Economy

Funding Circle Report Shows Demand for Alternative Financing

June 14, 2018

Funding Circle, together with Oxford Economics, released a report this week using data from its customers last year. Funding Circle is a business loan platform that matches small business borrowers with investors that want to lend. Some of these findings may be reflective of the broader alternative finance market.

Data from the report conveys that there is an increased appetite among small business merchants for online lending products. Of the small business customers surveyed, 70 percent did not attempt to get a bank loan before applying for an alternative loan from the Funding Circle platform. The main reason for this, cited by more than three-quarters of these customers, was a perception that the bank loan process would be too burdensome. Another nine percent skipped banks because they said they thought they would be rejected.

Of the businesses that had first approached a bank before seeking funding from Funding Circle, 50 percent said they didn’t obtain a bank loan because their application was rejected. Another 36 percent responded that the bank loan process took too long, and seven percent felt that the bank’s rates and fees were too high.

When asked about the impact of not receiving funding through Funding Circle (or we can imagine a different online funder), the most common response, given by 27 percent of respondents, was that they would have missed an opportunity. After this, 22 percent believed they would not be able to consolidate their debt and 16 percent thought that they would not have been able to achieve profit growth.

Loan volume in the U.S. rose significantly for Funding Circle last year. A total of $509 million in new loans were issued in the U.S. in 2017, an increase of 80 percent from $281 million issued the previous year.

“It has become evident that small businesses are underserved in every country we operate,” said Funding Circle co-founder and CEO Samir Desai. “From butchers and bakers, to IT consultants and accountants, these are the businesses that are creating jobs, boosting productivity and driving our economies forward. The economic impact that these businesses have had as a result of accessing finance through Funding Circle is hugely rewarding to see.”

Founded in 2010, Funding Circle has helped 40,000 small businesses find financing. The company operates in the U.S., U.K., Germany and the Netherlands.

Student, Auto Loan Delinquencies Rise Slow and Steady, Report Says

July 7, 2016Is there reason for concern?

A Morningstar report on debt shows rising delinquencies in student loans and auto loans. While the rate for student loans more than 90 days past due declined to 11.0 percent in the first quarter, from 11.5 percent in the fourth quarter 2015, it has been rising since the end of 2011 when delinquencies were 8.5 percent

This corresponds with the increase in student enrollment at for-profit colleges that target lower income groups with the lure of higher paying jobs. Enrollment in these institutions have quadrupled since 2000 and a study revealed that 70 percent of the students who defaulted on their loans in 2013 went to for-profit educational institutions.

In 2014, 47 percent of students at these institutions defaulted on their loan, compared to 38 percent who went to two-year institutions and 27 percent who did the traditional four-year courses.

Auto loans

The report also warns of rising delinquencies in auto loans propelled by an increase in subprime lending.

The rising competition among lenders lending to millennial borrowers with thin files has led to the uptick in subprime auto loans. Experian reported a 10.9 percent year-over-year increase in the balance of subprime auto loans and leases held by consumers in the first quarter of 2016

Auto delinquencies have crept higher, with the rate of loans more than 90 days late reaching 3.5 percent in the first quarter, up from 3.4 percent in the prior quarter.

“For student and auto loans, it’s important to keep the eyes on the road and watched as these are vulnerable to subprime lending with rising delinquencies,” said Stephanie Mah, director of research at Morningstar and author of this report. “Even though the pace of student-loan delinquencies slowed in the previous quarter, they remain at near record levels..”

As Credit Tightens, Borrowers and Investors Retreat Alike

July 5, 2016 America’s bond market is drying up.

America’s bond market is drying up.

The value of bonds packaged with personal, corporate and real-estate loans fell by $98 billion, a 37 percent decline from the first half of 2015 making it tough for businesses to refinance their debt.

Lenders have for long relied on securitization for capital but as the credit market tightens, companies will be forced to diversify and soon.

There are currently more than $10 trillion in outstanding securities backed by personal, business and other loans, according to the Securities Industry and Financial Markets Association, the Wall Street Journal said.

And it’s not just investors who are retreating. A recent study found that small businesses are hesitant to borrow and rely on personal resources to meet their business’ capital needs. Demand from businesses with revenues of less than $5 million shrunk 15 percent from Q1 2016 to Q2 2016, from 38 percent to 32 percent.

