Maryland MCA Prohibition Bill Morphs Into MCA APR Limit, Broker Licensing, Double Dipping, Uniform Disclosure, and Go to Jail Bill

February 18, 2021Update: A Recording of the Hearing is Here

Plans to enact “prohibition” in Maryland on merchant cash advance transactions abruptly came to a halt last year, but the legislature there has brought the issue back front and center in 2021, designing a system of prohibition while dropping the actual word from the name.

Plans to enact “prohibition” in Maryland on merchant cash advance transactions abruptly came to a halt last year, but the legislature there has brought the issue back front and center in 2021, designing a system of prohibition while dropping the actual word from the name.

No MCA transacted in the state would be permitted to have an estimated APR that exceeds 24%, for example. The penalty for violating such a statute can be imprisonment for up to 3 years.

Newly introduced House Bill 664 (SB0532) would “prohibit a person from engaging in the business of making or soliciting a sales-based financing transaction unless the person is licensed by the Commissioner of Financial Regulation” and would require that an applicant “for a license having $20,000 in available liquid assets and to have demonstrated a sufficient level of responsibility to command public confidence and warrant faith in the honest operation of the business.”

The 26-page bill includes a laundry list of requirements and restrictions like specific disclosures, how to calculate a forward-looking estimated APR on an MCA, and a limitation of 24% on that APR.

The bill draws heavily from the recently passed law in New York, going so far as to copy and paste the section requiring MCA funders to disclose if there is literally any “double dipping” in the contract.

The Commissioner of Financial Regulation would retain sole authority to judge compliance with the law.

A House committee hearing on the bill was conducted yesterday and a subsequent one in the Senate is scheduled for February 23rd at 1pm.

You can read the full version of the Maryland House Bill here.

Shopify Originated $226.9M in MCAs and Business Loans in Q4, Close to $800M For the Year

February 17, 2021 Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

That is a posted increase of 96% over the same quarter in 2019 but was down 10% from q3. The full year 2020 originations of $794M were nearly double the $430M in 2019.

“Products like Shopify Capital are increasingly sought out by entrepreneurs and small businesses that face unnecessary barriers to access from traditional banks,” Shopify President Harley Finkelstein said in the quarterly earnings call. “Merchant empathy runs deep at Shopify. When traditional businesses were turned away, for the perceived high risk, we financed a record number of merchants when they needed it most.”

“We also introduced Shopify Capital to Canada and to the U.K. in 2020,” Finkelstein said. “To expand where we could help merchants.”

Shopify Capital still lagged behind rival OnDeck in origination volume, who reported a little over $1B in originations for the year.

Broker in Early Twenties Builds MCA Business in Less Than Three Years

February 10, 2021 Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

The Staten Island native said he first started at a Long Island City shop and quickly made some early deals, eventually leaving to start his own firm, FunderHunt, and recently opened an office in Miami.

But do the YouTube videos help him make deals? Of course they do, Karimov says, and he not only gets deals through his video platform but he also get questions from other MCA brokers who reach out for help.

“Of course, we get people all the time calling in, people that have questions, people in the industry need help with their merchants,” Karimov says. “I started around 2018, and there was no info on YouTube about business funding, a huge void online. I stepped up and thought I could be the one to supply info.”

Nearly three years later, Karimov has built an expanding business while helping others through the struggles of being a broker and CEO in the MCA world. In the last year alone, the pandemic caused applications to explode, Karimov says.

“It’s been better than ever; I’ve never seen so many applications in March and April; they were just soaring,” Karimov says. “And then I’ve never seen so many applications get denied because of the industry at the time everything was shutting down.”

It was a time to capitalize if your shop was strong enough to survive what Karimov called the “dark ages” for MCA. If you survived, you get to reap the reward of a capital-deprived market, he says.

“The whole crisis took out so many funders that were just not good, they probably were supposed to go out of business a long time ago, but this accelerated it,” Karimov says. “It took out all the bad funders and replaced them with people that are solid, fast, and have everyone’s best interest at heart, from the merchant to whoever the ISO is.”

According to Karimov, 2020 solidified who is a real player in the game. Launching a new office himself, Davron says he enjoys sunny days in Miami while it is twenty degrees in-between blizzards in New York. Though snow wasn’t the reason he moved, but instead the funding environment.

