Economy

Small Business Funders Are Hiring, But Does Anyone Want the Jobs?

September 28, 2021 As the small business finance market gets back to normalcy, the industry’s latest challenge is filling all of the open positions. Jobs that would once attract hundreds of resumés are now ending up with very few, if any at all.

As the small business finance market gets back to normalcy, the industry’s latest challenge is filling all of the open positions. Jobs that would once attract hundreds of resumés are now ending up with very few, if any at all.

Even after pursuing LinkedIn, the applicant pool just looks light.

In our research, deBanked found five fintech companies on LinkedIn that have ads that are at-least a week old with three or less applicants.

One company based on Long Island, promoted a $5,000 signing bonus for an underwriting position and only had five applicants. Meanwhile, a self-acclaimed “prestigious” Manhattan lender even has a month-old ad posted that offers a $10,000 per month salary. That job has one active applicant, according to LinkedIn.

Chad Carter, Director of Franchise Success at Lendio, says the hiring process has been difficult, but isn’t impossible to navigate. “Being based in Utah has been somewhat challenging as unemployment is extremely low and the Silicon Slopes area has a lot of tech headhunting,” said Carter. “We’ve hired and are hiring hundreds more people this year so we feel it too. Luckily we have extremely good reviews on Glassdoor, which helps keep applications coming and our culture keeps them here.”

Some companies have gotten creative when it comes to building their staff to counter the lack of applicants in the workforce. “We have seen some open roles have more interest than others,” said James Webster, CEO of ROK Financial. He says his company has been able to expand hiring by offering remote sales positions that opens the applicant pool nationwide.

Some companies have gotten creative when it comes to building their staff to counter the lack of applicants in the workforce. “We have seen some open roles have more interest than others,” said James Webster, CEO of ROK Financial. He says his company has been able to expand hiring by offering remote sales positions that opens the applicant pool nationwide.

“We have been hiring and building an outside sales division known internally as the Remote Sales Division,” Webster said.

He claims the number of applicants for remote sales positions have been high, but that doesn’t mean his company is hiring a ton of staff to add to the program. “We are still extremely selective on who we allow onto the platform as they represent ROK in the market,” said Webster.

“All in all, recruiting is harder now than it has been in previous years,” Webster said. “Especially when the culture in the office is such a priority to maintain.” He noted that the roles that are currently difficult to fill are mostly administrative positions, not sales.

A recruiter for a large finance-centric company that wishes to stay anonymous told deBanked that the finance industry in general is having hiring troubles, not just fintech. “There’s tons of turnover all around,” said the recruiter, who claims that they themselves are actively being poached by other companies due to the lack of people wanting to work.

“I can only assume that fintech is just as crazy,” the recruiter said.

Earnings Week: PayPal

February 3, 2021PayPal held their earnings results for Q4, describing its strongest year in history by chief executive Dan Schulman.

In Q4 alone, PayPal added 16 million net new million active customers and 1.4 million new merchants and raised $6 billion in revenue. That brings the total to 377 million new users for the entire year.

After adding cryptocurrency to the platform, Schulman said that users that bought virtual assets log in twice as frequently as they did before.

“We have seen an exceptional response to pour crypto launch,” Schulmann said. “The crypto volume traded on our platform greatly exceeded our projections.”

The payments by-now-pay-later product added raised $750 million in the last quarter.

The Pain in America’s Food Supply Chain

January 29, 2021 It was last November, Mark Mavilia says, when he and three friends in Washington, D.C. rendezvoused for dinner at Ghibellina’s, an Italian gastropub in Logan Circle “specializing in Neapolitan-inspired pizzas and craft cocktails,” says the online restaurant guide “Popville.”

It was last November, Mark Mavilia says, when he and three friends in Washington, D.C. rendezvoused for dinner at Ghibellina’s, an Italian gastropub in Logan Circle “specializing in Neapolitan-inspired pizzas and craft cocktails,” says the online restaurant guide “Popville.”

Hold the pizza! Mavilia, who is art director at the Association of American Medical Colleges, couldn’t wait to tuck into the pasta-bolognese, his favorite dish. “In my opinion,” he says, “it’s the best in the city.”

Or rather was the best. When the foursome assembled outside the restaurant, they were disappointed to find Ghibellina’s had closed. “They had shut down for good,” Mavilia says, adding: “It was not boarded up. Just a note on the door thanking patrons for their support. I will surely miss the bolognese.”

The Ghibellina brand was later consolidated into a sister restaurant called Via in Ivy City.

Mavilia’s experience in Washington is typical of a nationwide phenomenon. Tens of thousands of restaurants and bars and eateries of every kind have closed their doors as the Covid-19 pandemic has ravaged the country and Americans have sharply limited their social interactions. As U.S. fatalities surpassed 410,000 in January, the economic damage to the restaurant and bar businesses has been staggering.

“Washingtonian” magazine keeps a running tab of restaurants that have closed their doors in and around the nation’s capital owing to the pandemic. In December, its tally listed 75 casualties in The District alone, including such icons as the Post Pub and Montmartre, Momofuku and Tosca, plus many more in the Maryland and Northern Virginia suburbs.

“Washingtonian” magazine keeps a running tab of restaurants that have closed their doors in and around the nation’s capital owing to the pandemic. In December, its tally listed 75 casualties in The District alone, including such icons as the Post Pub and Montmartre, Momofuku and Tosca, plus many more in the Maryland and Northern Virginia suburbs.

The area around the White House dominated by the influential K Street law firms and lobbyists, and the World Bank and International Monetary Fund has been nearly barren. With few people trickling into the central city, says Madeleine Watkins, owner of 202strong, a fitness club featuring personal trainers, her business is getting battered. Receipts are off by 80% over last year and she sees the effects all around her.

“There are definitely a lot of restaurants closed, but I’m hoping and praying that lot of it is temporary,” she says. “We need people to come downtown for Washington to be a vibrant and bustling city with coffee shops, restaurants, and sandwich shops.”

One hopeful sign: Tosca, a white-tablecloth restaurant near Metro Center which boasts an enthusiastic, upscale audience and earns 4.8 stars from customer reviews, promises to re-open in the spring. “This was my go-to Italian restaurant near my office,” declares Deborah Meshulam, a partner at multinational law firm DLA Piper and a former lead trial counsel at the Securities & Exchange Commission. “I loved their grilled Branzino and pretty much anything else they made.”

