Marketplace Lending

Lending Club Raises Minimum Deposit Amount for New Investors

May 18, 2017The micro retail investor can no longer experiment with peer-to-peer lending through just a handful of loans, according to a recent announcement made by Lending Club. Going forward, new users must deposit at least $1,000 to get started. Those investors can still allocate $25 per loan, however. The reason for the deposit increase? Forced diversification.

A Lending Club blog post explained that “data shows that Lending Club investors who are able to diversify their accounts have generally experienced less volatility than investors with more concentrated holdings. This is in part because investors are able to purchase multiple Notes, reducing their exposure to any single Note.” 98% of accounts with more than 100 notes have experienced positive returns, they claim.

On the LendAcademy blog, Peter Renton advocated for an even higher minimum, $2,500, so that investors could at least start off with 100 notes.

It’s an acknowledgment that the type of investing actually carries the risk of loss and is not actually for everyone. I would not be surprised if they eventually set a minimum deposit amount of $10,000 or simply phased out retail investors altogether in favor of accredited ones at a minimum instead. Time will tell.

Prosper Loaned $585M in Q1, Losses Continued

May 16, 2017Prosper had a net loss of $23.9 million in Q1 on only $30.8 million in revenue, according to the 10-Q they filed Monday. They originated $585.6 million in loans, 90% of which were funded through their Whole Loan Channel, the segment made up of accredited and institutional investors who buy entire loans.

Prosper had 371 full-time employees at the end of Q1 compared to 667 full-time employees at the end of Q1 2017.

The full report can viewed here.

—–

Note: The net loss figure was originally published with an incorrect digit. It has since been corrected

System Error: Prosper Showed Incorrect Returns to Investors

May 3, 2017Investor returns weren’t what they claimed for at least seven quarters, according to a notice Prosper issued on Wednesday.

It recently came to our attention that the annualized net return numbers displayed on your account overview page were inaccurate due to a system error. This error affected the Annualized Net Return and Seasoned Net Annualized Return numbers and has now been fixed.

This error did not impact any other part of your account, including payments, deposits, monthly statements, tax documents and note and loan level information – including estimated returns.

We sincerely apologize for this error. If you have any questions, please email us at investorquestions@prosper.com.

And this was no small adjustment. On LendAcademy, Ryan Lichtenwald said his returns were adjusted from 13.55% down to 9.27%. One user on the LendAcademy forum said his returns were adjusted down from 10% to 8% and another from 14% to 7%. Yet another individual who interacted with me on twitter claims his return dropped from 10% to 1.2%. While we can’t confirm some of these accounts, Prosper’s admission and Lichtenwald’s post on LendAcademy are pretty alarming.

An old LendAcademy forum post shows users mulling over Prosper’s return calculation more than a year ago, but were unsure what to make of it.

In December 2016, the subject came up again.

That same month, Prosper hired a new CFO, Usama Ashraf.

Update: According to Bloomberg, “some of the investors that were affected saw their annual returns fall in half, but in most cases returns fell less than 2 percentage points.” A Prosper spokesperson said that the issue has been going on for several quarters.

Update 2: According to Financial Times, “The miscalculations affected a majority of Prosper’s customers and date back as far as seven quarters.”

Links to additional websites that show investors were growing suspicious of Prosper’s calculations:

Oct 2016: Prosper showing return of 8% – “What I don’t understand, is that when I look at my statements and compare account balances, I’m seeing a return of closer to 4%.”

Reactions from Prosper investors on the Internet:

“My displayed returns are now 1/2 of what they used to be.”

“I was at 16.81%. Today my account shows 9.42% – so not exactly half, but a lot.”

“Prior to the update I was somewhere close to 11%. After the correction…6.65% HAHA”

Re-Banked

April 23, 2017

Just a few years ago, the financial services community was fixing for a battle of David and Goliath proportions—with scrappy, upstart online lenders threatening to rise up and vanquish the fearful and mighty brick and mortar banks. Instead, the unexpected happened: a number of well-respected online lenders and banks set aside their battle arms and began looking for ways to collaborate with their rivals—offloading loans, making referral agreements and establishing more formal partnerships, for example.

