Business Lending

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

What Happened to OnDeck? (ONDK)

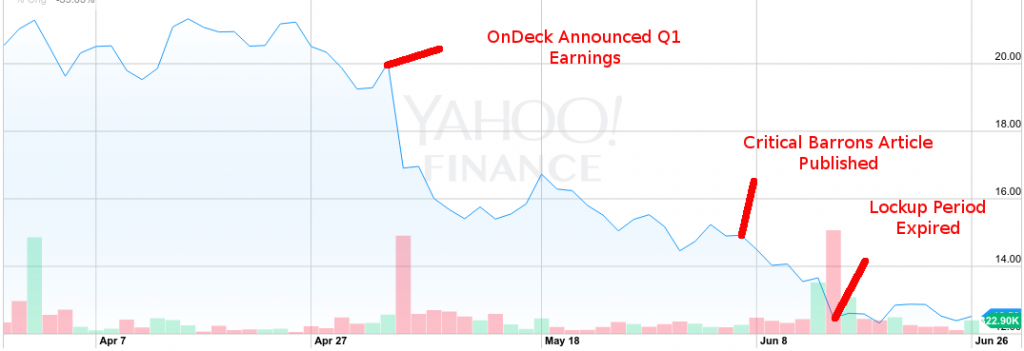

June 29, 2015The lockup expiration came and went but the fall of OnDeck’s stock price started much before that. There were no insider stock sales reported to the SEC since shares became unrestricted anyway.

There’s very little trading volume on an average day and investors on the big message boards either ignore this stock or don’t understand it.

The trend started on May 4th when they released Q1 earnings. The direction wasn’t very much different than Q4. Loan volume went up, interest rates came down, and no profits were to be had, nor were any expected for the rest of the year.

The market interpreted decreasing interest rates as pressure from competitive forces however and down went the stock price.

OnDeck’s execs insisted that they had lowered rates as part of a deliberate strategy to create stickier customers and attract new borrowers. CEO Noah Breslow himself said during the previous 2014 Q4 earnings call that “there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they [small businesses] typically just take that offer that OnDeck has provided to them.”

His theory is supported by the results of Lending Tree’s recent survey that revealed nearly 60% of small businesses did not comparison shop business loans online during their loan application process.

It’s possible though that the drop had little to do with OnDeck’s actual performance. That same day, Goldman Sachs hinted that they would be joining the tech-based lending field when they announced the hire of Harit Talwar from Discover Financial Services.

But before they had a chance to recover, Barrons published a story that was highly critical of OnDeck just a month later on June 5th. “It’s a subprime lender in dot-com clothing,” the author wrote. It was a tough characterization for them to refute, what with their 50% interest rates and double digit percentage charge-offs and all.

And then the lockup expiration on June 15th coincided with the big reveal of Goldman’s intentions to compete in the marketplace. News sources that picked up the story predicted that the move would impact online lenders like Lending Club and OnDeck. OnDeck’s stock hit a record low that day.

OnDeck has been stuck in the 12s ever since. Can they dig themselves out?

If competition is a factor in the market’s perception, and it probably should be, then investors should keep an eye on the industry’s other top players. OnDeck is not alone in this space and Goldman Sachs will be in for a bigger fight than they probably expect.

Source: deBanked’s May/June Magazine issue

The CFPB is Pretty Busy With Actual Consumers

June 28, 2015 It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

There is currently no categorical option to report business loan or merchant cash advances on their website and the complaints lodged by consumers pertain to very basic consumer problems, such as issues with their credit cards or student loans.

Here’s an example of a CFPB complaint:

2009 XXXX XXXX, XXXX XXXX Thursday of every month I got pulled from class to get a new loan for my living and tuition expenses. I was at XXXX for one year and if I didn’t go to sign the papers for my new loan every month I wouldn’t be able to continue my classes to XXXX. I missed out on important class information and had to make them up on my own time. Homework and other hands on tasks became more difficult to accomplish if I didn’t make up the lost time going to sign loan papers. I was told a rough amount that my school loan would be. About {$15000.00}. I started paying {$120.00} a month for my loan agreement then Genesis Lending increased it to {$190.00}. I called to ask why the increase in payment amount each month. I was told they saw i had a higher income so they adjusted the payment accordingly. Is that legal? I’ve been paying this amount for 6 years and still owe {$13000.00}. I called Genesis Lending and come to find out they have been rolling over all the interest I pay on the loan every year. So all I’m paying is interest basically for the last 6 years. I don’t think I ‘m being treated fairly or legally.

