Industry News

Renaud Laplanche Barred From the Securities Industry

September 28, 2018

The SEC announced today that it charged LendingClub Asset Management, formerly known as LendingClub Advisors LLC (LCA), and its former president and co-founder Renaud Laplanche, with fraud – for improperly using fund money to benefit LendingClub Corporation, LCA’s parent company. LCA, Laplanche and Carrie Dolan, LCA’s former CFO, also were charged with improperly adjusting fund returns.

LCA, Laplanche and Dolan have agreed to settle the SEC’s charges against them and will pay penalties of $4 million, $200,000, and $65,000, respectively. The SEC also barred Laplanche from the securities industry for three years. LCA, Laplanche, and Dolan agreed to the entry of the SEC’s order without admitting or denying the agency’s findings.

This follows Laplanche’s ouster from LendingClub in May 2016 amid revelations of falsified loan records and conflicts of interest under Laplanche’s leadership. He is now the CEO of Upgrade, a San Francisco-based online lender, and he has been hailed recently for his resilience for making such a quick comeback.

A representative from Upgrade provided deBanked with a statement from Laplanche:

“I am pleased to have worked out a settlement with the SEC to put to rest any issues related to compliance lapses that might have occurred under my watch at Lending Club. Consistent with SEC policy, I have agreed not to admit nor deny the specific narrative of the events contained in the settlement order. I would like, however, to provide additional context:

1. To the extent there was an imbalance between 60-month and 36-month loans in one of the LCA funds as compared to its initial target, the specific 36/60-month balance was disclosed to investors every month.

2. Any manual adjustments used by the LCA team as part of the funds valuation methodology had a total net impact of 0.08% of the funds value over 5 years, and I strongly believe those adjustments were made by the LCA team in good faith.

In any event, I am glad that we can now put these issues behind us and focus on the important goals of making credit more affordable to consumers and delivering attractive returns to investors through disciplined underwriting and exciting product innovation. With the benefit of my prior experience, I feel better equipped to establish a strong culture of compliance and effective internal controls under the supervision of capable professionals.”

LendingClub, the actual company, or LendingClub Corporation, was spared any charges from the SEC because of its cooperation with the agency. The SEC press release explains below:

“The SEC’s Enforcement Division determined not to recommend charges against LendingClub Corporation, which promptly self-reported its executives’ misconduct following a review initiated by its board of directors, thoroughly remediated, and provided extraordinary cooperation with the agency’s investigation. LCA also reimbursed approximately $1 million to investors who were adversely impacted by the improperly adjusted monthly returns.”

Lending Club, which Laplanche brought public 2014, did not respond in time to questions before publication.

Three Men Indicted in $345 Million Consumer Debt Ponzi Scheme

September 26, 2018 On September 19, a federal grand jury indicted three men on charges of conspiracy, wire fraud, identity theft and money laundering in connection with a $345 million ponzi scheme, tracing back to January 2013, according to the U.S. Department of Justice.

On September 19, a federal grand jury indicted three men on charges of conspiracy, wire fraud, identity theft and money laundering in connection with a $345 million ponzi scheme, tracing back to January 2013, according to the U.S. Department of Justice.

Simultaneously, the SEC obtained a court order to shut down the ponzi scheme allegedly created by these men, Kevin B. Merrill, 53, Jay B. Ledford, 54, and Cameron Jezierski, 28. The SEC complaint alleged that these men attracted investors to their scheme by promising sizable profits from the purchase and resale of consumer debt portfolios. However, the defendants were allegedly fabricating documents and forging signatures in a complex scheme to entice investors and perpetuate the fraud.

The SEC complaint alleges that Merrill and Ledford stole at least $85 million from investors to maintain lavish lifestyles, spending millions of dollars on luxury items, including $10.2 million on at least 25 cars, $330,000 for a 7-carat diamond ring, $168,000 for a 23-carat diamond bracelet, millions of dollars on luxury homes, and $100,000 to a private fitness club.

According to a story from WBAL TV, a Baltimore-area NBC news affiliate, SEC employee Stephanie Avakian said that from one investor’s $500,000 investment, “Merrill allegedly used [it] for a $400,000 payment for a 2014 Bugatti sports car, made payments to prior investors and repaid $20,000 of his own credit card debt.”

According to the WBAL TV story, a related complaint filed by the Securities and Exchange Commission, alleges that the investors included small business owners, restaurateurs, construction contractors, retirees, doctors, lawyers, accountants, bankers, talent agents, professional athletes and financial advisers in Maryland, Washington, D.C., Northern Virginia, Las Vegas, Texas and elsewhere.

“Most of these investors are just learning that they have been victimized,” said U.S. Attorney Robert K. Hur. “The effects of this kind of fraud can be devastating. We urge anyone who thinks they may be a victim to contact the FBI at MerrillLedford@fbi.gov.”

