Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

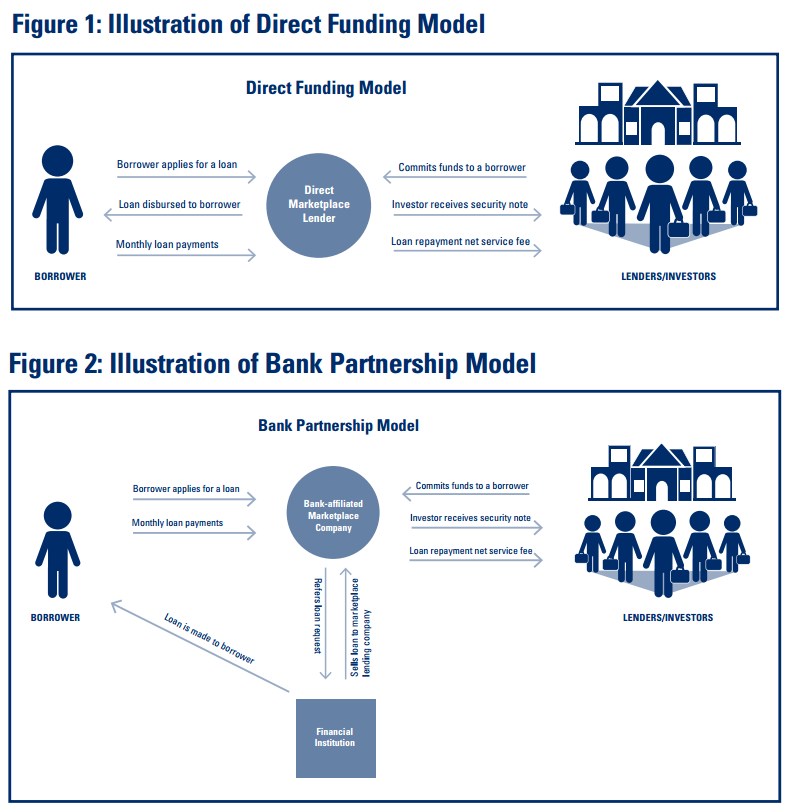

How the FDIC Defines Marketplace Lending

February 5, 2016Marketplace lending is one of this year’s hottest buzzwords but its meaning is not very intuitive. According to a recent Federal Deposit Insurance Corporation (FDIC) report, “marketplace lending is broadly defined to include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary.” This might sound similar to peer-to-peer lending and that’s because it’s the same thing, the FDIC explains. “Although the model, originally started as a ‘peer-to-peer’ concept for individuals to lend to one another, the market has evolved as more institutional investors have become interested in funding the activity. As such, the term ‘peer-to-peer lending’ has become less descriptive of the business model and current references to the activity generally use the term ‘marketplace lending.'”

Voilà, marketplace lending is what you get when peers are replaced by private equity firms, pension funds, and hedge funds. Additionally, there is a general assumption that the intermediary platform is also underwriting and grading the loans.

The FDIC separates marketplace lenders into two categories, the “direct funding model” and “bank partnership model,” both of which are illustrated below:

In both circumstances, investors are actually buying securities, rather than participating in the loans themselves.

The FDIC says that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, education financing, real estate loans, merchant cash advance, medical patient financing, and small business loans.

For even more information, read the official report.

The Ghost of Second Source Funding Has Lost a Desperate Court Battle

February 4, 2016The notorious company returned from the dead for one last final stand

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

Meir Hurwitz, a co-founder of NY based Pearl Capital, immortalized the Second Source years through a Bloomberg exposé about how his own company rose and sold for $40 million. In his tale, he claimed that Second Source founder Sam Chanin still owed him $2 million for the work he performed there. For Hurwitz, the falling out set the stage for the company he would go on to start. For other employees, it was the beginning of a grudge that would stick around for almost a decade.

Chanin has gone so far as to admit on his blog that he became known as “the guy who ripped them off and didn’t pay their residuals.” According to him, it wasn’t his fault. Court records do show Second Source Funding filing a complaint against Cynergy Data back in 2009 for $60 million in damages. Cynergy was the processor behind their lucrative merchant services operation and ultimately where the residuals they paid out to sales agents originated from. The case was dismissed in October of that year because Cynergy declared bankruptcy.

