Business Lending

Gale Force Twins

April 24, 2018

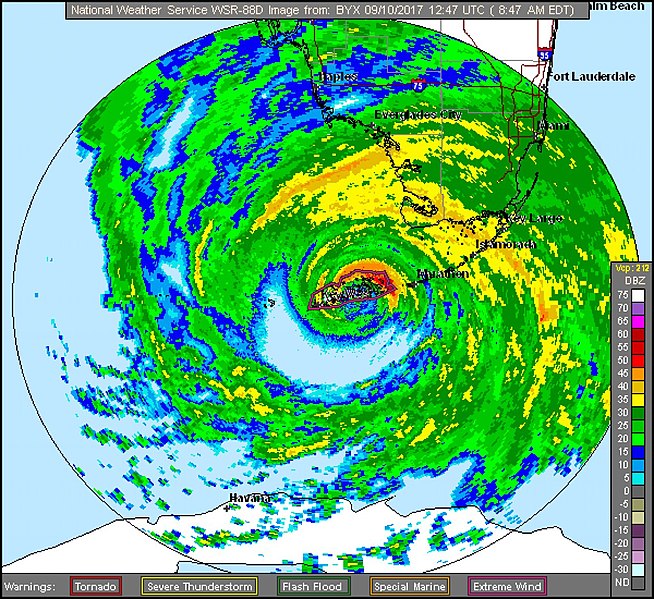

As Hurricane Irma swept through the Caribbean and barreled toward the Florida Keys early last September, Wendy Vila, chief executive, at Unicus Capital evacuated her home in West Palm Beach and decamped to Panama City in the Florida panhandle where “it was just a little bit rainy.”

After safely waiting out Irma, she says, her return south was precarious. The roads were strewn with tree branches and other debris. Fuel was scarce. Many gas stations were either closed or posted signs reading “No Gas.” “Restaurants had run out of food,” Vila adds, “so there was nothing to eat” along the highway.

She returned to West Palm Beach but didn’t stay long. Instead, Vila again drove west, this time across the Florida peninsula to the South Florida city of Naples, not far from where Irma had made landfall. “I went there to volunteer with Samaritan’s Purse for two days,” she says, referring to the Boone, N.C.-based Christian organization that provides humanitarian aid to people in physical need. “Things were a lot worse there than in West Palm Beach,” she reports. “A lot of trees were down, houses were flooded and people had to throw all of their belongings out onto the street.”

Meanwhile, many of the Florida merchants whom Unicus funds were distressed. “If people had no power,” Vila says, “they couldn’t function. A lot of businesses had to close down. For some merchants in the affected areas,” she adds, Unicus extended “a 90-day grace period.”

Vila’s experience with Hurricane Irma – both professionally and personally — is not an isolated one. She is among several business lenders whom deBanked interviewed about the storm and its aftermath. This article grew out of deBanked’s Florida networking event at the Gale Hotel in South Beach in late January. We went back to many of the attendees as well as to other business-funders in The Sunshine State and sought out their experiences before, during and after the powerful tempest.

At one point, Hurricane Irma was the strongest hurricane ever recorded in the Atlantic by the National Hurricane Center. As Irma took dead aim at Florida, it packed sustained winds exceeding 157 miles per hour, earning it the designation of a Category 5 storm, the highest and most destructive. It slammed into the Florida Keys as a Category 4 hurricane, reached the Gulf of Mexico, and then came ashore a second time on Florida’s west coast at Marco Island, just south of Naples, and began traversing the state as a Category 3 hurricane, gradually losing strength. By the time Irma exited Florida, it had been downgraded to a tropical storm. According to the National Hurricane Center, Irma caused an estimated $50 billion in damage in the U.S., making it the fifth-costliest hurricane to hit the mainland.

Financiers and brokers told personal stories of working with and assisting merchants across Florida who sought to regain their lost footing and keep from going — literally — underwater. In many cases, members of the alternative business financing community said, they were simultaneously assisting troubled merchants while they themselves struggled with Irma-occasioned troubles that ranged from inconvenience to hardship.

“I was ten days without power,” says Manny Columbie, funding manager at Axiom Financial, based in South Miami. Columbie, who lives in the residential Westchester district of Miami, not far from the campus of Florida International University, says that he conducts much of his business from his home. That power loss not only constrained his ability to keep working but posed a life-or-death situation for his family: Columbie’s 90-year-old grandmother, who lives with him and his girlfriend, depends on electrical power to operate her oxygen pump.

Fortunately, he says, he had a backup generator, the use of which alternated between providing power for his grandmother’s oxygen and the family’s refrigerator. Meanwhile, his roof was leaking and there was six inches of rainwater swamping the house — the water gushing into the kitchen through the laundry room, dishwasher and even the oven.

Fortunately, he says, he had a backup generator, the use of which alternated between providing power for his grandmother’s oxygen and the family’s refrigerator. Meanwhile, his roof was leaking and there was six inches of rainwater swamping the house — the water gushing into the kitchen through the laundry room, dishwasher and even the oven.