If convicted on the criminal charges, Merrill and Ledford could face up to 262 years in prison and Jazierski could face up to 120 years in prison.

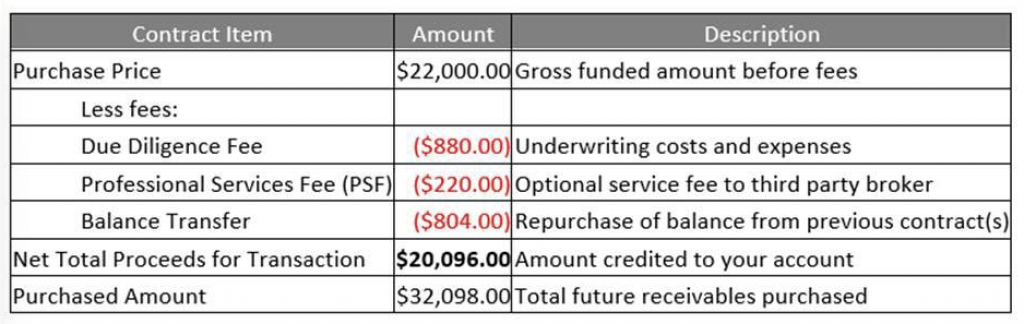

Yellowstone Capital Introduces a Smarter Box In Move Towards Transparency

September 26, 2018Yellowstone Capital CEO Isaac Stern announced a “Smarter Box” through social media channels this morning. The itemized box will be provided to merchants through a post-funding email as part of a company effort to maximize transparency.

According to the announcement:

“[We are] very serious about maximum transparency and disclosure to our funding partners’ great merchant customers. In addition to our new Purchase and Sale Agreement we will be using with each of the funding partners on our platform, we are also implementing a transaction summary email to ensure that all applicable fees, costs, disbursements and hold-backs are clearly understood by all parties. Our new contract will increase disclosure while simplifying the product, while our summary confirmation ensures greater understanding and improved communication between our funding partners and their customers.”

Example of the box:

Based in Jersey City, NJ, Yellowstone Capital has originated more than $2 billion to small businesses since inception.

RDM Capital Funding is a Sponsor of deBanked CONNECT – San Diego

September 19, 2018RDM Capital Funding is a sponsor of deBanked CONNECT San Diego. The half-day event for funders, lenders, brokers and industry professionals is being held at the Andaz on October 4th!

Check out photos from deBanked’s past CONNECT event in Miami

CAN Capital To Bring its Executive Functions Back to Kennesaw

September 18, 2018 For CAN Capital, the power is coming back to Kennesaw, GA.

For CAN Capital, the power is coming back to Kennesaw, GA.

Gary Johnson, CAN’s Executive Chairman, said “Today, CAN Capital announced it will be moving its finance and executive functions from New York to Kennesaw. The board believes this move will position CAN for increased efficiency and faster decision making as it continues to meet the growing needs of small businesses. As a result, CEO Parris Sanz and CFO Tom Davidson currently based in NY, will be transitioning out of their roles. CAN Capital recently crossed the $7 Billion milestone of providing access to capital to small businesses which includes almost $300 million over the past year. The company also secured a commitment from Varadero Capital for up to $287 million to augment its expansion initiatives and capital.”

A spokesperson from CAN confirmed that Sanz and Davidson did not want to move to the Atlanta-area headquarters for personal reasons and that the board is conducting a new search for a CEO. Sanz has been with the company since 2004, rising to the CEO position in November 2016.

Founded in 1998, CAN Capital is among the oldest alternative lending companies.

1st Global Capital’s Activities Spilled into Cryptocurrency and ICOs

September 14, 2018Curious details are emerging in the wake of the 1st Global Capital bankruptcy and subsequent SEC charges. Among them is that $161,000 of company funds were used to purchase cryptocurrency.

Many of those purchases were made in February of this year for a total of $92,492. The cryptocurrency market has slumped since then. Bitcoin, for example, is down 35%.

In May, less than three months before 1st Global filed Chapter 11, a purchase of $61,000 in cryptocurrency was addressed to TraNexus Ireland LTD. TraNeXus is an Ireland-based travel technology blockchain company that is currently raising capital via an Initial Token Offering (aka an Initial Coin Offering, ICO). “TraNexus is committed to changing the way people travel and revitalizing the travel and tourism industry by making travel easier, greener, more valuable and more fun,” the company says of itself in a recent press release. 1st Global Capital owner Carl Ruderman is something of a vanguard in the global tourism business whose acumen includes ownership of Elite Traveler magazine.

Separately, 1st Global is alleged to have funded a $40 million merchant cash advance to an auto dealership in California. Though it remains unconfirmed, industry insiders say it wasn’t even a 1st position deal and that the dealership had multiple advances.

