Business Lending

Rebanked? Wells Fargo to offer short-term, easy credit to small biz

May 10, 2016

Wells Fargo wants to lend $100 billion in five years and wants to do it quick.

The bank’s new loan product, FastFlex, ostensibly an answer to easy online loans will provide short-term credit to small businesses to be processed in a day.

To qualify, businesses need to have been Wells Fargo customers for at least a year and have strong cash inflows. The loan size will range from $10,000 to $35,000 with a one-year term and payments will be automatically deducted from the customer’s deposit account.

“With a $100 billion lending goal, we want to make every responsible small business loan we can,” said Lisa Stevens, Wells Fargo’s head of small business in a news release.

The announcement comes at a time when loan originations by online lenders is slowing and the industry is grappling with growing pains. Lending Club’s stock tanked 35 percent after CEO Renaud Laplanche resigned amidst a loan manipulation scandal and last week, Prosper laid off 171 employees and shut down its office in Utah.

Is the baton being passed on to the banks again?

Defrauding Fintech Lenders Leads to Conviction

May 8, 2016 It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

According to the original indictment filed in August of last year, “Byrd did knowingly devise and intend to devise a scheme and artifice to defraud Windset Capital and RapidAdvance by means of false and fraudulent pretenses, representations and promises.” As part of that, Byrd submitted fake bank statements, a fake lease agreement and other misleading documents. He faked his own name, calling himself Jason Hester, and pretended to be the landlord of the property in question, confirming falsely to underwriters that a lease existed and was in good standing.

In reality, he had no business location.

Once Byrd received the funds from each company, he wired portions of the ill-gotten proceeds to other accounts.

The jury convicted him on three counts of wire fraud and three counts of engaging in monetary transactions in criminally derived property. The trial concluded on March 24th of this year and Byrd is expected to be sentenced on June 16th.

The case is unique because the sole victims were fintech lenders and the criminal charges were brought by United States Attorney Edward L. Stanton III.

On his twitter account, Byrd describes himself as a “multifamily housing developer, entrepreneur, business consultant, public speaker, mentor, yogi, and (some might say) a cool dude.” Not mentioned there however is that Byrd was previously convicted of wire fraud in 2003 and that he also lost a lawsuit brought by Arvest Bank for fraud.

The criminal case # concerning Byrd with Rapid and Windset is 2:15-cr-20025-JPM

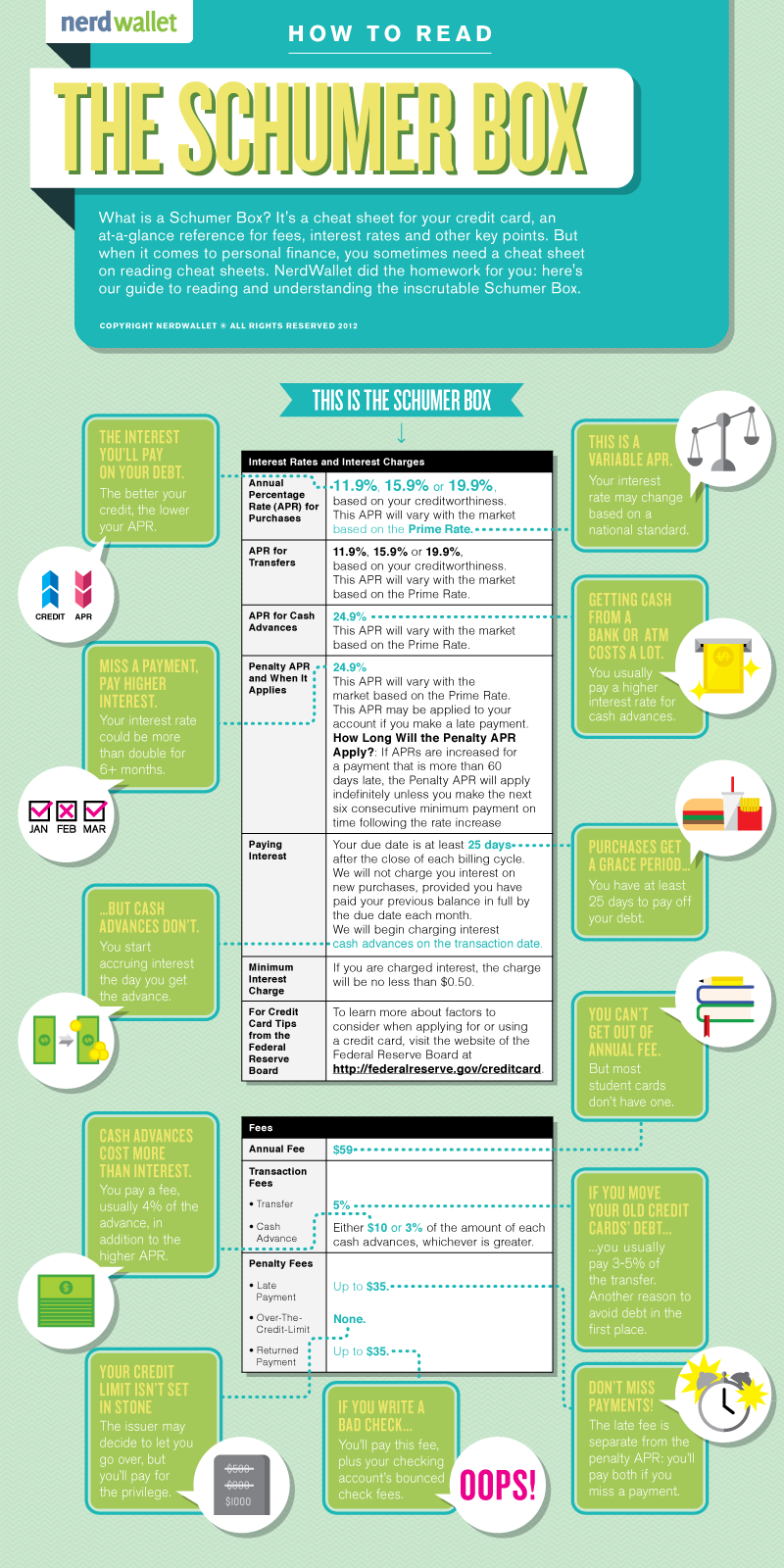

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When deBanked asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told deBanked that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?