Many complaints are just like this, where consumers are not actually reporting illegal activity but instead using the CFPB to vent their frustration. In this situation, the victim was busy with homework and wasn’t sure how their student loan worked so they filed a complaint with the federal government…

The end result was that the lender responded by saying it wasn’t really their problem, the borrower didn’t dispute this response and the CFPB marked the case as closed. Seems like a great use of everybody’s time.

In the handful of presentations I’ve attended by the CFPB, they said they often find themselves redirecting complaints to the business that the consumer is complaining about much like the BBB would do.

The Challenges in Offering Financing to Latino Businesses

June 20, 2015 The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The SBA is the largest guarantor in the U.S. and does not offer any specific minority business loan program to Latinos. The U.S. Hispanic Chamber of Commerce offers advice to Latino business owners, but does not offer any loans. Traditional banks continue to maintain stringent guidelines for all businesses. Alternative finance companies and online lenders have a long way to go to tap into this

niche market.

Alternative lenders, online lenders and peer-to-peer lenders can cater to this niche market, but it requires a lot of resources and knowledge. We can categorize Latino businesses into one broad category. However, as a Hispanic entrepreneur, my experience has been that the Latino business community is complex in nature.

Latino Businesses by Age Groups

There are two types of Latino entrepreneurs. The older generation tends to be within the age range of 45 to 70 years old. These business owners are not accustomed to doing business over the Internet, email, fax, or phone. Online lenders may have difficulties in retrieving information from these clients. This group has a high level of distrust in doing business via the Internet. The majority of our clients within this age group are accustomed to doing business face to face. This sales and marketing strategy can be very expensive for lenders, unless you have a team of field agents. The younger generation of this group is made up of Latino entrepreneurs in the age range of 25 to 45. This group is more accustomed to using online banking and online systems. Forbes recently reported that, “With a median age of 28 years old, the timing is ripe for organizations/brands to make a firm commitment to the Hispanic consumer.”

Family Decisions and Delayed Gratification

Despite the age category, many Latino businesses are family-based. Based on my experience, the decision making process is made among family members. You could offer a $50,000 loan at a cost of factor of 1.30 to the husband and he may need to consult with his wife and his children before he signs his John Hancock. This makes the decision-making

process challenging.

Manuel Cosme Jr., the chair of the National Federation of Independent Businesses (NFIB) Leadership Council in California and co-founder of Professional Small Business Services in Vacaville, California has said, “Family plays a big role in Hispanic culture, so naturally it plays a big role in Hispanic-run businesses.”

Trust Factors

Even if you have a Latino staff or bilingual staff, Latino business owners need to trust you in order to gain their business. You will need to build good rapport with these businesses to get them to fill out a loan application and send it via fax, email or online. Latinos are accustomed to traditional banking methods and brick and mortar businesses.

“When we looked at online US Hispanics in 2006, there were four main roadblocks to US Hispanic e-Commerce adoption: 48% of online Hispanics did not want to give out personal financial information; 46% wanted to be able to see things before buying; 26% had heard about bad experiences purchasing online; and 23% did not have access to a credit or debit card,” says Roxana Strohmenger, Director in charge of Data Insights Innovation at Forrester. These are some of the challenges that we face by conducting our business in a digital manner.

According to mediapost.com, only 32% of online Hispanics use the Internet for their banking needs. In order for online lenders to succeed with this marketplace, U.S. banks need to do more to market to Hispanics online. Alternative lenders need to understand that there are barriers to entry in this marketplace.

