Jersey City is Quietly Becoming a Fintech Hub

January 11, 2018 Jersey City is luring yet another innovative small business finance company to their community. This time it’s NYC-based Pearl Capital. According to NJ state records, Pearl was approved on January 9th for a total of $5.6 million over 10 years to relocate under the Grow NJ tax program to boost jobs in the area.

Jersey City is luring yet another innovative small business finance company to their community. This time it’s NYC-based Pearl Capital. According to NJ state records, Pearl was approved on January 9th for a total of $5.6 million over 10 years to relocate under the Grow NJ tax program to boost jobs in the area.

Other finance companies that have relocated to Jersey City, thanks to Grow NJ, are Yellowstone Capital, World Business Lenders, and Principis Capital. But that’s not all, companies like BlueVine and Funding Metrics have also set up operational centers there.

We do not yet know what address Pearl intends to move to.

What’s Lending Got to do With Cryptocurrency?

January 10, 2018 Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

A meetup hosted by partners of Central Diligence Group (CDG) on Tuesday night in NYC, for example, was geared towards cryptocurrency enthusiasts. CDG is a merchant cash advance and business lending consulting firm. Those that attended, talked candidly about Ripple, Bitcoin, Ethereum, and the hot topic of Initial Coin Offerings (ICOs). And it did seem all connected. Companies successfully raised more than $3 billion through ICOs in 2017, for example, some of them online lending companies.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

Whether these valuations are overdone is besides the point. A smart phone is all that’s required to get in on the action and trade thousands of cryptocurrencies online, many of which move up and down by astronomical percentages over the course of a day. Becoming a millionaire overnight by hitting on the right one is a dream sought after by many. And young people, especially millennials, are become unconsciously comfortable transacting in non-government-backed currencies through technology that completely shuts out banks.

And that may be the shift in all of this to pay attention to. It isn’t that a local restaurant is going to collateralize their Bitcoin to get a loan and outcompete an MCA company, but that a portion of the monetary system eventually starts to sidestep banks.

Trying to collect on that judgment? Good luck tracing the money in cryptos.

Need to freeze funds? You can’t freeze someone’s Bitcoins if they’ve got them stored on their own hardware.

Evaluating a business’s bank statements? The transactions can only be verified on a blockchain.

You might not believe me, but it’s incredibly likely that you’ve encountered a client that has defaulted on an MCA or loan whose stash of money has been obscured in cryptos all the while their bank statements appear to show insolvency.

It’s also likely that you’ve encountered a client that has used the proceeds of their MCA or loan to buy a crypto. Maybe not the whole amount, but with some of it. One study, for example, revealed that 18% of people have purchased Bitcoin using credit. Bloomberg reported that the phrase “buy bitcoin with credit card,” just recently spiked to an all-time high.

People are even taking out mortgages to buy Bitcoin, according to CNBC.

If you think cryptocurrency is an industry completely independent of your business, consider that the market cap of cryptocurrencies is currently valued at more than $700 billion. That’s nearly twice the market cap of Goldman Sachs and JPMorgan, COMBINED. The #3 cryptocurrency by market cap, Ripple, is being pitched almost entirely to traditional financial institutions.

Bet all you want on the prediction that this bubble will burst. Maybe it will. But the underlying technology, transacting without banks in non-government backed currencies that may be difficult to trace and recover, is a genie that’s not returning to its bottle anytime soon.

In the meantime, now might be a good time to poll your employees or colleagues about their knowledge or use of cryptocurrency. You may be surprised by what you find, especially among the younger crowd.

——–

Disclaimer: I currently hold a material amount of Ether, the currency of the Ethereum blockchain.

In 2018, Sell More and Make More Money

January 4, 2018Did you hear about the MCA sales rep that made a $160,000 commission this week on a single deal? It was a monster deal, the largest ever approved by the company that funded it. Numbers like that are proof that facilitating commercial finance deals is still red hot.

That’s me in that photo above, wearing that shirt back in 2009 when the industry was not even a fraction of the size it is today. Hat tip to the friend who found this. I used to joke about putting on your funding pants but perhaps in 2018 it’s time to put on a selling shirt too.

In 2018, will you sell more and make more money?

If you want to operate at the top of your game, I highly suggest you register to attend Broker Fair 2018. With 24 major sponsors already signed on, Broker Fair will be the place to learn, get inspired, and connect with the right people to do even more business.

May the next big commission check belong to you.