Square Capital’s Default Rate is 4%

May 5, 2016

Square revealed today that its Square Capital division had extended $153 million through more than 23,000 advances and loans in the first quarter. The company is still transitioning from merchant cash advances to loans to appease institutional investors. This was not only said at LendIt by Jackie Reses but also reiterated in their Q1 earnings report. “We believe that the transition to a loan product further increases our ability to attract new Square Capital investors,” it said.

Their default rate continued to hover at 4%.

That number is shockingly low considering that under a pure merchant cash advance model they did not conduct credit checks, nor did even they review bank statements or tax returns. Rather the company relied almost entirely on a merchant’s sales history with Square.

This process may have made funding easy but was potentially a hard sell to regulators. As part of their transition to a lending model, all applicants are now subject to a credit approval and have to supply identifying documents. Square also bought an analytics startup less than two months ago to help them make more informed underwriting decisions. This can only mean that if their default rate was 4% with no underwriting, their prowess as a lender will likely increase considerably.

California Lending License Questions Answered – Even the Tricky Ones

May 2, 2016 Q: Can a loan broker operate under the authority of a lender that’s licensed in California?

Q: Can a loan broker operate under the authority of a lender that’s licensed in California?

A: “The CFLL requires both lenders and brokers to hold their own licenses.”

That’s one of many responses provided by Department of Business Oversight Commissioner Jan Lynn Owen to a series of questions and hypothetical scenarios posed by the Equipment Leasing and Finance Association. The nine pages of answers, available on Leasing News basically explains that any funny business or creativity to try and circumvent the law will not be tolerated.

Tom McCurnin, an attorney at Barton, Klugman & Oetting, wrote in Leasing News that “disguising the commissions as something else, like a markup or consultation fees, won’t pass muster before the DOB. The parties engaging in this may be subject to a cease and desist order and hefty fines.”

“While many may claim the recent letter is a revelation, I believe it is simply a restatement of what we’ve known all along—get a license or face the consequences,” he concludes.

CAN Capital Makes Prized Alliance With Entrepreneur Media Inc

May 2, 2016CAN Capital partnered with Entrepreneur.com to create another channel of funding small businesses.

Last month (April 7th), the 18 year old company surpassed $6 billion in small business funding and later this year, it will launch Entrepreneur Lending Powered by CAN Capital to process working capital loans on behalf of the media giant.

“As we get ready to celebrate National Small Business Week, we are excited to work with Entrepreneur Media to continue delivering on our vision of helping small businesses grow and achieve their goals through fast access to funding,” said Daniel DeMeo, CEO of CAN Capital.

The New York-based company which uses propriety data-driven models has made over 170,000 individual fundings including restaurants, medical offices and beauty salons. Last year, the company introduced two new special small business loans – TrakLoan, which adjusts daily payments with daily card sales and a monthly installment loan product offering a customer longer terms with higher transaction sizes.

The New York-based company which uses propriety data-driven models has made over 170,000 individual fundings including restaurants, medical offices and beauty salons. Last year, the company introduced two new special small business loans – TrakLoan, which adjusts daily payments with daily card sales and a monthly installment loan product offering a customer longer terms with higher transaction sizes.

This comes in the context of small businesses being underfunded. Business Insider recently reported that “only half of small businesses with $100,000 to $1 million of annual revenue received at least some of the financing they applied for from large banks in late 2015.”

As banks wrestle with tight lending practices, online lenders have filled the gap for providing quick and smaller loans to businesses who need prompt financing.

OnDeck Prices $250 Million Securitization

April 29, 2016

OnDeck announced the pricing of its $250 million securitization. The online lender will issue notes in two classes consisting of $211.5 million initial principal amount of Class A Notes and $38.5 million initial principal amount of Class B Notes with final legal maturity in May 2020.

Notes were priced with an annual yield to expected maturity of 4.250% for class A notes and 7.754% for class B notes.

“We believe the successful pricing of our securitization demonstrates the strength of our hybrid funding model, which includes warehouse funding, securitizations and whole loan sales,” said Howard Katzenberg, OnDeck’s chief financial officer in a news statement.

As the alternative lending industry proliferates, companies scramble to secure long-term capital and diversify risk. The hybrid model for funding is one way of doing that as investors demand higher yields from loans sold by marketplace lenders. Moody’s downgraded loans consumer loans originated by Prosper on account of missed payments of underlying loans. And earlier this month (April 12th), Citigroup said that it will stop securitizing loans made by Prosper.

However, this does not signal gloom and doom yet. This week, Lending Club revisited securitization and confirmed that it is reportedly in talks with Goldman Sachs and Jefferies Group to put together its first big bond offering.

Will OnDeck’s loans face the same market trepidation?

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”