Effectively shuttered by the circumstances, the only reminder of what had once been, was another lawsuit filed by Second Source in September 2012 against a company (and more than 30 co-defendants) that acquired Cynergy Data’s assets. In October of 2009, Cynergy’s assets were reportedly sold to The Comvest Group for $81 million. In the complaint, Second Source sought at least $50 million from them in damages.

It has been approximately seven years since Second Source’s days ended, sources estimate. Users on industry forums were already speaking of the company in the past tense as far back as early 2009. The Second Source website no longer even exists. While ex-employees have long urged old peers to move on from those days, others have been forced to confront their demons.

THE GHOST OF MERCHANT CASH ADVANCE PAST

THE GHOST OF MERCHANT CASH ADVANCE PAST

In September of 2014, the very same Second Source Funding emerged through a complaint filed in the Supreme Court of New York against Yellowstone Capital, LLC, 8 named co-defendants and 25 John Doe defendants. Seeking damages in the astounding amount of $360 million, Second Source alleged that Yellowstone’s co-founders stole their “revolutionary business model” of which they describe as using “Independent Sales Offices to leverage economies of scale in marketing and selling a bundle of financial services, including credit card processing and cash advances.” As a result of that and other claims, they were allegedly the reason for “Plaintiff SSF going out of business.”

The ensuing battle was probably one of the most contentious litigations the industry has ever experienced, at least from what can be seen on the docket. In one publicly filed exhibit introduced by Yellowstone, was the draft of a complaint that the plaintiffs had allegedly sent them that named more than 40 defendants. It reads like a yearbook of the merchant cash advance industry in 2009.

Other exhibits are packed with plenty of Second Source era nostalgia, including copies of the entrance exams given to new hires. One test question embodies the culture of the time, when it asked applicants:

What movie is this quote from, “Put the coffee down, coffee is for closers?”

While motions and cross motions at times appear to venture into the arena of insanity, especially considering Second Source went out of business a long time ago, deBanked has learned that Yellowstone was vindicated this week in a decision that dismissed all the claims with prejudice. That means they can’t have a do-over. The suit lasted 17 months.

deBanked has been quietly following the docket for over a year. We did not ask either party to comment on the decision for the reason being that Second Source may be considering an appeal, or at least they alluded to that in the court transcripts.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

THEN AND NOW

Yellowstone Capital was one of the first merchant cash advance companies to experiment with the ACH payment method. Today, they originate nearly a half billion dollars a year in funded deals.

If you want to see just how much has changed since the Second Source days, check out this answer to the Second Source exam in 2008.

Q: If a merchant is getting an advance from MCA and can’t switch processors, what can the agent offer this merchant?

A: Lock box

It’s amazing to think that ACH was inconceivable at the time. Touched by ghosts indeed…

Ponzi Scheme Threat Hangs Over Marketplace Lending

February 3, 2016 What if all the notes you bought on a peer-to-peer or marketplace lending platform were tied to loans that didn’t exist?

What if all the notes you bought on a peer-to-peer or marketplace lending platform were tied to loans that didn’t exist?

Such a scenario has not only happened but is a recurring theme over in China. The recent $7.6 billion fraud that was allegedly perpetrated by the management of Ezubao (a Chinese-based P2P lender) affected more investors than Bernie Madoff. Approximately 900,000 investors were impacted, according to CNBC.

But it gets worse, way worse. If you can believe this, the bosses of 266 other Chinese peer-to-peer lenders have fled and are in hiding. And that’s just in the last six months. Ratings agency Moody’s has said that 800 platforms have already failed or were recently facing liquidity issues.

In the case of Ezubao, there’s little doubt about what happened. Company executive Zhang Min told Xinhua news agency, “Ezubao is a Ponzi scheme.”

Lend Academy’s Peter Renton, who has witnessed the peer-to-peer lending industry in China firsthand wrote in his blog today that it’s too easy to start a platform there. “You need just US$1,000 to create a smartphone app, then obtain a very inexpensive business telephone license and you can be up and running,” he wrote.