The survey also noted that a third of business owners that responded transferred personal assets like savings and personal credit cards to their business accounts in the last quarter.

“Business borrowing habits suggest owners may not see a need for an immediate infusion of capital,” said Dr. Craig R. Everett, assistant professor of finance and director of the Pepperdine Private Capital Markets Project. “However, these findings suggest business owners are still feeling the lasting impact of the recent recession and remain skittish about the future, as reflected in an abundance of caution when it comes to the economic environment.”

Business owners are being tightfisted with borrowing, instead using earnings and profits for capital expenditure.

“There are far fewer small businesses taking a loan, as they don’t see opportunity for expansion,” said Holly Wade, director of research and policy analysis at NFIB, a small business trade association. “Some are uncertain about the future so they don’t want to take out a loan and in some instances, owners have a more difficult time finding desired loans.”

Don’t Look Now, But The US Treasury is Staring At Marketplace Lending

June 24, 2016 The US Department of Treasury is concerned about marketplace lending. Again.

The US Department of Treasury is concerned about marketplace lending. Again.

The Financial Stability Oversight Council which was established per Dodd Frank to monitor excess risks to the financial system by bank and nonbank financial entities categorized marketplace lending as one in its annual report.

Concerned by the quick proliferation of nonbank lenders, the FSOC said that new financial products, its delivery mechanism and the business practices involved although contribute to “efficient” financial intermediation, the technology-backed underwriting models pose credit risk.

“Marketplace lending is an emerging way to extend credit using algorithmic underwriting which has not been tested during a business cycle, so there is a risk that marketplace loan investors may prove to be less willing than other types of creditors to fund new lending during times of stress,” the report said, worrying about the possible erosion of lending standards.

The Treasury however recognizes that the threat is still moderate but is still cautious.

“Financial regulators will need to continue to be vigilant in monitoring new and rapidly growing financial products and business practices, even if those products and practices are relatively nascent and may not constitute a current risk to financial stability.”

This is not the first time marketplace lending industry has garnered attention from authorities. Last month, (May 10th) the Treasury released a white paper titled “Opportunities and Challenges in Online Marketplace Lending” listing the risks associated with data and modeling techniques and the new data model being untested through a complete credit cycle.

The CFPB is also turning its attention towards small business lenders. Bloomberg reported that the agency wants to collect credit data in small business lending.

However, there are some who believe that regulating the lending industry cannot have a one-size-fits-all solution, nor does it need one. Thomas Weinberger, partner at Schulte Roth and Zapel is less inclined to believe that this will affect different market segments. “Marketplace lending has a self correcting system where if default rates go up, investors won’t buy,” he said. “The discipline is enforced by the capital.”

Taking Stock of China’s Changing Fortunes in Fintech

June 21, 2016

It’s been called the Wild West of the financial world, and it appears the sheriff is finally headed to town.

Chinese fintech, the P2P practice of connecting borrowers to lenders via the Internet, was supposed to bring much-needed competition and efficiency to the country’s outsized, government-run banking system, turning a sizable profit for a visionary group of investors in the bargain. Investors weren’t the only ones that stood to benefit from the boom. With large Chinese banks choosing to lend primarily to mammoth, state-owned corporations, the country’s small business community was similarly poised to profit.

That’s exactly how it played out for a while. Buoyed by bullish expectations, fintech startups with good marketing skills attracted large numbers of investors. This resulted in nearly a decade’s worth of easily amassed capital, dizzying returns in high interest rate bearing vehicles, and little in the way of meaningful regulation. Before you could say “Alibaba”, roughly one fifth of the world’s largest fintech firms hailed from China, with ZhongAn, an online insurance group backed by the e-commerce titan’s founder, Jack Ma, topping the list.

It was indeed the Wild West, but there was trouble on the horizon.

The twin villains irrational exuberance and negligent oversight eventually flipped the script, and China’s fintech sector has been reeling ever since. Returns derived from investing “captive capital” into funds that returned high spreads started drying up. Payment companies came under fire for questionable practices that at least one investment research firm, J Capital Research, likened to a Ponzi scheme. Doubt set in, followed by panic. Capital began flowing out of the country instead of into it, with investors that could head for the exit door doing just that.