While Columbie saw instances of tempers growing short in Miami’s September heat, he was nonetheless cheered by the way his community responded. “Neighbors were coming by to see if I needed gasoline for my generator,” Columbie says. “People were firing up food on their outside grills. There was no air-conditioning or cold showers but we cooled off by jumping in a neighbor’s pool. I saw a lot of people coming together.”

At the same time, he was doing what he could to assist merchants who did business with Axiom. Only one – a retail clothing store in Miami – was permanently shuttered. One of his clients, Oscar Pratt, owner of Odessy Party Supplies in Miami Gardens, was grateful for a moratorium on daily payments.

“We’re in the business of selling party accessories for events from births to funerals and everything in-between,” Pratt says. “Baby showers, christenings, birthdays, quinceaneras, ‘Sweet Sixteens,’ graduations, weddings, and all kinds of themed parties like Halloween,” he says. “We sell plates and cups, candy bags, cake-toppers, small favors, pinatas…”

Pratt said he’d called his funders ahead of the storm and “requested some leeway” from payments. Once the storm hit – and for two weeks afterward while there was no electricity – the party-supply business was pretty much on hold. “We had a few days without electricity or phone,” he says. “We couldn’t open the doors and do business because we use computer-generated receipts. Our customer base was down to just about nothing. Without electricity, people weren’t working and they weren’t having parties.”

Following the two-week grace period, Pratt says that his funders, which included QuarterSpot, granted a second two-week period of leniency in which Odessy was allowed to make reduced payments. “It was very difficult,” he says. “There was no help from FEMA (Federal Emergency Management Agency) or from our insurance company since we’re on high ground and there were no physical damages, just the electricity.”

He reckoned that Odessy, which boasts annual revenues of $1.2 million, was deprived of roughly $50,000-$60,000 in sales because of Irma. Pratt reports that if his lenders had “played hardball” and demanded that he make his payments, he could have stayed in business thanks to “cash on hand” but it wouldn’t have been easy.

Meantime, his lenders’ forbearance was soon rewarded. By October, business was back to normal and he resumed making payments in full. “As soon as the lights went on,” Pratt says, “the parties started again.”

Similarly, says Paul Boxer, chief marketing officer at Quicksilver Capital in Brooklyn, the ultimate impact of Hurricane Irma on his firm’s funding business was to build trust and cement relationships with clients in South Florida. “We had a full team on board to answer the large number of calls coming in and to assist our merchants with any questions they had,” he says.

Many affected merchants, Boxer reports, were forced to evacuate ahead of the storm. When they returned, it was common for them to discover that their shops and stores sustained flooding damage from the heavy rains and a storm surge. Roofs were blown-off and structures were battered by 100-plus mile-an-hour winds, falling trees, and whipped-up debris. Even businesses that suffered little damage were paralyzed by the loss of electricity, impassable roads, and the absence of customers.

Many affected merchants, Boxer reports, were forced to evacuate ahead of the storm. When they returned, it was common for them to discover that their shops and stores sustained flooding damage from the heavy rains and a storm surge. Roofs were blown-off and structures were battered by 100-plus mile-an-hour winds, falling trees, and whipped-up debris. Even businesses that suffered little damage were paralyzed by the loss of electricity, impassable roads, and the absence of customers.

“Some were down for a few days,” Boxer reports. “Some were down a month to two months. We kept in touch. We were really on top of things with our merchants and asking them what they needed. We even fielded general safety questions and directed them on whom to call with insurance questions and other related business questions. It was good business,” he adds, “because it showed you cared. We were looking to do the right thing by our merchants and they appreciated it.”

Quicksilver typically offered merchants a two-to-three week “reprieve” on payments, Boxer says. For those businesses and entreprenuers whose operations were “completely out of commission” and needed more time, he says, the company suspended payments for as long as two months.

In the end, Quicksilver’s policy of forbearance reaped dividends. It not only built up good will with its customer base but also with the Independent Sales Organizations (ISOs) who’d brokered many of the firm’s Florida deals. “We helped grow that relationship,” Boxer says of the merchant-ISO connection. “They (ISOs) love getting renewals. It’s been a win-win for everybody.”

Doug Rovello, senior managing partner at Fund Simple, Inc., an alternative business lender and broker in Palm Harbor, a beach town just outside Tampa, says the Tampa-St. Petersburg area was spared from severe flooding but “we did experience power outages.” Among his clients, he reports, businesses in the food industry were among the most vulnerable. “I had one restaurant that lost $200,000 in business in the month of September,” he says.

When the electricity went down, grocery stores and bodegas, restaurants, bars, pizzerias, sub shops, delis and luncheonettes suffered outsized losses. Without power, businesses in the food industry were forced to dump spoiled meat, rotting fish, unusable dishes like appetizers and other foodstuffs requiring refrigeration.

When the electricity went down, grocery stores and bodegas, restaurants, bars, pizzerias, sub shops, delis and luncheonettes suffered outsized losses. Without power, businesses in the food industry were forced to dump spoiled meat, rotting fish, unusable dishes like appetizers and other foodstuffs requiring refrigeration.

