It seems that even the startup masters don’t want to deal with more startups.

So we took to LinkedIn discussion groups and replied to the many individuals claiming to be angel investors or startup lenders. All of them backtracked on their original statements, with most eventually revealing that they were really looking for businesses that have been operating two years with positive cash flow. Are they liars? Not really. A young business is technically still a startup. What we did find though is that some Merchant Cash Advance providers are funding businesses that have been open for as little as three months. Not bad! (Check out: Capital Stack, Yellowstone Capital, United Capital Source, and Merchant Cash and Capital)

We thought we struck gold when we joined Startup Specialists, expecting to find lenders swarming the discussions with startup lending spam. Instead, we found no mention of financing at all. Interestingly though, this group was abuzz with activity. Thought you were cool because your post got 1 thumbs up? Thought that nothing was happening on LinkedIn? Some posts in this group are receiving hundreds or THOUSANDS of engaging, thoughtful responses! Sadly, no one seems to know where the money is, but that doesn’t seem to matter to them.

While writing this, our own inbox has grown considerably bigger and our voicemail box more full. Many are reaching out to us with questions about startup financing. The fatigue is slowly starting to set in.

One is a voicemail from Google, asking us to reactivate our Adwords campaign, something this site experimented with in the past with $100 in free ad credits. In their message, the account rep mentions that they have reviewed our site and can help startup lenders like ourselves create successful ads(what gave them this impression?). In startup-obsessed America, a stable, sustainable, and somewhat aged business is a mythical beast. Even Google has somehow mistaken our small business information site to be startup information. Too many people assume that small business means the act of trying to start a business. “Do You Have An Existing Business?” a bank advertisement might ask. Tons of people who don’t will still answer ‘yes‘ simply because the idea exists in their mind. It’s a beautiful thing in America to think that way, but getting off the ground and generating revenue shouldn’t be like winning the lottery, a game that you’ll never win but is fun to dream about.

We have interviewed writers for our site, some for volunteer positions, others to be paid. While instructing them to use small business as the subject matter, almost all of them revert to writing about starting a business. Marketing companies have also made the same mistake by pitching us their proposal to make cool videos for the site and then go on to create a demo video that talks about starting a business. One company actually asked us to provide a script and still they CHANGED IT to talk about how Merchant Processing Resource is a premier helper of startups. WHAT?!!!

By now, we’re running a high fever and the doctors suspect we have startup fatigue. Eleven more people have left voicemails, to request $300, $10,000, or $100,000,000 because they have this really sweet idea to make a restaurant named Chesster’s, (Chester’s with a double ‘s’) because each dining table will have a chessboard on it with chess pieces. Boo ya!! They haven’t worked out all the details yet but they thought the name was brilliant and oh yea… they need the money by tomorrow.

We’ll refer them to SCORE, a nonprofit association dedicated to helping small businesses get off the ground, grow and achieve their goals through education and mentorship. They may not get financing, but they will get HELP. And that’s really what Americans need. There isn’t a lending problem, there’s a helping problem.

Entrepreneurs like Mark Zuckerberg made it tougher for all of us. His progression went from random idea to scooping up cash from a classmate, to billionaire CEO of a publicly traded empire. He didn’t sit down with a SCORE mentor, do market research, and consult with a lawyer about how best to structure an organization. These are things he would have considered as obstacles to achieving his dream before someone else beat him to it. “I need the money by friday because this is going to be big,” Zuckerberg might have told a Merchant Cash Advance account rep who had heard the same story 97 times that morning alone.

Zuckerberg’s whirlwind success story portrays him as a role model genius, a boy who acted and capitalized on the split second window of opportunity while all the pieces fell into place after the fact. The rest of America so badly wants to replicate that. Too many people envision themselves in an interview with a New York Times reporter two years from now to talk about how they were driving down 3rd Street and the idea of starting a home-based gas station just popped into their heads, prompting them to Google business loans, and the rest of their billion dollar story is history. Similarly, when that doesn’t happen, just as many people chalk up their failure to a bad economy, Obama’s unwillingness to help, or the big bad banks indifference to the little guy.