Unsurprisingly, another Chinese peer-to-peer lender that just recently joined the New York Stock exchange, Yirendai (NYSE: YRD), was collateral damage to the Ezubao bombshell. Shares of the company dropped nearly 21% Tuesday to $4.88, down more than 50% from their IPO price.

Does the threat exist in the US?

Here at home, industry insiders are hardly worrying about China. “Could this level of fraud happen in the US?” Renton asked in his blog. “I think it is highly unlikely. There is a well-developed ecosystem in the US for both consumer and small business credit and appropriate lending licenses need to be obtained in most states before a company can begin operations.”

Renton is partially right. Most of the well-known platforms in the US are operating under watchful eyes. But there is a surging over-the-counter (OTC) marketplace that most outside investors don’t even know exists. Enter the syndication market where commercial finance brokers and investors can co-invest in loans or merchant cash advances through private marketplaces that may or may not have a website. With alluring yields of up to 100% a year or even more, it’s the perfect environment to pull off a scam if one maliciously intended to do so. [note: most are not scams at all]

The OTC market for these investments rely almost entirely on trust. There is little to no transparency into how investor funds are actually used. deBanked has received tips over the last twelve months that some companies have co-mingled investor funds with operational cash flow, with the result sometimes being a total loss of investment. Several lawsuits have been filed against these alleged fraudsters, deBanked has discovered, but none compare to the scope of damages taking place in China.

The last major Ponzi scheme to grip the commercial side of the industry for instance, involved Agape Merchant Advance (AMA), a Long Island based company that was part of a wider fraud conducted by sister company Agape World Inc. According to the 2012 complaint, “the defendants actually ran a Ponzi scheme, paying returns to Agape and AMA investors not from any profits earned on investments, but rather from existing investors’ deposits or money paid by new investors.”

The last major Ponzi scheme to grip the commercial side of the industry for instance, involved Agape Merchant Advance (AMA), a Long Island based company that was part of a wider fraud conducted by sister company Agape World Inc. According to the 2012 complaint, “the defendants actually ran a Ponzi scheme, paying returns to Agape and AMA investors not from any profits earned on investments, but rather from existing investors’ deposits or money paid by new investors.”

In a report published by the FBI that explained how it worked, they wrote, “the defendants received an e-mail from Agape’s loan underwriter informing them that the interest rate that a bridge loan borrower had agreed to pay Agape was only 16 percent for one year, at the same time the defendants had promised to pay their investors 12 percent for 60 days for this investment, or 73 percent for the year. The defendants raised approximately $32.5 million for this bridge loan, although the loan was never made.”

The fraud, carried out mainly by its chief executive Nicholas Cosmo, was captivating enough to earn it a spot on CNBC’s American Greed series.

At the time Agape was operating, such yields should’ve raised an immediate red flag for investors, at least that’s the moral the TV show tried to communicate to viewers. In the real world today, those yields could be considered too low since actual commercial bridge financing transactions can pay out up to 40% over 90 days. And therein lies the danger. When legitimate deals are transacting for incredible premiums, how do you resist considering an investment?

It’s easy to chalk up China’s peer-to-peer lending fraud woes to China being China. But the pervasiveness and ease with which such scams have been carried out should send a strong message to marketplaces in the US.

Do you trust where your money is going? Are they using it exactly how they said they will?

Next on American Greed…

JP Morgan Deal With Santander Shows Nothing To Fear From Lending Club Loans

February 2, 2016 After Santander Consumer USA Holdings Inc. [NYSE: SC] announced they were trying (almost desperately it seemed) to shed $1 billion worth of Lending Club [NYSE: LC] loans from their balance sheet, investors weren’t sure if was the loans themselves that were a problem or if there was something else going on.

After Santander Consumer USA Holdings Inc. [NYSE: SC] announced they were trying (almost desperately it seemed) to shed $1 billion worth of Lending Club [NYSE: LC] loans from their balance sheet, investors weren’t sure if was the loans themselves that were a problem or if there was something else going on.