Rovello reports that the hurricane managed to bollix up the business of one top client, a leading ticket broker in the area with a reputation for obtaining “exclusive” tickets to major events such as A-list rock concerts and featured sporting contests – including the Super Bowl. “He buys tickets in advance and when one big event was canceled he got stuck with $30,000 in tickets that he had to eat,” Rovello says.

Other kinds of businesses that depend on alternative lenders and got hit hard from the loss of power, Rovello observes, were medical clinics, doctors’ offices, pain-management centers, and assisted-living quarters – particularly those south of Sarasota. A number of golf courses also closed down for a couple of weeks, Rovello notes, further impairing the tourism and entertainment economy. “They were not allowed to move any of the damage that was done – poles, trees, et cetera until FEMA got there,” he says.

For some 30 days following Irma’s arrival, Rovello reports that he asked clients to make modest payments – perhaps $100 instead of a $750 monthly payment — “to keep their accounts active.” He also used his connections with FEMA adjusters and interceded with funders on behalf of clients– and even businesses that were not clients – who found themselves in arrears.

While many Floridians were seeking higher ground or hightailing it out of state, Jay Bhatt, who is a senior vice president of marketing at Breakout Capital in McLean, Va., was catching one of the last Jet Blue flights into Orlando to help out his aging parents. They are now in their late 60s and 70s, he reports, and living in a retirement community in Polk County, about ten miles south of Disney World.

Irma was still a Category 1 hurricane with 100 mph winds when it hit Orlando. The electrical grid went down, but Bhatt was able to purchase a generator – the kind designed specifically to provide electricity for oxygen respirators — from Home Depot. During his stay, Bhatt made several car trips in search of fuel, each of which took him probably 35-40 minutes. “We also leveraged some of the neighbors’ sockets,” he says, “but they were so small that the wattage only allowed for the operation of the fridge and a fan.”

Electricity was restored after four or five days. “The fact that it was a retirement community might have been why we got power back so soon while it took two or three weeks for many others,” he reckons.

While Bhatt’s attention was focused on his parents, his employer – which had just offered a blanket hold on payments to its merchant accounts in 11 Texas counties that had been simultaneously inundated and walloped by Hurricane Harvey – now faced the challenge of responding to the second hurricane in two weeks. With Irma, Breakout chose to deal with its customers individually. “We didn’t do an immediate blanket response” as in Texas, Bhatt says, adding: “We were able to contact each one and we only wrote off one small business.”

While Bhatt’s attention was focused on his parents, his employer – which had just offered a blanket hold on payments to its merchant accounts in 11 Texas counties that had been simultaneously inundated and walloped by Hurricane Harvey – now faced the challenge of responding to the second hurricane in two weeks. With Irma, Breakout chose to deal with its customers individually. “We didn’t do an immediate blanket response” as in Texas, Bhatt says, adding: “We were able to contact each one and we only wrote off one small business.”

Rakem Lampkin, senior customer service representative at Pearl Capital, a New York-based alternative funder, says that his firm funds “roughly 175” businesses in South Florida. In addition to those establishments already mentioned as economically reeling because of Irma, such as restaurants, he cited “car dealerships, automotive repair shops and tech companies” as among the hardest hit, especially from the lack of electricity.

Lampkin also noted that many of Pearl’s merchants felt Irma’s wrath when colleges and state schools closed their doors. “Everything from transportation, lunches, sports equipment, even mom-and-pop florists” were slammed, he says, adding: “When the schools shut down, our payments slowed down.”

Pearl provided preferential treatment to merchants on the coast who were granted “a hold on debit payments,” Lampkin says. Even for coastal businesses that remained “structurally sound,” the business owners’ and employees’ “homes were affected, which kept them from getting to work,” he says.

As for businesses situated inland, “We were still sympathetic,” Lampkin says, but after an initial five-day grace-period their discounts were in the range of 66%-75% “so that we could focus our resources toward the people on the coast.”

To monitor the situation from New York, Lampkin says, the company was able to rely on accounts in the local news media, Google Maps, and other Internet sources. “We evaluated the situation case-by-case and week-by-week,” he says.

Jennifer Legg, a co-owner of Rochelle’s Jewelry & Watch Repair at the Indian River Mall in Vero Beach, is a Pearl-funded merchant who says she shut down the family-run business “for six or seven days” after Irma while the electricity went out. “Trees were down and a lot of people lost food and trailers, but we were not impacted as much as we were supposed to be,” she remarked.

Most of the shop’s business consists of customers stopping in for a new battery or a watch-band. Once they’re in the store, there’s a chance that they’ll purchase something else. But Irma put the kibosh on mall traffic. “A lot of people left the state, so that hurt business,” Legg says.

The store – which records annual sales of about $200,000 — lost probably $10,000 in revenue because of Irma. “It was very hard for that month of September,” Legg says. “Even after the doors opened, it was dead. No money came in for about two weeks.”

Fortunately, though, her capital source “did not take money out for a week,” she says. “If they’d kept taking it out,” she added, “we would have defaulted.”

Finitive Launches Alternative Lending Investment Platform

April 24, 2018 Finitive, which brings capital from institutional investors to alternative lending companies, announced earlier this month that it received capital commitments totaling $1.3 billion. It also officially launched its financial technology platform.