The Minneapolis Star-Tribune recently counted 94 restaurants that had closed down permanently in the Twin Cities. “Saying goodbye to a beloved watering hole, a neighborhood café or a four-star restaurant is never easy,” reporter Sharyn Jackson wrote in late December. “But in 2020, the pain kept coming as the pandemic brutalized the Twin Cities hospitality industry.”

Among the notable casualties, were Bachelor Farmer, Muddy Waters, and Fig+Farro.

Angharad Bhardwaj, communications manager at medical technology company GenesisCare and a lifeling Minnesotan, told deBanked of her sorrow at learning that Fig+Farro had closed. “My husband and I were there for their opening, and I am so sad to see it close,” she says. “This was one of our favorite restaurants, just steps away from our condo in Uptown. We spent our first Valentine’s Day there. It was fresh vegan food. We even sat with the owner’s children one night. The little boy was helping his parents with the restaurant, taking orders.”

In Denver, online entertainment publication “Do303” recently highlighted closures of 15 area restaurants it called “the great ones that kept our hearts and bellies full for years.” Notable among the cohort was El Chapultepec, 12@Madison, and Biju’s Little Curry Shop. Michelle Parker, a Denverite who has a short commute to suburban Westminster where she is the City Clerk, says: “The feeling around town is that this has been a big loss to neighborhoods and to the food scene, which was just coming into its own as the pandemic hit.”

Nationwide, more than 110,000 restaurants, bars and food-service establishments have closed their doors, reports the National Restaurant Association, the premier Washington-based trade group representing the food-service industry. The membership includes not only restaurants, pubs and cafes but non-commercial restaurant services, cafeterias, institutions like college cafeterias, and even food services at military installations.

Nationwide, more than 110,000 restaurants, bars and food-service establishments have closed their doors, reports the National Restaurant Association, the premier Washington-based trade group representing the food-service industry. The membership includes not only restaurants, pubs and cafes but non-commercial restaurant services, cafeterias, institutions like college cafeterias, and even food services at military installations.

The food-service industry is the nation’s second largest private employer and accounts for $2.1 trillion in economic activity, reports Vanessa Sink, director of media relations at the trade group. On average, when a restaurant closes, fewer than 50 people find themselves unemployed, but it adds up. As many as eight million food-service workers – waiters and bartenders, hosts and hostesses, cashiers, general managers and dishwashers, parking valets and cooks and chefs — were out of a job at the height of the pandemic in early 2020.

Curtis Dubay, senior economist at the U.S. Chamber of Commerce in Washington, D.C., notes that a whole array of food-service jobs are interwoven into the fabric of the U.S. economy. “Anything that involves large gatherings – transportation, travel and tourism, athletic events, the theater, the hospitality industry,” he says. “In places like The Hyatt in Orlando, food-service workers are involved in setting up a ballroom for conventions and small meetings. It’s a big part of the economy.”

Since the spring, many of the lost jobs came back as restaurants were able to add take-out and delivery services. Many states and localities allowed restaurants to re-open with outdoor-seating, limited occupancy, customer-spacing, and Plexiglas booths. Through the end of November, 2020, 75% of the lost jobs were recovered but 2.1 million food-service jobs had still vaporized.

As more and more people prepare their own meals at home, the switch from dining-in to curbside and takeout services has met with limited success. For take-out people are more likely to order fast-food from Chick-fil-A or Pizza Hut and Domino’s rather than something fancy. “Who wants to spend $60 for a meal you have to eat out of a cardboard container,” one Minneapolis woman complained to deBanked.

Restaurant closures, meanwhile, are having devastating consequences across a broad swath of society. “When a restaurant closes or has to cut back, it not only impacts the economy of the local community, it also affects the culture of the community,” says Sarah Crozier, communications director at Main Street Alliance, a 30,000-member, small-business advocacy group headquartered in Washington, D.C. “Local, independent places are where we create our memories as cities and towns. From losing the cries of “Keep Austin Weird” to stripping away the innovative recipes coming out of Raleigh, N.C., it deeply scars the culture and feeling of a place when we have only chain restaurants to fall back on.”

Adds Sink: “Restaurants are the cornerstone of communities. You often find that neighborhoods and local economies have built up around a restaurant. Restaurants provide jobs, they pay rent and contribute to the tax base. Other businesses will grow up around them. People will go to a restaurant – and then they’ll go next-door to shop.”

Food-service establishments are also long-term tenants. The “vast majority” of the closures, Sink asserts, have involved restaurants that had been in business for more than 16 years. Roughly one in six had been in operation for 30 years or more.

Backlit downtown restaurants with inviting awnings, valet parking and limousines idling out front are giving way to boarded-up buildings, many battened down with battleship-gray steel shutters. “I’ve been talking to mayors about empty storefronts and the effects of business failures,” says Karen Mills, former administrator at the U.S. Small Business Administration and a senior fellow at Harvard Business School, says. “It’s significant. It devastates the whole community and brings down the whole environment. People don’t want to go downtown to Main Street anymore.”

Many cities and towns have invested heavily to revitalize their inner cities and urban areas around restaurants and bars to add sparkle to the nightlife and draw visitors and tourists. The economic development strategies often commingle trendy restaurants and nightclubs, shops and boutiques with spruced up warehouses or old buildings converted into artists’ studios, lofts and apartments.

Some cities feature sports arenas and stadiums as a major draw, and the food offerings go beyond hotdogs, peanuts and Cracker Jack. St. Louis’s “Ballpark Village” promises, according to its website, a “buzzing, sports-themed district close to Busch Stadium with restaurants, bars and nightlife venues”; Baltimore’s Inner Harbor, which is walking distance to Oriole Park at Camden Yards, features a science center, aquarium and historic warships moored at the dock, as well as a complex of bars, eateries and music venues in a repurposed electric-power station known as “Power Plant Live!”