Social Media

The Pew Research Center conducted a study that clearly indicates the usage of social media by Hispanics. Accordingly, 80 percent of Hispanic adults in the U.S. use social media and the same study revealed that Latino Internet users admitted to using Facebook as the leading social platform. A lot of business owners love to show the storefront, their family working in their businesses, and other images. You should consider Facebook as part of your overall marketing strategy to tap into this marketplace.

Going overseas

Going overseas

Another option to consider is going overseas. CAN Capital set up an operation in Costa Rica mostly for their business processing services. In fact, we at Lendinero decided to do something different that no one else is doing. We set up the majority of our operations in Central America, consisting of outbound agents, digital marketers, programmers and loan analysts. There are great benefits to having a full bilingual staff overseas and the cost of personnel is less expensive. At the same time, there are huge challenges. Since I am of Hispanic descent, it was easier to set up our operation in a Latin American country. However, there are cultural differences and you have to take into account the economic and political conditions of each country. Setting up a corporation can take 1 to 3 months and it is more expensive than the U.S.

The labor pool is huge, but finding the right people can be a challenge. In addition, training agents, processors, and support staff can be time consuming and you may run for a few months before you begin to see a profit. If your staff did not live in the U.S., you need to train them on U.S. culture, the economy, and other topics.

Furthermore, Internet speed and Internet services can be a challenge. Be prepared to pay a high cost for Internet. And labor laws are not like the U.S. If you fire an employee, you will be forced to pay unpaid vacation and a severance. In addition, you have to take other costs into consideration such as travel costs, lodging, auto leasing, and more.

Lastly, if you don’t know people in the country you plan on setting up in, an outsourced business processing service will charge you more money for rent and other services knowing that you are coming from the U.S. It is highly recommended you pair up with a native or someone who has done business in the countries you consider.

In summary, the Latino business community continues to lack financing. This niche market needs to be educated on the revolutionary paradigm shifts in business lending and online lending. If you can obtain these clients, they are clients for life. Once you obtain them as a client, they are loyal. They will not leave you.

OnDeck Stock Pummeled in Run Up to Lockup Expiration

June 10, 2015 OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

The OnDeck drop may have also been caused by the recent story that appeared in Barrons that labeled the company and the industry they operate in, risky, saturated, and overpriced.

On Deck is a different business. Its profits come from using its own balance sheet to make risky, high-interest rate loans to small businesses. With rivals as large as Goldman Sachs gathering around these companies’ shallow high-tech moats, the competition for quality borrowers will make it tougher for On Deck to keep growing loan originations near a triple-digit pace without loosening underwriting standards. Even in today’s benign conditions, On Deck charges off more than 12% of its loans annually, while its yields on those risky loans have declined for nine straight quarters. It’s a subprime lender in dot-com clothing.

Barrons laid out the case that OnDeck is a lender. OnDeck has always taken the position that they are a tech company. The conflicting market perceptions have made their stock price very chaotic.

OnDeck’s lockup period expires on June 15th.

