Marketplace Lending

Marketplace Opens for New Student Financing Investments

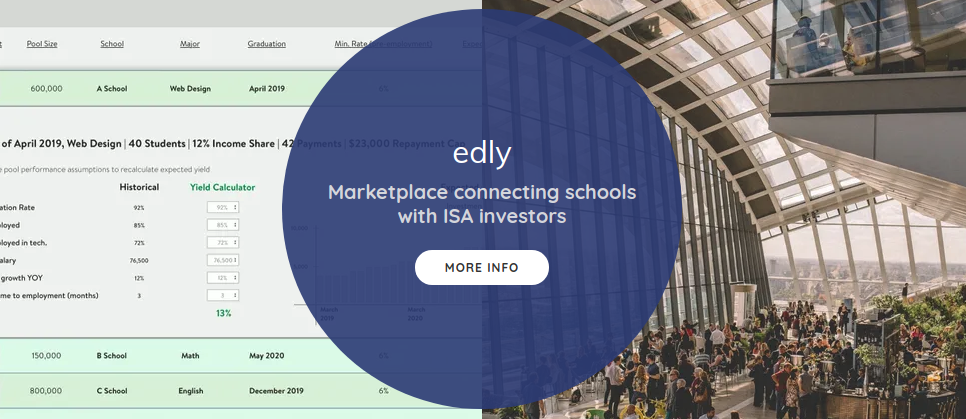

April 5, 2019 Edly, a new online marketplace that connects Income Share Agreement (ISA) investors, announced last week that a prestigious software engineering school in San Francisco listed $2 million in inaugural ISA trades via the Edly marketplace. The school is called Holberton and offers only two payment programs, an ISA or pay it all upfront. LinkedIn CEO Jeff Weiner and many others who are well-established in tech are closely involved with the school.

Edly, a new online marketplace that connects Income Share Agreement (ISA) investors, announced last week that a prestigious software engineering school in San Francisco listed $2 million in inaugural ISA trades via the Edly marketplace. The school is called Holberton and offers only two payment programs, an ISA or pay it all upfront. LinkedIn CEO Jeff Weiner and many others who are well-established in tech are closely involved with the school.

An ISA is an arrangement where investors front the cost of a students’ college education in exchange for a percentage of their future earnings. According to Charles Trafton, co-founder of Edly, ISAs differ from traditional student loans in three primary ways, all of which protect the student: 1) repayments don’t begin until the graduate starts making above a certain amount of money, 2) repayment is limited to a certain amount of time (usually 8 years) and 3) there’s a cap on the amount that the graduate repays, usually one to two times tuition.

“Today, schools have an incentive to maximize the amount they get from each student on their way in – which usually means maximum borrowing – and then spend as little as possible on the student as he matriculates through the school,” Trafton said. “The school has no skin in the game.”

With the ISA model, the school usually has skin in the game. The Edly marketplace requires that participating schools own part of the ISA. This way, the school’s interest is aligned with the student, and later the graduate. If the students are well trained, then they are likely to succeed in the workplace, earn good money quickly and pay the money owed.

The first ISA program in the U.S. was launched at Purdue University in 2016 and Trafton said there are now 23 programs in the country. His mission with the Edly marketplace is to provide liquidity for these investments and Holberton’s $2 million of ISA trades is its first transaction.

Holberton’s ISAs are set up so that graduates only make payments when their salaries are more than $40,000. But Trafton said that Holberton graduates are usually hired by top Silicon Valley tech companies and they typically make nearly six figures in their first year after graduation.

Ron Suber: ‘This Industry Will Look Very Different One Year From Now’

February 25, 2018 Ron Suber wears many hats. His official LinkedIn profile lists him as President Emeritus and Senior Advisor at Prosper Marketplace. Now you can add a new title to his repertoire – the Magic Johnson on fintech. That’s because when it comes to Suber’s legacy, he’s all about the passing game.

Ron Suber wears many hats. His official LinkedIn profile lists him as President Emeritus and Senior Advisor at Prosper Marketplace. Now you can add a new title to his repertoire – the Magic Johnson on fintech. That’s because when it comes to Suber’s legacy, he’s all about the passing game.

“I really enjoy the assist in basketball more than the score or the dunk and so I’m trying to be that leader of assists in our industry, Magic Johnson, if you’ll let me use that analogy … I want to be him for our industry and help everybody win and help the whole thing be bigger, but you have to give the ball to the people in the position where they can score and that’s what I’m trying to do,” said Suber in a podcast discussion with Lend Academy’s Peter Renton, who is also a co-founder of LendIt.