Some cities feature sports arenas and stadiums as a major draw, and the food offerings go beyond hotdogs, peanuts and Cracker Jack. St. Louis’s “Ballpark Village” promises, according to its website, a “buzzing, sports-themed district close to Busch Stadium with restaurants, bars and nightlife venues”; Baltimore’s Inner Harbor, which is walking distance to Oriole Park at Camden Yards, features a science center, aquarium and historic warships moored at the dock, as well as a complex of bars, eateries and music venues in a repurposed electric-power station known as “Power Plant Live!”

Beyond Main Street, restaurant closures are part of the collateral damage in suburbia as pandemic-wary people work and shop from home. “As I go around from town-to-town on Long Island and shoot out to the malls, I can see business closings everywhere,” says Ray Keating, chief economist at the Small Business & Entrepreneurship Council, a Washington-based trade group claiming 100,000 members. “When one business shutters, it affects other businesses. There’s a ripple effect.”

Adds Sink of the restaurant association: “Restaurants are often located with the anchor store inside malls. You never find any kind of mall without some sort of food court.”

When a restaurant closes its doors, it has a knock-on effect as well, sending shockwaves coursing up and down the supply chain. Prior to the pandemic, Sink reports, the industry generated $2.5 trillion in economic activity and supported 21 million jobs. Cutbacks in food service hurts “everything from butchers and farmers and distillers to the Cisco and Aramark food companies that depend on restaurants.

“It will reach farther back into the economy,” she adds, causing economic pain to such disparate businesses as cleaning companies, local plumbers, handymen, and maintenance workers. Even “technology companies that provide systems (for restaurants) to run a credit card or make reservations or keep track of service orders” are affected.

Andrew Volk, owner of the Portland Hunt & Alpine Club, a restaurant and bar with the reputation for offering possibly the tastiest cocktails in Maine, says that keeping his business going hasn’t been easy. The establishment was forced into lockdown in March and “stayed dark until Memorial Day,” he says, when it got the green light from the state to sell food and cocktails to go. On July 4, the restaurant went to outdoor seating, which it maintained until New Year’s Eve, adding heaters and umbrellas in the autumn to fend off Maine’s frigid temperatures.

Volk reckons that his restaurant’s sales were off by roughly 55 percent in 2020 over the previous year. Fully 95% of revenues go to pay expenses, including rent and utilities and employees’ wages. And the rest of the money scarcely lands in the cash register before it’s passed on to his vendors.

But as he has cut back operations, all of his vendors are feeling the pinch as well. There are no longer twice-weekly deliveries from the local package store from which, by state law, Volk is required to purchase hard liquor. His beer purchases –- craft beer prepared by Rising Tide Brewery and Oxbow Brewery, both of Portland, as well as Miller, Budweiser and Narraganset, the popular Rhode Island-made brew – are no longer so robust. Volk has also reduced his procurement of French and South African wines from importers.

Purchases of farm-to-table produce from Stonecipher Farms, Dandelion Springs, and Snell Farms, which came to a halt last March, remain diminished. The daily deliveries from Baldor Specialty Foods, a New York-based food supplier of, among myriad foodstuffs, out-of-season vegetables and citrus fruit, are less frequent.

Purchases of farm-to-table produce from Stonecipher Farms, Dandelion Springs, and Snell Farms, which came to a halt last March, remain diminished. The daily deliveries from Baldor Specialty Foods, a New York-based food supplier of, among myriad foodstuffs, out-of-season vegetables and citrus fruit, are less frequent.

Volk is still offering fresh cooked fish for take-out, including cod, trout, halibut, hake and shrimp (but not cold-water Maine lobster). Even so, he’s ordering less seafood from Browne Trading Market. He has also cut back on specialty soft cheeses he buys from several local dairy farms, including Larkin’s Gorge and Fuzzy Udder.

Other vendors affected include Portland Paper Products, which supplies him with paper goods such as toilet paper and paper towels, cleaning supplies and chemicals for the dishwasher. One bright spot for the paper products supplier: it is meeting Volk’s increased demand for take-out boxes, paper napkins and plastic utensils.

Meanwhile, Volk is not looking as much to Pratt Abbott Cleaners for freshly laundered linens such as tablecloths, napkins, and kitchen shirts. Capone Griding Company in Boston, which sharpens kitchen knives and cutlery, isn’t making as many pickups and deliveries these days.

Ian Jerolmack, owner-operator of 10-acre Stonecipher Farms in Bowdoinham, Maine, is one of Volk’s food suppliers. He has been providing fresh, farm-to-table produce to several dozen restaurants in Portland, plus a couple “up the coast,” he says, since he began tilling the Maine soil a decade ago. Now the grower of organic fruit and vegetables – a garden of delights that includes tomatoes, carrots, beets, onions, cabbage, turnips, squash, sweet potatoes, and fennel – has been feeling the economic hardship along with the restaurants.

By year-end 2020, Jerolmack says, he is down to only 15 restaurants as customers, a two-thirds attrition from his 45 customers prior to the pandemic. “Our farm was sort of unique in that it almost exclusively sold to restaurants,” he says. “They’re all in various degrees of agony,” he adds, “and I don’t know how the dust will settle. It’s been super-bizarre.”

By year-end 2020, Jerolmack says, he is down to only 15 restaurants as customers, a two-thirds attrition from his 45 customers prior to the pandemic. “Our farm was sort of unique in that it almost exclusively sold to restaurants,” he says. “They’re all in various degrees of agony,” he adds, “and I don’t know how the dust will settle. It’s been super-bizarre.”

When the restaurants went into lockdown last March, Jerolmack was faced with zero demand for his produce, and his livelihood was in jeopardy. At the same time, he was forced to reckon how much seed to plant. “There’s only one window in which to plant seeds,” he explains.

He had to decide whether to take on fulltime seasonal workers, which is not a simple proposition. In order to plant, tend and harvest his crops, he’d need to hire and house four Mexican workers under the federal government’s H-2A visa program. By law, he says, he was required to guarantee the foreign workers payment of 75% of their wages for eight months of employment. “I felt as if I were drowning,” he says. “It was a heavy weight.”

He opted to hire the H-2A workers and forged ahead with the planting, albeit at reduced acreage, consoling himself with the farmer’s ancient adage: “People always need to eat.”