“In the real world, sometimes David wins. Sometimes Goliath wins. Just as plausibly, sometimes both sides carve up a market and they often have different offerings that target unique customers,” says Brayden McCarthy, vice president of strategy at Fundera, a New York-based marketplace for small business lending that works with a variety of lenders, including traditional banks.

Certainly, the change didn’t happen overnight. But over time, both online lenders and banks have been forced to tailor their expectations more closely to market realities. Despite their fast growth trajectory, several online lenders have come to realize that they lack several things many banks have, namely a strong, time-tested brand, a solid customer base and ample capital. Banks, meanwhile, have realized that their slow start out of the gate with respect to technology is a severe competitive disadvantage, and that they need more nimble, savvy partners to stay in the game.

Given these shifts, more and more online lenders and banks are taking the approach that if you can’t beat ‘em, join ‘em. Although some industry leaders are actively pursuing strategies that put them in direct competition with banks, partnerships of varying degrees between traditional banks and alternative players are increasingly common. As a result, the lines separating the two are getting increasingly blurry.

“Market forces are acting as a shotgun at the wedding. Whether the two sides are entirely comfortable with the marriage is irrelevant, they need one another,” says Patricia Hewitt, chief executive of PG Research & Advisory Services LLC in Savannah, Georgia. “They’re stronger together than they are alone.”

The evolution of Square is a prime example. The San Francisco-based company really packed a punch in the merchant services world with its mobile card reader designed for small businesses. From there, the payments company sought additional ways to diversify, eventually turning to merchant cash advance as a way to help small business customers obtain funds quickly. Then, in March of last year, Square moved into online lending, teaming up with Celtic Bank of Utah to offer small business loans online. The partnership got off to a running start. In its most recent earnings report, Square said it facilitated 40,000 business loans totaling $248 million in the fourth quarter of 2016—up 68 percent year over year—while maintaining loan default rates at roughly 4 percent.

Even SoFi, the San Francisco-based online lender that has been pointedly outspoken in its anti-bank rhetoric, now has bank-like aspirations. In February, the lender acquired mobile banking startup Zenbanx, giving it the ability to offer checking accounts and credit cards in 2017. Also in February, SoFi teamed up with Promontory Interfinancial Network to enable community banks to purchase super-prime student loans originated by the online lender. Large banks have been buying SoFi loans for several years.

COLLABORATION IS THE WAVE OF THE FUTURE

Many see collaboration between banks and online lenders as a logical step in the industry’s evolution. Online disrupters have forever changed the face of lending—in the same way that online brokerage shaped the financial advisor industry, according to Bill Ullman, chief commercial officer of Orchard Platform.

“There’s a tendency to want to view things as either black or white, online lenders vs. banks. The reality is that the entire financial services industry is undergoing a transformation with technology as the core driver,” he says. “I am of the view that both traditional financial services companies and fintech players can survive and thrive,” Ullman says.

For its part, Orchard recently inked a deal with Sandler O’Neill that provides access to the Orchard platform for the investment bank and brokerage firm’s bank and specialty finance clients. The deal is expected to help small banks better evaluate their options with respect to online lending opportunities.

Partnerships between online lenders and banks take many forms. Some of them are behind the scenes, where marketplaces sell loans to banks or banks informally refer customers. Others are more public. For example, in September 2015, Prosper and Radius Bank of Boston teamed up to offer personal loans to certain customers through the bank’s website using the Prosper platform. Customers can borrow from $2,000 to $35,000 in this manner.

Then in December 2015, JPMorgan Chase and OnDeck joined forces in order to dramatically speed up the process of providing loans to some of the banking giant’s small business customers. In April 2016, Regions Bank and Avant announced a partnership to better serve customers who don’t meet Regions’ credit criteria.

Avant’s customers typically have a credit score between 600 and 700, while Regions sets the bar higher. “The benefit for banks is that they do not need to worry about a platform taking away customers that meet their own credit criteria,” according to Carolyn Blackman Gasbarra, head of public relation at Avant.

She notes that Avant expects to replicate this model with more banks in 2017. “Lately many platforms and banks have come to realize their counterparts are more friend than foe,” she says.

Given the changing tides, industry watchers expect to see more relationships develop between online lenders and banks over time. These could include referral agreements, technology licensing arrangements, formalized revenue-sharing partnerships and perhaps even outright acquisitions.