Since Suber stepped down as president of Prosper, his presence in marketplace lending and fintech only seems to have blossomed, which in hindsight may have been the plan all along. The godfather of fintech, as he’s also known, is in the midst of what he’s dubbed a professional rewiring, one that didn’t prevent him from participating in a podcast with Renton.

During the discussion, Suber didn’t shy away from any topic, fielding questions on everything from his investment portfolio, to Prosper, to travel and his views on marketplace lending and fintech. His travels have taken Suber to Patagonia and the straits of Magellan to his favorite Aussie city of Melbourne. Next up Suber plans to explore Africa, including Rwanda and Tanzania.

Suber on Aussie IPO Credible

Suber on Aussie IPO Credible

San Francisco-based Credible, a consumer finance marketplace for millennials, just raised $50 million in an Australian IPO. Suber, who serves as chairman of the fintech, got to know Credible CEO Stephen Dash a few years ago. When Dash needed to raise money, Suber was the first to work with other fintech influencers including a group in Asia to invest $10 million in the company at a $40 million valuation.

Credible followed up with another equity round before deciding to IPO in Australia, where the market is different versus the United States or Hong Kong.

“We were able to meet with the asset managers, the family offices, and the superannuation funds and some of the pension funds in Asia, Hong Kong in particular, and throughout Australia who were very supportive of Stephen Dash, who is from Australia,” said Suber, adding that Credible was the biggest tech/fintech IPO in Australia last year.

Incidentally, Suber has also met with Australia Treasurer Scott Morrison, who sparked a meeting with Suber, Dash, US cryptocurrency exchange Coinbase and other members of the payments market to discuss how Australia can engage with young US entrepreneurs.

We asked Suber what to expect with crypto and lending, in response to which he told deBanked: “Like the very early days of the internet, there were lots of dot-com companies with high valuations in the hype cycle, little revenue and unclear long-game solutions…think Amazon. Big winners emerged, and the majority lost money on the early bets. The same is true for cryptocurrencies. Enormous winners will emerge. In my opinion, the winners include CoinBase, Ripple and Ethereum.”

Suber on Prosper

While Suber has moved on from an executive role at Prosper, he remains engaged with the company and is close with the leadership team, including CEO David Kimball and CFO Usama Ashraf. Suber’s involved across the board, from customer acquisition, to business development and on the capital markets side of things as well.

While Suber has moved on from an executive role at Prosper, he remains engaged with the company and is close with the leadership team, including CEO David Kimball and CFO Usama Ashraf. Suber’s involved across the board, from customer acquisition, to business development and on the capital markets side of things as well.

“It’s again doing close to $300 million a month in originations, it has $100 million in cash it generates cash each quarter, it has its own securitization channel at this time in addition to the consortium … There’s a lot going on there including some product expansion, so there’s no shortage of things to do with Prosper, which I care a lot about,” said Suber.

Suber on Hindsight Being 20/20

Marketplace lending has had peaks and valleys along the way as it has matured from a nascent segment to essentially a transformational influence on the lending space, with its technology touching everything from the business model, to the borrower to the banks.

But if hindsight were 20/20, there are some things he’d do differently the second time around.

He pointed to Prosper’s acquisition of American HealthCare Lending, which he characterized as a “great decision,” giving the marketplace lender an opportunity to tap the healthcare borrower market. But as in any relationship, you can’t change each other.

“We changed American Healthcare Lending too much and tried to make it into something that it just couldn’t be with the point of sale financing. I think the lesson there is it’s great to do an acquisition, but you have to make sure you execute and keep it fresh and focused and successful once you get it,” said Suber, pointing to the acquisition of Tel Aviv’s BillGuard as yet another example of this.

Prosper also took on too much office space around the country.

“Perhaps we could have outsourced a little more instead of all the hiring. Clearly diversifying committed capital and maybe back then even using some of the capital we raised to do these own CLUB deal securitizations, which Prosper does now very successfully with its balance sheet,” he noted.

Suber also urged the marketplace lending market to showcase its technology and unique abilities as “tech-enabled finance companies” more. As the innovator that he is, Suber suggested there should be greater collaboration among marketplace lenders, comparing it to the airline industry. He explained:

Suber also urged the marketplace lending market to showcase its technology and unique abilities as “tech-enabled finance companies” more. As the innovator that he is, Suber suggested there should be greater collaboration among marketplace lenders, comparing it to the airline industry. He explained:

“So, the airline industry is competitive, they’re competing for dollars and seats and people and talented pilots and the best planes, but the reality is they have to work together, they have to make sure that planes don’t crash and that the industry is on time and does lots of good things together… And that’s really what I think we can do better, a better job of as an industry is really working together, competing, but communicating and making sure everybody lands safely.”