With restaurants closed, his only recourse would be to sell directly to consumers. Yet Jerolmack had no online presence and was pretty much frozen out of the local farmers markets. So he turned to local restaurants and arranged to sell produce to their top customers. “I threw together a ‘farmer’s choice,’” he says, “a mixed bag of chard, carrots, onions, and beets – or whatever vegetables were in season and charged $25 a bag.”

Right away, he was able to sign up 175 customers paying $100 apiece for four weeks of produce, enough of a cushion for him to sell his “storage crops” and stay in business. Individual customers were grateful to buy the fresh organic food and avoid grocery stores, he says, the arrangement worked out for the restaurants. “They got increased foot traffic and helped their takeout business. Everybody loved it.”

By being creatively entrepreneurial and employing several direct-to-consumer sales strategies, he was able to chalk up revenues of $300,000 in 2020. That’s a hefty, 35% drop compared with the $440,000 in 2019 gross receipts. But Jerolmack says he kept five fulltime workers employed, he’s got a new consumer trade, and he’s getting ready for the 2021 planting season.

Thomas McQuillan, vice-president for strategy, culture and sustainability at wholesale food distributor Baldor, says that in a given year his Bronx-based company – with major operations centers in Boston and Washington, D.C. – delivers high-quality food to 10,000 restaurants from Portland, Me. to Richmond, Va. The wholesaler also supplies food in bulk to corporate dining rooms and cafeterias, hotels, institutions like hospitals and schools, and sports stadiums.

Baldor buys its produce from 1,000 regional farms, both big and small, and trucks in out-of-season produce from the West Coast. A visit to the company’s website discloses a vast cornucopia of edibles and victuals for sale. A few clicks discloses a gastronomic wonderland of fruits and vegetables, organics and cold cuts, meat and poultry and seafood, specialty and grocery items, dairy and cheese, bakery and pastry, and wine.

When the pandemic hit and restaurants went on lockdown, Baldor’s business plummeted by 85%, McQuillan reports, and the company reacted in much the same way as the Maine farmer. “With Covid-19,” says McQuillan, “all industries in the food business were affected. But we knew that the same number of people in our geographic area would be looking for food and we pivoted to a business-to-consumer platform and began shipping directly to people at home.

“We also knew many corporate types were no longer working in offices and, early on in the pandemic, people were fearful of going to grocery stores,” he adds, “and we began deliveries to apartment buildings all over New York. It’s not that different from delivering to a restaurant.”

According to a New York Times story, the company required a $250 minimum for consumer purchases and delivered 6,000 items within a 50-mile radius of New York City. McQuillan told deBanked it pressed its 400-truck fleet of “sprinter vans to tractor trailers” into service for the residential deliveries. The consumer business and limited restaurant re-openings allowed Baldor “to rebound, but nowhere near pre-Covid levels,” he says. By year-end 2020, the company had furloughed 20% of its workforce.

Fresh fish is for sale on the fishmonger, outdoor seafood market.[/caption]The seafood industry was among the hardest hit by the pandemic’s throttling back the restaurant industry, says Ben Martens, executive director of the Maine Coast Fishermen’s Association. Seafood is much less likely than poultry or meat to be prepared at home or ordered for takeout. Groundfish like flaky cod, haddock, pollack, hake and flounder, he explains, are especially popular dishes in high-end restaurants in New York, Boston and Chicago.

Fresh fish is for sale on the fishmonger, outdoor seafood market.[/caption]The seafood industry was among the hardest hit by the pandemic’s throttling back the restaurant industry, says Ben Martens, executive director of the Maine Coast Fishermen’s Association. Seafood is much less likely than poultry or meat to be prepared at home or ordered for takeout. Groundfish like flaky cod, haddock, pollack, hake and flounder, he explains, are especially popular dishes in high-end restaurants in New York, Boston and Chicago.

“Seafood is a celebratory food,” Martens says. “It’s a food people embrace when things feel good. It’s covered in butter and people eat it outside when they’re with family and friends.”

Early data, he says, showed a 70% decline in “landings revenue” at the non-profit Portland Fish Exchange Auction, the major marketplace connecting fishermen with wholesalers and processors. Some fishermen and lobstermen have had some success selling directly to consumers by switching over to scallops and other seafood popular with Mainers who, Martens asserts, are somewhat more inclined to prepare seafood at home than people in other states.

But what has really given the industry a boost, he says, has been an anti-hunger program run by his trade association. Seeded with $200,000 from an anonymous donor, and bolstered with $200,000 received through the CARES Act passed by Congress last year, the program purchases seafood at a fair price and funnels it to food pantries. “Maine is the most food-insecure state in the country,” Martens says. “and high quality protein is hard for a lot of people to find.”

The program contributed enough fish portions to contribute to 180,000 meals in 2020, while helping soften economic damage to fishermen. “Now we’re seeing some stabilization with outside restaurant seating,” Martens says.

Sam Cantor, who is vice-president for sales at Gotham Seafood, a New York broker doing an estimated $16 million in sales, according to Buzzfile, sounded glum and subdued in a telephone interview with deBanked. He reports that the company delivers salmon, tuna, lobster, King Crab legs, red snapper and other seafood directly to eateries in Manhattan as well as the tri-state region of New York, Connecticut and New Jersey.

The last year has been a burden. “A ton of places are closed — cafeterias, cafes, hotels,” he says. “People are not going to the Berkshires or the Hamptons, offices are closing. In the beginning of the pandemic when (New York Governor Andrew) Cuomo shut down indoor dining it was brutal. And it’s still a difficult situation.”

Describing layoffs at the company as “significant,” Cantor says it’s also been emotionally draining to see the misfortune that has befallen restaurant workers. “It’s been a hard thing to witness,” he says. “A lot of our relationships are with chefs and they have families.”

Gotham has had some success selling directly to consumers by revamping its website and putting money into advertising on the online platforms Facebook and Instagram, he says, but “we’re not back to 100%.”

Cantor also says he is concerned that the country’s commercial infrastructure is at risk of fracturing. “It’s more than just losing your favorite restaurant or what happens to the individual fisherman and farmer,” he says. “It takes a very intricate supply chain for you to get your favorite fish. There’s a lot of work that goes into it.

