Business Lending

California Finance Lenders Law Licensing Compliance for Merchant Cash Advance Financiers

August 2, 2016 Since the Richard B. Clark v. AdvanceMe Inc. class action case settlement was brought to the awareness of the Merchant Cash Advance (“MCA”) industry, many MCAs applied and obtained a California Finance Lenders Law License from the Department of Business Oversight. (“DBO”)

Since the Richard B. Clark v. AdvanceMe Inc. class action case settlement was brought to the awareness of the Merchant Cash Advance (“MCA”) industry, many MCAs applied and obtained a California Finance Lenders Law License from the Department of Business Oversight. (“DBO”)

After your company obtains a California Finance Lenders Law license, it will then need to comply with the California Finance Lenders Law. (“CFLL”)

CFLL does not contain specific financial code sections and regulations to regulate MCAs. However, CFLL regulates consumer and commercial loans. So, MCAs licensed under the CFLL will need to comply with the code sections and regulations that apply to commercial loans, assuming that MCAs provide advances that are each “bona fide” $5,000 or more in principal amount and for commercial purposes.

The MCA contract you use when making advances in other states is likely not in compliance with CFLL. CFLL regulation includes without limitation, (either directly or by incorporation of other California and federal laws) the rates and charges, marketing and advertising, disclosures, contractual provisions, electronic transactions, collections, credit applications, default and repossession, brokers and finders, and general operations of main and branch offices.

The CFLL license application requires the MCA company’s principal (corporate officer or LLC manager) to acknowledge on behalf of the MCA company, that it read the contents of and is familiar with the CFLL, and that it agrees to comply with the CFLL.

Lack of compliance can be brought to the attention of DBO’s enforcement officials as a result of either, a customer or competitor complaint, a DBO audit, through the Annual Report that must be filed by CFLL licensees by March 15 of each year, or by other means.

It is important to not only obtain the CFLL license, but to also comply with the CFLL to keep the license. DBO publishes online enforcement actions, such as Desist and Refrain Orders and Accusations. A CFLL licensee has a right to request an administrative hearing to defend itself and present its case. Unfortunately, although the legality of this practice by DBO is questionable, DBO publishes online none-final (and also final) administrative enforcement actions such as Desist and Refrain Orders (“D&Rs”) and Accusations. (publishing of final administrative orders is specifically authorized by the Financial Code but not none-final orders) Potential customers and competitors who review none-final D&Rs, are under the mistaken belief that the D&R is a final order, and may therefore refuse to conduct business with the licensee.

MCAs who are either CFLL licensees or potential licensees should familiarize themselves with CFLL law to avoid administrative enforcement actions, court actions, loss of business, and other adverse repercussions.

National Funding Deploys $1.5B, Beefs up Automated Underwriting

July 26, 2016California-based small business lender National Funding said that it has deployed $1.5 billion in capital, funding small businesses with short-term working capital loans.

The 17-year-old company funded $152 million in loans in the half of 2016, up 45 percent from the same period last year. The company’s customers include general contractors, medical services and trucking companies that average about $1 million in sales annually.

While 80 percent of the loans are for working capital, the company has seen demand for equipment leasing slowly resurge after the financial crisis. “After 2008, the market turned negative in LA and we had to shrink our company,” said CEO Dave Gilbert.

The company is also preparing for a technology overhaul, trying to get access to data pools to automate underwriting. “We need to be tech driven,” he said. “As deals get smaller, we need to automate them to make it affordable.”

National Funding generates 25 percent of its loan volume through brokers. “Given everything that’s happening in the industry, a lot of lenders will be forced to become balance sheet lenders,” he said.

The company hired Geoff Howard from Intuit to lead its technology efforts and aims to automate underwriting for 40 percent of its deals, doubling up from its present rate of 20 percent.

The average size of its loans is $50,000 and the company also plans to launch its first long-term loan product later this year.

Brief: Lending Marketplaces Bizfi and Lendio Forge New Partnerships

July 21, 2016Online lending marketplace Lendio has partnered with digital marketing company Townsquare Media to tap into its customer base and offer loans to small businesses.

The two companies will collaborate on cross-promoting appropriate products and services and marketing Lendio’s platform with 75 lenders and its loan products to businesses.

Meanwhile, another marketplace lender Bizfi got together with The National Directory of Registered Tax Return Preparers & Professionals to reach a wider net of small businesses to fund for products like lines of credit, equipment financing, invoice financing and mid-term to long-term loans.