Suber on Marketplace Lending

As the godfather of fintech, Suber is often looked to as a guiding voice on the status of the market. That’s why when he says the industry has advanced in innings, it’s revelatory.

“I think we’re in the home stretch, I think we’ve done the seventh inning stretch,” he said. Suber pointed to Asia, where the market has gone from 3,000 platforms to 50 and in the United States where it’s consolidated from 300 to fewer than 100.

“The mature are maturing,” he said,” pointing to a race in which some platforms are pulling away from others in terms of valuation, volume and the ability to engage the industry.

“The separation will continue,” he said. “The industry will look very different one year from now.”

Suber on His Investment Portfolio

If you’ve ever wondered which investment areas Suber believes represent the next opportunity, look no further. He’s “struck” by financial inclusion, in particularly a telecom play Juvo for which he’s an advisor and in which invested a few rounds. Juvo is looking to serve the unbanked in the developing world where they lack financial identities, internet access and smartphones. The company has partnered with the likes of Samsung.

“We talk a lot in the online lending industry about top down, super-prime and prime and near prime; this is my way of coming from the bottom up with technology and data and finance to be involved in financial inclusion. I’m really quite excited about that one,” said Suber.

He also likes startup Unison and the emerging fractionalization of the home equity market, which he characterizes as “the next big thing.” In addition to Suber, this market has attracted the likes of Marc Andreessen.

Suber has nearly 20 investments in private companies, including payment companies, financial inclusion and lending. He’s also become a debt investor to some online lenders, invoice finance plays among others. “I’ve really enjoyed the debt side of investing as much as the equity side,” he proclaimed.

Suber on Broader Fintech

In addition to marketplace lending, Suber is also a believer in the point-of-sale (PoS) solution and invoice finance companies, which he says are “fixing the way invoicing is financed and making it better, cheaper and quicker.” And in taking an overarching view of the market, he also likes the cleantech, pointing to solar fintech play Mosaic and a company called CleanCapital.

Suber on Rewiring

Suber on Rewiring

Suber is a big believer in rewirement, both in his personal life and in business. He defines it as “redesigning one’s life personally and professionally.” Before he applied it to his career, Suber and his wife Caryn pursued a rewirement in their personal lives, one that included selling their home and material possessions, buying a new home and traveling.

In 2017, he decided to do the same thing professionally to strike a better balance in his life. Since then, he’s developed a color-coded regiment by which to live, separating the hours of the week across categories including exercise = blue, personal = green, work = purple and teaching and managing his family office = red.

“There’s a lot of green on my calendar,” he said.

For those interested in rewirement, Suber has launched a blog on the topic, with the maiden couple of entries documenting the first 360 days and counting.

Many of Suber’s quotes here originated from his interview with Peter Renton. Renton is the co-founder of the LendIt Conference.

Get Your Free Hard Copy of deBanked Magazine

October 2, 2017

If you haven’t already signed up to receive our magazine in the past, you should register today to make sure you receive our September/October issue! Subscribing is FREE and this issue is packed with stories, stats, and industry data you can’t find anywhere else.

We can also arrange for multiple copies to be shipped to your office if you like distributing them to your employees, partners or investors. Our magazine is on display in many lobbies and waiting rooms of alternative finance companies nationwide.

Isn’t it time you deBanked?

SIGN UP HERE

Reaction to Lending Club’s New Credit Model

September 13, 2017The few retail investors discussing the recent change Lending Club made to their credit model weren’t exactly optimistic, according to comments on the Lend Academy forum. Of particular concern is grade inflation wherein borrowers who previously scored a C or lower may now find themselves in the A or B category.

“We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model,” Lending Club stated in an email last week.

Retail investor sentiment may not be all that important, however, as capital from self-managed accounts on the platform has waned after peaking in the first quarter of 2016. In Q2 of 2017, self-managed accounts only accounted for 13% of the capital used to fund loans. The majority came from banks and institutions.

Lending Club Launches Its Most Advanced Credit Model Ever

September 11, 2017Lending Club is feeling pretty good about its newest credit model, according to an email that circulated to retail investors this morning. A copy of it is below:

We have launched the most advanced and predictive credit model ever used on the LendingClub platform. It’s the latest in LendingClub’s long history of innovation on behalf of borrowers and investors.