“I hope my kids don’t have through something like this,” he went on. “The home delivery has been a shining light. But we want travel and tourism to come back. We want people going back to The Garden to watch the Knicks. I’m hoping there will be a renaissance, and this is just the start of the Roaring Twenties.”

Shopify Releases 3 Years of Shopping Trends: 1 Million Merchants Say Pandemic Purchases New Normal

December 14, 2020 Shopify released a treasure trove of data from customer surveys collected in the past three years. The firm reached a milestone of 1 million businesses using their platforms this year. The data Shopify gathered paints an accurate portrait of a dramatically going-digital world.

Shopify released a treasure trove of data from customer surveys collected in the past three years. The firm reached a milestone of 1 million businesses using their platforms this year. The data Shopify gathered paints an accurate portrait of a dramatically going-digital world.

“2020 has accelerated the industry by a decade, permanently altering the way entrepreneurs start, run, and grow businesses, as well as how consumers choose to shop and pay,” President of Shopify, Harley Finkelstein, said in an introduction. “Consider this report your crystal ball into the future of this industry.”

Finkelstein put forth five key predictions based on the trends Shopify found in the data. Be prepared, Finkelstein warns, for a new generation of retailers and consumers to forever change the world of commerce.

Key prediction one: Young consumers will change the business landscape as eCommerce charges ahead. Shopify predicts that younger shoppers changing their habits due to the pandemic will likely shop this way from now on. 67% of shoppers under 35 shifted to shopping online, compared to 57% of the 35-55 bracket.

Overall, 84% shopped online this year, compared to 65% in person. 53% of those that shopped online did so because they wanted to avoid crowds, 46% of consumers felt uncomfortable shopping in person.

Key two: Physical retail is transforming, giving local businesses new advantages. Consumer reports showed 62% of people prefer contactless purchases for in-store purchasing in 2020, an increase of 122% during the pandemic. Go figure. 94% of the point-of-sale retail lost in the first six weeks of shutdowns was replaced with online sales.

Key three: Consumers want to shop independently but are not. Businesses will adapt to make it easier to buy from a small business. Half of the consumers look for independent business owners, while 65% say they support small businesses. It turns out that only 29% of consumers shopped at a small business during the pandemic, giving ground to findings that small business is having trouble adapting to online-only commerce compared to larger chains.

Independent retailers need to make customers put their money where their mouth is. Shopify said that fast and free shipping could help. 59% of online shoppers say free delivery would improve their online shopping. 75% of merchants who generated sales in March through September did so with free shipping options on their site.

Key Four: Consumers will vote with their wallets. 53% prefer environmentally sustainable products, and 49% want the retailer to donate proceeds to charity when they make a purchase. The fourth of consumers that did buy local this year did so to support their community and local economy and create jobs.

Finally, our favorite, Key Five: Modern financial solutions will disrupt business and consumer banking finance and lending. Shopify found evidence for growth in their merchant financial platforms. 24% that applied for financing agreed with the 36% that faced problems from COVID-19 by stating: “My bank or financial institution does understand the needs of my business.”

The quality of user experience plays a massive factor for merchants; accordingly, 48% say “a good online bank or mobile app experience” is a top-three feature, while 62% of marketplace sellers say the same.

The findings conclude that explaining the trends was shared to encourage businesses to use the info to adapt and change, as they have been the past year.

When The Music Stopped: How The Pandemic Threatened the History and Culture of Austin, Texas

November 15, 2020

In April of this year, Threadgill’s – a legendary Austin music venue and beer joint that, in the 1960s, famously launched the career of blues singer Janis Joplin — turned off the lights and pulled the plug on its sound stage.

A converted gasoline station, Threadgill’s had been a rollicking music scene since 1933 when musician and bootlegger Kenneth Threadgill secured the first liquor license in Texas after Prohibition. His juke box was crammed with Jimmie Rodgers songs and Threadgill himself famously sang and yodeled Rodgers’ tunes.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

For generations of students at the University of Texas, Threadgill’s was a rite of passage.

“The first time I went to Threadgill’s was in the fall of 1968, when I was a freshman at UT,” recalls Perry Raybuck, a songwriter-folksinger and retired government worker who, as a member of the Southwest Regional Folk Alliance, played the stage in 2018. “It was the beginning of an education for me,” he adds. “I had been a Beatles and rock n’ roll kid and it opened me up to different music styles. I became a convert.”

In 1981, Threadgill’s was taken over by another acclaimed club owner, Eddie Wilson, who previously had been the proprietor of the Armadillo, a fabled music venue. Wilson began to actually pay musicians – Threadgill had compensated them mainly with free cold beer – and installed a circular stage.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

It was Threadgill’s and an assortment of funky clubs and stages with names like the Soap Creek Saloon and Liberty Lunch helped put Austin on the map as “The Live Music Capital of the World.” The city remains home to the widely acclaimed television program “Austin City Limits” on PBS and the internationally renowned South by Southwest festival, which was canceled this year amid fears of a “superspread” of the coronavirus.

“Live music,” says Laura Huffman, chief executive at the Austin Chamber of Commerce, “is why people come here. It is a central component of Austin’s cultural and economic life.”

Omar Lozano, director of music marketing for Visit Austin, the city’s main tourism organization, says: “We have close to 250 places in the greater Austin region where you can hear live-music, although it’s closer to 50-70 on any given night. During South by Southwest, no stone is left unturned — everything becomes a stage: parking garages, grocery stores, housing co-ops. There are also four or five stages at the Airport, which helps liven up the mood.”

But that identity is being put to the test. So far this year, Austin has lost a raft of live music venues. Among those joining Threadgill’s in honky-tonk heaven since the pandemic struck are Barracuda, Plush, Scratchhouse, Shady Grove, and Botticelli, all of which provided niche audiences to both established musicians and up-and-coming acts.

The roller-coaster ride of government mandated shutdowns followed by a limited re-opening in the spring and another shutdown since July fourth is making life miserable and untenable for both club owners and already hardpressed musicians and artists, says Marcia Ball, a piano player and blues singer.

Ball, who was named by the Texas Legislature as “2018 Texas State Musician” and whose musical style was once described by the Boston Globe as “mixing Louisiana swamp rock and smoldering Texas blues,” told deBanked: “There was already a limited amount of opportunity for musicians to perform and monetize their work in Austin, so it has always been necessary to travel to make a living. But we still depend on a thriving local scene, and we’re losing that when key venues like Threadgill’s disappear.”

