Business Lending

Citing Unnamed Sources, Reuters Reports Kabbage Possibly Looking to Acquire OnDeck

March 23, 2017 Reuters is reporting that Kabbage is in talks to raise equity capital to potentially use for acquisitions and that OnDeck is one of several targets under consideration. As Reuters attributed the OnDeck portion to just one of their multiple unnamed sources, it’s entirely speculative at this point.

Reuters is reporting that Kabbage is in talks to raise equity capital to potentially use for acquisitions and that OnDeck is one of several targets under consideration. As Reuters attributed the OnDeck portion to just one of their multiple unnamed sources, it’s entirely speculative at this point.

From a theoretical perspective, would such a thing make sense?

Kabbage has momentum on their side right now. Their recent half billion dollar securitization that was finalized earlier this month was oversubscribed. Although they only originated about half the loan volume of OnDeck last year, Kabbage’s last private market valuation ($1 billion in Oct 2015) is nearly 3x as large as OnDeck’s current market cap.

Valuations in the industry have changed a lot over the last 18 months but there’s no doubt that Kabbage has become a unique competitor. At LendIt, company CEO Rob Frohwein revealed a bit of their secret sauce when he said that their customers borrow from them on average 20-25 times over the course of 4 years, whereas their competitors make only 2.2 loans to their customers on average.

There is a general view in this industry that acquiring a competitor adds little value other than more marketshare. Kabbage, however, may potentially believe that (1) OnDeck is too undervalued to pass up (2) That OnDeck could generate better margins using Kabbage’s strategy (3) That OnDeck’s partner relationships would add additional value (4) That the company cultures are compatible enough to make an acquisition work (5) that the combined entity would allow them to better align their political and regulatory agendas.

We mustn’t forget however that a single unnamed source is pretty weak to go off of. One possible reason that someone would want to report that OnDeck is an acquisition target is to cause a temporary spike in their stock price. (and I certainly do not have any position in the stock)

For now, it’s fun to think about such an acquisition scenario and we’ll report more, if and when we hear anything.

Managing Risk in Small Business Lending

March 16, 2017 Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

This year, I took on an even bigger role when I was named chief risk officer of the Silicon Valley company, which offers working capital financing to small and medium-sized businesses.

My promotion comes at a time when risk is becoming a bigger concern in fintech, which is ushering in big changes in banking and financial services.

Fintech revolutionizes financial services

Data science technology has dramatically improved access to financing and the way we manage our money. The fintech wave that began with my former company, PayPal, and the world of payments, has spread to other aspects of personal finance, from mortgages to student and auto loans to investing.

This expansion was accompanied by growing concern that the fintech boom is fraught with risks that, if left unchecked, could lead to a major bust in the financial services industry that could in turn cause harm to the broader economy.

In a speech in January, Mark Carney, the governor of the Bank of England, cited the need to “ensure that fintech develops in a way that maximises the opportunities and minimises the risks for society.” “After all, the history of financial innovation is littered with examples that led to early booms, growing unintended consequences, and eventual busts,” he said.

Risk management as key to success

Risk management certainly has been a focus area for BlueVine from the beginning.

BlueVine joined the revolution in small business financing in 2014 when it rolled out an innovative online invoice factoring platform.

Factoring is a 4,000-year old financing system that allows small businesses to get advances on their unpaid invoices by providing easy, convenient access to working capital. BlueVine transformed what had been a slow, clunky, paper-based solution into a flexible and convenient online financing system that enables entrepreneurs to plug cash flow gaps that often hamper business growth.

Because the BlueVine platform is based on cutting-edge data science technology that can process and analyze information to make quick funding decisions, managing risk inevitably became a major challenge in building our business. As Eyal Lifshiftz, our founder and CEO, recalled in a recent column, in BlueVine’s first month of operation, almost every other borrower defaulted.

In fact, that was partly the reason Eyal invited me to join his team. BlueVine serves small and medium-sized businesses seeking substantial working capital financing of up to $2 million. To succeed, we needed to build a robust data and risk infrastructure.