“Everyone has been warm and welcoming [in Miami], the government knows what this is, and that’s what we do. We try to educate them: not a lot of people know here about this; it’s like it’s a secret,” Karimov says. “If you go to New York, it’s like everybody knows, there are so many shops there. But here, it’s kind of rare to see someone that knows what a cash advance is.”

Compared to New York’s increasingly restrictive funding ecosystem, the Florida space is open to growth. That’s exactly the environment Karimov hopes to profit from, expanding his business in any way that will be geared toward helping businesses.

“I’m not a huge fan of diversification,” Karimov says. “I like doing one thing. But we opened up an office in Miami; we’re bringing experienced people in and trying to fund deals as fast as possible. We’re maybe looking to develop into offering a debit card, whatever is in the business’s best interest.”

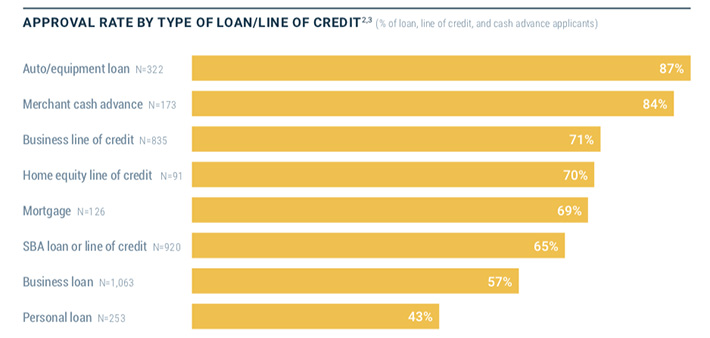

Merchant Cash Advance Approval Rate Was 84% in 2020, Federal Reserve Finds

February 3, 2021Eighty-four percent of applicants that applied for a merchant cash advance in 2020 were approved, according to the latest study published by the Federal Reserve. However, that figure includes the pre-March 2020 covid era.

When MCAs and online loans were blended, for example, the approval rate shrank from 81% pre-March 1st to 70% after March 1st.

Eight percent of all small businesses sought a merchant cash advance in 2020, down slightly from 9% in 2019. Leasing dropped from 9% to 7% and factoring dropped from 4% to 3%. Pursuit of credit cards even dropped, down from 29% to 21%.

There were some downsides for the online lending industry reported.

Only 9% of PPP applicants used an online lender.

Online lenders had the lowest satisfaction rate (43%) for small business credit needs. Credit unions scored the highest (87%).

Net satisfaction with online lenders dropped to its lowest level since 2016.

Small businesses satisfaction with big banks actually grew from 2019 to 2020.

Small businesses were less likely to apply for a business loan or MCA from an online lender in 2020 and more likely to apply for them at a bank in 2020 than they were in 2019.

Eighty-two percent of businesses applied for a PPP loan. Forty-seven percent applied for an EIDL loan.

Banks, perhaps counterintuitively, were the big winners in 2020. That trend could increase as banks and online lenders become the same thing.

Double Dipped: What’s Next For New York’s Small Business ‘Truth in Lending’ Act

January 11, 2021 Last year, when the Small Business ‘Truth in the Lending’ bill came through the New York State Senate Banking Committee, Senator George M. Borrello said he and other members went to work. Their job: to write a version everyone would like, which fell apart when the bill passed in July and it was signed into law just before Christmas.

Last year, when the Small Business ‘Truth in the Lending’ bill came through the New York State Senate Banking Committee, Senator George M. Borrello said he and other members went to work. Their job: to write a version everyone would like, which fell apart when the bill passed in July and it was signed into law just before Christmas.

“I’m a small business owner myself, but I also come from local government, and in local government, the committee is where the work gets done,” Borrello said. “We had the opportunity to fix this in committee. By the time it got to the floor, the governor basically reversed all the things I presented that were flaws, and he signed it.”

That’s the story of how S5470B came to be in Albany. Instead of ironing out the kinks in committee, Borrello said he watched as the bill with all its problems passed over the summer. There was a process to clean it up afterwards to make it suitable for Governor Andrew Cuomo’s signature, since it’s said that even he himself had expressed reservations about the language. But then he signed the original version and all the edits were discarded.