Adds Graham Williams, a prominent Texas promoter of touring bands: “These venues and bars are vital to the music ecosystem. Local bands and cover bands need hangouts, even if people are not buying tickets. They’re places to play every night of week.”

While unheralded outside the Austin scene, the local music joints were often a port-of-call for out-of-town promoters and nightclub owners checking out Austin talent – “most notably Barracuda (which) had super-popular acts and was like a hipster garage venue,” says promoter Williams. “A lot of touring bands played there on their way up.”

A July study by the Hobby School of Public Affairs at the University of Houston found that the city’s live music industry is in desperate straits. Sixty-two percent of live music spots and 55% of the bar-and-restaurant businesses reported to researchers that that they can endure for no more than four months, making them the most vulnerable of 16 industries surveyed.

And the situation has become “even more ominous” since the report was published, explains Mark P. Jones, a political scientist at Rice University in Houston and a lead researcher on the Hobby study. “That survey finished polling two hours before all bars and restaurants closed back down,” he says. “Everything people were saying was when bars were at 50% capacity. That’s a best-case scenario.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

Austin’s experience amid the Covid-19 pandemic mirrors what is occurring nationwide as bars, nightclubs and music halls in myriad cities and towns experience similar trauma. In Seattle, Steven Severin is co-owner of three nightclubs – Neumos, Barboza and recently opened Life on Mars – all in trendy Capitol Hill, the hub of the city’s club and live-music scene. He reports that he is barely holding on thanks to some help from the city and a sympathetic landlord who is “a big music advocate.”

“He knocked down the rent a little bit,” Severin says of his landlord, but the situation is dire. “We just had a fifth venue, Re bar, close at the end of August,” he says. “It was a punch in the gut. This could be me.”

The Bitter End in Greenwich Village is also keeping its head above water despite not opening its doors since March. The nightclub has a storied past: owner Paul Rizzo recounts that it is where pop singer Neil Diamond got his start and where “everyone from Curtis Mayfield to Randy Newman” has performed since its opening in 1961. But the club is silent now since the pandemic overwhelmed the city’s hospitals and made New York the epicenter of sickness and suffering during the spring. So far the club is getting help from a landlord’s forbearance and loyal musicians.

Peter Yarrow (the “Peter” in the bygone trio Peter, Paul and Mary), donated a streamed concert to patrons who contributed to a fundraiser that raised more than $50,000. And grateful local musicians also put on a benefit directing people to a Go Fund Me page on the Internet that raised another $16,000. “We’re a major venue for local musicians,” Rizzo says. “We should pull through.”

It’s in their self-interest for artists to do whatever they can to keep the doors open at a club like The Bitter End. “These days because of the last two decades of declining record sales — live music is the bread and butter of a musician’s income,” says journalist Edna Gundersen, a recently retired, 28-year-veteran of USA Today. “That’s true whether it’s a local entertainer or an international superstar.” (Gundersen earned the reputation as Bob Dylan’s favorite journalist; it was she who scored his only interview after he won the Nobel Prize for literature in 2018, publishing his eccentric musings in the The Telegraph of London and breaking the news that he would indeed accept the prize.)

“Touring has been crushed,” Gundersen adds, “and festivals have been canceled. So people doing the circuit and clubs are gone for all intents and purposes. Streaming — while initially up — is down because people aren’t listening to music in the gym or in their cars. Physical record sales are also down because people aren’t going to stores. All of this is just killing musicians.”

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

The Paycheck Protection Program, the multi-billion, multi-tranche aid package for small business which Congress authorized as part of the CARES Act in March, has provided some funding for the live-music and entertainment industry. But because of the PPP’s requirements that only 40% of the funds can be spent on rent, mortgage and utilities, which are major expenses for nightclubs and music venues, the program has largely been a disappointment.

Hoping to win attention and assistance for their plight from the federal government — “We’re the first to close and the last to reopen,” Severin says — live-music entrepreneurs like himself and Rizzo and more than 2,800 club-owners and promoters across the country have banded together to form the National Independent Venue Association.

Their membership includes independent proprietors (no corporate members allowed) of saloons, cabarets and concert halls as well as theaters, opera houses and auditoriums from every state plus the District of Columbia. To help plead their case with Congress, the organization hired powerhouse law firm Akin Gump Strauss Hauer & Feld, the largest Washington, D.C. lobbying firm by revenue.

NIVA also blanketed Congressional offices with two million letters, e mails and correspondence generated from hordes of fans and performers. Among the many scriveners are a slew of boldface names: Mavis Staples, Lady Gaga, Willie Nelson, Billy Joel, Earth Wind & Fire, and Leon Bridges. Comedians Jerry Seinfeld, Jay Leno and Jeff Foxworthy have also penned notes to lawmakers championing NIVA’s cause.

Their message: without federal funding, 90% of independent stages will go under over the next few months. “The heartbreak of watching venues close is that once a building is boarded up, it’s not going to be a music venue any more,” warns Audrey Fix Schaefer, communications director at NIVA. “They operate on thin business margins to begin with and they’re too hard to develop.” For touring acts, each city stage is “an integral part of the music ecosystem,” Schaefer explains. “When artists finally do get back on the tour bus, they might have to skip the next five cities and go on to the sixth.”

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

Thanks to the bi-partisan efforts of Senator Amy Klobuchar (D-Minn.) and Senator John Cornyn (R-Texas), NIVA’s campaign has gotten traction. The unlikely couple have teamed up to author a rescue bill, known as the Save Our Stages Act. If enacted, it would establish a $10 billion grant program for live venue operators, promoters, producers, and talent representatives.

The legislation would provide grants up to $12 million for live entertainment venues to defray most business expenses incurred since March, including payroll and employees’ health insurance, rent, utilities, mortgage, personal protection equipment, and payments to independent contractors.

NIVA’s chief argument for the legislation is coldly economic rather than sentimentally cultural. The organization cites a 2008 study by the University of Chicago that spending by music patrons produces a “multiplier effect” for the broader economy. For every dollar spent by a concert-goer at a live performance, the Chicago study determined, $12 in downstream economic activity occurs.