Small startup with big data needs

Joining BlueVine also posed a personal challenge.

At PayPal, where I started as a fraud analyst and then moved into the company’s data science division where I helped develop behavior-based risk models, I had enormous amounts of data to work with to do my job. Now, I was joining a young startup with very limited data history, but with big data needs.

This meant putting together exceptional and experienced teams of data scientists and underwriters and developing a technology that becomes progressively more precise and accurate as it draw lessons from our steadily expanding data and underwriting decisions. It was important for us to have a group of super smart, highly-motivated and technologically-strong people working closely with a team of experienced and sharp underwriters.

Here’s how the process works: Our underwriters develop a robust methodology which is then translated into detailed logic decision trees.

Each decision tree includes dozens, even hundreds of branches, made up of question sets on different underwriting situations.

For example, a decision tree could focus on approving new clients coming from a specific industry, such as transportation or construction, or on increasing the credit line for a client with a specific financial profile.

A typical decision tree would drill down on further financial questions: What’s the expected cash-flow of the business in three to six months? What’s the pace at which it has accumulated debt over the past year? Are the business sales seasonal in a material way?

The questions could also focus on non-financial areas: Does the company’s website look professional? How does it compare with major companies in its industry? Does the business actively maintain its Facebook and Twitter accounts?

The goal is to build a risk infrastructure that steadily becomes more efficient in answering questions in an automated, large-scale and highly accurate manner. Our data scientists leverage multiple external data sources and use dynamic advanced machine learning models to answer these questions pretty much in real-time and with a high degree of accuracy.

So it’s a combination of technology and human input. There will always be gray areas, questions and situations that cannot immediately be addressed by our computer models.

But as the models get better and more robust, the gray areas will shrink. Our models are constantly and automatically enhanced, re-trained and expanded by the most recent data and input from our underwriters.

Think of it as the fintech version of Deep Blue and AlphaGo, the powerful computer programs that famously outplayed topnotch chess grandmasters. Both programs were based on similar principles: the more they played, the more knowledge they absorbed and the more formidable they became at chess.

Technology and teamwork

An even better example is the self-driving car powered by Google’s artificial intelligence technology. Human input is still required, but the more driving the car does, the smarter and more autonomous it becomes.

Building our risk infrastructure is an ongoing process for BlueVine. But it already has helped us steadily expand our reach, making us stronger, smarter and even faster in financing small and medium-sized businesses.

In just a couple of years, the strides we’ve made in managing risk more effectively enabled us to increase our credit lines to $2 million for invoice factoring and $100,000 for business lines of credit, which means we’ve been able to serve bigger businesses with bigger financing needs.

While we initially focused mainly on small businesses with annual revenue of under $250,000, today we have an increasing number of clients with annual sales of more than $1 million and increasingly, we’ve been able to serve clients with revenue of more than $10 million a year.

By the end of 2016, BlueVine had funded roughly $200 million. We’re on track to fund half a billion dollars by the end of this year.

We’ve accomplished this in a time of heightened skepticism about fintech in general and alternative business lending in particular. But rather than scoff at this skepticism, I’d point out two things.

First, fear often accompanies the rise of a new technology. Second, in the wake of the 2009 financial crisis, it’s prudent to raise hard questions about the rapid emergence of new financial technologies.

While building technologies and companies that can provide financial services faster and easier is a laudable goal, It’s wise to move cautiously and with humility.

The BlueVine experience underscores this.

Risk is still a challenge we take on every day. But we have found ways to take it on confidently and effectively with a vigorous combination of technology and teamwork.

Ido Lustig is Chief Risk Officer of BlueVine.

Kabbage CEO Rob Frohwein Pokes Fun at “Alternative Lending”

March 14, 2017 At LendIt, Kabbage CEO Rob Frohwein poked fun at alternative lending, suggesting that it should just be called lending. His presentation, titled “Alternative Lending is Dead Long Live Data,” put the last few years of irrational exuberance into perspective. Below are some of his one-liners:

At LendIt, Kabbage CEO Rob Frohwein poked fun at alternative lending, suggesting that it should just be called lending. His presentation, titled “Alternative Lending is Dead Long Live Data,” put the last few years of irrational exuberance into perspective. Below are some of his one-liners:

“You don’t disrupt banks by focusing on the advantages that banks have over you.”