Finitive, which brings capital from institutional investors to alternative lending companies, announced earlier this month that it received capital commitments totaling $1.3 billion. It also officially launched its financial technology platform.

According to founder and Executive Chairman Jon Barlow, the company, which was founded last August, has two kinds of clients: institutional investors and alternative lending companies. So far, the company has four alternative lender clients.

“We are very selective [with our lending clients],” Barlow said. “We are not a list service.”

Among these four lenders, Barlow told deBanked that $1 billion has been committed from institutional investors and $250 to $300 million has actually been funded. Finitive gets paid by its lender clients based on how much money gets funded of the capital they provide from institutional investors. Finitive does not charge its institutional investor clients.

“We perform due diligence for [institutional investors] so that they don’t have to, and we give them our due diligence files for free,” Barlow said. “We don’t think anyone has ever done this. We think it’s revolutionary.”

Through the Finitive platform, institutional investors, along with banks, insurance companies and fund managers can directly access proprietary, alternative lending transactions that are vetted by a team of highly trained credit professionals, Barlow said. For the lending companies, or “originator partners,” the platform allows them to raise capital from a variety of sources.

“We are unique for the institutional investor community because we show [institutional investors] highly vetted transactions,” Barlow said.

Barlow estimates that it takes roughly 500 hours and several hundred thousand dollars to perform proper institutional due diligence on an alternative lending transaction, and Finitive does this for free for investors. So this also benefits participating lenders that now have access to more funds. Finitive is based in New York and has 11 full-time employees.

Boiler Rooms Are Not Brands, Kabbage CEO Says

April 21, 2018

Kabbage CEO Rob Frohwein has a knack for speaking his mind at lending conferences and LendIt two weeks ago was no different. Below are some of the most notable quotes from his April 10th presentation.

On building a brand

Unfortunately, in the online lending space, most companies basically think that boiler rooms = brand. Boiler rooms don’t equal brand. They have these huge call shops and that’s what they’re focused on. That doesn’t create brand. It just doesn’t. You have to spend money in order to build a brand over time. You have to have a brand obviously from a user experience and a customer service experience that people love. That’s how you build a brand.

We’ve invested over $125 million into building our brand specifically. We don’t use brokers and brokers are those 3rd parties that go out and find loans for you, but they don’t represent your company in the process.

How 2018 differs from 2015

About 6 months ago, I was asked to speak on a panel and it wasn’t this conference. And so, I got on the phone with the conference organizer and he said to me “Hey, we’d like to do a panel on fintech and bank partnerships.” Total yawn. 2015 called. They want their panel topic back. I mean, after all, there are probably more panels on fintech and bank partnerships than there are actual conversations going on between fintechs and banks. 2018 is all about relationships.

If the only thing you’re doing is lending money online, it’s going to go the way of the dinosaur. It’s very important. It doesn’t mean that the companies are gonna blow up. It doesn’t mean that there’s going to be any challenges, you know, trying to grow that business, but they’re not going to be the kind of exciting companies that we saw just a few years ago.

The only way to build substantial enterprise value is to be in a position to expand your brand’s offerings.

On whether or not your relationship with the customer can naturally extend to other products

I’ve heard lots of people say I had 2 million customers so I can sell them an auto loan. Actually, you can’t. That’s not the way it works. That’s not the way you build the company. You can certainly try, but the question becomes do you have implicit permission from the customer to make this kind of an offer?

How close is the next product you’re launching from both the function and a brand perspective to your last product? Right? Is it close? Smith & Wesson came out with a lot of bicycles. I am not sure what amendment covers bicycles, but they did not do great with the Smith & Wesson bicycles as far as I know.

The challenge is that most online lending companies don’t really have much of an idea about what their customers want or need because they only have basic credit info at the time of qualification and they also are just getting repayment information. That does not equal understanding the customer.

On engaging with your customers

If you’re not interacting with them very often, then they’re not thinking about you very often.

Kabbage customers take 20 loans over 4 to 5 years, 4-5 loans a year every year. We have that many positive interactions. Our competitors average 2.2.

Finally, I really think of this as the potato chip dream. And I think about Amazon a lot when I talk about the potato chip dream. What that dream is the day that Kabbage is able to sell bags of potato chips to our customers and our customers are like “of course, I’m gonna buy potato chips from Kabbage, why would I buy them from anybody else?” That will mean that Kabbage is worth hundreds of billions and our customers are incredibly happy in the process because it necessarily means that we will provide them with every product and service between where we are today and potato chips tomorrow. And that’s really the key for what we’re trying to accomplish, is allow us to expand our offerings in a natural evolutionary way and take care of our customers. And I really do think that all of us here should think about that as well especially if you’re running an online lending company. Focus back on the customer. Build those relationships. Figure out how to take it to the next level.

Wayward Merchants

April 19, 2018

Wayward merchants and outright criminals are continuing to bilk the alternative small-business funding industry out of cash at a dizzying pace. In fact, an estimated 23 percent of the problematic clients that funders reported to an industry database in 2017 appeared to have committed fraud, up from approximately 17 percent in the previous year. That’s according to Scott Williams, managing member of Florida-based Financial Advantage Group LLC, who along with Cody Burgess founded the DataMerch database in 2015. Some 11,000 small businesses now appear in the database because they’ve allegedly failed to honor their commitments to funders, Williams says.