Explains Scott Plusquellec, nightlife business advocate for the City of Seattle: “You buy a ticket to a show and the direct economic impact of that purchase is that it pays the artist, bartender and the club itself as well as the band, advertisers, and promoters. The indirect economic impact,” he adds, “is that after you bought the ticket, you went to a barber shop or a hair salon to look good that night. You might also have dinner, go to a bar for a drink and tip the bartender. That’s the whole the idea of a ‘multiplier.’”

In Austin, that economic logic is an article of faith with city burghers, asserts Lozano of Visit Austin, who reports that live music in the capital city is roughly a $2 billion industry. To promote live music, the tourism bureau sponsors such endeavors as “Hire an Austin Musician.” That program, Lozano says, “sends musicians around the U.S. to represent us during marketing season.” In another promotional campaign, Visit Austin arranged for singer-songwriter Julian Acosta to play a gig at travel agents’ offices in London when Norwegian Air inaugurated direct flights between London and Austin in 2018. “The U.K. is one of our best markets,” he reports.

Even so, efforts by the business community and the City of Austin have failed to stanch much of the industry’s bleeding. According to its website, the city has disbursed $23.7 million in loans and grants to small businesses and individuals, but slightly less than $1 million of that has gone to live-music and performance venues, entertainment and nightlife, and live-music production and studios.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

In late September, The city of Austin’s Economic Development Department released a slide show breaking down how the $981,842 in industry grants and loans – of which $484,776 was provided by the federal government under the CARES Act – were awarded. Most top recipients appeared to be well known nightclubs and entertainment venues downtown or close to the city’s inner core.

The Continental Club on South Congress – a key fixture in the hip “SoCo” strip just over the Colorado River from downtown – appeared to do best. It picked up $79,919 from two programs: $40,000 in the CARES-backed small business grants program, and $34,919 from the city’s Creative Space Disaster Relief Program. Other clubs receiving $40,000 in the small business grants program included Stubbs, The Belmont, Cheer Up Charlies and the White Horse. (For a full list go to: http://www.austintexas.gov/edims/document.cfm?id=347299)

Joe Ables, owner of the Saxon Pub, a major Austin venue for jazz – blues singer Ball hailed it as one of several important Austin clubs “that sustains creative endeavor, especially for songwriters” – was vexed that his grant application was denied by the city “with no explanation.” Ables also voiced dissatisfaction that the city paid the Better Business Bureau a 5% administration fee to handle $1.14 million in relief funds, including determining which applicants were approved. “What would they know about live music,” he says.

Even for clubs that received city largesse, it hasn’t been nearly enough to sustain them. The North Door, which got $15,240, closed for good on September 11 (an ominous day — the anniversary of the attacks on the World Trade Center and the Pentagon.)

Meanwhile, enough clubs and venues were left out in the cold that club owner Stephen Sternschein could tell deBanked just before the slide show was released: “I’ve heard talk of a $21 million grant program but most people I know haven’t seen a dollar of that.”

Sternschein is managing partner of Heard Presents, an independent promoter and operator of a triad of downtown clubs that includes the spacious Empire Garage, which features hip hop and urban jazz, and has space for 1000 music-goers. A member of NIVA, Sternschein describes efforts by both the state and local governments as “woefully inadequate.” Says he: “People are looking to the federal government for answers.”

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

The diminution of places for musicians to ply their trade is a double edged sword. If Austin loses its luster as a hot music town, it puts the city’s overall economy in jeopardy. Explains Jones, the Rice political scientist: “The difficulty for Austin is that it could lose its comparative advantage. Unlike restaurants, movie theaters or sports events, which people can find just as easily in other cities, the Austin music scene draws capital and revenue from across the country.

“You can go out to dinner in Waco,” he observes, referring to the mid sized Texas city between Austin and Dallas best known as home to Baylor University and its “Bears” football team, fervent Baptist religiosity, and unremarkable night life. “Music brings in revenue to Austin and to Texas that wouldn’t otherwise come here.”

In addition, Jones says, the large presence of “artists, creative types, and freelancers” helps make Austin a strong selling point for “brain industries” to attract talent from the East and West Coasts. “It supports the technology industry by making it easier to recruit employees to live there,” he says. “Austin is an alternative to Silicon Valley. People who are progressive might be hesitant to come to conservative, red-state Texas from California but they’ll come to Austin because it’s culturally cool.”

Austin, which embraces the slogan “Keep Austin Weird,” is on the verge of becoming just like every place else in Texas. Should it relinquish its flavor and charm, it could discourage many of the assorted business groups and professionals from keeping Austin on their dance card as a popular destination for meetings, conferences and get-away trips.

Howard Freidman, managing director at Bluechip Jets, a broker of private luxury aircraft, had an earlier career as a technology industry executive. Partly drawn by his previous experiences with the city, Freidman moved to Austin earlier this year. “It had the same coolness and weirdness of New Orleans — but also with the professionalism of a tech city,” he says.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

“Whenever we’d come here,” Freidman adds, “the music was always integral to the Austin scene. Even when you’d go to private parties you’d end up downtown at the club scene on Sixth Street. Austin was always a place everybody liked going to.”But as Austin has steadily been morphing into more of a high-technology center than a live-music town, it’s experiencing a silent exodus of musicians and artists who are being gentrified out of their apartments and Craftsman duplexes. Displacing them are software engineers, website designers and the like, their sleek BMWs and black, tinted-glass SUVs glistening in the parking lots of steel-and-glass corporate centers.

Many of the technology firms – including such needy companies as Samsung, Intel, Rackspace, Facebook, and Apple – have each received tax breaks, grants and subsidies worth tens of millions of dollars from a variety of local jurisdictions. Not only have the city of Austin and Travis Country been beneficent, but adjacent county governments and the state of Texas have provided abundant support. A 2014 study by the Workers Defense Project, in collaboration with UT’s Lyndon B. Johnson School of Public Affairs, reported that the state of Texas showers big business with $1.9 billion annually in state benefits. Most recently, officials with Travis County and a local school district granted Tesla more than $60 million in tax rebates to build a massive “gigafactory” southeast of town near Austin-Bergstrom International Airport.

