Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

CFPB Now Accepts Complaints About Marketplace Lenders

March 7, 2016 The Consumer Financial Protection Bureau wants consumers to voice their complaints about marketplace lenders on their website, according to an announcement made earlier today.

The Consumer Financial Protection Bureau wants consumers to voice their complaints about marketplace lenders on their website, according to an announcement made earlier today.

“When consumers shop for a loan online we want them to be informed and to understand what they are signing up for,” said CFPB Director Richard Cordray. “All lenders, from online startups to large banks, must follow consumer financial protection laws. By accepting these consumer complaints, we are giving people a greater voice in these markets and a place to turn to when they encounter problems.”

A consumer guide to marketplace lending published by the CFPB, says “If you consider a marketplace lender as one of your options when shopping for a loan, keep in mind that marketplace lending is a young industry and does not have the same history of government supervision and oversight as banks or credit unions. However, marketplace lenders are required to follow the same state and federal laws as other lenders.”

Consumers can submit complaints in the manner they normally would. For instance if the marketplace lender is a student lender, consumers should choose the “student loan” option.

“The CFPB forwards complaints to the marketplace lender and works to get a response – generally within 15 days,” the CFPB says. “Consumers are given a tracking number after submitting a complaint and can check the status of their complaint by logging on to the CFPB website. The CFPB expects companies to close all but the most complicated complaints within 60 days.”

This new complaint feature applies only to consumer products, but according to a recent report, business lenders are next on the list.

Merchant Cash Advances Costly But Not Opportunistic, Fed Study Finds

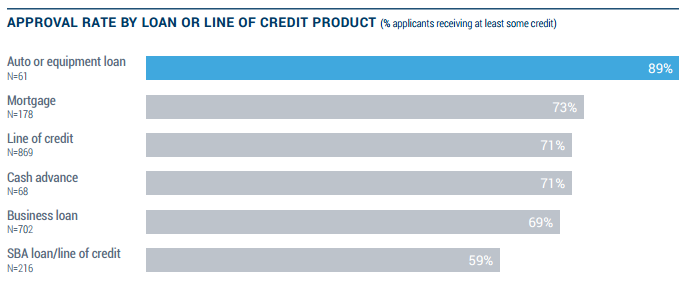

March 6, 2016Only 71% of business owners that apply for a merchant cash advance actually get approved for them.

Equipment loans, commercial mortgages, and company vehicle loans all have higher approval rates than merchant cash advances, a comprehensive Federal Reserve study revealed. Lines of credit were approved just as often as merchant cash advances. Right behind them were business loans and SBA loans at approval rates of 69% and 59% respectively.

The statistics disprove the theory that merchant cash advance companies don’t underwrite or that they are doing so recklessly at the expense of their small business customers.

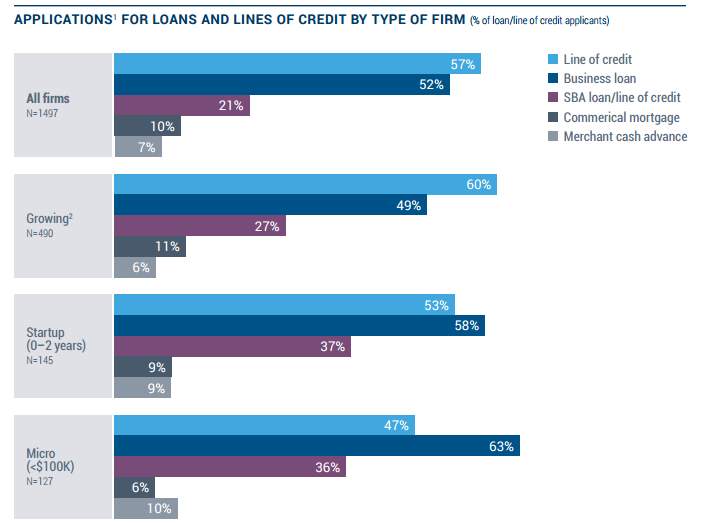

Only 7% of small businesses have ever even applied for a merchant cash advance.

The propensity to apply for a merchant cash advance ranked higher among businesses less than two years old and those seeking less than $100,000.