World Business Lenders Wants To Take On The World of Business Lending, From Jersey City

July 21, 2016

On the thirty third floor of the third tallest building in the state of New Jersey, World Business Lenders’ (WBL) CEO Doug Naidus spoke of another third to a crowd of several hundred people. WBL, which was being honored by state and local politicians for moving their office to Jersey City, is Naidus’ third company. And as he put it, his final one.

In exchange for tax incentives, WBL will bring 225 jobs to Jersey City by the end of 2016. But the perceived benefit to the community is two-fold, because the company itself helps other companies grow through the loans it makes. Collateralized though they may be and different from their many unsecured lending peers, former Congressman Ed Towns, who spoke at the event, said that what the company does makes sense. Current Congressman Donald M. Payne Jr., who was also there, welcomed WBL “to the right side of the river.”

They were joined by Jersey City Deputy Mayor Marcos Vigil, Councilwoman Candice Osborne, Archbishop David Billings and Mitchell Rudin, the CEO of Mack-Cali.

After the speeches and ceremonial ribbon cutting, Naidus told deBanked that he wants to build a company that lasts, one that he can look back on and be proud of. With an average loan size of $200,000, Naidus believes that their system is built to endure. A disbeliever in purely algorithmic underwriting, he said that he sees a correction coming for lenders that have forsaken sound underwriting. His premise for this belief comes from his experience in the mortgage industry, a type of lending that has obviously had its own highs and lows.

WBL Chief Revenue Officer Alex Gemici echoed same, who said that one of their competitive advantages is responsible underwriting and lending. “Our product is sound,” he told deBanked. And because their business model unabashedly pursues profit, they are able to redeploy capital into marketing effectively. Compared to a company like OnDeck, Gemici explained, they can often lend more because of collateral, but only up to what they believe a small business can afford. Their ideal borrower is a business looking to increase their revenue, he added.

Jersey City Mayor Steven Fulop, reportedly said earlier that “helping small businesses thrive has been one of the guiding priorities of my administration, which makes World Business Lenders’ relocation to Jersey City even more rewarding.”

Fulop had recently just welcomed Fundry, one of WBL’s rivals, to his city a few months earlier, who also benefited from tax incentives. Fundry’s office is only a little more than three blocks away from WBL’s 101 Hudson Street address known locally as the Merrill Lynch Building.

“The Grow NJ program was designed to help New Jersey compete with other locations that are attractive for businesses looking to expand or relocate,” said Melissa Orsen, CEO of the state’s Economic Development Authority. WBL stands to receive up to $16.8 million in performance-based tax credits over ten years.

For employees of the company, the spectacular views from their new office seem to have convinced them that moving from their previous headquarters just outside of Times Square in Manhattan isn’t so bad.

“We are thrilled to contribute to the growth of Jersey City as a haven for commerce,” Naidus said. “We are delighted to call Jersey City our new home.”

Confidence Down, But Not Out On Continued Success of Small Business Finance, Survey Reveals

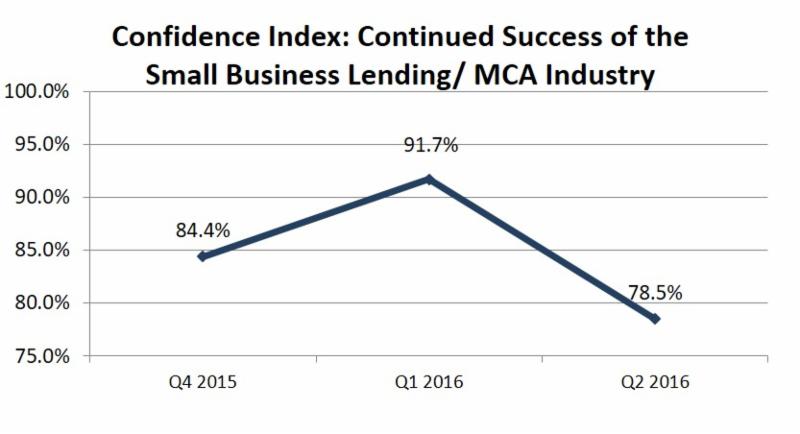

July 19, 2016 A joint Bryant Park Capital/deBanked survey of chief executives in the small business lending and merchant cash advance space showed a decline in confidence in the industry’s continued success, down from 91.7% in Q1 to 78.5% in Q2.