PARTNERSHIP ADVANTAGES

Certainly, working together can be mutually beneficial for both online lenders and banks. For new online lenders and other fintech players, partnering with an established bank allows them to bypass significant regulatory and compliance hurdles because the necessary requirements are already in place.

“Why jump through all the hoops when you can just have a buddy system with an existing lender?” says Kerri Moriarty, head of company development at Cinch Financial, a Boston-based company dedicated to helping people make smarter investment decisions.

Fintechs that license their technology to banks still have to meet the high standards of third-party vendors determined by bank regulators, notes Stan Orszula, co-head of the fintech team at the Chicago law firm Barack Ferrazzano Kirschbaum & Nagelberg LLP.

“But it’s still less onerous than being a direct lender,” says Orszula, who works closely with banks and fintech providers on legal, regulatory and corporate issues. “They are learning that they need banks. They really do.”

Even seasoned online lenders that have a regulatory framework in place can benefit from bank relationships by using banks’ established brands as leverage. “Everyone knows Chase, Bank of America and American Express,” says McCarthy of Fundera. “They have a solid name and a solid in-built customer base to be able to offer product to them,” he says.

Teaming up with a bank gives added credibility to an online lender, at a time when the public’s confidence has faltered due to highly publicized troubles at certain firms. “Partnering has a very important signaling effect that these online players are here to stay,” McCarthy says.

Banks, meanwhile, need the nimbleness and innovation that online lenders provide. “Banks realize they have to catch up with the fintech disrupters,” says Mark E. Curry, president and chief executive of SOL Partners, which provides strategic management and information technology consulting services to financial services companies.

DIFFERENT TYPES OF PARTNERSHIP OPPORTUNITIES ABOUND

When it comes to partnerships between banks and online players, there are numerous options. In the small business lending space, for example, McCarthy of Fundera says he expects banks to continue buying loans from online lenders, as they have been for many years. He also expects more banks will route declined applicants to online lenders or online loan brokers. “This is a partnership that will allow them to make up some incremental revenue by referring business,” he says.

In addition, McCarthy says he expects banks to make products available through online marketplaces and use an online lender’s technology for online loan applications. He also expects banks will use online lenders’ technology for underwriting and servicing loans.

Years ago, before John Donovan joined Bizfi, he recalls talking to a salesman for a large national bank. The bank didn’t offer a lending product that he could give to small businesses and the salesman was losing customers as a result. “That’s where we see a lot of those opportunities,” says Donovan, chief executive of the online marketplace for small business loans.

For instance in March 2016, Bizfi partnered with Western Independent Bankers, a trade association, for over about 600 community and regional banks, to link small business clients to financing options through Bizfi. Many banks don’t offer small business loans below $150,000, whereas the average loan Bizfi does is $40,000, Donovan says, adding that the company would like to develop additional relationships similar to its agreement with Western Independent Bankers.

In the future, he predicts fintechs will continue to be more receptive to the idea of working with banks and vice versa, as the industry digests the impact of deals that are still in their early days.

FINDING STRATEGIC GROWTH OPPORTUNITIES

As banks and online lenders become increasingly accustomed to working together, there may be more opportunities for strategic acquisitions. For instance, Sandeep Kumar, managing director of Synechron, a global consulting and technology firm, expects to see banks—especially mid-tier players that don’t have the resources to innovate like big banks buying lending-related start-ups. He says banks will likely be most interested in companies that can help them with AI and other techniques to pinpoint where they should spend more efforts on cross-selling and customer profiling, for example. “There are many start-ups in this area that have very compelling technology,” he says.

On the other hand, Chris Skinner, an independent commentator at The Finanser Ltd., a research and consulting firm in London, points out that the two cultures don’t always mesh. “Quite a few startups have young, entrepreneurial founders that would loath the idea being acquired by a bank. So it really depends on the circumstances,” he says.

Valuation differences between large banks and leading online lenders may also be a sticking point for some deals, Ullman of Orchard points out. Banks’ concern over their valuation “will place a certain amount of restraint and discipline on the tech M&A activities they pursue,” he says.

