This Just In: Crypto Transactions Aren’t Tax Free

January 20, 2022 Patrick White, CEO, Bitwave

Patrick White, CEO, Bitwave“I don’t always believe people that say they are surprised about having to pay taxes on crypto. There’s a field on your tax form to say where you’ve made money doing illegal things. If you sell drugs, there’s a place to report how much money you’ve spent selling drugs. The IRS doesn’t care. Everything is taxed in this country.”

There is no such thing as too many crypto transactions when it comes to accounting purposes according to Patrick White, CEO of Bitwave. Bitwave operates the software that does the accounting for major blockchain companies and retailers who have taken crypto as payment.

White says that the high volume of crypto transactions aren’t coming from individuals sending digital assets back and forth, but rather from the companies that host the infrastructure of these transactions.

“It’s not just trading, trading is fun and we all love the rat race that is trading, but where it’s a lot more interesting is how some of our customers who are in the NFT space are seeing millions of revenue transactions a month.”

These sites like OpenSea, a client of Bitwave, are seeing sky high amounts of these types of transactions. When asked about the cost of accounting for an individual doing ten-thousand trades a month, White laughed.

“Ten-thousand trades a month is nothing,” he said.

White spoke of an instance which is seemingly a common occurrence in the crypto world. “We had a customer who when we were running their [transactions], I couldn’t figure out [an issue] with one of their months. I went to go look at the data, and they had turned on a Binance bot and without even realizing it, they didn’t know this, they accidentally had 200,000 trades in a month. The volume is incredible.”

White spoke of an instance which is seemingly a common occurrence in the crypto world. “We had a customer who when we were running their [transactions], I couldn’t figure out [an issue] with one of their months. I went to go look at the data, and they had turned on a Binance bot and without even realizing it, they didn’t know this, they accidentally had 200,000 trades in a month. The volume is incredible.”

When asked about how digital assets have impacted the accounting world, White stressed that the amount of transactions have resulted in companies appearing larger than they are from a transactional-perspective. According to him, some of his clients are doing as many transactions as some of the largest companies in the world.

“[One client] is a one-year old company that is doing the volume of a sixty year-old retail business, it’s unheard of.”

When asked further about the difference of cost in accounting digital assets versus dollars, White explained that it isn’t much different than how larger companies have maintained their books for some time.

“No matter what, if you are a high frequency trader and you’re making hundreds of millions of trades a year, you will need software to deal with that,” said White. “I wouldn’t say that [the amount of transactions] are increasing costs across the board, it is a cost that you would already be expected to [have].”

When asked about the apparent vacuum of crypto-native accountants, White seemed to cast blame on the approach of the information. When hiring, he says he finds more value in people with engineering experience over accounting experience, and blockchain experience over anything else.

“[Other accountants] are trying to apply finance 1.0 things to this crypto world,” said White. “We look for good engineers. A good engineer can figure anything out, a bad engineer with accounting experience can’t. We’re looking for blockchain experience, as blockchain [technology] is more difficult than accounting in many ways.”

While most businesses will file extensions this time around and finish their taxes in October, White believes that blockchain accounting will become more widespread as new firms leverage the infancy of the space and settle into their niches.

“Cottage industries will come up in order to enable the IRS,” said White. “I don’t expect the IRS to build this technology or this understanding in-house. There will be people and businesses that will do it for them.”

With the IRS’ decisions about taxing crypto having the potential to change at any notice, White stressed the necessity for malleability when developing this kind of accounting technology in such an unpredictable space.

“We’ve designed Bitwave from the very beginning to be able to rapidly adjust to the new laws that are coming out,” he said. “Even back then, it was very obvious that we couldn’t build this tech in such a way that it is inflexible.”

Dorsey Focuses Tweets on Bitcoin and Anti-Web3 Since Leaving Twitter

January 18, 2022 Jack Dorsey’s departure from Twitter didn’t leave him without a job. He’s still the CEO of Square (now Block), a payments company that is one of the largest small business lenders in the country. Still, all that extra time on his hands must mean he has plans in the works, especially since he believes hyperinflation is right around the corner.