The new model leverages machine learning and 10 years of LendingClub data to better assess and price credit risk. LendingClub has helped 1.5+ million borrowers since 2007; each borrower provides unique insight that we can use in our next decision.

What investors need to know about the new credit model:

• It’s 24% better at differentiating the likelihood of a borrower charging off than the fourth-generation model, and is more predictive than a borrower’s FICO score alone.

• It’s built on a wealth of proprietary data, incorporates more data points for each borrower, uses best-in-class modeling techniques, and uses dozens of new custom attributes that are predictive in assessing risk.

• We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model, and other higher-risk borrowers, who may have received an offer previously, will be screened out.

• We continue to see lower delinquency rates across grades and terms in the existing loan portfolio than in the second and third quarters of 2016.

We see this credit model as the latest innovation in our continuous enhancement cycle, and one that helps us continue to provide investors with solid risk-adjusted returns. See here for more on what makes the model unique.

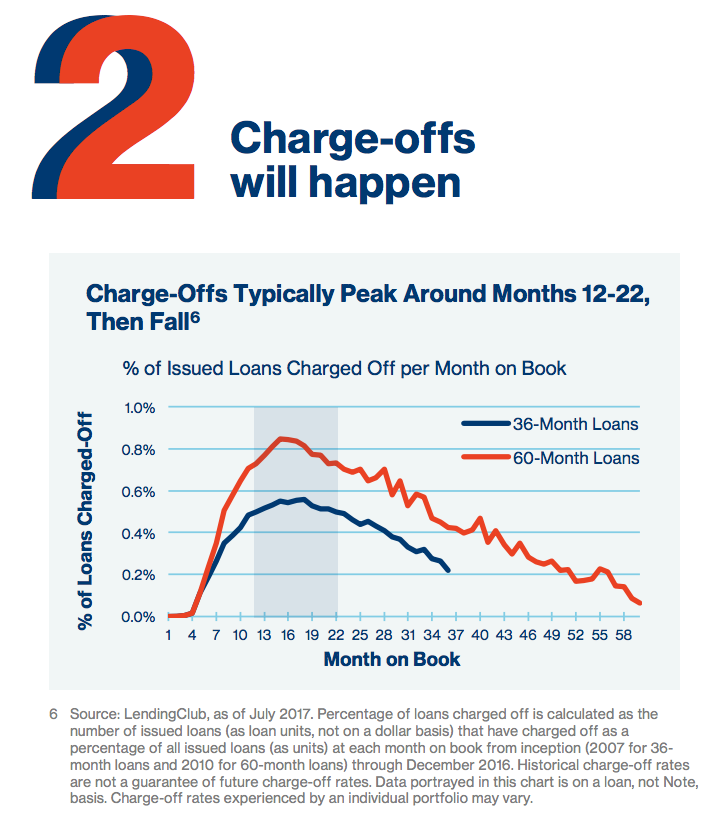

Lending Club: Charge-offs will happen

August 16, 2017 A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

1. Focus on net returns

2. Charge-offs will happen

3. Diversification is key

4. Monthly payments include principal and interest

5. Reinvestment is critical for consistent returns

Lending Club has gradually drawn more attention to the effect of prepayments on loans and this guide is no different.

“Prepayments impact returns because they reduce the amount of principal earning interest from Notes. A Note is considered prepaid when the dollar amount received is greater than the amount due for any given month,” they say. “It is inevitable that certain loans will charge-off or prepay and result in a loss of investment capital.”

Not mentioned however is that investors are charged a 1% fee on all outstanding principal if a borrower pays off their entire loan early despite it being no fault of the investor. And investors are less likely to monitor the impact of these fees if they keep reinvesting their cash which of course Lending Club advises investors to do.

The guide is still helpful in setting expectations for retail investors who ignored or did not understand all the fine print when they signed up. Quoted below about charge-offs:

“It’s inevitable that some borrowers will get behind on their loan payments. Some of these borrowers will get back on track and others will stop repaying their loans. After it’s clear that a borrower won’t make any more payments a loan is considered ‘charged-off.’ All investors in consumer credit experience some charge-offs, so it’s important to understand them and consider how they might impact your investment strategy.”

Overall, the guide is a nice way of keeping retail investors engaged. As someone who invested on the platform for a few years, one of the biggest disappointments I found was that the platform did not feel like a “club” at all. There was no sense of peer community and there was almost no communication whatsoever from Lending Club about anything other than requests to deposit more money.