Santander CEO Jason Kulas said back in October that, “although the personal lending portfolio is performing well, we no longer intend to hold these assets for investment.” The rationale was that they would refocus their efforts on subprime auto lending. The market didn’t take the news well and rewarded Santander by gutting the share price from $22.10 on October 28th down to $10.10 by February 1st.

In a report put out last week by Chris Donat, a company analyst at Sandler O’Neill & Partners, it was intimated that the Lending Club loans Santander was still holding may have contributed to the fourth-quarter loss of $232 million that they reported last week on its unsecured personal loan portfolio. “In light of the damage that the personal loan portfolio inflicted on Santander’s income statement in 4Q15, we will be relieved when Santander is out of this business,” Donat wrote.

But fears of possible toxic Lending Club loans subsided on Monday when the WSJ announced that JP Morgan Chase was acquiring Santander’s portfolio and at a “premium.” The average FICO score of those loans is reportedly around 700. “The sale was being closely watched by credit markets as an indicator of the health of the market for online personal loans,” the WSJ said.

Lending Club’s share price closed up 3.12% on the news, but is still stuck near its all time low.

Bet On the Iowa Caucus and Political Primaries With Bitcoins

January 31, 2016 I’m often asked if bitcoin still has a future or if it’s dead. As someone who has mined bitcoins, made purchases with them, sold advertising space with them, traded them, and contributed to political campaigns with them, I feel pretty confident that bitcoins are here to stay. While the system isn’t as anonymous as some people believe, bitcoin fills a void that many people the world over have long sought, a way to move money outside the banking system, and all without a replacement form of centralized control. It is the only way to truly de-bank.

I’m often asked if bitcoin still has a future or if it’s dead. As someone who has mined bitcoins, made purchases with them, sold advertising space with them, traded them, and contributed to political campaigns with them, I feel pretty confident that bitcoins are here to stay. While the system isn’t as anonymous as some people believe, bitcoin fills a void that many people the world over have long sought, a way to move money outside the banking system, and all without a replacement form of centralized control. It is the only way to truly de-bank.

The value is volatile but there are several markets where such volatility is the cost of doing business. Would you rather your bitcoins be worth 5% less when you receive them as payment or would you rather get nothing of what you are owed because the traditional banking system is preventing the transaction?

Enter one black market, betting on US elections, a practice that is largely illegal. And if people could bet on it they would, according to odds maker Jimmy Vaccaro at the South Point Casino in Las Vegas. He told CNN that opening up betting on elections would be the biggest thing they’d ever booked. “It would make the Super Bowl look like a high school football game,” he reportedly said.

But you can still bet on elections if you really want to, according to Market Watch’s Brett Arends. In the name of journalism, Arends successfully bet $1 on the Iowa Caucus… using bitcoins. He bet on Rand Paul with 40 to 1 odds. If he wins, he’ll collect those winnings in bitcoins.

And nobody can stop him.

As an independent system controlled by nobody, there are no bank accounts to freeze, ACH processors to shut down or physical dollars to confiscate. And despite the critics that claim bitcoins have to be converted to a “real” currency at some point in order to realize the value, that’s not necessarily true. You can live your life on bitcoin.

For one bookmaker (and you should view it as a reference only), the odds of a Ted Cruz win in the Iowa caucus is 2.6 to 1. Marco Rubio is paying 10.5 to 1. On the Democrat side, Bernie Sanders is paying 2.92 to 1.

Market Watch’s Arends argues that such activity might not be gambling at all since the IRS ruled bitcoin to be property, not a currency. In his simplistic view, they might as well be digital jelly beans. “When I wagered $1 worth of bitcoins on Sen. Paul last week, in the eyes of the law I wasn’t actually betting real money. I was just betting jelly beans,” he wrote.

You can of course buy cool stuff with those jelly beans.

It’s quite gray indeed, but if the interest in political gambling truly dwarfs the Super Bowl, then a totally bank-less decentralized system opens up all kinds of doors, the kind that don’t want to be closed.

In non-bank finance, a topic I often write about, all roads inevitably lead back to banks, no matter how much the system is disrupted. The truly de-banked use bitcoins and with that, the possibilities with it are endless.

