Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

CFPB’s New Arbitration Rule Does Not Apply to Business Loans

July 10, 2017The CFPB’s new rule to regulate arbitration clauses in consumer finance contracts does not apply to business loans, according to the agency’s fine print. Page 403 of 775 (that’s how long the rule is) includes a footnote that says:

As is explained in proposed comment 3(a)(1)(i)-1, Regulation B defines “credit” by reference to persons who meet the definition of “creditor” in Regulation B. Persons who do not regularly participate in credit decisions in the ordinary course of business, for example, are not creditors as defined by Regulation B. 12 CFR 1002.2(l). In addition, by proposing to cover only credit that is “consumer credit” under Regulation B, the Bureau was making clear that the proposal would not have applied to business loans.

Watch the video on what the CFPB’s rule is about below:

What Happened to Bizfi?

July 1, 2017

Update 9/22: Select assets of Bizfi including the brand and marketplace were acquired by rival World Business Lenders

Update 8/30: Credibly was selected to service Bizfi’s $250 million portfolio

This past week, Bizfi gave their remaining employees a 90-day warning notice, according to sources familiar with the matter. It was the latest wave of layoffs to hit the company over the last few months. At its peak, Bizfi, which provided capital to small businesses, employed more than 200 people. Some of those riding out their potentially last 90 days are anxiously awaiting the outcome of nonpublic negotiations to salvage parts of the company’s legacy, if it can be done at all.

It’s a bittersweet moment, according to newly former employees I spoke with, some of whom are so young they vaguely recall Bizfi’s past as both Merchant Cash and Capital (MCC) and Next Level Funding (NLF). They characterized their experience as having worked in fintech.

MCC was founded in 2005 as a buyer of future credit card sales, way before the rise of modern fintech. They later spawned affiliate company NLF, which was eventually consolidated into the newly minted Bizfi brand in 2015. In 2016, they were one of the top three largest originators of merchant cash advances. Today, they are no longer funding new business.

Overall, the company grew too fast and missed the window of opportunity to sell, observers maintain. In a CNBC interview in 2015, a Bizfi representative said that they believed securing a major equity investment would allow them to go public by 2017. Such an investment never came. And with the market cooling last year, institutional interest in the space waned and several of the industry’s better-known players were forced into a precarious position.

Bizfi held on, until recently.

I myself was the third employee of MCC, or fourth depending on who actually walked through the door first on my first day that I shared with another new hire back in 2006 (who by the way was Jared Feldman, the eventual co-founder and CEO of Fora Financial, which sold for millions to Palladium Equity Partners LLC). I was at MCC until 2008 and then worked at NLF until 2010. That means I had been gone for five years before the companies ever merged to become Bizfi and seven years before the current dilemma. Therefore I’m not able to personally comment on what exactly went wrong because the company was nowhere near the same as when I left it.

I will report new developments as they become public.

All Companies Can Now Submit Draft IPO Registrations Confidentially

June 29, 2017 There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

There’s a reason the public never got to view BFS Capital’s September 2015 IPO registration documents. Thanks to the JOBS Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.” They can then choose to abandon the offering altogether without having to suffer the fate of their financial statements being made public, which is what BFS Capital did. But if they ultimately had chosen to move forward, their documents would’ve been shared in the public domain.

A new decision handed down by the SEC is now expanding that privilege beyond “emerging growth companies” to all companies. That means that any company can submit draft documents confidentially. It will take effect on July 10th.

“This is an important step in our efforts to foster capital formation, provide investment opportunities, and protect investors,” said Director of the Division of Corporation Finance, Bill Hinman. “This process makes it easier for more companies to enter and participate in our public company disclosure-based system.”

The only reason BFS Capital’s confidential filing is known, is because the company broadcasted that they had filed accordingly in a press release.

“By expanding a popular JOBS Act benefit to all companies, we hope that the next American success story will look to our public markets when they need access to affordable capital,” said Chairman Jay Clayton. “We are striving for efficiency in our processes to encourage more companies to consider going public, which can result in more choices for investors, job creation, and a stronger U.S. economy.”

It is possible that other companies in the industry have filed draft registration statements, got discouraging feedback from the SEC and then decided to withdraw without any of their competitors being the wiser.

Puerto Rico Bankers Association Calls Section 1071 Absurd and Unreasonable

June 28, 2017Section 1071, the law that grants the CFPB authority to collect loan application data on minority and women-owned businesses, is under fire, again. This time it’s the Puerto Rico Bankers Association in response to the CFPB’s RFI on the matter. In a letter, the PRBA points out the sheer irony of conducting costly disparate impact studies on minorities in minority-only communities.

An excerpt from their statement:

According to the 2010 US Census Bureau, 99% of the population of Puerto Rico is Hispanic.

[…]

The direct and evident effect of Section 704B of ECOA for the financial institutions in Puerto Rico will inevitably be the collection, recordkeeping and reporting of virtually all commercial loan applications received within the Puerto Rico marketplace, since most of such applicants would be regarded as “Minority Owned Business”, in accordance with Section 704B.