Notably, small businesses reported being much less satisfied with online lenders than banks, but overwhelmingly cited cost as the reason behind it. Big banks scored worse on transparency than online lenders among dissatisfied borrowers.

The findings are not surprising. 35% of small businesses said that speed of the decision process was a factor influencing where they applied. 37% said ease of the application process was a factor and 40% said the perceived chance of being funded played a role.

In these areas, online lenders walloped small and large banks. More than 50% of dissatisfied bank borrowers fingered a difficult application process as a reason and more than 40% said it was the long wait for a credit decision.

The results fall in line with expectations, that speed and ease often come at a cost. However, merchant cash advance companies do not appear to be approving applicants just to opportunistically charge a high fee. The approval rates are in line with other types of financial products, and are even less likely to be approved than a mortgage.

Hedge Funds Will Call The Shots in P2P Lending, Survey Says

March 6, 2016 P2P lending platforms will increasingly rely on larger hedge funds to fund their expansion, The New York Hedge Fund Roundtable believes.

P2P lending platforms will increasingly rely on larger hedge funds to fund their expansion, The New York Hedge Fund Roundtable believes.

The Roundtable is a non-profit organization committed to promoting education and best practices in the hedge fund industry. Timothy P. Selby, the organization’s president, said of a recent study they conducted, that institutional investors can’t afford to ignore Peer-to-Peer (P2P) lending. “Investing in peer to peer loans not only means the promise of high risk-adjusted returns, such private debt investments also provide less correlated risk relative to more traditional fixed income portfolios,” he said.

And as P2P platforms expand and need money, hedge funds feel it is they that will have the leverage in the negotiations.

In a survey of their members, 21% of respondents chose Lending Club as the business they believe best represents the future of banking 10 years from now. 11% picked Capital One. 6% chose Facebook.

Yet only 17% of respondents had actually actually invested in P2P lending so far. Part of the hesitation comes from the present state of interest rates. 20% of respondents believe that institutional capital will move away from P2P lending and back into traditional finance once interest rates start to really increase.

In the meantime, increasing interest in P2P lending by institutional investors will lead to riskier loans, they say, and it could lead to another credit crisis.

Credit crisis? What Credit crisis?

78% of respondents said history has proven that investors have incredibly short memories and that if securitizations backed by P2P loans offer attractive returns investors will likely dive in.

Of the survey respondents, 24% were fund managers; 9% were allocators; 9% were risk management or trading; 46% were service providers; and 12% were other industry participants.

Lending Club Loan Size Cap Raised to $40,000 (Should Investors Be Worried?)

March 5, 2016 Consumers can now borrow up to $40,000, an increase from the previous cap of $35,000.

Consumers can now borrow up to $40,000, an increase from the previous cap of $35,000.

The new maximum should raise eyebrows. That’s because while one of Lending Club’s biggest allures is the ability to refinance credit cards into a lower rate over a fixed term, there are zero safeguards in place to ensure that the borrower actually uses the proceeds to do just that. Instead, the applicant simply checks a box and if approved, gets the loan minus the origination fee wired to their bank account. That means today’s consumer can obtain 40 grand in one lump sum online. Unsecured. In their bank account. For whatever purpose. From a lending marketplace that puts none of their own money in the loans.

No Recessionary Data for Loans Over $25,000

The numbers look okay, for now. Using NSR’s backtesting tool revealed that loans of exactly $35,000 have generated higher returns for investors than loans of smaller sizes, but have a higher loss rate. This is because the interest rate increases with loan size. The all time loss rate on $35,000 loans is 6.60%, according to the tool, but Lending Club didn’t start making loans this big until February 2011, after the recession had already ended.

That in itself should be alarming because when we examine the time period of June 2007 through June 2010, when the Great Recession occurred, loss rates hit the largest loans the hardest. At that time, the maximum loan size was $25,000 and the loss rate on those was 11.54%.

That in itself should be alarming because when we examine the time period of June 2007 through June 2010, when the Great Recession occurred, loss rates hit the largest loans the hardest. At that time, the maximum loan size was $25,000 and the loss rate on those was 11.54%.

With the maximum size having increased to $35,000 and now to $40,000, there is no recessionary data to indicate how these large loans will perform.

The Temptations of a Cash Windfall?