By the end of 2015, nearly a third of all Chinese fintech lenders were in serious trouble, according to a recent article in the Economist, “trouble” being defined as everything from falling returns to halted operations to frozen withdrawals.

A few brave souls stuck to their guns, wrangling over how to make their finance models more sustainable for the long haul. Other so-called industry leaders simply skipped town. Literally. Enter “runaway bosses” into your preferred web search engine and the hits keep coming. According to the same Economist article, the delinquent bosses of some 266 fintech firms have fled over the past six months alone. It’s a worrying trend that pessimists say represents yet another nail in the coffin of China’s so called “Era of Capital.”

I wouldn’t be so sure.

Emerging trends will always be susceptible to periods of protracted volatility. It’s how industry leaders – and government officials – respond to such crises that lays the groundwork for what happens next. Now, the “maturation” process has begun in China. Unfortunately, to date it’s happened exclusively in the form of mass consolidation, with the state sector swooping in and taking over what was up until now a strictly private sector trend.

The Chinese government’s fondness for consolidating its interests is no state secret of course, but it would be a mistake for it to use the failings of the fintech sector to reassert the dominance of the country’s state-owned banking sector. The reason for this is straightforward enough. Big banks aren’t usually the biggest allies of small business, and every economy needs a robust small business sector in order to thrive.

Where could the Chinese government look for guidance? Not the US, unfortunately. If anything, the fintech market in America suffers from too much regulation. Everyone knows there’s no friendlier country on the planet for budding entrepreneurs than the US, and you certainly don’t have to look far to find examples of fast-growing American fintech success stories. You could go so far as to argue “disruptive innovation” in the financial sector is in our DNA, from the rise of Western Union to the emergence of giant credit card companies like Visa and Mastercard to the recent arrival of game changers like Lending Club, OnDeck and Venmo.

And yet, ask any fintech startup CEO about the thicket of regulation he or she has to routinely navigate in order to figure out which agencies have jurisdiction over, or which laws apply to, the various aspects of their businesses. Better yet, don’t. The alphabet soup of regulatory bodies they will be obliged to list – the SEC, the Fed, FINRA, OCC, FDIC, NCUA, CFPB, etc. – will put you both to sleep. The point is that these days the US lags behind other regions of the world in creating the environment the fintech industry needs to flourish. (One discouraging example: In the United States, the licenses needed to become a money services business (MSB) have to be acquired on a state-by-state basis; in the European Union, a single license is all it takes to do business in Berlin, Paris, Madrid, and Rome.)

Making finance safer is one thing, but blinding business with an unusually harsh regulatory spotlight isn’t the answer.

Why does it matter if the fintech sector goes belly up in China, the US, or anyplace else? To reiterate: Fintech isn’t some passing trend or get-rich-quick scheme. It’s one of the essential engines that drives small business development. According to the site VentureBeat.com, the World Economic Forum recently reported that a healthy fintech industry could close a $2 trillion funding gap for small businesses globally. You could drive a healthy uptick in the global GWP through a gap that size.

This brings us back to China. Chinese regulators may be tempted to capitalize on the country’s fintech troubles to reassert their influence, but they should strongly resist the urge. Instead, they might focus their efforts on taking steps to create a healthy ecosystem for the country’s fintech sector, one with regulatory controls that are clear, efficient, and properly implemented. Transparency will be key. One of the things American fintech companies do right is publishing essential information about those seeking loans, including their credit history, employment status, and income. This is to ensure that the investors putting up the money know what they’re getting into. It’s a critical confidence-builder, and China’s fin-tech model will need to be similarly transparent if it wants to succeed.

I happen to believe that it will succeed, and that it will continue to attract big money. The case could be made that it’s already happening. In December 2015, Yirendai, the consumer arm of P2P lender CreditEase, became the first Chinese fintech firm to go public on an overseas exchange, listing on the NYSE with a valuation of around $585 million. In January of this year, Lufax, a platform for a range of products, including P2P loans, completed a fundraising round that valued the company at $18.5 billion, setting the stage for a highly anticipated IPO.

Both companies pride themselves on their transparency protocols and risk controls.