Politics are suspected to have played a role in that.

Politics are suspected to have played a role in that.

“When the governor finds something is flawed, he usually vetoes and sends it back,” Borrello said. “It concerns me that there is an underlying political angle that has nothing to do with the Truth in Lending.”

Steve Denis, the executive director of the Small Business Finance Association, said that he doesn’t think that the signed bill that is up on the state senate website will be the final version.

“It is so poorly drafted that even companies that support the bill have liability and will be the first to get sued,” Denis said. “The SBFA will be a lot more aggressive; the legislature has a lot to work on in the next session. It has been a wake-up call, unifying the industry. We will be more aggressive to create a more favorable version.”

Denis has attested to the harm the bill will do to the SMB finance industry in New York, costing billions of dollars in fines and litigation. He pointed out that major companies like PayPal have fought against the bill, and the proponents “recognized it was not a good bill, but passed it to fix it.”

Borrello said that it is common in Albany to encounter legislation written by lawmakers who don’t understand small business owners who deal with regulation every day. Borrello and his wife worked in the hospitality business for years before going into public service. Borello said he feels business owners’ pain during the pandemic, especially in the restaurant and hotel industry.

He said the end result of this new bill when it comes into effect this July: funding and lending companies will stop providing services in New York State, directly harming the small businesses the bill claims to help.

“One of my frustrations, being on the banking committee, is that we do things that ultimately make it more difficult for people to access credit and financing in New York State,” Borrello said. “You’re talking about small businesses that are already hurting, having financial difficulties accessing lines of credit. This disclosure law passing during this pandemic is one more nail in the coffin for small business.”

The Legislature, the Governor, and the Department of Financial Services (DFS) all reportedly had issues with the bill: yet it passed. Borrello said a problem with “nonsense lawmaking” comes from competition with other states. New York compares itself with California to “prove we’re the most progressive.” Borrello also pointed out that California passed its version of a lending disclosure bill more than two years ago, and their version of the DFS still cannot find a way to calculate an APR metric for factoring or MCA.

The Legislature, the Governor, and the Department of Financial Services (DFS) all reportedly had issues with the bill: yet it passed. Borrello said a problem with “nonsense lawmaking” comes from competition with other states. New York compares itself with California to “prove we’re the most progressive.” Borrello also pointed out that California passed its version of a lending disclosure bill more than two years ago, and their version of the DFS still cannot find a way to calculate an APR metric for factoring or MCA.

As the bill was argued on the legislative floor, Borrello brought up the controversial “double-dipping” term that had been inserted in the language. Borrello came to the same conclusion as Denis, that there is no double-dipping term: It was just conjured up for the bill to sound scary, negative, and damaging.

“Other than talking about potato chips, I’m not sure what you’re talking about,” Borrello said. “When you haven’t defined it, in the legislature, it comes down to a political talking point and dog whistle. You enshrine a rather vague piece of jargon in the legislation, and it shows how deeply flawed it is.”

Borrello now plans to work with the Governor, DFS, and legislature to amend and change the bill. He is also fighting for a Republican banking overhaul to provide further credit access to small businesses.

“The next step now is to go back and see what needs to be fixed,” Borrello said. “Hopefully, my role now as the ranking member of the banking committee, we can have a common-sense conversation about how to actually fix it.”

Greenbox Capital Comments on Landmark Florida Legal Victory

January 7, 2021 Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

Greenbox Capital was the victor of a major lawsuit argued before Florida’s Third District Court of Appeal that conclusively established the legality of merchant cash advances in the state.

When asked for comment, Greenbox Capital® CEO Jordan Fein said:

“It’s been a long, arduous, and expensive battle over the last few years proving in a court of law that a Merchant Cash Advance is not a loan. Today, we celebrate a win for all Merchant Cash Advance companies in Florida and the entire United States who are dedicated to funding small businesses through ethical practices. Our hard work and commitment to helping small businesses grow was validated and we are thrilled with the final decision of the District Court of Appeal.”

The decision in Florida echoes a similiar opinion reached in New York in 2018.

