Has PayPal Eclipsed OnDeck in Small Business Loans?

April 26, 2019

It’s been said that Kabbage is on pace to surpass OnDeck in small business loan originations, but PayPal has already done it.

When PayPal announced a working capital program in the Fall of 2013, few were predicting that the initiative would propel them to the top of the small business lending charts. Just two years later, however, the payment processing giant had already loaned more than $1 billion to small businesses.

Today, that number is over $10 billion, according to a comment made by PayPal CEO Dan Schulman on the company’s Q1 earnings call.

That figure would suggest that they had loaned approximately $9 billion from Fall 2015 to the end of Q1 2019. OnDeck, by comparison, loaned $7.5 billion since Fall 2015 through Q4 2018. Several other data sources, including previous statements from PayPal that they had surpassed more than a billion dollars in quarterly small business funding in 2018 (already more than OnDeck), indicate that PayPal has become #1 on the deBanked small business funding leaderboard.

PayPal’s growth was helped in part by its acquisition of Swift Capital in 2017.

Two of the top four are payment processors:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| PayPal | $4,000,000,000* | $750,000,000* | ||||

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate

Merchant Cash Advances Surpass Leasing As Goto Financing Option for Small Businesses

April 16, 2019

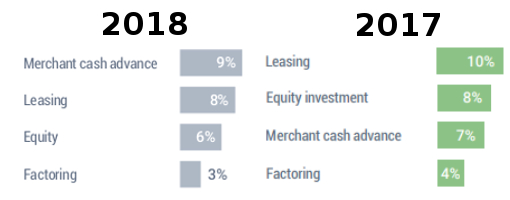

More small business applied for merchant cash advances in 2018 than they did leasing, factoring, or equity investments. That’s according to a recent Federal Reserve study of small businesses with less than 500 employees.

Nine percent of applicants applied for merchant cash advances in 2018 while only 3% applied for factoring. Leasing dropped year-over-year from 10% in 2017 to 8% in 2018.

On average, merchant cash advances were approved 85% of the time compared to business lines of credit (73%), business loans (67%), and SBA loans (52%). Six percent of all small businesses surveyed said they used merchant cash advances on a regular basis, versus 9% for leasing and 3% for factoring.

Unsurprisingly, small businesses overwhelmingly still sought loans or lines of credit. Of those surveyed that applied for any type of financing in 2018, 85% applied for a loan or line of credit and 28% applied for a credit card.

You can download the Federal Reserve’s complete report here.

Learn From Josh Feinberg and Will Murphy in Person at Broker Fair

April 16, 2019You’ve seen them on social media. Now you can see them in person. Josh Feinberg and Will Murphy of Everlasting Capital will be doing a joint presentation on how to scale your broker shop at Broker Fair on May 6th at The Roosevelt Hotel in New York City.

Limited tickets are still available. Register now at Brokerfair.org

The Everlasting Capital co-founders will be presenting at 3:15pm on May 6th in the Promenade Suite. To view the full agenda, CLICK HERE.

-

Brokers

Access to the conference as a broker - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop of The Roosevelt Hotel

- Your conference badge will identify you as a broker

-

Funders/Lenders

Access to the conference as a capital provider - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop of The Roosevelt

- Your conference badge will identify you as a direct capital provider

-

General Admission

Access to the conference as a third party - Full access to the May 6th conference

- Complimentary access to the post-event cocktails on the rooftop at The Roosevelt

What Am I?

Broker

- You are employed by a non-bank business financing Broker/ISO — OR — You are an independent sales agent

- You are NOT employed by a direct lender or direct funder

- Broker Fair reserves the right to verify your selection.

- Your conference badge will identify you as a broker

Funder/Lender

- You are employed by a direct capital provider whether it’s loans, merchant cash advances, factoring, or other products

- Your conference badge will identify you as a direct capital provider

General Admission

- You are not employed by a broker/ISO or direct capital provider

- Your conference badge will not display a specific business model designation

- You will have the same conference access as a funder/lender does

Give Up Equity In Your Business?! Try Alternative Funding Instead

April 4, 2019One thing you can’t get back is your company.

Michele Romanow, a judge on Dragon’s Den, Canada’s version of Shark Tank, realized from the show that a lot of companies should not be pursuing venture capital at all. She recalled a company that was willing to give an investor 25% of their company in exchange for $100,000.