The bottom line is this: No financial sector benefits from descending too far into a Wild West of laissez-faire everything, and China’s regulators were right to ride to the rescue. They would do equally well not to strong arm the sector’s brightest leaders. The country should strive to create a safe, healthy environment for third-party service providers to prosper and grow. If they do, it won’t just be investors in mobile transactions and digital currencies who benefit.

China’s entire economy will.

Consumer Credit Defaults Are Falling, But Don’t Celebrate Yet

June 21, 2016Waiting for some good news? Here’s half an attempt.

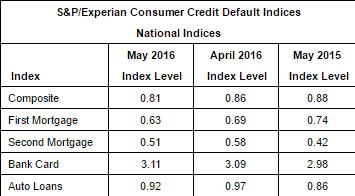

The S&P Dow Jones and Experian Consumer Credit Default Indices, which measures consumer default rates fell to 0.81 percent in May, down five basis points from April. The index measures comprehensive changes in consumer default rates — broken down into mortgage, auto loans and bank cards.

While this is some respite, all but bank card defaults fell in May. The bank card default rate however increased two basis points in May to 3.11 percent

The bank card default rate however increased two basis points in May to 3.11 percent

Among the cities that contributed the most, New York led with a 12 basis points drop to a default rate of 0.89 percent, followed by Dallas where rates fell by seven basis points to 0.69 percent. Chicago’s default rate fell by five basis points to 0.98 percent and Los Angeles came in fourth recording a default rate of 0.67 percent, down four basis points. Conversely, Miami’s default rates edged up higher ( six basis points) for the third consecutive month at 1.27 percent.

“Overall the consumers’ credit picture is very good,” says David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices. “Consumer credit default rates continue at the lowest levels in more than 10 years and well below those seen before the financial crisis.”

Is this silence before a storm?

As Mortgage Applications Slow Down, is it Smarter to Rent?

June 1, 2016It turns out those who rent might be smarter, after all. Applications for refinancing mortgages and new home purchases fell 4 percent from the previous week, according to Mortgage Bankers Association.

As home prices rise and the anticipation around Fed raising rates builds, it will only lead to loans getting more expensive. As such, refinance applications decreased 4 percent, seasonally adjusted, and purchase applications decreased 5 percent and applications for government loans fell 6 percent. The average loan size on refinances also dropped for three straight weeks.

“House prices have breached the peak levels of 2006, raising concerns about the long-term sustainability of current price levels,” Sean Becketti, chief economist at Freddie Mac, wrote in a report on the housing market.

This doesn’t bode well for lenders like SoFi which is trying to make a big headway into mortgage refinancing. “While we launched our mortgage business focused on larger ‘jumbo’ loans, the certainty and efficiency offered by Fannie Mae will enable us to serve more members by expanding geographically and into smaller loan amounts,” Michael Tannenbaum, VP of Mortgage at SoFi said when the lender became a Fannie Mae seller.

Is That a Bird, a Plane or a Recession in the Wings?

April 26, 2016

The R-word has been rearing its ugly head with more frequency in recent months, propelled by falling stock prices, higher borrowing rates and the dollar’s ascent.

While a recession—typically defined as a fall in GDP in two consecutive quarters—is far from certain, it would most definitely be a double whammy for an industry that many believe is already ripe for a pullback due to multiple years of unfettered growth. Indeed, many funders have experienced great success riding on the coattails of the long-running favorable market. Some industry participants fear these funders are masking loss rates behind strong volume—a particularly problematic strategy if the volume were to taper off due to an economic downturn.

“It’s no different than what happened in the housing market in 2008,” says Andrew Reiser, chairman and chief executive of Strategic Funding Source Inc. in New York. If and when a recession occurs, several industry participants expect there will be a culling of the weakest firms. They say inexperienced and less-diverse funding companies are particularly at risk, as are MCA funders that don’t keep close tabs on their business dealings. They also believe that venture capital funding will be even harder to come by and regulation will rain down more heavily on the industry.

RISK FACTORS THAT SPELL TROUBLE IN RECESSIONARY ENVIRONMENT

For a variety of reasons, Glenn Goldman, chief executive of Credibly, a New York-based small business lending platform, believes that fewer than 50 percent of the funders today are prepared to weather a recession. Many don’t have strong data science and risk management, for example. Some newer platforms also don’t have the seasoned management to help guide them appropriately, he says.

