NY Court Says MCA Agreement is a Factoring Agreement, Not a Loan

March 22, 2021 A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

In Principis Capital LLC v Team Van Eyk, Inc. et al, Principis sued the defendants over a breach of contract. Defendants “did not deny the facts underlying the motion or the the amount due,” the judge said, “but asserted instead that the Agreement is not an agreement for the purchase of future receivables; but is instead, a criminally usurious loan, and is therefore void as a matter of public policy.”

This defense actually led to victory for the plaintiff.

The Appellate Division, First Department, in Champion Auto Sales, LLC v Pearl Beta Funding, LLC (159 AD3d 507, 507 [1st Dept], lv denied 31 NY3d 910 [2018]) has considered this issue, involving a merchant agreement substantially similar to the agreement in this matter, and has held that the type of agreement involved in this case is a factoring agreement rather than a usurious loan. This court is bound to follow Champion and, therefore finds that the Agreement is a factoring agreement and not, as defendants assert, a usurious loan. There are, therefore, no genuine triable issues of fact, and plaintiff is entitled to summary judgment on its complaint.

Case closed.

Steve Denis, SBFA on Why Maryland MCA Bill Failed

March 22, 2021 “In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

“In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

Denis was referring to the nearly unanimous canning of Maryland’s MCA “Prohibition” bill last week. The bill failed to get enough support to leave the committee, blocked by a 19 to 3 vote against bringing the law out to the House floor. Denis, a proponent of the MCA and alt financing industry for years, said it was due to legislators understanding the need for capital “out there during the pandemic” and how harmful an APR cap could be for both business owners and the broker industry.

The law was originally proposed last year before covid shutdowns, but that also failed to make it to the floor. It now appears to be an annual event.

“Our goal as an organization is to make sure that small businesses have access to all different types of financial products and that we believe that small businesses are in the best position to make good decisions for their businesses,” Denis said. “The bill in Maryland narrowly targeted MCA products, and as you know and a lot of folks in the industry know, that sometimes MCA is in the best interest of the business, there’s a lot of benefits to an MCA.”

Denis punctuated his statement with the mantra- we were not out of the woods yet. An APR disclosure bill was just introduced in the Connecticut State Senate last month, modeled off the New York APR bill set to go into effect this year. Denis was hopeful the legislators could learn from speaking to industry interests and change their course like in Maryland.

“We are engaged, I think we’re in a good spot. With any of these bills, Maryland, Connecticut, I caution you know we’re not out of the woods yet,” Denis said. “We still want to work really closely with policymakers. We’re for meaningful disclosure, we think there needs to be some guardrails on our industry, but I think that the most important thing we can do is continue to educate folks in states.”

Tune In Tuesday at 10:30 AM EST: deBanked TV Live – With Guests From the Business Funding Industry

March 22, 2021 deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked’s massive in-person conference, Broker Fair, will return to NYC later in the year on December 6th at Convene at Brookfield Place in lower Manhattan.

Merchant Cash Advance is as Old as The Renaissance

March 21, 2021 The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

In Jakob Fugger the Rich, historian Jakob Strieder writes the Fugger enterprise began as one of the upstart merchant families of the Renaissance. The Fuggers were traders and cloth merchants from Augsburg, Germany. They created a network of aristocratic clients, furnishing weddings and parties through trading warehouses in modern-day Venice, Florence, and Austria. Jakob Fugger I lent some money around, but when Jakob Fugger II joined the family shipping warehouse in Venice, he looked for a better return on capital.

According to International Business History: A Contextual and Case Approach, Fugger entered an agreement to supply some cash- 23,627 Florins to a silver mine owned by Archduke Siegmund in 1487.

Siegmund had plenty of silver laying around for collateral; he just needed cash for the day-to-day. It was a collateral-backed loan, common today: if he couldn’t pay it back, the Fuggers would get paid in silver. The transaction worked so well that a year later, Siegmund reapplied, this time in a revolutionary way. Siegmund would get 150,000 florins, and the Fuggers would get paid the future receivables of the silver mine: unrefined and cheap future silver for cash now.

The problem, written by historian Greg Steinmetz in The Richest Man Who Ever Lived, was the Church. Any interest-based transaction was specifically outlawed, though there were hundreds of lenders during this era. The line from Luke 6:35, “Lend and expect nothing in return,” was taken by the Church to mean an outright ban on usury, defined as the demand for any interest at all.

Even savings accounts were considered sinful, but Venetians ignored these rules as they preferred making money to pleasing God, entombed in the motto “First Venetians, then Christians.” Fugger began accepting deposits like a bank to his clients, with a 5% return to investors.