ANTICIPATING TROUBLE IN PARADISE

While increased collaboration between online lenders and banks sounds good on the surface, John Zepecki, group head of product management for lending at D+H in San Francisco, urges both sides to proceed with caution. “You have to find an arrangement where you don’t have conflict,” he says. “If your innovation partner also is a competitor, it’s a challenge. If you have an inherent conflict, it doesn’t get better over time.”

That’s one reason why companies like Chicago-based Akouba have come on the scene. In Akouba’s case, its goal is to provide banks with the technology such that they don’t have to partner with an online lender that has the potential to compete for business. “We don’t compete with the bank in any way whatsoever,” says Chris Rentner, the company’s founder and chief executive.

Akouba’s business lending platform—which the American Bankers Association endorsed in February—provides banks with leading edge technology that integrates the bank’s own unique credit policies into a convenient, online process—from application to documentation— all the way to closing and funding. The bank uses its own credit policies, originates its own loans and owns the entire brand and customer relationship.

Rentner says he started the business with the idea in mind that the online lending model wouldn’t be sustainable long-term and that working alongside banks—as opposed to competing head to head— was the direction to go. “The idea that they could somehow get all of the consumers out of the banking world and onto their platforms was never going to happen. That’s why we exist today,” he says.

Catching Up With Marketplace Lending – A Timeline

April 20, 20172/17

- Prospa, an online small business lender based in Australia, was valued at $235M (AUD) in a $25M capital raise

- Square announced funding $248 million worth of business loans in Q4 2016

2/21 A Massachusetts state court vacated a merchant cash advance COJ

2/24 SoFi raised $500M in a financing round led by Silver Lake Partners that reportedly gave SoFi a $4.3B valuation

2/27 Prosper Marketplace closed a loan purchase agreement with a consortium of lenders for up to $5 billion of loans that has a provision that also enables the lenders to buy up to 35% of the company

2/28 BlueVine secured a warehouse line of up to $75M from Fortress

3/1 Lendio launched a new franchise program, allowing local offices around the country to become Lendio franchisees

3/3 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Marlette Funding for violating the state’s usury cap

3/5 Two trade associations, the Innovative Lending Platform Association (ILPA) and the Coalition for Responsible Business Finance (CRBF), joined forces. The merged company will continue to be known as ILPA

3/6 Upstart raised $32.5M

3/7

- It’s reported that former CAN Capital CFO Aman Verjee is now the COO of 500 Startups

- Kabbage priced a $525M securitization. It was oversubscribed

3/9 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Avant for violating the state’s usury cap

3/13

- Melvin Chasen, the founder of Rewards Network (originally Transmedia Network, Inc.) passed away. He was 88.

- The New York State Assembly rejected the Governor’s proposal to grant the Department of Financial Services (DFS) regulatory authority over any online lender doing business in the state

3/15

- The New York State Senate also rejected the proposal to further regulate lending

- The OCC published a manual on how it will evaluate charter applications from fintech companies

- The New York DFS published a statement rejecting the OCC’s plans

- The WSJ reported that Marlette Funding was cutting nearly 1/5th of its workforce

3/16 WebBank announced that it had a net income of $29.2M for 2016 and that it had a market valuation of $319.4M

3/20 Prosper Marketplace announced that it had originated $2.2B in loans in 2016, down from $3.7B in 2015, and had a net loss of $119M.

3/21 It’s reported that Kabbage will set up its European headquarters in Ireland

3/22 OnDeck expanded its credit facility with Deutsche Bank by $52M to a total of up to $214M

3/27 IOU Financial wins Gold Stevie Award for Best Use of Technology in Customer Service

3/30 In Advance Capital announced that they had secured access to an additional $50M

4/5

- Budget passes in New York. Proposed lending legislation was not included in it.

- Kabbage surpasses $3 billion funded to small businesses

See previous timelines:

12/16/16 – 2/16/17

9/27/16 – 12/16/16

Lending Club to Beta Hardship Plans for Borrowers (and Protect Returns for Investors)

April 5, 2017Lending Club wants to make it easier to accommodate borrowers facing hardship and in the process potentially protect the investor from unnecessary losses. A full explanation of the program was sent out to Lending Club investors on Wednesday, the full text of which we’ve pasted below:

At Lending Club, we are committed to improving experiences for both borrowers and investors. We’re excited to announce that after a beta test, we will begin offering hardship plans to borrowers effective May 4, 2017. Hardship plans allow borrowers to temporarily make interest-only payments to accommodate an unexpected life event. As part of this change we are also making additional data fields related to these plans available for investors.