Whether fraudulent or not, defaults remain plentiful enough to keep attorneys busy in funders’ legal departments and at outside law firms funders hire. “I do a lot of collections work on behalf of my cash-advance clients, sending out letters to try to get people to pay,” says Paul Rianda, a California-based attorney. When letters and phone calls don’t succeed, it’s time to file a lawsuit, he says.

Lawsuits become necessary more often than not by the time a funder hires an outside attorney, according to Jamie Polon, a partner at the Great Neck, N.Y.- based law firm of Mavrides Moyal Packman Sadkin LLP and manager of its Creditors’ Rights Group. “Typically, my clients have tried everything to resolve the situation amicably before coming to me,” he observes.

That pursuit of debtors isn’t getting any easier. These days, it’s not just the debtor and the debtor’s attorney that funders and their attorneys must confront. Collections have become more difficult with the recent rise of so-called debt settlement companies that promise to help merchants avoid satisfying their obligations in full, notes Katherine Fisher, who’s a partner in the Maryland office of the law firm of Hudson Cook LLP.

Meanwhile, a consensus among attorneys, consultants and the funders themselves holds that the nature of the fraudulent attacks is changing. On one side of the equation, crooks are hatching increasingly sophisticated schemes to defraud funders, notes Catherine Brennan, who’s also a partner in the Maryland office of Hudson Cook LLP. On the other side, underwriters and software developers are becoming more skilled at detecting and thwarting fraud, she maintains.

Meanwhile, a consensus among attorneys, consultants and the funders themselves holds that the nature of the fraudulent attacks is changing. On one side of the equation, crooks are hatching increasingly sophisticated schemes to defraud funders, notes Catherine Brennan, who’s also a partner in the Maryland office of Hudson Cook LLP. On the other side, underwriters and software developers are becoming more skilled at detecting and thwarting fraud, she maintains.

Digitalization is fueling those changes, says Jeremy Brown, chairman of Bethesda, Md.-based RapidAdvance. “As the business overall becomes more and more automated and moves more online – with less personal contact with merchants – you have to develop different tools to deal with fraud,” he says.

A few years ago, the industry was buzzing about fake bank statements available on craigslist, Brown recalls. Criminals who didn’t even own businesses used the phony statements to borrow against nonexistent bank accounts, and merchants used the fake documents to inflate their numbers.

Altered or invented bank statements remain one of the industry’s biggest challenges, but now they’ve gone digital. About 85 percent of the cases of fraud submitted to the DataMerch database involve falsified bank documents, nearly all of them manipulated digitally, Williams notes.

Merchants alter their statements to overstate their balances, increase the amount of their monthly deposits, erase overdrafts, or hide automatic payments they’re already making on loans or advances, Williams says. Most use software that helps them reformat and tamper with PDF files that begin as legitimate bank statements, he observes.

To combat false statements, alt funders are demanding online access to applicants’ actual bank accounts. Some funders ask for prospective clients’ usernames and passwords to examine bank records, but applicants often consider such requests an invasion of their privacy, sources agree.

That’s why RapidAdvance has joined the ranks of companies that use electronic tools like DecisionLogic, GIACT or Yodlee to verify a bank balance or the owner of the account and perform test ACH transfers – all without needing to persuade anyone to surrender personally identifiable information, Brown says.

Other third-party systems can use an IP address to view the computing device and computer network that a prospective customer is using to apply for credit, Brown says. RapidAdvance has received applications that those tools have traced to known criminal networks. The systems even know when crooks are masking the identity of the networks they’re using to attempt fraud, he observes.

RapidAdvance has also developed its own software to head off fraud. One program developed in-house cross references every customer who’s contacted the company, even those who haven’t taken out a loan or merchant cash advance. “People who want to defraud you will come back with a different business name on the same bank account,” Brown says. “It’s a quick way to see if this is somebody we don’t want to do business with.”

Sometimes businesses use differing federal tax ID numbers to pull off a hoax, according to Williams at DataMerch. That’s why his company’s database lists all of the ID numbers for a business.

All of those electronic safeguards have come into play only recently, Brown maintains. “We didn’t think about any of this five years ago – certainly not 10 years ago,” he says. In those days, funders were satisfied with just an application and a copy of a driver’s license, he remembers.

Since then, some sage advice has been proven true. When RapidAdvance was founded in 2005, the company had a mentor with experience at Capital One, Brown says. One piece of wisdom the company guru imparted was this: “Watch out when the criminals figure out your business model.” That’s when an industry becomes a target of organized fraud.

As that prediction of fraud has become reality, it hasn’t necessarily gotten any easier to pinpoint the percentage of deals proposed with bad intent. That’s because underwriters and electronic aids prevent most fraudulent potential deals from coming to fruition, Brown notes. The company looks at the loss rates for the deals that it funds, not the deals it turns down.

Brown guesses that as many as 10 percent of applications are tainted by fraudulent intention. “It’s meaningful enough that if you miss a couple of accounts with significant dollar amounts,” he says, “then it can have a pretty negative impact on your bottom line.”