Letter From The Editor

December 23, 2017 It was a year to remember, our sources declare

It was a year to remember, our sources declare

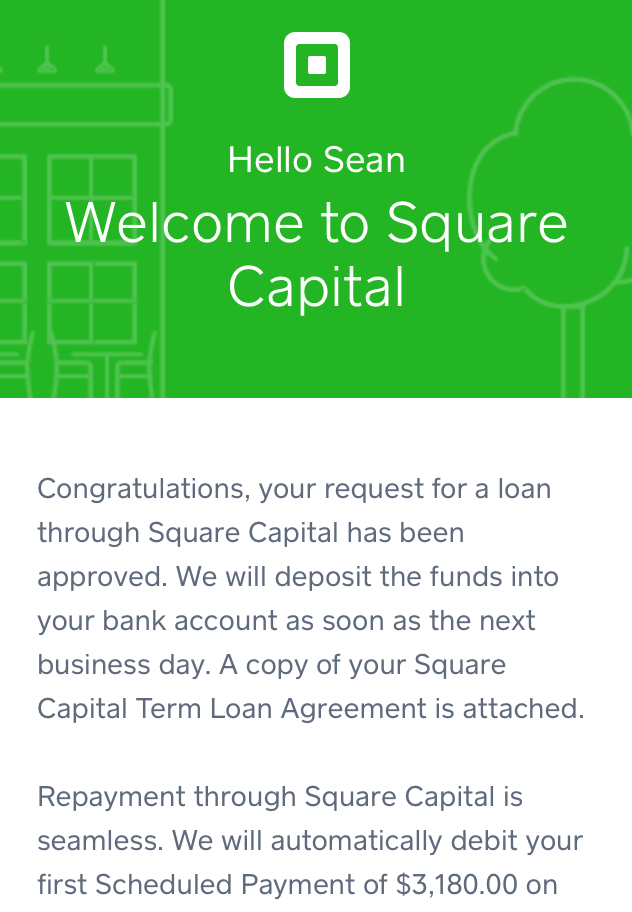

‘Twas the Jan/Feb issue I wrote about my loan from Square

Through March into April salespeople closed deals via text

Through March into April salespeople closed deals via text

As banks looked to fintech as their plan for what’s next

We went to Texas a nexus for finance and lending

We went to Texas a nexus for finance and lending

It was May, maybe June when Bizfi’s final days were pending

Merchants talked, banks adjusted, it was a summer of learnings

Merchants talked, banks adjusted, it was a summer of learnings

For the pressure was on to produce solid quarterly earnings

September, October, liens and judgements were removed

September, October, liens and judgements were removed

But the world hardly noticed and deals still got approved

Winter coats and furry hats meant the year would end soon

Winter coats and furry hats meant the year would end soon

But by golly 10k, no 19k! Bitcoin went straight to the moon!

And so boys and girls the story of ‘17 has been told

And so boys and girls the story of ‘17 has been told

What a time for finance, for money, and a world to behold

See you in ‘18, in ‘19, and the roaring twenties my friend

We’ll be right there, whether you deal in receivables or lend

– Sean Murray

MCA’s Top Social Media Voice

December 18, 2017 LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

By most standards she’s a newbie to fintech, having joined her previous employer Pearl Capital only two years ago. But that hasn’t prevented her from making her social media presence known. And while she reserves Facebook for her personal life, if you know Villano then you wouldn’t be surprised at her success on LinkedIn, as she seems to have a knack for social media.

“I felt like I needed a very strong presence in this industry to get anywhere,” Villano told deBanked. “It’s funny, I think a lot of people associate sales with a type A personality and being pushy. I’m not an aggressive, pit-bull woman. You don’t have to be that type of woman to get ahead. I thought about how am I going to show this to the industry? Social media was my answer. My Facebook and LinkedIn attract a lot of views.”

Indeed, it was because of her Facebook profile that Villano was featured by a famous painting by David Uhl. The painting, dubbed Steampunk Seduction, is the first in Uhl’s Steampunk series. “I got that through Facebook,” Villano explained. “Someone saw my profile on Facebook, reached out and said, ‘you should contact the artist.’ I told them they were crazy. They insisted, and he chose me. It’s been a blessing.”

Meanwhile, her LinkedIn posts designed for MCA ISOs have similarly caught on like wildfire, and she only “amped up” her activity on the site in July. Villano has been posting on LinkedIn once per week, and the proof is in the pudding. “Since then, in September, October, and November, we broke funding records every month. It works,” said Villano of her previous employer Pearl Capital.