It’s Official, Merchant Cash Advances Not Usurious in Florida

January 6, 2021 Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Big news in the State of Florida. The Third District Court of Appeal entered its order on January 6th to decide the fate of Craton Entertainment, LLC, et al., v Merchant Capital Group, LLC, et al..

Merchant Capital Group, LLC dba Greenbox Capital sued Craton in December 2016 over a default in a Purchase and Sale of Future Receivables transaction. In turn, Craton responded with various defenses and counterclaims that asserted the underlying transaction was really an unenforceable usurious loan.

The Circuit Court for Miami-Dade County sided with Greenbox in August 2019. The defendants appealed.

The District Court of Appeal decided the matter conclusively on January 6, holding that the original ruling was affirmed on the basis that:

- The transaction is not indicative of a loan where repayment obligation is not absolute but rather contingent or dependent upon the success of the underlying venture

- that the transactions in which a portion of the investment is at speculative risk are excluded from the usury statutes

- when the principal sum lent or any part of it is placed in hazard, the lender may lawfully require, in return for the risk, as large a sum as may be reasonable, provided it is done in good faith.

The decision can be viewed here.

The lawyers representing Appellee Greenbox Capital were Henderson, Franklin, Starnes & Holt, P.A., William Boltrek III, Shannon M. Puopolo and Douglas B. Szabo.

You should contact an attorney to discuss the implications of this ruling. Merchant Cash Advance contracts are not all the same.

This ruling is similar to a ruling in New York that was made in 2018.

Failing Main Street NY

December 21, 2020 During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

The struggle between understanding and posturing is on display right now in Albany. While small business owners struggle to open their doors, the legislature passed a so-called “truth in lending for small business” bill that claims to provide more disclosure to business owners seeking financing. Led by Senator Kevin Thomas and Assemblyman Ken Zebrowski the bill is currently pending before Governor Cuomo. The legislators recently authored an op-ed that further demonstrates their failure to recognize that the innocuously named bill is rife with faults and lacks a competent grasp of small business issues. The critical blind spots in the bill’s design threatens billions of dollars in capital leaving New York—a failing small businesses owners can scarcely afford at such a difficult time.

Yet, rather than incentivizing finance providers to stay in New York, the legislature is focused on complex disclosures that lack real meaning or understanding to small business owners. Senator Thomas opined on the Senate floor “… the reason I introduced this bill is because people don’t use standard terminology.” Interestingly, this bill creates several new terms and metrics that would be required to be disclosed that have never been used before in finance. Terms like “double-dipping” and new confusing metrics that even the CFPB under President Obama labeled as “confusing and misleading” to consumers. This bill’s fatal flaw is that it has confused information volume with transparency, somethings a recent study proved would harm small business owners.

Even Senator Thomas acknowledged the legislation’s myriad of problems while still encouraging its passage. In his colloquy with Senator George Borrello on the Senate floor, right before he called New York small business owners “unsophisticated,” he mentioned how his bill had “many issues” that he “hoped” would be worked out before implementation. Hope is not a strategy and it won’t help small business owners obtain the financing they need to stay in businesses. Advancing legislation that would limit options for entrepreneurs working to stay in businesses during a pandemic that has crippled the New York economy represents a reprehensible failure of leadership.

Minority-owned businesses have faced a disproportionate economic impact from the pandemic. According to the Fed, Black-owned businesses have declined by 41% since February, compared to only 17% of white owned businesses. Further, the Paycheck Protection Program (PPP), the federal government’s signature relief program for small businesses, has left significant coverage gaps: these loans reached only 20% of eligible firms in states with the highest densities of minority-owned firms, and in counties with the densest minority-owned business activity, coverage rates were typically lower than 20%. Specific to New York, only 7% of firms in the Bronx and 11% in Queens received PPP loans. Moreover, less than 10% of minority-owned businesses have a traditional banking relationship—something that was initially required to have access to the PPP.

The lack of cogency and lazy approach to this legislation is a disservice to the hard-working entrepreneurs who continue to open their businesses while facing daily economic uncertainty. Governor Cuomo has worked tirelessly to continue to provide economic relief to both businesses and consumers—removing billions in financing for small businesses will only hinder this effort. New York can do better.

Steve Denis

Executive Director

Small Business Finance Association