A joint Bryant Park Capital/deBanked survey of chief executives in the small business lending and merchant cash advance space showed a decline in confidence in the industry’s continued success, down from 91.7% in Q1 to 78.5% in Q2.

Respondents were not asked to explain the reasons behind their confidence levels, but increased competition is likely one contributing factor. No doubt some of the creeping pessimism is also spillover from the adjustments occurring in consumer lending, namely declining loan volumes, layoffs and the events that took place at Lending Club.

Decreased confidence may have been the reason that attendance at AltLend last week was down compared to last year. AltLend is an alternative small business lending conference hosted each year at the Princeton Club in NYC. deBanked has been a media partner of the event for the last two years.

On Forbes, Lendio CEO Brock Blake wrote that “2014 and 2015 brought an unhealthy amount of euphoria characterized by huge growth rates, hundreds of millions of dollars in venture capital, enormous valuations, high-flying IPOs, new lenders sprouting (almost) daily, and yield-hungry hedge funds chasing the newest, sexiest cash-producing asset.” But he added that “the industry is maturing and the future for online lending remains bright.”

Notably, 78.5% isn’t even bearish territory, but rather just a step down from the highs Blake described that have catapulted the industry for some time. Even as executives come to grips with the increasing regulatory scrutiny, non-bank small business financing companies have come to view themselves as in it for the long haul. That’s because growth in this sector has been less about refinancing credit cards to a lower interest rate for evermore narrow yields like on the consumer side, and more about fulfilling a role with small businesses that banks have been reluctant to take on for some time.

“Small business lending provides the fuel for small businesses across the country, and the fundamentals are still in place for this to be a formidable industry,” Blake wrote. “I am confident the supply of capital will continue to come from online lenders using technology to minimize risk and streamline processes.”

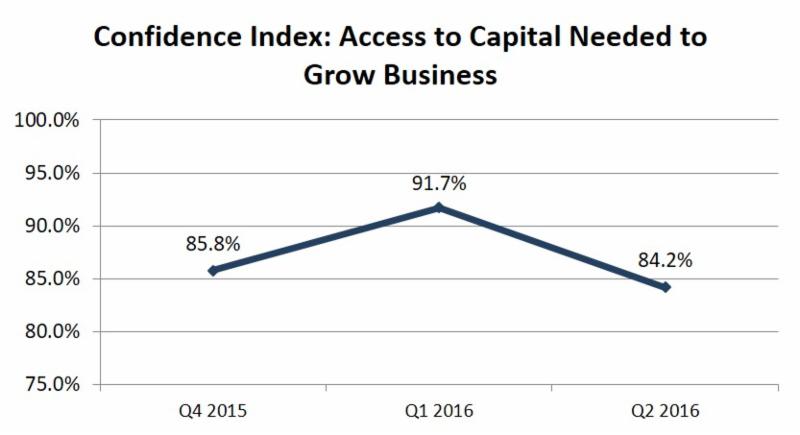

To his point, June and early July were a bright spot for companies raising capital. Fundry, Bizfi, Pearl Capital and Legend Funding all announced deals. The BPC/deBanked survey showed that industry optimism in this endeavor hasn’t shrunk by much, decreasing only from 91.7% in Q1 to 84.2% in Q2.

United Capital Source is Now Licensed in California

July 19, 2016

United Capital Source, the company featured in deBanked’s September/October magazine issue, announced that they’ve become licensed by the State of California Department of Business Oversight as a finance lender and broker. “With its new license, UCS will be writing high quality loans for California small business owners,” Weitz wrote.

California attorney Paul Rianda wrote a guide for deBanked about that process late last year and stressed, “you need to make sure the packet you submit [to the DBO] is perfect.”

In an email, Weitz said that he is “really excited about the opportunity it will create for UCS and for CA merchants to be offered our low rate financing programs.”

The Fed’s Analysis of Online Lender Satisfaction is Bogus

July 15, 2016

A strange statistic about borrowers and their supposed overwhelming dissatisfaction with online lenders is circulating where it shouldn’t be.

Only 15% of small business borrowers were satisfied with the loan they were approved for by an online lender, according to a Federal Reserve study published back in March. That’s actually not even what the study says but that’s the selective takeaway that some very influential people have gleaned from it. That figure in some way shape or form is being repeated at conferences, cited in academic papers, and even referenced in Congressional testimony. Apparently when it comes down to it, people are starting to believe that small businesses overwhelmingly hate their experience with online lenders because it’s something they think a very credible Fed study has confirmed.