The PRBA believes that this absurd and unreasonable result must not have been intended by Congress when it enacted Section 1071 of the Dodd-Frank Act. The data so collected, maintained and reported will not serve the purposes for with Section 1071 was enacted since, for the reasons set forth above, it will be completely inaccurate and unreliable. The potential complexity and cost of compliance with the minority-owned businesses data collection and reporting requirements of Section 704(B), will impose on our banks an unintended and unreasonable burden.

Other responses to the CFPB’s RFI have so far called Section 1071, “literally impossible to comply with” and a duplicated effort.

Dubious Story On Strategic Funding Unfounded

June 22, 2017 A questionable story published by Allen Taylor of Lending Times pushed the boundaries of journalism earlier this week. Citing a single anonymous source, Taylor wrote that an alleged breakdown in negotiations between Strategic Funding Source (SFS) and CAN Capital (CAN) had compounded into more problems for SFS when a burst water main drenched their main office and server room at a time when they supposedly had no disaster backup plan in place.

A questionable story published by Allen Taylor of Lending Times pushed the boundaries of journalism earlier this week. Citing a single anonymous source, Taylor wrote that an alleged breakdown in negotiations between Strategic Funding Source (SFS) and CAN Capital (CAN) had compounded into more problems for SFS when a burst water main drenched their main office and server room at a time when they supposedly had no disaster backup plan in place.

“Unfortunately, in order to save money, they [SFS] did not have a disaster backup plan in place,” is the quote Lending Times ran with from their anonymous and only source.

Peculiar on its face, especially with no published response from SFS to confirm it, the story was nonetheless rebroadcast by a new blog calling itself SmallBusinessLending.io, who added their own little editorial flair to it in an email they sent out.

“Having cut a few corners to save money, the company [SFS] didn’t have a disaster backup plan in place. Owch,” the email said.

Eager to determine the accuracy of the story, I reached out to SFS personally for comment, whose executives responded with an astonished bewilderment. They invited me over to go see for myself, which I took them up on. deBanked had ranked SFS as one of the largest small business funders of 2016, and their demise (especially in a great flood of some kind) would indeed be newsworthy.

A water main was struck on the 5th floor of Tower 45 at 120 West 45th Street, only one of three buildings in Manhattan that SFS has offices in. Andy Reiser, the company’s CEO, and David Sederholt, a Senior Advisor, gave me a tour of several floors, including the 5th where the incident happened. There is some water damage on lower floors, prompting some employees and executives to reshuffle their workspaces, and necessitating the use of available office space up on the 19th floor. That much is true.

Little, if anything seemed to have been disrupted, however, least of all their servers, which Sederholt maintained is in Amazon’s cloud anyway. They have redundancy built in nonetheless for all types of disasters should something impede New York’s operations, they explained, with Virginia and Texas operations as their fallback.

Just to be sure, I visited their other Manhattan offices at 1501 Broadway and 145 West 45th street, each of which hummed with normal activity.

The company wouldn’t comment on matters regarding CAN. CAN, if you recall, suspended funding operations almost 7 months ago and rumors have surfaced from time to time on industry forums regarding a comeback, but none have been confirmed.

On June 13th, American Banker reported that CAN had laid off an estimated 55 employees in their Kennesaw, GA office.

A message left for Lending Times about their reporting on SFS had not been answered by the time this story went live.

Pearl Capital Secures $15M in Financing From Chatham Capital Management

June 21, 2017

Pearl Capital Business Funding, LLC has closed on $15 million in financing from Atlanta-based Chatham Capital Management, according to the company. Pearl is a NY-based small business funder that was acquired in 2015 by Capital Z Partners, a private equity firm.

“We understand that despite personal credit issues, many small business owners have triumphed in building successful businesses,” said Pearl CEO Solomon Lax. “Locked out of the traditional bank financing channels, those small business owners turn to Pearl Capital Business Funding to enable their dreams. By partnering with Chatham, we are able to make those dreams a reality.”

Chatham has invested in other companies such as iPayment, Vitamin Shoppe, DirectTV, QVC, Neiman Marcus, and 5-hour energy, according to their website.

Pearl also secured $20 Million from Arena Investors, LP in July of last year.

Déjà Vu: Some Small Business Funders are Fading Away

June 20, 2017 Apparently I’m old enough to see this happening all over again. A handful of big names in the alternative small business space are faltering and many of you have asked what this means for the industry. It really doesn’t mean anything other than those who do not learn history are doomed to repeat it.

Apparently I’m old enough to see this happening all over again. A handful of big names in the alternative small business space are faltering and many of you have asked what this means for the industry. It really doesn’t mean anything other than those who do not learn history are doomed to repeat it.

We already went through this in 2008-2009 when at least half of the funders in the merchant cash advance industry were wiped out over the course of several months. Merit Capital Advance, Fast Capital, First Funds, Summit, and Global Swift Funding were the Goliaths of their time. Those companies going out of business seemed unthinkable in principle and for what that would mean for the industry as a whole. Smaller players disappeared too, names like iFunds, Infinicap, and others for those of you who might remember.