Jack Dorsey’s departure from Twitter didn’t leave him without a job. He’s still the CEO of Square (now Block), a payments company that is one of the largest small business lenders in the country. Still, all that extra time on his hands must mean he has plans in the works, especially since he believes hyperinflation is right around the corner.

If his tweets are any indication, Dorsey is focused mainly on Bitcoin as both an answer to inflation and as a counter to the burgeoning “web3” concept attributed mainly to projects on the ethereum blockchain.

“You don’t own ‘web3.’ The VCs and their LPs do,” Dorsey tweeted on December 20. “It will never escape their incentives. It’s ultimately a centralized entity with a different label. Know what you’re getting into…”

“The VCs are the problem, not the people,” he later added.

His comments rubbed some in Silicon Valley the wrong way.

I’m officially banned from web3 pic.twitter.com/RrEIAuqE6f

— jack⚡️ (@jack) December 22, 2021

Since being “banned by web3,” Dorsey announced that Block is building an Open Bitcoin Mining System to help make mining more distributed and efficient. A tweet thread he shared by Block Hardware Manager Thomas Templeton explained exactly what that means:

“We want to make mining more distributed and efficient in every way, from buying, to set up, to maintenance, to mining. We’re interested because mining goes far beyond creating new bitcoin. We see it as a long-term need for a future that is fully decentralized and permissionless.

We started by digging into two big questions. 1) What are customer pain points today? 2) What are the specific technical challenges? We spoke with members of the mining community to learn more about their experiences. Here’s what we’ve found so far:

1/ Availability. For most people, mining rigs are hard to find. Once you’ve managed to track them down, they’re expensive and delivery can be unpredictable. How can we make it so that anyone, anywhere, can easily purchase a mining rig?

2/ Reliability. Common issues we’ve heard with current systems are around heat dissipation and dust. They also become non-functional almost every day, which requires a time-consuming reboot. We want to build something that just works. What can we simplify to make this a reality?

3/ Performance. Some mining rigs generate unwanted harmonics in the power grid. They’re also very noisy, which makes them too loud for home use. Unsurprisingly, all miners want lower power consumption and higher hashrates. What’s the right balance of performance vs other factors?

Developing products is never a solo journey, and evaluating existing tech is always part of our practice. For this project, we started with evaluating various IP blocks (since we’re open to making a new ASIC), open-source miner firmware, and other system software offerings.

We are interested in performance *and* open-source *and* our own elegant system integration ideas. Which tech and which partners should be on our list to consider? We’ve learned so much just from these preliminary conversations and we want to keep this going.

Team. We’re incubating this investigation within Block’s hardware team and are starting to build out a core engineering team of system, asic, and software designers led by @afshinrezayee. A few of the open roles are Electrical Engineers, Analog Designers, and Layout Engineers.

Thanks for engaging with our work. If you have questions, want to share more feedback about the pain points or missing features of the existing mining solutions, or know someone we should be talking to about our open roles, you can reach us at miningsystem (at) block (dot) xyz”

As for inflation, well Dorsey’s not so shocked that the number continues to tick upwards.

damn Santa didn't take the transitory inflation away https://t.co/P1CFEIQyNV

— jack⚡️ (@jack) January 12, 2022

Buying the Constitution at $20 Mil? More Like $25 Mil

November 16, 2021 While crypto fans rally to hit a $20 million fundraising target in order to make a competitive bid for a copy of the United States Constitution on Thursday, lurking in the background is another cost, the auction house fees.

While crypto fans rally to hit a $20 million fundraising target in order to make a competitive bid for a copy of the United States Constitution on Thursday, lurking in the background is another cost, the auction house fees.