It’s okay to go slow and get your ducks in a row. Hell, doing it this way is probably more honorable than what Zuckerberg did. You don’t need the funds by tomorrow, friday, or even next week. What you need is proof that you can provide a product or service for a profit and then to carefully plan and structure an organization that will last. Raising money should be a contingency for expanding sales, not for registering your LLC or to solidify an idea.

There’s a reason that the topic of small business is inundated with information on how to start one. So many fail to get off the ground. There are conflicting and sensational statistics that claim that 9 out of every 10 startups fail. In startup-obsessed America, it’s probably more than that. We would argue that John’s wild foray into entrepreneurship started when he spotted available space for a restaurant and failed when his first instinct was to search for lenders. In the meantime, a few financial firms got caught in the cross fire and spent money to answer his phone calls. Both sides were left frustrated since neither got what they wanted.

In today’s world there is a growing anti-startup movement. Americans want jobs to feed their families and lenders prefer to invest only in existing businesses. The problem is that without startups, fewer businesses will become established (bad for lenders) and fewer jobs will be created (bad for Americans). Our only hope then to turn the tide is to embrace the startups, not shun them. The message shouldn’t be: Get lost you potential job creating jerks! Every lender (and Merchant Cash Advance provider) should have a model to assist startups in some way. It’s okay to charge for this service and profit from it by the way. Any potential business owner who enters the startup arena expecting not to pay anything out of pocket is dreaming.

If America associates small business with starting a business, can a lender really parade themselves as a small business champion if their public message is to send startups packing? We don’t think they can. Similarly, individuals need to do their part and calm their impulses. Drawing up a plan, forming an LLC, and obtaining the necessary licenses aren’t annoying obstacles to take care of after the fact. You can’t really expect to raise capital on a wild whim while you’re flying down the street talking about a random building you saw on the side of the road. Imagine how crazy that sounds to a lender?

Patience and hard work, we say. That goes for the entrepreneurs and lenders alike. Let’s help each other, not hate each other. It won’t be easy, but then again success isn’t supposed to be like winning the lottery, a game that you’ll never win but is fun to dream about.

Why LinkedIn is King

June 9, 2012This may be risky…but we’re doubling down on LinkedIn. The Los Angeles Times will disagree with us, since they recently embraced the radical view that LinkedIn is a big joke. Sure, LinkedIn recently got hacked and that’s a major security issue they’ll need to deal with, but for the haters that brag they haven’t logged into their accounts in years, they probably missed the point of this social media site. LinkedIn isn’t Facebook. They aren’t even competitors. If you want to share your funny photos and write witty updates about how you hate work, please by all means spare the rest of the business world from it. We’ve got some tips for those haters:

- If you view your job as a 9-5 that’s a burden to living your life, LinkedIn is not for you.

- If you’re employed in an entry level position and don’t care about climbing the corporate ladder, LinkedIn is not for you.

- If your goal is to make sure that you never get any kind of individual recognition in your field, LinkedIn is not for you.

- If you want to avoid talking about your line of work with other like-minded people in a way that can help you grow, LinkedIn is not for you.

- If you’re a business owner that has no desire to speak to other business owners, LinkedIn is not for you.

- If you LOL at the thought of networking, in person or online, LinkedIn is not for you.

- If you want to spam the Internet and submit updates that no one will ever read, go sign up for Google Plus.

LinkedIn isn’t a resumé site or a social network. It’s a cooperative movement to make the private sector vastly more efficient. We’ve heard grumblings from Merchant Cash Advance industry insiders that some of the most popular vBulletin-style forums are pretty much losing their value. The discussion is sporadic, many people hide behind a screen name, and there isn’t any way to validate the information being shared. At best, it’s an anonymous way to spread propaganda. Traditional web forums rely on users to visit the site and once there, go on a scavenger hunt to find new posts and discussions. If there are no new posts, then the time spent going to the forum is nothing more than a waste.