Another red flag is when funders rely too heavily on a single source of funding. Goldman points back to 2008 when the commercial paper market disappeared. Companies that had on balance-sheet funding capacity were able to weather that storm because they weren’t exclusively relying on commercial paper or securitization, he says.

Goldman believes the prudent way to manage an alternative funding business is to utilize a combination of on-balance sheet financing, whole loan sales and securitization. “If the market moves sideways and you rely only on a single source of funding, you are at risk. It’s an incredibly obvious statement, but it becomes more acute when the economic environment comes under pressure,” he says.

Notably, there are very few sizable alternative funders who successfully survived the last big recession, meaning there are hundreds of companies now doing business in this space that don’t have years-worth of data to help them make more prudent underwriting decisions. Strategic Funding, for example, had the highest loss rate in its history in the third quarter of 2008 and has used its wealth of data to learn from past mistakes. “There’s no doubt that it is critical to be able to correlate events with history,” Reiser says.

Funders are also going to have to batten down the hatches when it comes to their underwriting standards. “Just because someone paid you back yesterday doesn’t mean he’s going to pay you back tomorrow,” Reiser says. “You have to be right more often in a recessionary environment.” Indeed, liquidity for originators and investors will become even more critical in a recession.

“Liquidity is king,” says David Snitkof, chief analytics officer and co-founder of Orchard Platform, a New York-based technology and data provider for marketplace lending. He points out the large number of companies that went belly-up in the last big recession for lack of liquidity. “The more that participants in this market are able to diversify their capital structure, diversify their funding sources and work with multiple providers, the better off they will be,” he says.

Another challenge will be for funders that haven’t had their servicing and collection capabilities adequately stress tested, Snitkof says. These firms should consider working with an outside provider to help them scale their collections as necessary. In this way, a company that needs additional resources can scale up pretty quickly without disrupting operations.

THE P2P OUTLOOK

To be sure, all types of companies fall under the alternative funding umbrella and each will have its own special challenges in a recession. In the P2P space, for example, having a diverse investor base and a sound credit model will become increasingly important. Peter Renton, an investor and founder of Lend Academy, an educational resource for the peer-to-peer lending industry, predicts that some of the newer P2P platforms will struggle more in a recession. That’s because they haven’t had as much time to accumulate and interpret borrower data and adapt their models accordingly.

To be sure, all types of companies fall under the alternative funding umbrella and each will have its own special challenges in a recession. In the P2P space, for example, having a diverse investor base and a sound credit model will become increasingly important. Peter Renton, an investor and founder of Lend Academy, an educational resource for the peer-to-peer lending industry, predicts that some of the newer P2P platforms will struggle more in a recession. That’s because they haven’t had as much time to accumulate and interpret borrower data and adapt their models accordingly.

Lending Club, for example, has gone through many iterations of its credit model over its multiple years in business, and it’s much better than it was even five years ago, says Renton, who had around $37,000 invested with Lending Club as of the third quarter of 2015. “The best data that anyone can get is payment history with your existing borrowing base,” he says.

Particularly in a recession, P2P players need to be extra careful about maintaining strict underwriting standards. Marketplaces may have to tighten their borrowing standards to lend to more solid companies, so the likelihood of defaults isn’t as great. So, for instance, if their standard was once borrowers with a FICO score of at least 640, they could up it to 660, Renton says.

Platforms also have to make sure they have enough investors to satisfy their borrowers, which is why having a diverse investor base is so important. In a recession if you have three hedge funds and that’s your entire investor base, they could all go away. By contrast, if a platform has five thousand individual investors, they aren’t all going away. You may lose 10 percent or 20 percent of them, but if you still have four thousand investors, you can still have your loans funded, Renton explains.

One way to do well even in a recessionary environment is for P2P players to tweak their credit model to be more restrictive so their default rates are lower. “If your default rates are only 3 percent and your competitors are at 6 percent, you’re going to get more business,” Renton says.

Certainly, alternative funding companies can get into trouble if they don’t act early enough when they see a change in activity and economic performance, says Ron Suber, president of Prosper Marketplace, a P2P lender based in San Francisco. Funders need to be able to nimbly adjust their pricing, risk models and expected default rates as needed. “Every marketplace will see a change in borrower behavior as unemployment increases and there are economic declines. Therein lies the question: what does the marketplace do?” Prosper, for instance, recently raised rates on loans, telling investors it had increased its estimated loan loss rates and therefore was updating the price of loans to reflect increased risk. Understanding risk and pricing loans accordingly is always important, but even more so in a shaky economic environment. “You always have to stay on top of it,” Suber says.