But convicted usurers could be excommunicated and denied a Christian burial, a nightmare for a capitalist who relied on a Christian network. Fugger did not worry about punishment or the apparent sin of money lending, but as he became a fixture in European society, his reputation became increasingly vulnerable.

Fugger needed the laws to be changed, or at least relaxed, or his lending business was in trouble. In 1515, he wrote a letter to Pope Leo X and funded a debate in the St. Petronius Basilica in Bologna. The debate ran for five hours, a back and forth of philosophy, scripture, and rampant crowd heckling. In the end, it was declared a tie, but Pope Leo X that year signed a papal “bull” reforming the concept of usury.

Originally, the Church pointed to the philosopher Aristotle’s model for determining what was okay to charge for and what wasn’t. Aristotle had said that charging someone for a cow because it produced milk was fine, but money was a dead thing and unfair to profit from.

A silver mine produced silver and as such paying cash for the future proceeds of the mine had allowed Fugger to more or less carry on his business. It wasn’t called merchant cash advance back then but he applied that model wherever he could. Not everyone in need of money had a business, however, and it was critical that he be allowed to charge interest when circumstances called for it.

More than a millennium after Aristotle, Pope Leo X found that risk and labor involved with safeguarding capital made money lending a living thing. As long as a loan involved labor, cost, or risk, it was in the clear. This opened a flood of church-legal lending: Fugger’s lobbying paid off with a fortune.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

McCarthy wrote: That was one of the problems with the Fugger model- “how does one take possession of Austria or France or Spain when its rulers default or lag behind debt repayment schedules?”

After gaining the good faith to lend in the Church’s eyes, the papacy itself became a Fugger customer. Positions in the Church were inseparable from social and political power, and the only way to get a place on the totem pole was by paying for a title. Just as the richest silver mine owners didn’t have the cash to pay for lunch- so did wealthy aristocrats need capital to afford positions in the cloth.

By the time Martin Luther “nailed” his 95 theses to the door of a church in 1517, he was rallying against the Fugger funding family and its stranglehold on the Roman Catholic Church.

It all came down to an in-house promotion. Albert Brandenburg brought a whole new meaning to the concept of “moneychangers in the temple.” A German Archbishop of Magdeburg, Brandenburg was promoted to Elector of Mainz: the second in command of the Holy Roman Empire. Unfortunately, he had to pony up 21,000 ducats to pay the Roman Curia (the Church’s admin)- for the title. Naturally, he didn’t have the cash, and the Fuggers stepped in.

Brandenburg got a loan on interest. To pay it back, he also paid Pope Leo X for the right to sell indulgences. Indulgences were contracts the church sold to forgive sins, allowing believers to purchase their way out of purgatory and into heaven. A fresh round of indulgences was printed to fund the construction of St. Peter’s Basilica, and Brandenburg was entrusted to sell them in 1517. (Their sale was later banned by the Church in 1567).

The sale of indulgences  interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

“I’m saying that there are some specific parts of modern life that derive directly from the Protestant Reformation. We couldn’t have these features if it hadn’t happened.” Ryrie said. “That combination of free inquiry, democracy, and limited government is pretty much what makes up liberal, market democracies. It runs the modern world.”

To this day, no one is sure of the extent of the Fugger fortune. Historian Mark Häberlein found that Fugger struck a deal with Augsburg Tax authorities in 1516: he agreed to pay an annual lump sum on the condition that his family’s true wealth would never be revealed. He died in 1525.

To get an idea of the extent of his wealth, we can base calculations on the cost of butchering a pig in 1522 (yes, that’s a real metric.) It cost one Gulden, a new coin minted in 1500 to butcher a hog. The German coin contained about the same amount of gold as a Florin.

Based on those ham prices, Jim Ulvog from Ancient Finances estimated that in 2017 a single florin would be worth ~$900, and other writers have put the florin in the same range. Though the true wealth of the Fuggers may never be known, when Charles V aimed to take control of the Holy Roman Empire in 1519, the Fuggers were lending Charles 543,000 guldens to buy votes: approximately $448 million. That’s just in a single deal.

It’s been said that merchant cash advances or sales-based financing is relatively new, but it could be argued that such transactions are so old that life as we know it in the modern world only exists because a guy 500 years ago was engaged in non-loan transactions to fund businesses in a manner that was Church-compliant and wanted to expand.

Connecticut Introduces Commercial Financing Disclosure and Double Dipping Bill

March 20, 2021 Ever since New York State Senator George Borrello famously questioned the meaning of “double dipping” in a commercial financing transaction, states have rushed to include the term in proposed laws despite no one knowing exactly what it means.