LinkedIn has groups, which are monitored and policed by the group owner much like a forum would be. The stakes are upped because everyone participating can view each other’s business credentials through their profiles. In a traditional web forum, you get situations like this all the time:

The individual offering to sell leads looks highly suspect. If only there were a way to find out who they really were, where they were located, how long they’ve been in the lead business for, what company they work for, who else they know in the industry, who has publicly recommended them, etc. Even if they had included a real company e-mail address and website in their post, there would still be much more information left to be desired. We believe it’s a lot harder to accomplish anything with anyone you don’t know via the inherent anonymity of traditional web forums. Sure, anyone can fake their credentials on LinkedIn but if you see they’re connected with a former colleague of yours, you can call that old colleague right up and get the scoop. The transparency leads to transactions that get closed faster and both parties can feel more confident in their decisions to do business with a stranger.

Is LinkedIn perfect? No, it’s not. But the results are incredible if you know how to use the site correctly. We’ll put it this way, in the month of May, LinkedIn brought 21% more visitors to our site than what came organically from the Bing search engine. If you LOL at that because Bing is notoriously smaller than Google, just think about how much money you or other people you know are spending on SEO experts to get traffic from search engines. So LOL it up because LinkedIn is free.

Those statistics also don’t count the relationships we’ve built purely through the site itself. You see, it’s not always about making a sale and the numbers of connections you have isn’t what we mean by relationships. You’re a lot better off reading the updates of a C-level executive on the ins and outs of Crowd Funding in a LinkedIn group than you would be from reading a sensationalist, empty opinion about it by the LA Times. Comment intelligently to that exec’s posts and you could find them wanting to connect with you to discuss further and possibly do some kind of business together.

Here are some of the industry groups we recommend you check out:

We cordially invite the haters described in the bullet point list above NOT to join. Not that we should really worry they will. If you actually visit the twitter accounts that the LA Times cites as proof of LinkedIn’s unpopularity, you’ll find that these people spend their time online talking about Kim Kardashian, Lindsay Lohan, and other useless crap. They read like play-by-play diaries of a junior high school girl. Hate away losers, they made twitter just for people like you.

To Fund or Not to Fund in Hawaii

June 1, 2012 Aloha! The Resource’s main operator is “busy” vacationing in Hawaii, hence the long gap in site news. But since we’ve got Hawaii on the brain, we figured now is a good time to discuss Merchant Cash Advance (MCA) financing in a state that practically exists in its own universe.

Aloha! The Resource’s main operator is “busy” vacationing in Hawaii, hence the long gap in site news. But since we’ve got Hawaii on the brain, we figured now is a good time to discuss Merchant Cash Advance (MCA) financing in a state that practically exists in its own universe.

Ask underwriters from different firms about how they approach applications from Hawaii and you’ll get some opposing views. Some will argue that the distance is too vast to risk their capital. A business tucked away in the middle of a remote Pacific island may feel less bound by their contractual terms since there is a very small likelihood that a funder will fly thousands of miles to enforce it. “What consequences am I really facing from a company light years away in New York City?,” a Hawaiian merchant might ask themselves. This is a negative Hobbesian view that promotes the idea that merchants are inherently corrupt and that they need a fear of recourse to honor their contracts. There’s a reason that the MCA industry feels particularly vulnerable.

The nature of the transaction provides funders with barely any recourse, giving credit to the psychology that being worlds apart is more than just a paranoid insecurity. When MCAs are structured as a sale, it is not possible to report a delinquency to the credit bureaus since no credit has been extended. Lawyers will argue that MCA funders are protected by their iron-clad contracts which grant numerous advantages to the funders in the event a merchant breaches their contract. However, if a funder files a lawsuit in Brooklyn, NY, how likely is it that a merchant in Hawaii will fly there to respond to it?

Merchant Cash and Capital may have had reason to hate the state back in 2007, when they got burned by Hawaii Travel Network, a Hawaii-based travel agency for an amount close to $1 Million. However, they have continued to fund businesses there without prejudice.