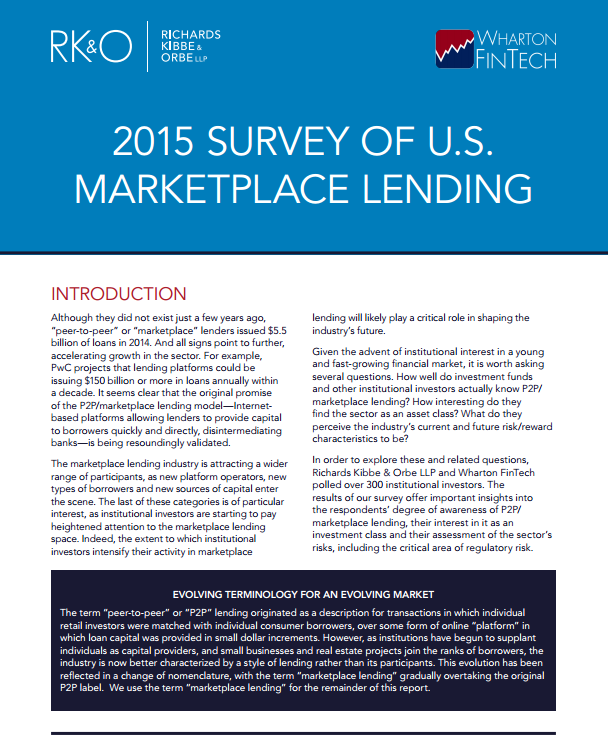

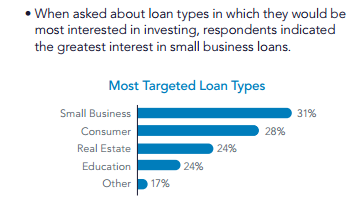

Small Business Lending is King to Institutional Investors

June 2, 2015

Richards Kibbe & Orbe LLP and Wharton FinTech polled more than 300 institutional investors to gauge their thoughts on marketplace lending. They published their findings in a recently released report.

The surveyors seemed surprised that institutional investors indicated their interest in small business loans was greater than that of consumer, real estate, education, and everything else.

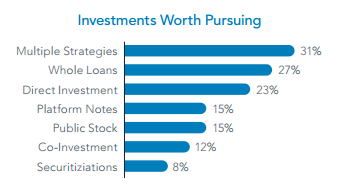

Securitizations ranked lowest on the list of investments worth pursuing and buying whole loans was second only to “multiple strategies.”

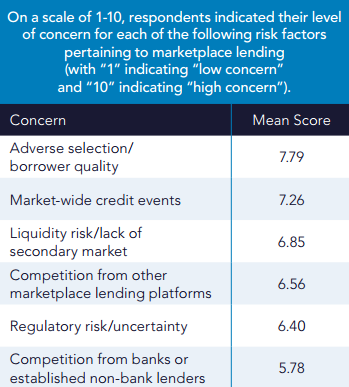

Regulatory risk and uncertainty was low on the list of concerns while borrower quality was the most concerning factor. Curiously, competition was the least concerning of all.

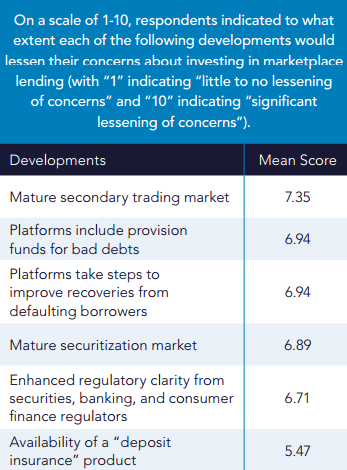

Speaking to the liquidity issues of the assets, institutional investors indicated that the development of a mature secondary trading market was more likely than anything else to lessen their concerns about marketplace lending.

Do any of these results surprise you?

Download the Key Findings report

Broker Business Planning – Selecting the Right Lenders

May 10, 2015Continuing The “Year of the Broker” Discussion

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

2015 is certainly the “Year of the Broker,” as the low barrier to entry into our space, in conjunction with various recruiting advertisements promising lucrative pastures, is attracting a variety of individuals with various levels of professional backgrounds. Some entrants have prior experience as a mortgage broker, insurance agent or banking specialist, while others are less familiar with professional sales and are under the belief that our space welcomes a lucrative introduction. Nevertheless, I believe that new broker entrants must be reminded that this is an entrepreneurial pursuit, rather than a get rich quick procedure, and efficient business planning will play a major part in the success or failure of your venture. A part of this efficient business planning, other than the basics of good resources for accounting, legal, marketing, market research, and financing, is the strategic selection of your lender partnerships. The right partnerships will grow, develop and sustain your business, but the wrong partnerships could add your entrepreneurial pursuit to the list of business startup failures.

The selection of your lender partnerships will depend on your unique value proposition (UVP). No entrepreneur should begin a pursuit without a well-defined UVP, for your UVP is the foundation of all of your business planning and return on investment forecasts. Your UVP should answer this question:

Understanding my market segment, what is it specifically that I will bring to the segment that isn’t already being provided by the current crop of solution providers?