Ever since New York State Senator George Borrello famously questioned the meaning of “double dipping” in a commercial financing transaction, states have rushed to include the term in proposed laws despite no one knowing exactly what it means.

The latest state is Connecticut, which introduced SB 745 in February, an “Act Requiring Certain Financing Disclosures.” It is essentially a copy & paste of New York’s recent law which is slated to go into effect in June.

The Connecticut bill similarly applies to factoring, merchant cash advance, business lending and more. It was introduced by State Senator Saud Anwar (D).

A hearing held on March 2nd, drew testimony from the Commercial Finance Coalition, Small Business Finance Association, Electronic Transactions Association, Innovative Lending Platform Association, and Secured Finance Network.

If the bill passes, it is designed to go into effect in October of this year.

Maryland’s Latest Merchant Cash Advance Prohibition Bill Failed to Advance

March 18, 2021 Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

“I don’t want to snatch defeat from the jaws of victory,” he maintained.

There were several amendments up for consideration, including the inclusion or removal of a 24% APR rate cap on MCA transactions. The subject of APR dominated the light Q&A that took place, but one delegate voiced concern that creating restrictions on capital providers to businesses that might not be able to obtain funding elsewhere would probably be counterproductive. And when a roll call of votes was taken to determine if the Bill should advance to the Floor, he voted no, as did nineteen of his colleagues. Only three voted yes, so the bill did not advance, ending its prospects for the 2021 legislative session. However, it could be reintroduced again in 2022.

Committee Vice-Chair Kathleen Dumais (D) said that she thought the bill “was not ready” despite Delegate Howard “having worked hard on it.” This was Howard’s second try in two years to move it forward. His first attempt, introduced on February 7, 2020, was called the Merchant Cash Advance Prohibition Bill. The more recent one dropped the “prohibition” label but used language that would have effectively prohibited them in the state of Maryland.

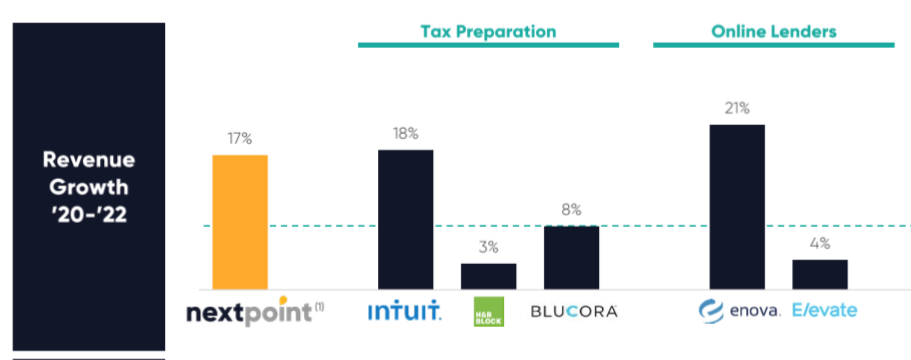

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.

The MCA of the Major Leagues

February 20, 2021 It’s been said a million times. It’s not a loan. The seller receives an upfront payment in exchange for an agreed upon percentage of future earnings. If there’s no earnings, then nothing is owed.

It’s been said a million times. It’s not a loan. The seller receives an upfront payment in exchange for an agreed upon percentage of future earnings. If there’s no earnings, then nothing is owed.

No, it’s not a merchant cash advance, it’s a big league advance, a deal offered by a company named just that, Big League Advance (BLA) to baseball players.

“Players receive an upfront investment from Big League Advance in exchange for an agreed upon percentage of their future Major League earnings,” the BLA website says. “If the player never makes it to the Major Leagues, the player will never owe or pay any money back to Big League Advance.”

The company was founded in 2016 and recently made the news because of its success with Padres player Fernando Tatís Jr. Tatís recently signed a 14 year contract with the team worth $340 million, the third highest in history. And now BLA stands to get their cut, potentially as much as $30 million, according to the WSJ.

The BLA website explains it as such:

Players choose what percentage of their future career earnings they want to give Big League Advance. For example, Big League Advance may offer a player $50,000 for every 1% of his future professional earnings. If a player wanted to sign a deal for 5%, he would receive $250,000, or if he wanted to sign a deal for 10%, he would receive $500,000. While our offer amounts are non-negotiable, the percentage the player would like to give up is up to the player.

The average deal is for 8% and the underwriting performed is a combination of the players’ background, scouting, and statistics.

Michael Schwimer, a former Major League pitcher, is the founder and CEO. The WSJ says that the company has made advances to 350 players for a combined $150 million.