At the end of the day, underwriters must leave their fears at home and rely on data analysis to make decisions. When the financial crisis hit, there was plenty of real data to support why funding in California, Nevada, and Florida was a bad idea. Many local economies got beat up really bad. It’s no wonder that when people started losing their homes to foreclosure, they began to forgo all of their financial obligations in order to get by. It was then that Hobbes’ theory of humanity was more appropriately applied, as merchants reverted to a state of nature and put self-preservation above all else. “If the recourse for defaulting on an MCA is just a lawsuit then so be it,” said a hypothetical business owner who had just lost 60% of his 401k and was hiding out from the Repo Man.

While Hawaii wasn’t exactly made a poster child for economic devastation, it was hit pretty hard by the loss of Americans’ disposable income. 80% of Maui’s economy is related to tourism. That means they are inevitably affected by problems on the mainland. However, one factor that makes Hawaii all the more resilient, is its location. In April 2012, the number of Canadian and Japanese tourists combined outnumbered visitors arriving from the eastern half of the United States. So in hard times, Hawaii may go down, but it will not go out!

Besides, while many mainland states are now coming to terms that the economy is still stagnating, Hawaii earned more income from tourists this past April than in any other April in history. Sure, there are problems, political qualms, and flaws in the state’s infrastructure, but it is really not that much unlike the rest of the country (except for the fact that it is way cooler 😛 ). Many of the vacation destinations feel more like America than some parts of mainland America.

So does the MCA industry really have anything to fear in Hawaii? It depends on the risk tolerance. Travel agencies and tour companies have historically been shunned by funders, although that’s changed a lot in the last six months. Even established tour companies can disappear overnight. Tour companies in exotic locations walk a thin line every second of operation. They face constant injury liability, state and local law restrictions, and pressure from the property owners on which the tours explore to meet a certain standard of care. It can’t be omitted that a few bad online reviews can cause all their potential customers to book with their competitors instead. The Internet is the public’s best resource for researching vacation activities. No one wants to book a tour that has poor feedback.

So does the MCA industry really have anything to fear in Hawaii? It depends on the risk tolerance. Travel agencies and tour companies have historically been shunned by funders, although that’s changed a lot in the last six months. Even established tour companies can disappear overnight. Tour companies in exotic locations walk a thin line every second of operation. They face constant injury liability, state and local law restrictions, and pressure from the property owners on which the tours explore to meet a certain standard of care. It can’t be omitted that a few bad online reviews can cause all their potential customers to book with their competitors instead. The Internet is the public’s best resource for researching vacation activities. No one wants to book a tour that has poor feedback.

Major resorts and hotels are the lifeblood of local economies there. If a big hotel fails, all the small businesses in the near vicinity will go right down with it. Some of the best restaurants in the state are on the grounds of a major resort, highlighting that nearly everything is tied to tourism. The weather too can be fickle.

If a funder can tolerate those risks, and they’re not unlike many of the other vacation destinations in the country, than we say, go for it! But when a Hawaiian MCA deal goes bad and the business phone number is disconnected, go ahead and file your lawsuit in Brooklyn and see how much good it does. You might end up imagining that the merchant has shrugged off your contract to spend their afternoons surfing instead. You’ll kick yourself for doing a deal in such a faraway land.

After being in Hawaii for just a week, I received a phone call from a friend to update me on MCA industry events. Truth is, I didn’t care what he had to say. It’s way too nice here to care about what’s going on elsewhere. If our website goes down next week, you may start to imagine that we have shrugged off the Resource to spend our afternoons surfing instead.

Don’t laugh, because you would be right. The rules change when you’re thousands of miles from the rest of the world. Mahalo and Aloha!

-deBanked

https://debanked.com

Note: No Hawaiians were injured during the course of this blog post.