Known as the “Buyer’s Premium,” Sotheby’s charges 25% on the first $400k, 20% on the next $3.6M and $13.9% on the amount over $4 million, according to the auction terms.

That would mean that a $20 million winning bid would generate $3,044,000 in Buyer’s Premium Fees. And that’s before an additional 1% overhead premium equivalent to $200,000, bringing the house fees to $3,244,000.

Oh, and that’s not inclusive of the upfront sales tax of $1,775,000 (8.875% of the sales price).

All combined, the fees and taxes to take the $20 million haul off the premises, before transport, preservation, and security is: $4,819,000.

That means that the ConstitutionDAO would really need at least $25 million in its coffers in order to place a legitimate $20 million bid.

On Tuesday at 5pm EST, approximately 48 hours before auction time, the DAO had only raised 1,382 ETH, equal to about $5.87M. Sotheby’s starts the bidding at 6:30pm on Thursday at its location in NYC.

Time will tell if it is able to muster up the rest in time.

El Salvador Becomes First Bitcoin Nation as 70% of Country Remains Unbanked

September 7, 2021 With over $20 million in Bitcoin, the El Salvadorian government is set to put the basis of their already crumbling economy on the back of the world’s most sought-after cryptocurrency. President Naykib Bukele took to Twitter over the weekend to boast about his country’s unprecedented economic shift in a time when 70% of residents lack access to traditional financial services.

With over $20 million in Bitcoin, the El Salvadorian government is set to put the basis of their already crumbling economy on the back of the world’s most sought-after cryptocurrency. President Naykib Bukele took to Twitter over the weekend to boast about his country’s unprecedented economic shift in a time when 70% of residents lack access to traditional financial services.

In a country where roughly half of its population has no internet access, the government has released a state-sponsored app (called Chivo Wallet) that will allow its citizens to buy goods using Bitcoin the government owns. Mostly dominated by the US Dollar, the local economies of El Salvador will now be forced to accept Bitcoin as legal currency.

Each citizen who uses Chivo will be given $30 worth of Bitcoin to jumpstart the spending.

Buying the dip 😉

150 new coins added.#BitcoinDay #BTC🇸🇻

— Nayib Bukele 🇸🇻 (@nayibbukele) September 7, 2021

The move has faced backlash from all different types of groups including economists, politicians, and investors. The world is watching to see if this shift in currency will help pull the country out of its troubles, or if it is more public relations posturing — at the expense of the El Salvadorian economy.

The United States top official in El Salvador, Jean Manes, referred to the nation at a press conference Saturday as “a democracy in decline” as the move is just one of a handful of that technically increase the power of the federal government in the small country. Manes compared Bukele to the likes of Hugo Chávez, using his notoriety with the population to cover up a strategic economic collapse and dismantling of democracy.

The El Salvadorian embassy did not immediately respond to a request for comment.

The value of Bitcoin dropped by 15% against the US dollar on the day of its debut.

Tether is Now So Big, Its Collapse Could Disrupt the Short-Term Credit Markets

June 26, 2021 More than $62.5 billion worth of Tethers have been printed in the last few years to facilitate liquidity in the crypto markets. The system has worked because the company behind Tether had long claimed that each unit of the digital currency was backed somewhere by a real dollar in a bank account.

More than $62.5 billion worth of Tethers have been printed in the last few years to facilitate liquidity in the crypto markets. The system has worked because the company behind Tether had long claimed that each unit of the digital currency was backed somewhere by a real dollar in a bank account.

That was determined false. “Tether’s claims that its virtual currency was fully backed by U.S. dollars at all times was a lie,” wrote the New York State Attorney General in February after the regulator announced a settlement with the company. “These companies obscured the true risk investors faced and were operated by unlicensed and unregulated individuals and entities dealing in the darkest corners of the financial system.”

Despite the characterization, Tether has continued to be the glue that makes the global crypto market hum. And their size is now so big, that it’s no longer just a crypto problem.