Lending Club continuously looks to put lending industry best practices to work. Hardship plans are commonly offered to borrowers in the lending industry because they allow borrowers time to adjust to a life event (like a medical emergency, temporary job loss, unexpected car or home repairs, death in the family, or other events). Hardship plans are in accordance with commercially reasonable efforts to service and collect on loans, as well as with our prospectus, which provides us flexibility to work with a borrower to structure a new payment plan if needed.

Our hardship plan program specifically targets borrowers who are more likely to return to repaying their loan. Under the plan, borrowers are allowed to temporarily make interest-only payments for a period of 3 months to accommodate an unexpected life event. After 3 months, regular payment terms and obligations resume. Only borrowers who fulfill specific characteristics (such as a demonstrated history of repayment) and who claim a hardship will be offered plans. Importantly, borrowers’ loans must be either current or between 1 and 30 days past due to qualify for a hardship plan.

We believe the hardship program will work to protect investor returns as borrowers whose loans may otherwise progress to charge-off status have the opportunity to make interim payments and some portion may revert to current status.

Finally, we are adding 15 new data attributes of borrowers who utilize hardship plans to investor reports and the API. The fields will only apply for hardship plans offered as of May 4, 2017 and going forward. You can find more information on these new data fields here.

Offering hardship plans is both consistent with our values – doing the right thing by borrowers while they’re getting back on their feet – and helps to protect investor returns. We will potentially look to expand to different types of hardship plans in the future as we gain further insight into borrower behavior and continue to listen to customer feedback.

Please feel free to reach out with any questions – we welcome your feedback.

Best regards,

The Lending Club Team

Prosper Lost A Whopping $119 Million in 2016

March 20, 2017 Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

| Year | Revenue | Profit (Loss) |

| 2012 | $7.6M | ($16.0M) |

| 2013 | $18.3M | ($27.0M) |

| 2014 | $81.3M | ($2.6M) |

| 2015 | $204.2M | ($26.0M) |

| 2016 | $136.0M | ($118.7M) |

General and Administrative was the largest line item expense at $102.7M, which consisted mainly of employee compensation. The second largest expense was Sales and Marketing at $70.1M.

The company originated more than $2.2 billion in loans for the year, down from $3.7 billion last year.

“The decrease in originations we experienced during the year ended December 31, 2016 were primarily driven by a number of our largest investors pausing or significantly reducing their purchases of Borrower Loans beginning in the second quarter of the year,” their earnings report said. “We believe these investors have paused or reduced their investment activity because of an increase in their cost of capital; negative actions and publicity at competitors; and our limited use of investor rebates, which have become more prevalent in the industry.”

To try and correct course, Prosper offered to sell up to 35% of their company to a consortium of Wall Street’s elite who have the right to buy up to $5 billion of their loans over the next 2 years.

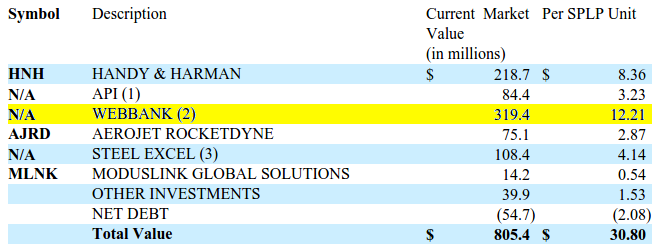

WebBank Releases Earnings, Market Valuation

March 20, 2017 WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

“Despite significant declines in a number of WebBank’s key programs, caused by capital market disruptions, WebBank successfully added new partners, new products and began holding more assets to maturity in 2016,” the report read.

Although Steel Partners also owns businesses in energy, defense, logistics, food products and more, WebBank is its most valuable segment with a market valuation of $319.4 million. That number, according to the release, is 12x the company’s after-tax net income.

Steel Partners got in on WebBank early, making their initial investment in the bank more than 20 years ago in 1996.

“WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank’s products,” the report says.”Revenue is largely derived from these loans, which provide fee and interest income.”