How The Facebook IPO Affects the Merchant Cash Advance Industry

May 18, 2012 Facebook went live on the Nasdaq earlier today, causing many people to become instant millionaires or billionaires. Yea…soo… how is this in any way relevant to Merchant Cash Advance (MCA)? you might ask. Well, because MCA is the next BIG thing. One of the major winners of the Facebook IPO is Accel Partners, a venture capital (VC) firm that invested $12.7 million in Mark Zuckerberg’s college networking website in 2005. Today, they’re cashing in on billions from that bet. Since then, Accel has repeatedly struck gold by backing wildly successful businesses such as Groupon and Etsy. Many hungry and jealous VCs are looking to jump into any industry Accel likes, to either compete for marketshare or to piggyback on the success.

Facebook went live on the Nasdaq earlier today, causing many people to become instant millionaires or billionaires. Yea…soo… how is this in any way relevant to Merchant Cash Advance (MCA)? you might ask. Well, because MCA is the next BIG thing. One of the major winners of the Facebook IPO is Accel Partners, a venture capital (VC) firm that invested $12.7 million in Mark Zuckerberg’s college networking website in 2005. Today, they’re cashing in on billions from that bet. Since then, Accel has repeatedly struck gold by backing wildly successful businesses such as Groupon and Etsy. Many hungry and jealous VCs are looking to jump into any industry Accel likes, to either compete for marketshare or to piggyback on the success.

And that’s how Facebook and MCA are related…

On February 7, 2012 Accel Partners invested $30 million into Capital Access Network (CAN), the holding company of AdvanceMe and NewLogic Business loans. There was some buzz about it in February, but it faded fast. It seems like every day there is a new press release from some MCA firm bragging about how they secured a mult-million dollar credit line. So it’s no surprise that industry insiders didn’t immediately poo themselves in hysterical awe of this announcement.

CAN is also on pace to fund $600 million this year, an astounding figure that makes $30 million sound like a mere drop in the bucket. It’s as if Accel gave them a Starter Advance. 😉

On a more serious note, the rest of the VC and Growth Capital world waited about 3 seconds before pouncing on all things MCA. The frequency in which we’re receiving random calls and e-mails from “investors” about putting money into MCA providers has increased dramatically. A few other funders and large ISOs have shared that they are experiencing the same thing. Right now there is a great chance that there are back room negotiations going on all over the industry between funders that already have millions and investors that have billions.

Raising capital has never been a real problem in the industry, as the Wall Street establishment has been funneling millions into the New York, California, and Florida MCA powerhouse providers for years. Do we really need Silicon Valley to jump into bed with us? Maybe. Although MCA has been around since the late 1990s, there’s been this lingering acknowledgment that most of the small business market that could benefit from financing still doesn’t know that MCA exists. Way too many business owners respond to an explanation of the MCA program with shock, “Wow, I never knew you could do something like that.” That’s a problem and it’s real.

Sean Murray, the founder of Merchant Processing Resource, recently did a presentation through the Manhattan Chamber of Commerce last month to 30 small business owners about MCA financing. The first question asked by one of the attendees after it was over was, “did you come up with this whole concept yourself?” He certainly did not, and it epitomizes that there is still room for exponential growth in a billion dollar industry that is more than a decade old.

Naysayers predicted that the MCA concept would fail years ago, and yet it has grown, mutated, and evolved. Some folks got into this business in their early twenties right out of college, and have literally made a career out of it. It’s quite a picture to see that they’ve grown up, gotten married, and had a few kids only to learn that Silicon Valley is picturing this entire industry as something still in startup phase. But hey, it took Pinterest years before anyone really noticed it.

In 2012, you can apparently still get in early on MCA. If you have stock in an ISO or funding provider, don’t be quick to sell it. It could be worth millions or billions in the future.

At some point in 2014, the Winklevoss twins will probably claim they invented Merchant Cash Advance, a challenge they will lose badly. Not even CAN, the company that did invent it, was able to prove in court that they did. But they did manage to continue their dominance of the industry and they are the ones that caught Accel Partners’ fancy. But the rest of the MCA players aren’t exactly going to wither away and die like MySpace. So the battle is on and there is money to be made.

Target valuation: $100 Billion. Who’s going to get there first?

– deBanked

https://debanked.com

Read how Merchant Cash Advance could be molded to be more like Silicon Valley: Just Call it a Coupon!