“Why use the most expensive form of capital, which is equity?”

It led her to co-found Clearbanc, a Toronto-based small business funding provider that does their own spin on merchant cash advances. The amounts range from $10,000 to $10 million and their caution against equity capital-raising is explicit.

“No equity, no fundraising, no dilution, no warrants/no covenants, no board seats, and no bullshit” is a pitch prominently displayed on the company’s homepage.

Romanow speaks from experience. In 2014, GroupOn acquired a company she co-founded and she joined Dragon’s Den shortly after at just 29 years old. She’s a serial entrepreneur with a net worth reported to be over $100 million.

VC money may be harder to obtain, regardless, even if an entrepreneur is willing to make the sacrifice. Funding from VCs tends to be unequally distributed geographically. She cited a May 2018 report by PwC and CBInsights that showed that more than half of all VC dollars invested in small businesses and startups during the first quarter of 2018 went to companies in California. And 80% of VC money in that quarter funded companies either in California, New York, Massachusetts or Texas, a trend bucked by alternatives provided by companies like Clearbanc whose backgrounds are much more diverse.

The message has worked. Clearbanc recently announced that it plans to invest $1 billion in 2,000 e-commerce companies within the next 12 months and the company has raised more than $120 million to-date. It probably helps that Romanow is a TV business celebrity. She is now on her fifth season of Dragon’s Den. And as for those pesky VCs? They tend to be big referral partners for Clearbanc. Go figure.

Undercover in the Underwriting Room

March 22, 2019 Think of the stereotype of a high energy, high testosterone sales floor of men practically shouting on the phone. And then scale it down to a level of about 2 out of 10. That was the environment I stepped into on a recent visit to a room of small business finance underwriters. They let me shadow one for a day so long as I didn’t reveal who they were.

Think of the stereotype of a high energy, high testosterone sales floor of men practically shouting on the phone. And then scale it down to a level of about 2 out of 10. That was the environment I stepped into on a recent visit to a room of small business finance underwriters. They let me shadow one for a day so long as I didn’t reveal who they were.

In the glass room where almost 10 underwriters sat, some spoke on the phone, but the conversations were measured. No shouting. No arguing. Sometimes there was near silence. More than anything, there was an air of focus. After all, when you’re evaluating dozens of documents, just a single oversight can cost the company a lot of money.

“You don’t want to be the guy who loses the company money because you didn’t see a red flag,” said the underwriter.

He asked me to sit beside his desk and watch the funding decisions he was making based on what he saw in the file. He surely didn’t take the merchant’s monthly sales numbers at face value. For instance, in one file, in addition to subtracting a $2,000 transfer from the owner’s personal account into their business account, he also noticed a $4.18 refund from Walmart that was being counted as sales.

“That’s not sales,” he said, and he subtracted $4.18 from the monthly sales number. In one instance, $103,000 in reported sales became $75,000, according to the underwriter.

While you could certainly feel the concentration in the room, it wasn’t quite a library either.

While you could certainly feel the concentration in the room, it wasn’t quite a library either.

“His FICO sucks,” one of the underwriters said to the others. “His FICO went down and he’s stacked. No.”

When an underwriter is uncertain about a decision, he’ll ask for everyone’s two cents. He said they call these impromptu discussions the “underwriters’ den.”

All the deals we looked at got declined, but I’m told that one underwriter can fund as many as five deals in a day, and then go a few days without funding any.

While the underwriting criteria is taken seriously, sometimes you can be a little more aggressive and push the boundaries a bit if it’s a deal you really like. That takes considerable thought and reasoning. But when the answer is going to be no, it can come at light speed. A few of them happened in under three minutes while I was there. And that was with him slowing down to narrate for me what he was thinking.

“I give a look at [most of] the documents in the file first,” he said, “so that if there’s an obvious red flag, I don’t want to spend time on it.”

In his cursory glance, he’ll look at the business owner’s FICO score, years in business, if the company has other financing, and if so, how they’ve been able to handle those payments. He’ll also count the number of negative days (when the company owes money and has none) and note how consistently the company makes sales.

“Consistency gives me comfort,” he said. “I can give them a stronger offer when they show consistent sales.”

Of course, funding a file takes a good bit longer because you have to continue to vet the business and the business owner, almost as if you suspect there’s something wrong. Has the owner ever been convicted of fraud? Have they owned any other businesses? Did the owner ever default on a loan? It can seem hard for small businesses to pass all these background checks. But the funder has to protect itself and the underwriter’s job is to do just that.