Credit cards can moderate spending habits because there is a limit on the type of goods and services one can acquire with them. With cash, consumers may be tempted to indulge themselves in other things. One has to wonder if the average consumer really needs 40 grand wired to their account on an unsecured basis with no strings attached on what to do with it.

Lending Club might have considered this already though. In December, they announced Direct Pay, a pilot program in which Lending Club actually requires borrowers to use up to 80% of the proceeds to pay off their outstanding debt. There’s one caveat, it’s only open to a category of the most risky borrowers, those with Debt-to-Income (DTI) ratios of up to 50%. Lending Club’s traditional DTI cap is 30%.

That means that investors have to rely on the ability of borrowers to do the right thing with 40 grand in unsecured cash. Should they trust them?

Big Banks Less Transparent Than Online Lenders Federal Reserve Study Finds

March 4, 2016The results are in. Dissatisfied small business borrowers are more likely to encounter transparency problems with big banks, not online lenders.

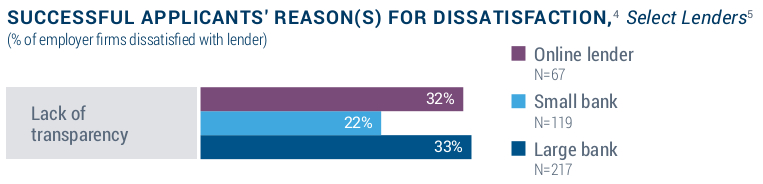

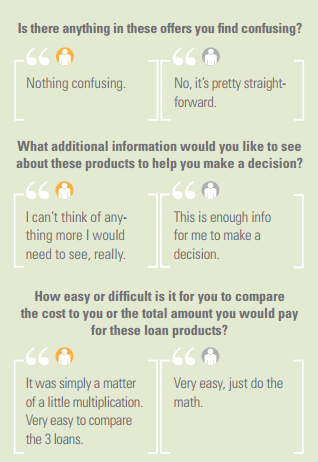

The margin of difference on this measure may have been razor thin, but the anti-online lender rhetoric isn’t matching up with borrower feedback. The 2015 Small Business Credit Survey, a comprehensive report released by the Federal Reserve, found that 33% of borrowers that were dissatisfied with a small business loan from a big bank, cited a lack of transparency as a reason. 32% of borrowers that were dissatisfied with an online lender cited a lack transparency. While both statistics show room for improvement, the results shatter the myth that online lenders are uniquely lacking in transparency.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

Small banks were less likely than online lenders and big banks to experience dissatisfaction over transparency.

Online lenders were defined by the Fed as “alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.” Respondents could select multiple options for dissatisfaction, ensuring that a separate issue didn’t merely trump transparency.

Big banks also scored worse on difficulty of the application process. 51% of dissatisfied borrowers that got a loan from a big bank cited difficulty. Only 21% of dissatisfied borrowers that got a loan from an online lender cited difficulty.

A more difficult, lengthier, and more regulated process at big banks has apparently not led to more transparency with borrowers. The findings echo B. Doyle Mitchell Jr.’s testimony presented during a House Committee hearing last fall. Mitchell, who was speaking on behalf of the Independent Community Bankers of America, said that adding more pages to loan agreements do not make them any more clear to borrowers. “In fact it is even more cumbersome for them now,” he said.

The Federal Reserve’s own study has proven to be consistent with that assessment.

Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

March 2, 2016UPDATE: This case is unrelated to another class action filed against Lending Club on April 6th

Lending Club is the latest publicly traded online lender to get hit by a shareholder class action lawsuit (OnDeck was first). Filed in the Superior Court of the State of California, plaintiff alleges in the complaint that Lending Club misleadingly concealed the fact that:

- Lending Club had an unsustainable business model that was predicated on it being able to issue loans with extremely high and/or usurious rates across the country

- that their loan investors would not be able to enforce the extremely high and/or usurious rates imposed by Lending Club because they violated state usury laws

- that without the extremely high and/or usurious rates, the loans generated through Lending Club’s marketplace would not be attractive to investors because the loans had very high credit risk and were subject to issues concerning insufficient documentation

- that a substantial portion of its loans were issued with rates in excess of those allowed by applicable state usury laws

The action seeks “recovery, including rescission, for innocent purchasers who suffered many millions of dollars in losses when the truth about Lending Club emerged and the its stock price plummeted.”