“Most online lenders thought by calling themselves a technology company, they are one.”

“However, the biggest piece of technology that most of them promote is an online application.”

“There’s nothing special about an online application.”

Frohwein also revealed some interesting facts about Kabbage during the presentation, including that their customers borrow from them on average 20-25 times over the course of 4 years, whereas their competitors only make only 2.2 loans to their customers on average.

On The Line With BlueVine After a Big Year

March 13, 2017 Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

BlueVine’s success comes at a time when some in the online lending space have lost their luster. Lifshitz feels his company, however, is positioned well. “The time of exuberance has disappeared,” Lifshitz says. “Investors are looking to create value.”

Part of what makes them different is that they not only factor invoices, but they also provide lines of credit to prime and near-prime customers. Factoring is still a bigger percentage of their overall business, Lifshitz says, but he asserts that their credit line segment is growing at a faster clip. And he insists that they are working on other products too, not just loans. It sounds like the beginnings of a bank, I tell him, while making references to SoFi and their ability to live on the threshold of banking without actually currently being one.

“People have been saying that PayPal would become a bank forever but they haven’t become one,” he points out.

Still, running a company as big as his does require prudent decisions. “We are very mindful of how we manage capital,” he says. I ask if he thinks his business model protects them from an economic downturn. “It doesn’t protect it,” he asserts. Instead, he explains, his model gives him the ability to make adjustments rapidly. Since BlueVine’s capital is typically repaid in a matter of months, they can react to economic changes quickly.

Big name backers aren’t afraid to show that they believe in this either since they have been funded by Lightspeed Venture Partners, 83NORTH, Correlation Ventures, Menlo Ventures, Rakuten Fintech Fund and other private investors. A recent announcement by BlueVine says that they are on track to fund approximately $500 million to small businesses in 2017.

New York’s State Government is Competing With Online Lenders on Pay-Per-Click and Misinforming Small Businesses

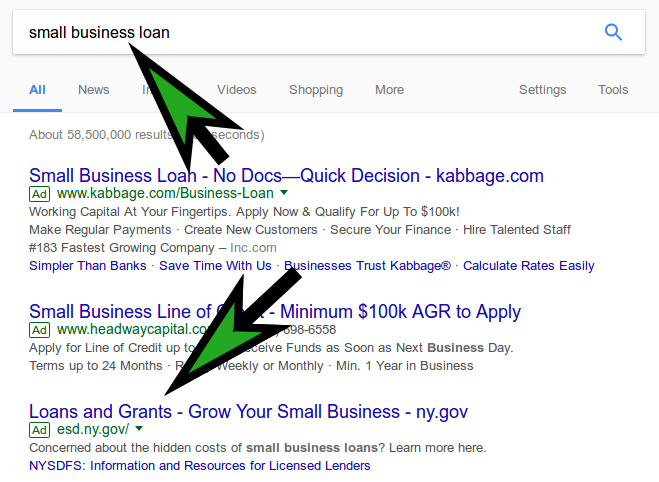

March 10, 2017Move over online lenders, New York’s financial regulator is apparently shelling out big bucks to steer away New York’s online small business loan searchers to THEMSELVES. As someone who has historically kept tabs on Google’s search results for lending related keywords, this new result is one of the more interesting developments I’ve seen yet.

From a New York IP, querying Google with the keyword small business loan produced not only an ad for Kabbage and other online lenders, but also prominent paid placement from New York State with a sitelink extension to the New York Department of Financial Service’s page about licensed lending requirements.