But lately, peer funding has been dropping off the platform after reaching an all time high back in the first quarter of 2016. In Q2 of this year, only 13% of loans were funded by peers. 44% of loans were funded by banks. Maybe they’re not entirely ready to see individuals disappear completely or maybe they just want those that remain to keep the faith as returns slide. Hopefully, they continue to supply interesting and helpful materials in the future.

Catching Up With Marketplace Lending – A Timeline

August 13, 20175/17 – Funding Circle surpassed Zopa in cumulative lending to become the UK’s biggest marketplace lender

5/18 – Breakout Capital announced appointment of Douglas J. Lanzo as EVP and General Counsel

5/22 – The New York State legislature held a joint hearing on online lending

5/25

- OnDeck had the maturity date of its $100M credit facility extended

- China Rapid Finance reported Q1 net revenue of $10.5M

- Prosper Marketplace closed $495 securitization transaction

- SoFi co-founder Dan Macklin announced his departure from the company

5/31 – IOU Financial reported Q1 results, had $1M loss on $4.3M in revenue and lent (CAD) $22.1M

6/2 – Zopa began allowing investors to sell loans that have previously been in arrears

New York State legislators proposed the formation of an online lending task force

6/6 – deBanked and Bryant Park Capital published their Q1 confidence index in which industry CEOs scored their confidence in the continued success of the MCA and small business lending industry at 73.8%, the lowest level since the survey started in Q4 2015. It peaked at 91.7% in Q1 2016.

6/8 – Amazon surpassed $3 billion in loans made to small businesses since their lending program launched

6/9 – RealtyMogul announced that they had exited the residential fix-and-flip market

6/12 – The US Treasury published a report that called for the repeal of Section 1071 of Dodd Frank

6/13

- SoFi applied for a bank charter, specifically an Industrial Loan Company charter

- Lendio announced a pilot agreement with Comcast business

6/14 – Patch of Land expanded its debt facility from $10M to $30M

6/19 – Goldman Sachs’ online lender Marcus surpassed $1 billion in loans made since inception

6/20 – Former Lending Club CFO Carrie Dolan joined Metromile, an insurance company, as CFO LendingTree acquired MagnifyMoney

6/21 – Pearl Capital secured $15M in financing from Chatham Capital Management

6/27

- Square Capital announced that it will pilot a consumer loan program

- Former RapidAdvance CFO Rajesh Rao became the CFO at Beyond Finance, Inc.

6/29

- Funding Circle hired Joanna Karger as US Head of Capital Markets and Richard Stephenson as US Chief Compliance Officer

- Pave suspended lending operations

- Ron Suber, president of Prosper Marketplace, announced that he was stepping down from the company

- The SEC announced that all companies will now be able to submit draft IPO registrations confidentially, a perk previously only reserved for businesses designated as “emerging growth companies” under the JOBS Act.

6/30

- PayPal Holdings Inc announced that it had invested in LendUp

- Yellowstone Capital announced that they had funded $47 million to small businesses in the month of June

7/3 – Funding Circle announced that Sean Glithero had joined the company as its new global CFO

7/5 – Lending Club appointed Ken Denman to its Board of Directors

7/6

- CAN Capital announced that they had been recapitalized and were resuming funding operations

- Orchard Platform and Experian announced a strategic collaboration on data

7/7

- CFPB announced that it was extending the deadline of its small business lending RFI from July 14th to September 14th

7/10

- China Rapid Finance announced that they had made 20 million cumulative loans since inception

- CFPB announced new arbitration rule that effectively bans class action waivers from consumer finance contracts

- Former OnDeck VP of External Affairs and Associate General Counsel Daniel Gorfine, was appointed by the Consumer Future Trading Commission to be Director of LabCFTC and Chief and Innovation Officer

7/11

- dv01 and Upgrade (Former Lending Club CEO Renaud Laplanche’s new company) announced a strategic reporting partnership

- PayPal hired former Amazon executive Mark Britto to lead its lending business

- Fora Financial expanded its credit facility led by AloStar

See previous timelines:

4/6/17 – 5/16/17

2/17/17 – 4/5/17

12/16/16 – 2/16/17

9/27/16 – 12/16/16

Funding Circle Rebrands

August 10, 2017Funding Circle is ditching their old circular logo with arrows in favor of a more modern purple logo. The website has also undergone a redesign as well.

On the new website, the company states that they are “revolutionising a broken system” and emphasize that “we believe in those made to do more.”

In a recent interview with deBanked, Sam Hodges, a co-founder and U.S. managing director of Funding Circle said, “We are focused on building a world-class technology platform that can handle millions of transactions daily and deliver a best-in-class customer experience for borrowers and investors,” Hodges told deBanked.