It’s not a percent of satisfaction

The statistic in the study is actually representative of how many more people were satisfied than dissatisfied. That’s how they define it in their footnotes. 15% represents a net satisfaction score and it indicates that more borrowers were satisfied than dissatisfied. So 15% net satisfaction means that more than 50% of borrowers were satisfied.

Still though, banks scored higher than online lenders in the report so one might think that’s the important part at the end of the day. After all, this was a highly scientific study that we can still all make important decisions off of, right?

This wasn’t a scientific survey

The Fed disclaims any statistical meaning of their results in the fine print. Under methodology, it actually says:

- The data are not a statistical representation of small businesses.

- The SBCS is not a random sample of small employer firms, and therefore suffers from a greater set of biases than surveys that contact firms randomly.

- Businesses are contacted by email through organizations that serve the small business community in participating Federal Reserve Districts.

The Fed’s own authors seem to be pretty clear in stating that the data is not random, it’s biased, it’s not statistically representative, and that it was collected by third parties who coordinated distribution of the surveys on their own accord. Therefore for a policymaker, this report has no scientific value. Nonetheless, the Fed opens the report by saying “Our hope is that this report contributes to policymakers’ and service providers’ understanding of the business conditions, credit needs, and borrowing experiences of small business owners.”

Admitted falsehood becomes truth

Even though the figures are meaningless, they are being recited over and over. A major US Treasury report published in May for example, cited the Fed’s 15% satisfaction figure in its own analysis of marketplace lenders.

Testimony by Greg Baer, the President of The Clearing House Association, cited the study as well during a Senate hearing three weeks ago, but seemingly interpreted it to mean that only 15% of small businesses were satisfied with online lenders. “As reported in a recent small businesses survey, borrowers are generally dissatisfied with online lenders,” he said.

Marcus Stanley, Policy Director for Americans for Financial Reform, made the same mistake when he testified before the House Small Business Committee last month. “The evidence indicates they often provide a substandard and even exploitative product – just 15% of small business borrowers from online lenders expressed satisfaction with their experience,” he said, while arguing why they should be regulated further.

An article published by Nerdwallet also made the wrong assumption. “In fact, only 15% of small-business borrowers in the Federal Reserve survey said they were satisfied with their experience with online lenders,” they wrote in a story back in April.

Sadly, these are just a few examples.

Now what?

Does a study that’s not random, biased, not statistically representative, and not even controlled by the researchers, do more harm than good for an industry? Perhaps, because readers assume that a government study is scientifically sound on its face. Despite the authors’ move to disclaim the scientific value of it altogether, a mischaracterization of what is even presented anyway is becoming an oft quoted truism.

What is happening now is that both advocates and critics of the industry are starting to believe that only 15% of small businesses are satisfied with online lenders. No study has ever come to that conclusion though, not even the Fed study. It’s all in the fine print that openly says its not statistically representative and biased. And if that wasn’t enough, they even add “caution should be taken when interpreting the results.” Which in other words means, don’t use this stuff for anything important.

OnDeck Sets Q2 Earnings Date And…

July 14, 2016

OnDeck has one thing going for it when it releases its Q2 earnings on August 8th, the fact that the market seems to be anticipating bad news at every turn for the marketplace lending industry right now. A large drop in Q2 origination volume, if that is in fact what they report, would probably just serve as a confirmation of what everyone is already expecting.

OnDeck has already stopped referring to themselves as a technology company, a classification that likely propelled their IPO. Back in January, company CEO Noah Breslow said in a CNBC interview that OnDeck was actually a “non-bank commercial lender.” And after their first truly disappointing quarter, the company’s stock price has come down to a more sober level. It closed at $5.29 on Wednesday, down 74% from the IPO price and down 80% from the all time high.

With a good deal of doubt presumably already priced in, investors may look for reasons to be optimistic in Q2 even if the results are unfavorable overall.

A report circulated by Compass Point’s Michael Tarkan last month said that, “credit is holding up well, and the OnDeck-as-a-Service platform opportunity remains attractive.” Though it also added “overall profitability remains distant and tangible book value should continue to move lower.”

The earnings call on August 8th will take place after the market closes.