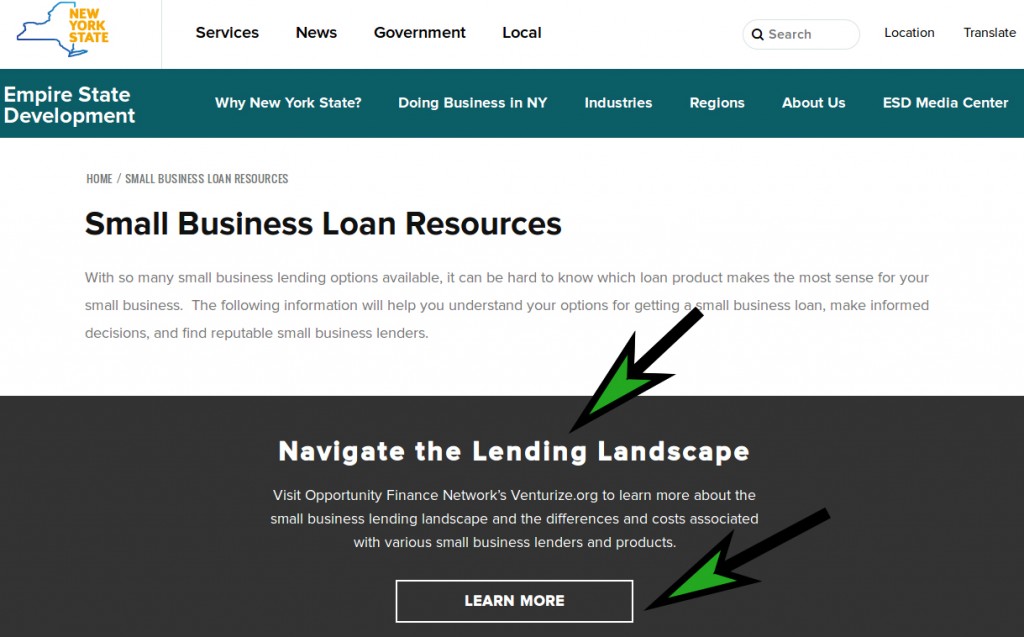

While there’s nothing that weird about marketing state-assisted development programs, the main Google ad link directs visitors to “Navigate the Lending Landscape” by clicking a “Learn More” button.

That takes you to Venturize.org, operated by Opportunity Finance Network, a Community Development Financial Institution (CDFI) that New York is apparently really doing the advertising for. And there’s a major problem with that.

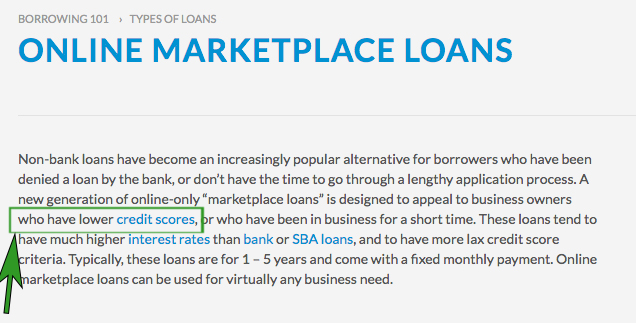

The information across that site is wildly incorrect. It explains online marketplace loans as “designed to appeal to business owners who have lower credit scores, or who have been in business for a short time.” That’s a pretty broad statement especially when many online marketplace lenders are in fact designed to appeal to business owners who have higher credit scores and have been in business for a long time.