To house the burgeoning cohort of “knowledge workers,” there are condominium conversions, tear-downs, high-rises and other forms of frenetic real estate development which, in their train, bring higher property taxes, steeper rents, and unaffordable housing.

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

Add in some of the country’s most snarled traffic, dirtier air, and a growing homeless population, and members of the artistic community are increasingly decamping for smaller satellite towns like Lockhart and San Marcos. Others in the diaspora are abandoning Texas altogether for more hospitable locales like Fayetteville Ark., Asheville, N.C., or Olympia, Wash. “Whatever made anybody think this would be a better town with a million people,” laments blues singer Ball. “This was a perfect town with 350,000. Now we’ve got Silicon Hills, Barton Springs are cloudy, and drinking water’s going to be scarce. Why is this supposed to be better?”

The drop-off in live music and the belt-tightening by musicians is causing third-party pain for people like veteran Austin journalist and publicist Lynne Margolis, whose national credits include stories for Rolling Stone online, and radio spots for NPR. “The public relations aspect of my work has dropped away because artists can’t afford to pay,” she says, “and music journalism is falling by the wayside. It’s hard not to feel to like a double dinosaur.”

Led by bars, restaurants and music venues, on many days the solemn departure of small establishments has the business news sections of Austin newspapers reading more like the obituary page. One hardy survivor is Giddy Ups – a throwback honky-tonk on the town’s outskirts that advertises itself as “the biggest little stage in Austin” – promising “just about everything,” says owner Nancy Morgan, including “country, blues, rock, bluegrass, and soul.” For the past 20 years Giddy Ups has developed a devoted following of musicians and patrons while fending off hyper modernity.

“It has an untouched, back-to-the-seventies, cosmic cowboy vibe,” says local musician Ethan Ford, a guitarist and bass player whose trio, The Slyfoot Family, has graced its stage. “It’s a time capsule,” Ford adds.

Morgan declined to disclose her annual receipts but in 2019, she reports paying out $188,000 in wages to employees, $72,000 to musicians, and $185,000 in combined sales taxes to the city of Austin and to the state. Despite her status as a taxpayer, employer and entrepreneur, she has received no state aid and is disqualified from receiving city pandemic assistance programs, meager as they may be, because she’s located in an extra-territorial jurisdiction.“

Nancy still bartends most nights and does all of the booking,” says Ford. “Her knowledge of the Austin music scene could fill a couple of books. I know a decent fistful of Austin venue owners and she’s about the only one that hasn’t given up, been forced out, or just retired. She’s a dynamo.”

Unless the cavalry arrives for Morgan and other holdouts, though, their musical days may be numbered.

Editors Note: Threadgill’s didn’t make it. The venue “has closed for good, the property has sold, and the building will eventually be torn down,” according to information disseminated for its Last Call Music Series. Its November 1st grand finale show featured Gary P. Nunn, Dale Watson, Whitney Rose, William Beckman, and Jamie Lin Wilson.

The building will be replaced with apartments.

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

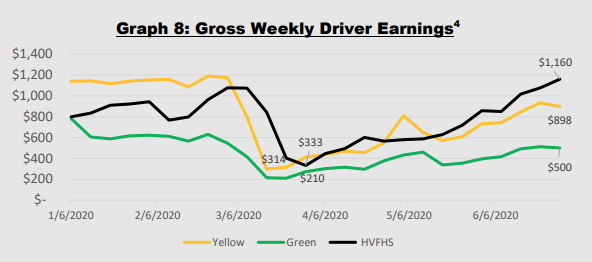

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.

How Stimulus Packages are Accidentally Ending Up in The Trash Bin

June 3, 2020 Since March, over 150 million Americans have woken up to find their banks accounts newly graced with checks from the government. Allowed by the CARES Act, this stimulus package, titled the Economic Impact Payment, was dispatched to help ease the short-term financial troubles that arose from covid-19’s disruption of the economy. And while many Americans have received their money from the Treasury, a selection of recipients are dropping their stimuli into the garbage.

Since March, over 150 million Americans have woken up to find their banks accounts newly graced with checks from the government. Allowed by the CARES Act, this stimulus package, titled the Economic Impact Payment, was dispatched to help ease the short-term financial troubles that arose from covid-19’s disruption of the economy. And while many Americans have received their money from the Treasury, a selection of recipients are dropping their stimuli into the garbage.

The reason for this being that the mode of delivery was switched up mid-May. Instead of having the money directly wired to their bank accounts, roughly four million Americans will instead receive their packages via prepaid VISA debit cards. This group is made up of those taxpayers who do not have bank information on file with the Treasury and who had their tax returns processed by the Andover or Austin Service Centers.

Treasury-sponsored and issued by MetaBank, these cards are shipped in a plain envelope that bares the words “Money Network Cardholder Services, and which contains instructions alongside the card: making the stimulus package look more like marketing spam than anything else. As such, numerous complaints have been made about the delivery method, with many of those who received the cards saying they threw out the entire envelope without thought, believing it to be junk mail.

“It really read to me like a scam,” said one woman interviewed by Yahoo! Finance. “So into the shredder it went.”

As well as this, Yahoo! also found that other recipients received cards that had mixed up their names with those of their spouse. A situation that proved confusing given that the cards must be activated via your phone using your social security number and other personal details.

Funds on the cards can be used to directly pay expenses as well as be transferred to personal accounts; they can also be used at ATMs, although the withdrawal amount per day is limited to $1,000, meaning multiple trips to a bank during a pandemic will be required.

Done in an effort to reduce instances of fraud as well as speed up the process of getting money to Americans, communication about the EIPCard setup seems to have gotten lost in the fray.

Going forward, the Treasury will be waiving the fees associated with reissuing an EIPCard to anyone who claims they shredded or threw it out, and initial reissuance fees from earlier dates will be reversed.

Interview With Polling Expert Scott Rasmussen

May 7, 2020On Tuesday, I interviewed nationally recognized public opinion pollster Scott Rasmussen, who is the publisher of ScottRasmussen.com and is the editor-at-large for Ballotpedia, about the trajectory of the presidential race and how the current environment is affecting how people think.

Mr. Rasmussen will be a guest speaker at Broker Fair 2020 Virtual on June 11, 2020. You can watch the video interview below.