According to the Federal Reserve Bank of Boston, Tether now poses a risk to all short-term credit markets. The central bank listed it as an example of “new disruptors” that pose financial stability challenges.

Eric S. Rosengren, the CEO of the Boston Fed, said “There are many reasons to think that stable coins, at least many of the stable coins are not actually particularly stable and actually have some of the same features as money market funds. The difference is prime money market funds have been losing market share but these stable coins have been growing very rapidly in part because of their use along with the cryptocurrency market.”

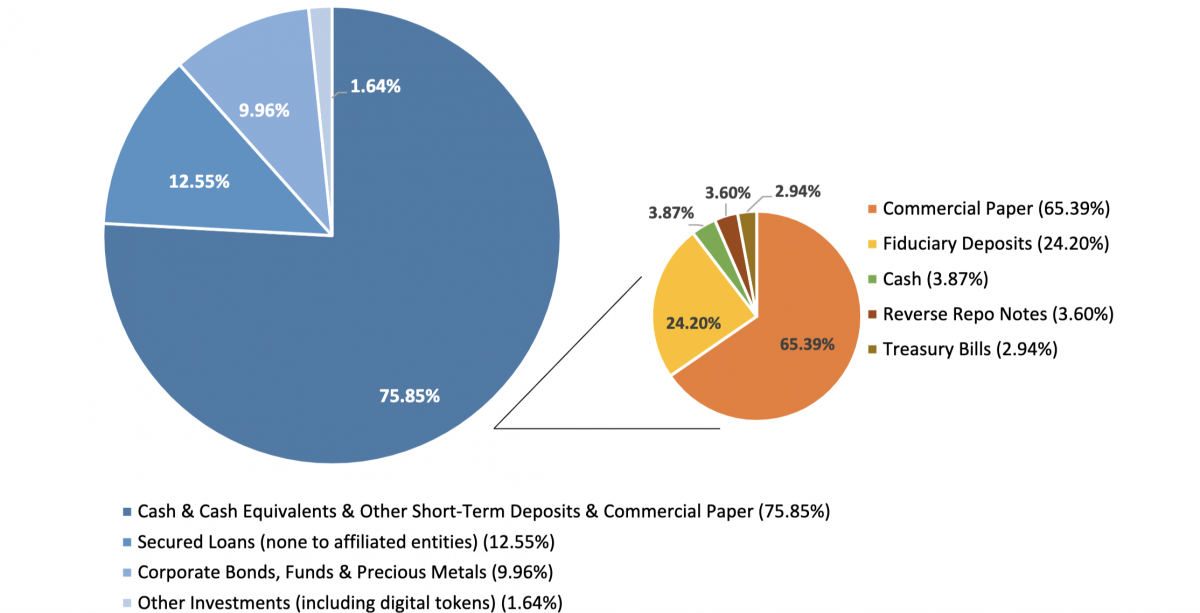

On Tether in particular, he said, “While [Tether talks] about being stable, if you look at the set of assets that are there, it includes corporate bonds, secured loans, commercial paper, in effect this is a very risky prime fund. Prime funds would not be able to hold all these assets.”

Tether has drawn enhanced public scrutiny in recent months after releasing the following breakdown of its assets. The digital asset company that once claimed all Tethers were backed by dollars, revealed that less than 3% of them were actually backed by dollars.

Tether’s riskiness was also the subject of a recent segment on Jim Cramer’s Mad Money show on CNBC:

deBanked first shed light on the Tether mystery more than two years ago in a story that questioned what drove the cryptocurrency bull market of 2017.

FBI Seizes 84% of Colonial Pipeline Bitcoin Ransom

June 8, 2021 A month after hackers shut down the Colonial Pipeline for a ransom of $4 million in bitcoin, the FBI got the majority of the money back.

A month after hackers shut down the Colonial Pipeline for a ransom of $4 million in bitcoin, the FBI got the majority of the money back.