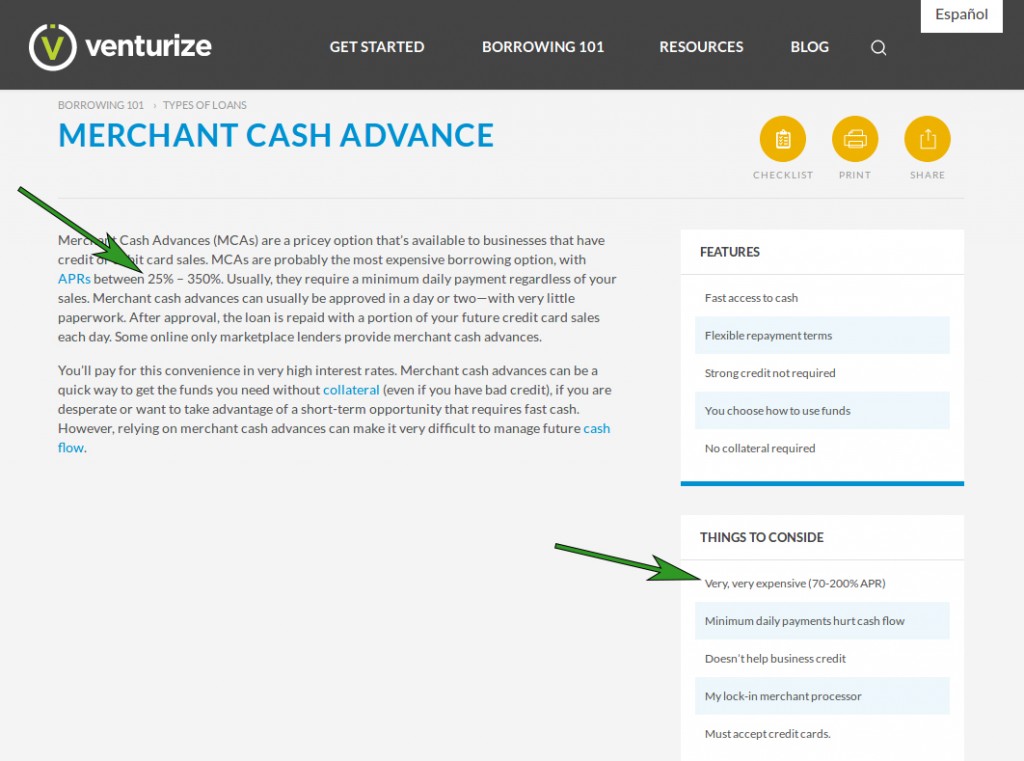

The description of merchant cash advances is even worse. Whoever wrote it has no understanding of them in the slightest. Good thing New York State is paying up to $100 a click with our tax dollars for premium keywords to teach businesses absolute nonsense! I quote what the website says below and my comments are in red next to them.

- “Usually, they require a minimum daily payment regardless of your sales.” – Um, no

- “After approval, the loan is repaid with a portion of your future credit card sales each day.” They’re not loans. This is mostly well settled in the New York Court system. Recently, see this and this

- “You’ll pay for this convenience in very high interest rates” – There are no interest rates

- “MCAs are probably the most expensive borrowing option, with APRs between 25% – 350%.” – Wrong. No APRs can be calculated on a purchase transaction

- “if you are desperate” – That’s a pretty unfair statement to say that a methodology is only for the desperate. New York State is insulting its small business constituency, private companies, and the jobs that have been maintained or created all at the same time

There are also typos and spelling errors throughout the page, as well as conflicting information. The very same page describes MCAs as having between 70% – 200% APR on one side and between 25% – 350% APR on the other side. You don’t need anymore proof that whoever wrote this stuff was just winging it on the fly to make it sound bad. These are the kinds of misleading figures that the CFPB sues financial institutions for and perhaps they should actually take a look at this.

It also says that businesses must accept credit cards. That’s not true either.

It’s strange that a CDFI would go to such great lengths to deliberately misinform small businesses, let alone have a state government foot the bill for them to do it.

Furthermore, as someone who recently used an online marketplace loan for my business, I’m personally offended that my state government would pay to market information that says it was designed to appeal to business owners who have lower credit scores. As my FICO score is over 800, the writer clearly does not understand the product, the market, or the appeal.

More troublesome of course, is that the NYDFS hopes to regulate these industries through language snuck in Governor Cuomo’s budget proposal. Given the above, what could possibly go wrong?

In Canada, Alternative Business Finance Industry Similar, Yet Different

March 8, 2017 David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

“We don’t view ourselves as directly competing with banks,” Gens says, suggesting that his target market is less than prime. It’s a point that his counterparts in the US have made often. But there’s a slight difference with that approach in their market, he adds. “Most Canadian consumers are prime.” And unlike the US, the banks are not necessarily portrayed as the enemy in Canada where five major ones dominate the market.