The question includes three main components that must be addressed:

- The identification of a market segment

- The characteristics of all services within your industry, being sold to that market

- The services that you will uniquely provide to said market and their unique characteristics

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

Once your UVP is set, now it’s time to look into the selection of your Lender Partnerships.

To begin, let’s say that you decide to come into the industry and target start-up retail/restaurant businesses, that is, those with less than 1 year in operation. Because you are selling working capital solutions, you would research all available working capital options to this market segment which include sources such as nonprofit loans, business credit cards, personal savings, loans from retirement accounts, friends and family, equipment leasing, and merchant cash advances. To serve this market segment efficiently, you would choose to offer merchant cash advances and equipment leasing.

Next, you would scroll through all of the direct lending sources in the country that provide the working capital solution you have decided to lead with, but who also specialize or at least “serve” the target market you are seeking. Many equipment leasing companies do not fund businesses with less than 2 years in business, and many cash advance companies do not fund companies with less than 1 year in business. Your goal would be to find these lenders and create that network, negotiate pricing, workout your commission schedules, and verify all aspects of said partnership to make sure that it’s beneficial for your clients and your office. It should be a win-win-win partnership, a win for your clients as they find a source for working capital that they didn’t know existed, a win for your partner as they obtain “feet on the street (or telephone)” reps without having to pay their overhead, and a win for your office as you are allowed to serve your market and be paid well in doing so.

Due Diligence Is Key

When finalizing your lender selections, make sure all forms of due diligence are completed on the lender(s) to verify their credibility and competency. These forms of research include all of the following:

(( Structure and Legality ))

- The lender should be a licensed direct lender (in states where necessary).

- The lender shouldn’t be a start-up, but instead a proven entity with at least 2 years of operation.

- The lender should have at least directly funded volume in the eight digits (over $10,000,000).

- The lender should have a full staff of employees rather than just one person.

- The lender’s customer service and support departments should be easy to reach.

- The lender should have some sort of press or news media releases on its establishment.

- The lender should specify if they are going to do advances or loans or both.

- The lender’s funding agreements should specify if the transaction will be an advance or loan.

(( Online Presence ))

- The lender should have a fully functional business website, registered for at least two years.

- The lender should have a business email from their business website domain.

- The lender should be BBB Accredited (www.BBB.org) with at least an A rating.

- The lender should be a part of business associations with logo(s) displayed on their website.

- The lender should be included on basic online business directory listings.

(( Broker Respect ))

- The lender should provide a comprehensive Broker Agreement full of legal provisions.

- The lender’s Broker Agreement should spell out all provisions of the relationship.

- The lender’s Broker Agreement should spell out any quotas.

- The lender’s Broker Agreement should spell out new/renewal deal commission structure.

This is a rough introduction and surely there are other criterion that are important in selecting your lender partnerships. However, these recommendations will surely give you a head start as you head into one of the most competitive industries in financial services.

Merchant Cash Advance Stacking – Sidebar

April 17, 2015 A claim brought by a first-position MCA company or lender may not be the only legal concern for a company that engages in stacking. Regulators could become involved if they believe aggressive stacking unfairly harm merchants. The Federal Trade Commission (“FTC”) and most state attorneys general can enforce unfair and deceptive trade practice acts even in B2B transactions.

A claim brought by a first-position MCA company or lender may not be the only legal concern for a company that engages in stacking. Regulators could become involved if they believe aggressive stacking unfairly harm merchants. The Federal Trade Commission (“FTC”) and most state attorneys general can enforce unfair and deceptive trade practice acts even in B2B transactions.

A merchant may be harmed because the stacker imposes so large an aggregate obligation on the merchant that the merchant’s business fails. Or, a merchant may be harmed if a first-position MCA company or lender declares a default under the first-position contract when the merchant accepts the stacker’s offer. Arguably, the merchant could have protected herself from such a default by refusing the offer that caused the harm. However, a regulatory agency may be sympathetic to the plight of an unsophisticated merchant that failed to understand that the stacker’s offer could harm her relationships with the prior MCA company or lender.

Read full article by Robert Cook, Cathy Brennan, and Kate Fisher of Hudson Cook, LLP

Stacking: Is it Tortious Interference?