MANY MCA FUNDERS AT HIGH-RISK IN RECESSION

MANY MCA FUNDERS AT HIGH-RISK IN RECESSION

If a recession strikes, some observers believe the risk to certain MCA funders will be particularly acute. That’s because new players have entered the MCA space over the past several years, and a sizable number of them don’t have a good handle on their business. Higher default rates could force many of them to shutter operations. Certainly merchants especially those with bad credit—will need more access to capital during a recession and MCA is a natural place for these businesses to turn. But MCA funders have to do a better job of adjusting for risk and keeping adequate records if they hope to weather an economic downturn, says Yoel Wagschal, a certified public accountant in Monroe, New York, who has worked with a number of struggling MCA funders. “A small recession could lead to big failures if you don’t take the right steps,” he says.

To avoid business-threatening issues, Wagschal recommends that MCA funders take steps now to develop stronger underwriting systems to vet merchants better. He believes it’s more prudent to do fewer deals with higher rated merchants than to continue taking on risky businesses as customers. If they see more defaults are coming in, funders should also consider raising their factor rates, he says. Another option is to halt new funding for three to four months to re-energize the business. “It’s much harder to make money than to lose money,” he notes.

If they don’t already have them—and many don’t—MCA funders also need to invest in a good accounting system that can flag their profits, losses and defaults on a real-time basis. This information allows funders to make swift decisions about the business so they can take necessary steps at the right time, he says. “You don’t wait for months, or year end, to analyze all the facts. You might have already lost your business and lost your money because money is just turning around so quickly.”

UNCERTAINTY ABOUNDS FOR VENTURE CAPITAL INVESTMENT

Existing funders won’t be the only ones to struggle in a recession; the well of venture capital funding for new entrants could easily dry up as well,like it did in the last big recession. That’s not to say VC firms will lose interest entirely, but new funders will have to work even harder to get noticed. “There are so many originators, for any new entrants, the bar gets higher and higher to prove that you have something truly unique,” says Snitkof of Orchard Platform. Reiser of Strategic Funding already sees this scenario playing out. “I don’t think the market [lately] has been very favorable to our space,” he says, noting the dearth of exit strategies that have made it riskier for VC firms to invest. “It’s always easy to get in; it’s hard to get out,” he says.

GET READY FOR MORE REGULATORY ACTION

Industry watchers also believe the alternative funding industry will become more heavily regulated in a recession and its aftermath.

Reiser points to all the additional restrictions placed on the mortgage industry in the wake of the housing market bust in 2008. At a time when the housing market was restricting, you had more compliance placed on it as well. “I think you’ll have more compliance in our industry too. That’s just another cost that will have to be absorbed,” Reiser says.

In a recession, there’s more likelihood that harm can come to customers and that will drive regulatory action as well, he adds.

THE ART OF MAKING TOUGH DECISIONS

If the economy turns south, many alternative funders will be forced to make tough underwriting decisions. It can be hard if your analysis of data tells you that things are going to turn downward and your competitors don’t take the same stance, says Stephen Sheinbaum, founder of Bizfi, a New York-based online marketplace.

In that case, funders have to decide whether they are willing “to tighten and pivot while the rest of the players in the space are going full steam ahead,” he says. “That’s where you have to have some conviction and trust your data and do the right thing.”

Of course, even as the rest of the economy is faltering, recessionary times can also be a boon for enterprising companies. For example, the 2008 recession turned out to be positive for Bizfi, which at the time was called Merchant Cash and Capital. Using housing starts, consumer spending and other data, the company correctly predicted the economy was going to take a severe turn downward. It therefore made tweaks to its underwriting guidelines, moving into certain industries and away from others it deemed riskier. “Change can be hard, but it can be for the better,” Sheinbaum says.

Indeed, alternative funders that embrace new opportunities can be successful even in a broad economic downturn. “It’s about having the foresight to be able to discern good from bad and just being really disciplined about it,” says Snitkof of Orchard Platform.