“We’re in the business of giving out money, but within limits.”

LinkedIn Posts Are Turning Into Deals & Dollars

March 14, 2019

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

Villano is among the growing crowd of industry insiders attempting to convert social media posts into measurable business. With more than 600 million users on LinkedIn, there is no question about the potential to reach clients. The prevailing wisdom is that you need to be on social media and sharing, but share what exactly?

New Hampshire-based Everlasting Capital is building a window into the business lives of co-founders Josh Feinberg and Will Murphy. One of their recent social media posts focused on their search for a new office lease, while another was a video stream of Feinberg making a real live cold call. The rewards span the gamut, from merchants seeking funding to offers to speak professionally in front of large audiences. And it’s not just about them. “We have worked with our employees to get confident on camera which is making them a lot more comfortable on the phone,” Feinberg said.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

For Jennie Villano, it’s not always a sales pitch. She has posted about being a single mom and about how to keep an upbeat attitude. “Your co-workers, your friends. Are they positive, or are they always complaining?” Villano asks in the video. “Try to surround yourself with positive people who see the best in everything.” She’ll typically extend the offer to do business in the videos that she makes and shares, but not all of them. She shares 2-3 videos a week and her posts typically receive thousands of views.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Though other social networks are being used in full force by many industry players, LinkedIn is definitely a platform to consider. “We’ve gotten tremendous value from posting to LinkedIn,” Smart Business Funding’s Collin said.

The Art of Moving The Deal – When it becomes too high risk for you

February 27, 2019 OakNorth, a small and medium sized business lender and online bank, has mastered a strategy to avoid merchants from defaulting 100% of the time, according to a story published in Quartz. The strategy: tell the merchants at risk of defaulting to refinance their loans at a competitor.

OakNorth, a small and medium sized business lender and online bank, has mastered a strategy to avoid merchants from defaulting 100% of the time, according to a story published in Quartz. The strategy: tell the merchants at risk of defaulting to refinance their loans at a competitor.

“We’ve said [to merchants], ‘Go renegotiate with another bank and refinance,’” OakNorth co-founder Joel Perlman said at the Finovate Europe conference in London on February 14, according to the Quartz story. “And they’ve gone and refinanced and then a few months later they’ve gone into default.”

Perlman’s phrasing may sound a little harsh, but the practice of moving at-risk merchants to another funder is really not uncommon. In fact, it seems like a fairly common and well-understood concept.

CEO of Accord Business Funding Adam Beebe said that brokers will contact Accord when their merchant is up for renewal. And if Accord knows it can’t continue to fund the merchant – either because it has missed payments or because it has become overburdened with other debt – the broker will shop that undesirable merchant elsewhere.

The merchant goes to a new funder and Accord is pleased to be rid of the merchant and not have it default on Accord’s balance sheet. Beebe notes, however, that the new funder is made aware of the merchant’s financial situation and is able to handle the higher risk. Transparency, he says, is important, particularly in a scenario like this.

Similarly, Heather Francis, CEO of Elevate Funding, said that she is more than happy for an ISO to move a stacking and defaulting merchant away from Elevate, as long as Elevate gets paid. Elevate only funds first position and Francis said they make it very clear to merchants that stacking (taking on additional funding from other sources before satisfying an existing contract) is not allowed.

“If a merchant is stacking, that’s not someone we want to work with,” Francis said. “And if the [new] funder understands the high risk, then is fine.”

As long as nothing is being hidden from the new funder, then it seems this practice is just an element of how funding works.

From the broker side, Rob Addison, Managing Member of Sentra Funding, an ISO, said that when a funder knows it will not be renewing one of his merchants, they will ask him to take the merchant away.

Addison said that some funders are so eager to get rid of defaulting merchants that they will offer deals like reducing the merchant’s balance just to get the merchant away from them.

It may not sound nice to jettison a defaulting merchant, but if a funder can avoid a merchant defaulting on its dime, then in many cases, it will.

“We try to move a financially distressed merchant from from, say, an MCA to a longer term loan,” Addison said. “If they haven’t been stacked, they have options. If they have, it’s harder. But if they have something, like commercial property or equipment, there’s usually a [a funder] willing to step in.”