Some perpetrators of fraud merely pretend to operate a small business, and funders can discover their scams if there’s time to make site visits, Rianda notes. Other clients begin as genuine entrepreneurs who then run into hard times and want to keep their doors open at all costs, sources agree.

Applicants sometimes provide false landlord information, something that RapidAdvance checks out on larger loans, Brown notes. Underwriters who call to verify the tenant-landlord relationship have to rely upon common sense to ferret out anything “fishy,” he advises.

Applicants sometimes provide false landlord information, something that RapidAdvance checks out on larger loans, Brown notes. Underwriters who call to verify the tenant-landlord relationship have to rely upon common sense to ferret out anything “fishy,” he advises.

Underwriters should ask enough questions in those phone calls to determine whether the supposed landlord really knows the property and the tenant, which could include queries concerning rent per square foot, length of time in business and when the lease terminates, Brown suggests. All of that should match what the applicant has indicated previously.

Lack of a telephone landline may or may not provide a clue that an imposter is posing as a landlord, Brown continues. Be aware of a supposed landlord’s verbal stumbles, realize something’s possibly amiss if a dubious landlord lacks of an online presence, note whether too many calls to the alleged landlord go into voicemail and be suspicious if a phone exchange with a purported landlord simply “feels” residential instead of commercial, he cautions.

Reasonable explanations could exist for any of those concerns, but when in doubt about the validity of a tenant-landlord relationship it pays to request a copy of the lease or other type of verifications, according to Brown. Then there are the cases when the underwriter is talking to the actual landlord, but the applicant has convinced the landlord to lie. It could happen because the landlord might hope to recoup some back rent from a merchant who’s obviously on the verge of closing up shop.

Occasionally, formerly legitimate merchants turn rogue. They take out a loan, immediately withdraw the funds from the bank, stop repaying the loan, close the business and then walk or run away, notes Williams. “We view that as a fraudulent merchant because their mindset all along was qualifying for this loan and not paying it back,” he says.

Collecting on a delinquent account becomes problematic once a business closes its doors, Rianda notes. As long as the merchant remains in business, funders can still hope to collect reduced payments and thus eventually get back most or all of what’s owed, he maintains.

In another scam sometimes merchants whose bank accounts are set up to make automatic transfers to creditors simply change banks to halt the payments, Brown says. That move could either signal desperation or indicate the intent to defraud was there from the start, he says.

Merchants with cash advances that split card revenue could change transaction processors, install an additional card terminal that’s not programmed for the split or offer discounts for paying with cash, but those scams are becoming less prevalent as the industry shifts to ACH, Brown says. Industrywide, only 5 percent to 10 percent of payments are collected through card splits these days, but about 20 percent of RapidAdvance’s payments are made that way.

Merchants occasionally blame their refusal to pay on partners who have absconded with the funds or on spouses who weren’t authorized to apply for a loan or advance, Brown reports. Although that claim might be bogus, such cases do occur, notes Williams of DataMerch. People who own a minority share of a business sometimes manipulate K-1 records to present themselves as majority owners who are empowered to take out a loan, Williams says.

In a phenomenon called “stacking,” merchants take out multiple loans or advances and thus burden themselves with more obligations than they can meet. Whether or not that constitutes fraud remains debatable, Rianda observes. Stacking has increased with greater availability of capital and because some funders purposely pursue such deals, he contends.

Some contracts now contain covenants that bar stacking, notes Brennan of Hudson Cook. As companies come of age in the alt-funding business, they are beginning to employ staff members to detect and guard against practices like stacking, she says.

Moreover, underwriting is improving in general, according to Polon “The vetting is getting better because the industry is getting more mature,” he says. “The underwriting teams have gotten very good at looking at certain data points to see something is wrong with the application – they know when something doesn’t smell right.” They’re better at checking with references, investigating landlords, examining financials and requesting backup documentation, he contends.

Despite more-systematic approaches to foiling the criminal element and protecting against misfortunate merchants, one-of-a-kind attempts at fraud also still drive funders crazy, Brown says. His company found that a merchant once conspired with the broker who brought RapidAdvance the deal. The merchant and the broker set up a dummy business, transferred the funds to it and then withdrew the cash. “The guy came back to us and said, ‘I lost all the money because the broker took it,’” he recounts. “Why is that our problem?” was the RapidAdvance response.

Although such schemes appear rare, some funders are developing methods of auditing their ISOs to prevent problems, notes Brennan. They can search for patterns of irregularities as an early-warning system, she says. It’s also important to terminate relationships with errant brokers and share information about them, she advises, adding that competition has sometimes made funders reluctant to sever ties with brokers.

Although fraud’s clearly a crime, the police rarely choose to involve themselves with it, Brown says. His company has had cases where it lost what it considered large dollar amounts – say $50,000 – and had evidence he felt clearly indicated fraud but the company couldn’t attract the attention of law enforcement, he notes.

Although fraud’s clearly a crime, the police rarely choose to involve themselves with it, Brown says. His company has had cases where it lost what it considered large dollar amounts – say $50,000 – and had evidence he felt clearly indicated fraud but the company couldn’t attract the attention of law enforcement, he notes.