Underpinning that deal flow has been a flow of new relationships she’s forming, evidenced by more than 500 ISOs having contacted Villano on LinkedIn via her previous employer’s Salesforce network.

“That was from posting one time per month and just educating; not posting pictures of me on a beach sipping a Pina Colada,” said Villano. Instead, she was educating them about Pearl’s funding options, the types of deals they wanted, their bonus structure, etc. “So, it’s very basic information. I was just letting them know what they can expect from Pearl, what kind of fundings we were doing, just being a constant reminder,” she added.

While Villano is no longer employed by Pearl Capital, her posts from her tenure there have had a lasting impact. “[Last month] I put up a post announcing that I was leaving Pearl Capital,” Villano said. “The post generated more than 35,000 views.” Meanwhile, since she’s been posting, she’s seen the number of LinkedIn connections skyrocket.

Villano is continuing her social media push at her new employer, Kalamata Advisors.

“Kalamata has a partnership-culture mentality. It’s an amazing opportunity to be elected a partner, like a partner at Goldman Sachs or McKinsey, here after a couple of years. Then you have a real stake in the company and work at a firm where everyone wants to pitch in,” she explained. “Second is their great reputation. The partners put their mission and values first. They’ve grown so fast; but they’ve grown with the purpose to genuinely help people. And lastly, they’re very respected in the industry. Everyone here is very responsive, honest and professional.”

And while she’s no longer employed by Pearl Capital, she has nothing but respect for her former employer as well. The feeling is mutual, evidenced by a going away party that they threw for her on her way to Kalamata.

Gender Gap

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

The other has to do with the fact that MCA is a male-dominated industry. “Women are more conversationalists through texting or social media. I find women are more intimate with it on a professional level. I have to say that I have the most active social media in our industry,” said Villano, who again only joined fintech two years ago. She’s inspired by the many women who are behind the scenes at ISO shops, many of whom she explained work as processors.

We asked Villano about whether sharing her trade secrets with competitors in the industry made her uncomfortable. “Not at all. I’m not made like that,” she said. “And Kalamata believes trust is the importance of every brand. With transparency, there is trust. Everyone is authentic and unique. Everyone should have the opportunity to share his/her own self in any industry.”

deBanked Connect: Miami — SOLD OUT

December 12, 2017deBanked’s cocktail networking event on January 25th in South Beach is now SOLD OUT!

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

With 20 sponsors already signed on, Broker Fair is sizing up to be the biggest event in the MCA and small business lending industry of the entire year! During this exclusive full-day conference, brokers, lenders, funders and service providers alike can expect education, inspiration and opportunities to connect and grow their business. You can view our preliminary agenda here.

DON’T GET LEFT OUT. REGISTER FOR BROKER FAIR 2018 TODAY!. Got questions? E-mail: info@brokerfair.org

Closing Loans and MCAs — From the Bedroom to the Office

December 8, 2017 The merchant cash advance industry has gone mainstream so quickly that it has become more difficult to identify potential customers.

The merchant cash advance industry has gone mainstream so quickly that it has become more difficult to identify potential customers.

Market saturation and industry consolidation have caused the cost of sales leads to increase sharply. Yet a New York business loan broker is finding success by applying lead generation and online marketing strategies to merchant cash advance, or MCA, while expanding the number of services he offers prospects. Funding is just the foot in the door.

Philip Smith, founder and CEO of PJP Marketing Inc., told deBanked the MCA industry’s acceptance has made it more difficult for sales lead generators to produce profits. But expanding the number of services that independent sales organizations (ISOs) offer can offset the contraction. Smith’s life as a stay-at-home-dad, was recently featured in Innovate Long Island, a regional newspaper.

An ISO can’t just be a broker anymore. It needs to change, identify new revenue streams to excel. In doing so, a lead generator transforms itself into a business consultant that prospective customers turn to for additional services they often didn’t even know existed, Smith said.

For example, business loans and MCA is Smith’s largest business generator. But his most popular add-on services with such sales leads are credit repair and credit monitoring.

“The market is relatively easy,” Smith said. “The hard part is monetizing. The ISOs are going out of business because they refuse to monetize the other, non-cash advance leads.”

Smith, armed with a degree in business/e-business from the University of Phoenix, is also an advocate for entrepreneurs who want to work from home. It’s a viable model for lead generators because low overhead costs provide entrepreneurs an opportunity to capitalize on aggressive business strategies.