“It’s exceptionally difficult for an alternative small business lender to build a brand,” said Jeff Mitelman, CEO of Montreal-based Thinking Capital, on a panel at the LendIt Conference. Despite that, his company has funded half a billion dollars to 15,000 unique businesses over the last 10 years. A panelist besides him half-joked however, that there is such an inherent conservatism with Canadian small business owners that some don’t even want to grow and are content with running lifestyle businesses.

But of the deals that are getting done, they’re often acquired through direct marketing. “The ISO market is not like it is in the US,” Gens says. “There’s just a handful of them.” Where there are ISOs though, competitive pressures usually follow. He says that they’re competing on at least 50% of the deals they work on, in part because of these ISOs. Stacking is happening in Canada too, he admits. “It’s not as crazy as it is in the states,” he contends. “Philosophically, it doesn’t align with our business.”

Some deals in Canada are actually being facilitated by US ISOs, he acknowledges, before clarifying that they should be aware that they will get paid in Canadian dollars, which at present are worth about a three quarters of an American dollar. They are in a different country after all.

Gens and others like Bruce Marshall, vice president of British Columbia-based Company Capital, agree that OnDeck’s push into Canada has been good for the entire industry. Six months ago, Marshall said, “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

Over time, they believe alternatives will become more mainstream. For Gens, part of that is about doing right by the customer. “We pride ourselves on being very transparent,” he says. There are no hidden fees with their products and they can make things easy like use APIs to access a merchant’s bank statement history, provided an applicant wants to do it that way. “More than 50% of merchants are still submitting bank statements,” he says. That trend is still pretty much true in the US as well. “There’s a much lower incidence of fraud in Canada,” he asserts. It’s a nation of small businesses he’s content to serve.

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate

How Banks Are Coming Back to SME Lending (Summary)

March 6, 2017

The banks are no longer sitting on the sidelines of small business lending. At LendIt on Monday, a panel featuring representatives from two of the biggest banks in the country, reminded young upstarts that they intended to be the primary capital sources for small businesses.

Unlike JPMorgan Chase, which partnered with OnDeck, Bank of America (BoA) decided to build the technology to deliver loans easily and quickly on their own. BoA SVP Nadeem Tufail said that reputational risk had held them back from partnering with a platform back when they were considering it years ago. “We couldn’t make that leap,” he explained, citing factors like cost, which they saw as simply being too high on some platforms to feel comfortable with.

But that doesn’t mean that the opportunity has passed them by. “A Bank of America customer can get funded in 48 hours,” Tufail proclaimed, while adding that a business that doesn’t bank with them can get a loan from them in about 7 days. The bank is also now doing fully automated approvals on a very small scale with a sliver of their best clientele to test the concept.

Meanwhile, Julie Chen Kimmerling, Senior Manager at Chase, made it a point to say that they were also really worried about things like reputational risk but that they found OnDeck to be a perfect fit. The maturity of their management team and platform really impressed them, she said. Still, Chase governs how the loans are underwritten and keeps the customers on their balance sheet. So they haven’t exactly handed the keys over to OnDeck but obviously trust their brand to be affiliated.

BoA recognized that some of their customers were telling them that they shouldn’t have to submit all these documents when the bank should already have access to their financial histories, particularly their cash flow. Tufail said that this was one of the most important factors in their underwriting. “Does the business have cash flow?” he said. “Does the business have liquidity?” The bank should already be able to evaluate these metrics.

“We certainly have an advantage with transactional level data,” Chase’s Kimmerling said of banks doing loan underwriting. And Chase is no amateur in this market. Kimmerling said that her bank had provided $24 billion of credit to US small businesses last year alone, a figure prominently displayed in their last earnings report.

To boot, both banks retain brick & mortar presences around the country, an advantage for small business customers, who they say are pretty likely to visit a branch.

The banks it seems are coming back. Lendio CEO Brock Blake moderated the panel.

Quotes and paraphrases were derived from the panel. The summary is my own analysis of it.