Rianda finds working with law enforcement “hit or miss,” whether it’s a matter of defaulting on loans or committing other crimes. In one of his cases an employee forged invoices to steal $100,000 and the police didn’t care. In another, someone collected $3,000 in credit card refunds and went to jail. If the authorities do intervene, they may seek jail time and sometimes compel crooks to make restitution, he notes.

“Engaging law enforcement is generally not appropriate for collections,” according to Fisher from Hudson Cook. However, notifying police agencies of fraud that occurs at the inception of a deal can sometimes be appropriate, says Fisher’s colleague Brennan, particularly when organized gangs of fraudsters are at work.

At the same time, sheriffs and marshals can help collect judgments, Polon says. He works with attorneys, sheriffs and marshals all over the country to enforce judgments he has obtained in New York State, he says. That can include garnishing wages, levying a bank account or clearing a lien before a debtor can sell or refinance property, he notes.

When Rianda files a lawsuit against an individual or company in default, the defendant fails to appear in court about 90 percent of the time, he says. A court judgment against a delinquent debtor serves as a more effective tool for collections than does a letter an attorney sends before litigation begins, Rianda notes.

But even with a judgment in hand, attorneys and their clients have to pursue the debtor, often in another state and sometimes over a long period of time, Rianda continues. “The good news is that in California a judgment is good for 10 years and renewable for 10,” he adds.

So guarding against fraud comes down to matching wits with criminals across the country and around the world. “It makes it hard to do business, but that’s the reality,” Brown concludes. Still, there’s always hope. To combat fraud, funders should work together, Brennan advises. “It’s an industrywide problem … so the industry as a whole has a collective interest in rooting out fraud.”

Demand for Tax Guard Grows, and Receives Private Equity Investment

April 19, 2018 Hansen Rada, CEO, Tax Guard

Hansen Rada, CEO, Tax GuardTax Guard announced on Monday that it received an investment from Falfurrias Capital Partners, a Charlotte, NC-based private equity firm.

“What really excites me about [partnering with Falfurrias Capital Partners] is the breadth of experience that they bring to the table,” said CEO and co-founder Hansen Rada. “They have some real icons in banking that are now going to be members of the board and will continue to assist us from a strategic point of view as we begin to expand our platform.”

Tax Guard generates tax liability research on companies and individuals for lender clients that want a clearer picture of who they might be lending to.

“Across the board, 22 percent of businesses owe money to the Internal Revenue Service, and no lien has been filed,” Rada told deBanked. “In other words, there’s no public record of this. That’s where Tax Guard [comes in]. We identify these tax liabilities before the lien has been filed to notify lenders of potential risk.”

Rada said that since 2010 tax liens have dropped by 70 percent, yet the number of people and businesses that owe money has gone up steadily. This is because of a tactic the IRS uses, according to Rada, where it issues fewer liens which allows people’s credit scores to rise. When credit scores rise, people and businesses can take out loans that they can ultimately use to pay back to the government in taxes.

Regardless of whether or not this is a tactic, in addition to fewer liens, even existing liens have become more difficult for lenders to see. In March, Experian, one of the three major credit bureaus, said that it would stop reporting all tax liens from its consumer credit reporting database this week. And the other two major credit bureaus, Equifax and Transunion, have already stopped including civil judgments and tax liens on their consumer credit reports.

Rada agreed that these developments are positive for his business and said that this continues to validate the company’s value proposition. Specifically, Tax Guard provides reports to commercial lenders to let them know, in real time, if a business fails to pay its taxes.

“Our clients are anyone that cares if the people or businesses they are lending money to owe money to the IRS,” Rada said.

Rada said Tax Guard does business with about 350 lenders, including a national bank, community banks and alternative online lending companies.

So how does Tax Guard conduct its research? It contacts the IRS directly about specific people and companies. For the most part, this data-collecting process can be done by anyone. But it takes a long time and Rada said they are able to bypass the “middleman,” like public record searches and county courthouses. Tax Guard gets paid by its clients per business/individual report that it produces, and it customizes pricing based on volume.

As part of the investment deal, four people connected to Falfurrias Capital Partners will be joining Tax Guard in some capacity. Chris Marshall, a co-founder of Capital Bank and previously a senior executive at Bank of America, will join Tax Guard as Executive Chairman. Marc Oken, co-founder of Falfurrias Capital Partners and a former Bank of America CFO, will join the Tax Guard board, along with Geordie Pierson, a principal at Falfurrias Capital Partners, and Joe Price, a former Bank of America CFO.

Founded in 2009, Tax Guard has 65 employees at its office in Boulder, CO.

Ascentium Capital Surpasses $4 Billion in Originations

April 18, 2018 Texas-based lender Ascentium Capital announced last week that it had surpassed $4 billion in origination volume since the company was founded in 2011.

Texas-based lender Ascentium Capital announced last week that it had surpassed $4 billion in origination volume since the company was founded in 2011.

The company has two key channels of business. The vendor channel, in which Ascentium creates custom finance programs for clients like equipment manufacturers, distributors and resellers. It calls these clients its “vendor partners.”