As such, Smith markets his pajama-centric business model with IWorkInMyJams.com. But he acknowledges that working from home presents its own challenges. Entrepreneurs need to be extra focused and tough to distract. No watching Dr. Phil during work hours.

Since they don’t work with more experienced managers, work-from-home entrepreneurs also need to seek their own sources of business advice and strategies. They deal with the reality that some lenders may deem them too small to do business. “Not everyone will work with you,” he said.

Working from home also requires a entrepreneur to set office hour limits and parameters to prevent burnout, Smith said.

“Do you know when to turn it off?” he asked. “That’s my problem. I’m up until 1 o’clock in the morning because I can.”

Smith now brokers sales leads in several verticals such as credit repair, tax relief, mortgage and solar energy. He claims revenue of $1.6 million last year and plans to reach $2 million this year.

When he was just 23, Smith launched his first company, We Link You Internet Services, a business that evolved into a web hosting concern.

He later worked for New York-based Canrock Ventures to launch a search-engine optimization platform called SEOPledge that was acquired in 2013. The following year, he founded what is now called PJP Marketing to broker leads amid the rapidly rising MCA space using the digital marketing skills he’d learned from the previous positions.

In October, deBanked reported that several factors have contributed to several changes in the MCA industry, including consolidation, making it more difficult for alternative-funding business lead generators.

ISOs and brokers have gotten pickier about the types of leads they’ll accept as MCA evolves from a niche business to one that’s more commonplace. Also, a stricter application of the Telephone Consumer Protection Act (TCPA) has chilled soliciting and hamstrung the ability to connect with business owners who are prospective clients.

Last year’s LendingClub Corp. scandal ousted several senior managers, including the company’s then-CEO. Last summer, Bizfi laid off workers and sold the servicing rights to its $250 million loan portfolio to rival Credibly.

The result has been a consolidation of the alternative funding business.

“There are still roughly 75,000 business owners every week who meet the criteria for an [MCA],” California-based Lenders Marketing partner Justin Benton told deBanked. “Now instead of there being 5,000 options in the space, there are 2,000, so those 2,000 are gobbling it all up.”

David Ross, a 12-year veteran of the MCA industry and owner of Pro Leads NYC, said MCAs higher profile has been a game changer for lead generators.

David Ross, a 12-year veteran of the MCA industry and owner of Pro Leads NYC, said MCAs higher profile has been a game changer for lead generators.

“MCA is beyond saturation,” he said. “All of the merchants know about it and understand it. Now, [funders] want exclusive leads.”

Working from home is a possible option for ISOs that are wizards at online marketing. But it’s less attractive for the conventional lead generator who relies on backing from a marketing team, Ross said.

“Realistically, if you’re a broker and want to make money you have to be on someone’s floor,” he said. “You need marketing.”

Last year, a Bryant Park Capital report estimated the MCA market to be worth about $12.8 billion. It’s projected to top $15 billion this year. Smith expects the continued strong demand for MCAs regardless of all the industry consolidation and costlier lead generation.

“I think they will always be fine because they can live through the storm,” he said. “It’s now a mainstream service so more people know about it.”

Smith told Donna Drake during an appearance on the Live It Up television program that going it alone as entrepreneur takes a “do-not-quit attitude” that has served him well so far.

“Any business is pretty much a numbers game,” he said. “I live and breathe it every single day.”

Originations Since Inception

December 8, 2017After several company announcements recently, we’ve compiled a milestone chart to plot where they rank. Originations may indicate business loans or MCAs funded on balance sheet, brokered, or placed through a marketplace. These rankings are a work in progress. This chart may not include companies for which public data is not available. If you’d like your figures to be listed here, e-mail sean@debanked.com.

| Company | Origination Volume Since Inception | Year Founded |

| OnDeck | $8 Billion | 2007 |

| Kabbage | $4 Billion | 2009 |

| Yellowstone Capital | $2 Billion | 2009 |

| BFS Capital | $1.7 Billion | 2002 |

| Funding Circle | $1 Billion (US only) | 2010 |

| IOU Financial | $500 Million | |

| Lending Club | $500 Million (SMB loans only) | 2006 |

| SmartBiz Loans | > $500 Million (SBA loans) | 2009 |

| Lendio | > $500 Milllion | |

| Forward Financing | $275 Million | 2012 |

| Blue Bridge Financial | $200 Million | 2009 |