True Story: I Cold Called a Merchant

February 25, 2019 While visiting the office of Excel Capital in Manhattan on a reporting assignment, I saw a few open desks. They weren’t exactly empty, just available. There were phones, headsets, and computers all set up, just waiting for a salesperson to sit down and plug in. I pictured the salespeople I’ve previously profiled, smiling & dialing, as they say, contacting small businesses and delivering their best pitch. And for a moment, I imagined it was myself in one of those chairs. A funny thought perhaps if you’ve gotten to know me, but it’s not an uncommon curiosity for a reporter to try and channel a source’s mindset.

While visiting the office of Excel Capital in Manhattan on a reporting assignment, I saw a few open desks. They weren’t exactly empty, just available. There were phones, headsets, and computers all set up, just waiting for a salesperson to sit down and plug in. I pictured the salespeople I’ve previously profiled, smiling & dialing, as they say, contacting small businesses and delivering their best pitch. And for a moment, I imagined it was myself in one of those chairs. A funny thought perhaps if you’ve gotten to know me, but it’s not an uncommon curiosity for a reporter to try and channel a source’s mindset.

Excel CEO Chad Otar obviously caught that flashing glimmer in my eyes, because the next thing I knew he invited me to sit down and make a call myself, a completely cold one… to a merchant.

My instinct was to just observe, but the journalist in me unconsciously accepted the invitation. Before I knew what I was getting myself into, I was sitting at Chad’s desk in the CEO chair, reviewing sales scripts that were handed to me. I read two of them and realized that they were fairly different in tone. The first said something like “I’m calling from the back office and it appears that you once had an interest in funding. I’m checking to see if you still do.” The other one was far more direct. It explained a special offer to prospective clients and it finished with a question, “What are you seeking capital for?”

Chad recommended the more direct route, the one I liked more as well. I didn’t like the idea of being in a “back office.” It sounds so distant, so non-urgent. And from my understanding, a sales call should sound urgent, without being too aggressive either. I knew I had to strike the right balance. I looked at the bolder script and practiced reading it a few times out loud. The script started with “Hello, my name is [John Doe.]” But I thought, “I think ‘hello’ is too formal. ‘Hi’ works better for me.” And I also thought that using just my first name might be more familiar and less intimidating than my full name. So I decided to just use my first name. Note that when introducing myself on the phone at deBanked, I always use my full name because I aim to be very intimidating. I’m totally kidding!

Back to my first EVER cold call. After rehearsing the script a few times and letting everyone around me know that this was my first cold call and a really big deal for me, I picked up the phone and I started to dial. “Hello, this is Kathy” a voice beamed from the other end of the phone. I said “Hi Kathy” and I started to read the script. Then I stopped. For a moment, it was just silent. She didn’t hang up! YES! She also didn’t curse at me or ask that I not call her back again. She didn’t even politely excuse herself. Instead, she asked a few clarifying questions.

“Where are you calling from?”

I could answer that! Except that I made a slight mistake. I called the company Excel Credit, instead of the correct Excel Capital. A subtle enough error, I thought, so I chose not to acknowledge it. And since I’ve been writing about companies like Excel Capital for a little while now, I felt comfortable enough to provide a brief sentence to this woman about what Excel Capital does. “We offer funding to small businesses throughout the US,” I said. I thought this would be a good opportunity to correct my earlier error, so I slipped in “we’re also known as Excel Capital.” That could have sounded shady. But I don’t think she heard it that way.

“How did you find us?” she asked.

“Wow,” I thought. “This is turning into a real conversation!” I didn’t know how her info had been obtained, so I just said “I get lists from my boss and I don’t know exactly how this list was obtained.”

Chad said something to me about previous funding, so I then added: “We got this list of businesses that have previously been funded.”

At this point, I thought to myself “Why don’t you ask a question now?” So I went down to the next question on the script sheet and I asked in a “just happen to be curious” way: “Is there a certain amount that you need?”

“That would be the owner who would know about that,” Kathy said.

Uh-oh. I wasn’t even on the phone with the owner. I wasn’t speaking to the decision maker. But for my first cold call ever, I felt pretty good about it. I gave Kathy Excel’s number and yes, my full name, and I feel like I helped warm up this potential client. They could call back and say that they (Me!) spoke with Kathy. My first cold call wasn’t so bad, and honestly, I’m kind of ready to make 200 more! Just kidding.