Would you bet on Bernie Sanders with 2.92 to 1 odds? You’re not supposed to be able to do it, but in a bankless world, you could.

SoFi to Air Super Bowl Commercial (Watch it here!)

January 29, 2016“great loans for great people,” the narrator says after zooming in on several young urban professionals. Humorously, the TV commercial, which will air during the Super Bowl, labels some people as “not great” and therefore ineligible to join a rather exclusive club of people who can get great loans. Watch the video below:

NOTE: SoFi has modified their ad to be less controversial by removing the last spoken line from it. The “you’re probably not [great]” ending apparently received some PR backlash. The updated ad is below:

Credit card companies use a similar technique of appealing to consumers by bestowing them with some kind of status. With labels such as Diamond Preferred, Platinum, Platinum Advantage, Platinum Prestige, Gold, Premium and World Elite, it’s an attempt to make the borrower feel like they are part of an important club.

SoFi however, may be the first to showcase borrowers who are just not good enough to be in their club, with the obvious intent that the commercial will be something to talk about. People are probably more likely to share something that is controversial than something that is plain vanilla. With 30 second slots going for $4.5 million this year, SoFi probably can’t afford to go unnoticed.

As part of a promotional campaign, SoFi has been selling their vision of a bankless world through a dystopian online video:

SoFi CEO Mike Cagney has consistently cast himself as the anti-banker, and once joked that his whereabouts are monitored by friends at all times to limit the opportunities for bankers to kidnap him.

What do you think about the SoFi commercial. Is it great?

NetSuite Stakes Claim in Alternative Lending Industry

January 28, 2016NetSuite (NYSE: N), a San Mateo, CA based software company that employs thousands of people, has been planting their flag throughout the alternative lending industry. Earlier today, they announced that Avant, an online marketplace for consumer loans, has gone live on NetSuite OneWorld to manage their “mission-critical business processes.”

In September, Avant had received a private market valuation of nearly $2 billion after completing a Series E round, with one of the investors being JPMorgan Chase.

“Our previous system just couldn’t keep pace with the rapid growth we’ve seen in our industry and our business,” Avant CEO Al Goldstein is quoted as saying in the release. So they turned to a NetSuite product.

NetSuite has a public valuation of over $5 billion and is a popular choice in the alternative lending industry for companies who require scalability. For example, NetSuite OneWorld can support 190 currencies, 20 languages, and automate the tax compliance for over 100 countries. Avant already operates in 3 countries, The US, UK and Canada. More than 24,000 companies and subsidiaries use NetSuite.

“Avant is among a growing number of financial services companies innovating in a market that’s ripe for disruption and are relying on NetSuite’s cloud platform,” NetSuite President Jim McGreever is quoted as saying in their release. “We’re excited to see Avant’s success and look forward to helping them grow.

To date, Avant has issued more than 400,000 loans worldwide.

Several business lenders and merchant cash advance companies also use NetSuite.

Are Small Business Loans the New Flavor of Fixed Income?

January 26, 2016Brendan Ross, the founder of Direct Lending Investments, the oldest and largest fund that buys small business loans from non-bank lenders, has recently filed an N-2 form with the SEC. If approved, it will make his $450 million fund that is currently only open to accredited investors, open to retail investors. To make that possible, the fund’s structure would be converted so that investors become shareholders in what would essentially be a lending business.

On CNBC, Ross explained his model to Trading Nation’s Dominic Chu. “I buy those loans from the non-bank lenders that make them and make them available in portfolio form,” he said.

Ross added that 85% of his fixed income portfolio is in private credit, but adding that’s because he’s an expert in it. Returns range from 6-14%, much better than fixed income government securities.

When asked if the high yields are due to the risk premium, Ross explained that they’re actually taking advantage of an inefficiency in the market, namely that the premium they’re tapping into is related to banks’ unwillingness and inability to package up short term loans. “Many of our loans are 1 year or less,” Ross said. Banks find it difficult to securitize the type of short term loans that they have in their portfolio, he added.

Watch the discussion on CNBC below:

Or if it’s not loading, visit CNBC’s site here.