Bitcoin, the digital currency idolized as free and far from the reaches of the government, was confiscated (some theorized “hacked”) this past week. The FBI took back $2.3M: half of the pipeline ransom. The Bureau followed the 75 bitcoins via the blockchain and, according to an affidavit uploaded by ABC News, seized the private key to the bitcoin account and took 63.7 bitcoin. Though the FBI secured 84.9% of the ransom in BTC, the crypto’s price is down to nearly half last month’s value.

Now, bitcoin enthusiasts like the editors at Decrypt will swear that there is no way the FBI could hack a private account that without the private key and account number, both long strings of numbers, the encryption makes it impossible to get in. But law enforcement could confiscate Bitcoin through other methods.

The blockchain is a ledger going back to the first block mined with all transactions perfectly traceable. With enough computer power, an agency can retrace steps hackers take and force the address owner to comply.

April Falcon Doss, executive director of the Institute for Technology Law and Policy at Georgetown Law, told NPR that while unlikely, there is even a theoretical possibility that the FBI outright hacked the private key.

But “The idea that the FBI would have, through some brute-force decryption activity, figured out the private key seems to be the least likely scenario,” She said. Still, a currency that is supposed to be “the future of finance” dropped more than 8% after the news that digital terrorists couldn’t rely on bitcoin for illegal activity.

The Mayor of Miami is Hosting a Crypto Conference

June 1, 2021Miami Mayor Francis Suarez has embraced crypto so completely that he’s hosting his own crypto conference on Wednesday, June 2.

Tomorrow I’m hosting my very own Crypto Conference with some of the top players in the DeFi space.

Use the link below or tune into Channel 77 to get in on the action🚀 https://t.co/QnmNa0WxKl pic.twitter.com/N8GSR2UPSa

— Mayor Francis Suarez (@FrancisSuarez) June 1, 2021

The mayor regularly shares photos with crypto executives on social media and his own city government website biography includes a section dedicated to the Bitcoin White paper. The Miami Heat’s home stadium is even being rebraned to the FTX Arena, named after a cryptocurrency exchange (which oddly cannot be accessed by US residents).

Suarez’s June 2nd conference will be 100% virtual and FREE.

In the three days that follow, the largest ever in-person Bitcoin conference will take place at the Mana Convention Center in Miami’s Wynwood neighborhood.

It’s not just crypto. Suarez has been heavily accommodating to the tech and finance industries with the hope that they might relocate their businesses to Miami.

In that vein, deBanked sat down with the mayor in person back in March.

PayPal Enables Purchasing With Bitcoin

March 30, 2021 PayPal launched Checkout with Crypto, allowing users to use Bitcoin, Litecoin, Ethereum, or Bitcoin Cash to checkout at more than 29 million PayPal merchants.

PayPal launched Checkout with Crypto, allowing users to use Bitcoin, Litecoin, Ethereum, or Bitcoin Cash to checkout at more than 29 million PayPal merchants.

“As the use of digital payments and digital currencies accelerates, the introduction of Checkout with Crypto continues our focus on driving mainstream adoption of cryptocurrencies,” CEO and President Dan Schulman said. “Enabling cryptocurrencies to make purchases at businesses around the world is the next chapter in driving the ubiquity and mass acceptance of digital currencies.”

The transactions will be settled in cash by PayPal automatically, and the firm said it does not plan on holding the coins and will likely sell the balance off. PayPal had previously offered to buy, sell and hold cryptocurrencies on their platform through a partnership with Paxos Trust Company.

PayPal said it added crypto purchasing to engage more customers with online merchants and make their purchasing platform more accessible.

How will the transactions be taxed? The terms and conditions state that PayPal will provide 1099 forms and report to the IRS, but “it is your responsibility to determine what taxes, if any, apply to transactions you make.”

A lot of Crypto news happened at once. Yesterday, Visa announced a USD Coin program, aiming to allow transactions to be settled through a stable coin backed by the USD.