On Wednesday of this week, the SEC served a subpoena on a JPMorgan Chase in Miami demanding all documents and payments related to 1st Global, Ruderman, and his companies.

In Anticipation of Hurricane Florence, Funders Suspend ACH Debits

September 12, 2018McLean, VA-based Breakout Capital is proactively suspending ACH debits for customers based in the counties designated by FEMA’s Major Disaster Declaration, according to an announcement made earlier today. They will be continuing to monitor the situation so that they can respond accordingly.

Gainesville, FL-based Elevate Funding is also pausing debits preemptively, the company says, for active merchants in North Carolina, South Carolina, and Georgia. After the storm, merchants can call in to report their damage or business status, they say. “Being based in Florida, exposed to many storms over the years, allows Elevate to understand how a hurricane’s damage can vary within 50 miles out to a 200 miles. Each case and customer will present different issues over the next week and some out to months.”

Chicago-based Lendr, echoed a similar plan. Company CEO Tim Roach says, “We will suspend payments for the rest of September for any client that is affected by Hurricane Florence. Most clients will come back on a reduced payment schedule for a short period of time. In the past we have provided additional funding for clients in need to help get their business back on track due to these types of natural disasters.”

Ft. Lauderdale-based Fundzio has announced that ACH payments are being suspended for businesses in South Carolina and North Carolina on Monday, Sept 17th through Friday, Sept 21st.

A State of Emergency has already been declared in North Carolina, South Carolina, Virginia, Washington DC, Maryland, and Georgia. It is currently a Category 3 Hurricane.

War on Debt Settlement Continues: 16 Defendants Sued in RICO Case

September 6, 2018

Fourteen individuals and two companies (including Decision One Debt Relief) were sued by Funding Metrics in Federal court last month for allegedly “conducting a nationwide illegal debt restructuring scheme through numerous acts of mail and wire fraud.”

The suit, which stems from the defendants’ interference with Funding Metrics’ merchant cash advance customers, makes six claims, among them financial damages resulting from state and federal crimes. Per the complaint:

“Defendant Decision One (along with its affiliate/alter ego D1 Servicing) fraudulently presents itself as being able to renegotiate and restructure merchant agreements with Plaintiff and other funding companies. It has established a deceptive business practice of making misleading and often outright false representations to merchants under contract with Plaintiff promising that, with its help, these merchants will save money on those contracts by defaulting on them. Decision One tells merchants that they can safely stop paying cash advance funding companies like Plaintiff; that it will go to work for them promptly; that it can reduce their debt by 60-80% or more; and that they will be provided with a Veritas insurance plan to cover legal expenses arising from their defaults, once cash advance companies exercise their rights under agreements with their merchants, as they inevitably will. Based on these misrepresentations, the merchants default on their contracts with their funders – that is, at Decision One’s direction, they stop paying their funders and instead pay Decision One – although Decision One does not even expect to achieve results for the merchants. The result is a fraud on the merchants and tortious interference with the contracts Plaintiff have with them.”

The suit is just the latest bomb dropped on the exploding debt settlement industry. deBanked began covering the controversy surrounding debt settlement in late 2016 after the owner and employees of an upstate New York debt settlement company were arrested for charging merchants to restructure their merchant cash advances and then not actually performing any services. The owner, Sergiy Bezrukov, was charged with money laundering, bank fraud, mail fraud, wire fraud and conspiracy to defraud. Bezrukov has been locked away in jail for almost two years awaiting trial. He is facing a maximum of 30 years. Two of his employees pled guilty, Vanessa Cardona to bank fraud and Dustin Walker to conspiracy to commit bank fraud.

Since then, nearly a dozen major lawsuits have been filed by merchant cash advance companies against other debt settlement companies that are alleged to be carrying out similar schemes. One of those sued companies, NJ-based Corporate Bailout LLC, was featured on the cover of the New York Post last summer for being “the craziest office in America.” Corporate Bailout was sued by both Yellowstone Capital and Everest Business Funding which later resulted in a very public settlement agreement that forced Corporate Bailout to fork over $500,000 to the two MCA companies.

Decision One Debt Relief, sued now by Funding Metrics, was also originally a co-defendant alongside MCA Helpline in a lawsuit filed by Everest Business Funding earlier this year. In February, after determining the two were not related, Everest dropped the claims against Decision One only. The suit against MCA Helpline is still pending.

Around that same time, a representative for Decision One revealed to deBanked that the company was on track to be doing more than $100 million a year in business.

Bezrukov, by contrast, who currently resides in a Niagara County New York jail, is accused of having only obtained $1.2 million throughout his entire debt settlement venture’s existence. Although Decision One is not being charged criminally, the private civil suit alleges damages caused by a violation of criminal statutes including RICO.

The Funding Metrics suit against Decision One was filed in the Southern District of Florida under ID# 9:18-cv-81061.