“We do a lot of our business with vendor partners, typically [a company] selling something to a small business,” said Ascentium Capital CEO Tom Depping.

The other business channel is a direct channel where Ascentium makes direct loans to small and medium sized businesses of up to $250,000. Depping told deBanked that the company’s direct channel makes up about 30 to 40 percent of its business. Not an insignificant percentage. But he said that the company’s primary business is equipment finance via vendor partners.

Ascentium gets its leads from an internal sales team of 120 people and Depping said that he anticipates adding 50 additional sales people this year. Why the significant growth?

“Our award-winning finance platform, elevated levels of efficiencies and our personalized service continue to drive demand for our financial products,” said Depping. “Everything with us is very simple and very fast.”

The company currently employs 250 people with headquarters in Kingwood, TX, near Houston, with smaller offices in Dover, NH and Irvine, CA. Depping also counts 30 to 40 locations throughout the country where Ascentium Capital sales people either work from home or in micro-offices of one to two people.

World Business Lenders Responds to the New York Post Story

April 13, 2018

A controversial story published in the New York Post earlier this week about World Business Lenders has drawn a response from the company. The text below was circulated by email to all World Business Lenders employees. With permission, it is being republished here.

——-

As you may be aware, an article appeared earlier this week in a local tabloid which described entirely unsubstantiated allegations against our company and members of its senior management team made by a disgruntled former employee. Because the allegations are as inflammatory as they are baseless, I thought you should hear from me, since I am responsible for the day-to-day operation of the company’s business and ensuring compliance with its policies. Nevertheless, I am accountable to WBL’s Board of Managers. As soon as we became aware of these false allegations, we alerted the Board, including retired U.S. Congressman Edolphus Towns, who chairs the Board committee which focuses on WBL’s reputation in the business community. During his many decades of distinguished service to our country, Congressman Towns chaired the U.S. Congressional Black Caucus and the U.S. Committee on Oversight and Government Reform.

First, the allegations of race discrimination are patently false. I am very proud of WBL’s unwavering commitment to the practice of providing equal employment opportunities to all of its employees and applicants; our company has zero tolerance for employment discrimination or retaliation of any type. And, I want to remind you that, if at any time you feel you are being treated unfairly at work, for any reason, WBL’s policy encourages you to surface and escalate such concerns.

Second, I want to address this disgruntled employee’s outrageous and untrue allegations that WBL defrauded the State of New Jersey. Since we moved to Jersey City in 2016, we have been welcomed with open arms by the State and maintained a cooperative and constructive relationship. WBL has participated in and supported State programs designed to provide employment to some of New Jersey’s most vulnerable residents. We continue to enjoy our partnerships with various State agencies, including our ongoing grant from the Economic Development Authority. To be clear, at no time has any agency of the State of New Jersey expressed any concerns or reservations about our Company or its activities. Rather, we have been commended for our contributions to the economy, both locally and on a state-wide basis.

Finally, I want to assure you that WBL is not in the habit of succumbing to poorly veiled financial demands, and we will not do so here.

– Doug Naidus, CEO

Lendio’s New Turndown Program Grows

April 11, 2018 Lendio, the marketplace for borrowers and lenders, announced on Monday that its Turndown program has facilitated nearly $60 million in loans in less than a year since its launch last summer. The Lendio Turndown program allows participating lenders to refer borrowers to the Lendio marketplace that have been declined.

Lendio, the marketplace for borrowers and lenders, announced on Monday that its Turndown program has facilitated nearly $60 million in loans in less than a year since its launch last summer. The Lendio Turndown program allows participating lenders to refer borrowers to the Lendio marketplace that have been declined.

“Instead of just saying ‘No’ to a customer and wishing them the best of luck, we’ve established this Turndown program where a lender can say ‘Unfortunately, [you’re] not a great fit for us, but we work directly with Lendio and they have a marketplace and other loan options,’” Lendio CEO Brock Blake told deBanked.

The lender has an incentive to refer a declined customer to the Lendio marketplace because the lender gets a revenue share if the customer it declined is funded by another lender on the Lendio marketplace.

“We’re very excited about the Turndown program because it allows us to deepen the relationships we have with our lenders…and it also helps [lenders] monetize and recoup some of their marketing spend,” Blake said.

While the Turndown program started in beta about two years ago, it wasn’t launched until the second quarter of 2017. So far, the program has 20 lender partners, some of which are not the same as the 70 participating lenders on the Lendio marketplace platform. Blake told deBanked that he hopes all 70 lenders will join the Turndown program, as well others, including banks.

Blake also said that most people think a “turndown” automatically means that a borrower has across-the-board bad credit. He concedes that this could be the case, but also acknowledged that there are a variety of loan products that have different credit requirements.

“If a borrower comes in for an equipment loan and they are not going to qualify for an equipment loan, then they might be declined,” Blake said. “But they might qualify for a working capital loan.”

Based in Salt Lake City, UT, the company was founded in 2011 and also has an office in New York. Of about 150 employees, 100 work at the headquarters in Salt Lake City and 50 work in New York.