Among the Defendants is former US Treasury Secretary Larry Summers.

The complaint alleges that the truth about Lending Club began to emerge after “the Second Circuit affirmed [in Madden v Midland] that the business model used by Lending Club was not valid because loans sold by banks to non-banks, third parties (such as Lending Club and its investors) are not exempt from state usury laws that limit interest rates.”

–In actuality, no such affirmation was made. Lending Club does not specifically use Midland Funding’s business model and the case was not about Lending Club, nor was Lending Club mentioned in it.

“Specifically, the Second Circuit observed that assignees and third-party debt buyers could not rely on the National Bank Act to export interest rates that were legal in one state but usurious in another, to the states where those rates were impermissible,” the complaint states.

–Perhaps, but Lending Club’s bank makes loans under the Federal Deposit Insurance Act, not the National Bank Act.

As supporting evidence, the complaint cites statements from Moody’s analysts, Morgan Stanley, Cross River Bank CEO Gilles Gade, and Lending Club CEO Renaud Laplanche himself in a quarterly earnings call.

While the impact of Madden v Midland has been seriously overblown, Lending Club’s stock has no doubt taken a beating since its IPO. The complaint states a loss of 43% from the original offering price. Among the defendants are:

- LendingClub Corporation

- Renaud Laplanche

- Carrie Dolan

- Daniel Ciporin

- Jeffrey Crowe

- Rebecca Lynn

- John J. Mack

- Mary Meeker

- John C. (Hans) Morris

- Lawrence Summers

- Simon Williams

- Morgan Stanley & Co. LLC

- Goldman, Sachs & Co.

- Credit Suisse Securities (USA) LLC

- Citigroup Global Markets Inc.

- Allen & Company LLC

- Stifel, Nicolaus & Company, Incorporated

- BMO Capital markets Corp.

- William Blair & Company, L.L.C.

- Wells Fargo Securities, LLC

NOTE: This case is unrelated to another class action filed against Lending Club on April 6th

Is Jamie Dimon in Favor of Stacking?

March 2, 2016In a featured interview with Bloomberg Markets, JPMorgan Chase CEO Jamie Dimon made a curious argument about small business lending. Speaking about tech-based lenders, Dimon paints the following picture:

For example, they might lend to one of our customers who’s got a $200,000 JPMorgan Chase loan, and this person wants to get another $20,000 for a new truck or a piece of equipment. And what does he do? He goes with them, because he gets it in 15 minutes. If he goes back to the bank, he may have to go through this whole big long process for that $20,000.

Can we do something like that? Of course we can. I’ve asked our people, “Why don’t we just put a revolver on top of our basic loan?” Make it easier for the client.

Whether intentional or not, Dimon’s example is the classic argument made in favor of stacking in the merchant cash advance industry and it’s entirely about doing right by the client. He also said there is nothing mystical about tech-based lenders. “They’re very good at reducing the pain points,” he said. “They can underwrite it quicker using—I’m just going to call it big data, for lack of a better term: ‘Why does it take two weeks? Why can’t you do it in 15 minutes?”’

Canadian Small Business Loan Marketplace Suspends Operations After Run-in With Securities Regulators

March 2, 2016Lending Loop, which describes itself as an online marketplace for Canadians to lend money to growing local businesses, has voluntarily suspended the posting of new loan requests since it is engaged in talks with the Ontario Securities Commission.

Ontario regulators started cracking down on peer-to-peer lending last June. “If you are approaching any Ontario investors to fund peer-to-peer loans or loan portfolios, then you should be talking to the OSC about securities law requirements, including whether you need to be registered or require a prospectus,” said Debra Foubert, Director of Compliance and Registrant Regulation at the OSC, in a news release.

The directive is not unlike the system set up for such lenders in the US. Lending Club and Prosper for example, issue a prospectus and file a registration statement for every single loan with the SEC.

“Lending Loop is Canada’s first peer-to-peer lending marketplace,” the website states. “Our core focus is providing businesses with accessible capital at fair interest rates through a simple online process.”

At present, the investor signup page has been replaced with a button to subscribe to their newsletter to find out when investing opportunities might resume.