Those companies failed. The industry continued.

While it’s easy to finger the financial crisis as the culprit for their demise, the truth, or at least the truth through the fog of war and days gone by, is a lot more relatable. Funders were undone by their dependence on a single source of capital, sloppy underwriting, defaults, rogue ISOs, a race to hit origination targets, overpaying commissions, misplaced predictions, and even stacking. If any of those things remind you of what’s happening today, well then of course there are companies failing.

One lesson from the past is that you won’t necessarily get a year or two to adjust and figure things out. It will seem like everything is great and then suddenly it’s not. No company is going to sit you down and tell you their 1-2 year going-out-of-business plan to prepare you for change. They probably don’t have any such plan, will fight to avoid it and their end may be just as much a shock to themselves as it is to everyone else.

What we’re learning again this time is that some business models just won’t pan out long term. And some business models that used to work no longer work so much today. Things like stacking are not going away. It’s not illegal and no legal precedent has been established against it. If you’re an ISO though, you may be risking a relationship or breaching your own ISO contract by helping a merchant engage in it. So it’s a slippery slope but one that has permanently disrupted the landscape.

I have heard a lot of complaints from ISOs about the supposed decay of funder loyalty, as in they feel their deals are getting swiped. Another lesson from 2008 is that in times of strain, parties are more likely to look to their contracts for guidance and if the contract says they can take your deal after a certain amount of time and they very much financially need to, they probably will do it. The whole hey, we’re friends, we wouldn’t do that kind of thing goes out the window if survival is at stake and the contract allows for certain actions. That also means that if you’re an ISO who has violated an ISO agreement before and got nothing but a shrug in the past, don’t be surprised if suddenly one day you’re put on notice of a breach and are forced to reckon with the consequences of it.

What failures in the industry may also mean is a return to a semblance of order, a return to a code. 2010-2011 was a refreshing time to be in the business with so much unhealthy competition out of the way even though approval terms were less flexible and there were fewer options to shop around for. By 2013 however, a flood of participants discovering the industry for the first time, believed that they had stumbled upon something brand new and lost were the lessons of yore. Some of them introduced lasting change, like ACH debits over merchant accounts splits. Others just replicated the cavalier tactics that had proved fatal in the previous generation, distorting a happy market equilibrium in the process.

Ultimately, the market will prevail, albeit with some new names and new faces at the top. This is the way of things. It has happened before. It will happen again. Look at the companies rising rather than those that are falling. Whatever they are doing may be the future, whether you agree with how they do business or not.

US Treasury Calls for Section 1071 to Be Repealed

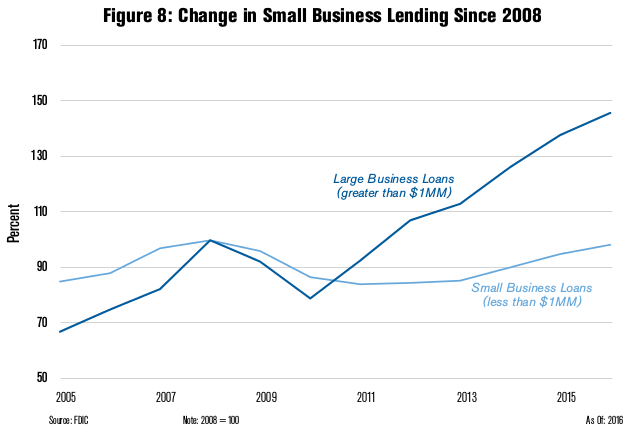

June 19, 2017In a 149-page report prepared for President Trump, the US Treasury has called for the repeal of Section 1071 of Dodd-Frank. Section 1071 is the governing law behind the CFPB’s jump into small business lending data collection. Citing the cost of data collection and anemic small business loan growth since 2008, the Treasury says, “Although financial institutions are not currently required to gather such information [required by the law], many lenders have expressed concern that this requirement will be costly to implement, will directly contribute to higher small business borrowing costs, and reduce access to small business loans.”

“THE PROVISIONS IN THIS SECTION OF DODD-FRANK PERTAINING TO SMALL BUSINESSES SHOULD BE REPEALED TO ENSURE THAT THE INTENDED BENEFITS DO NOT INADVERTENTLY REDUCE THE ABILITY OF SMALL BUSINESSES TO ACCESS CREDIT AT A REASONABLE COST” – US Treasury

The current deadline to reply to the CFPB’s Request For Information is July 14th though industry sources expect the deadline will be pushed back. Of course, if Section 1071 were successfully repealed, the RFI would be moot.

The Choice Act, a bill that just passed the House of Representatives, does indeed repeal Section 1071, but industry sources following the legislation believe the bill will die in the Senate.

Even if a repeal never happens, it is possible that regulations pursuant to Section 1071 may not even go into effect until the early 2020s if similar rulemaking trajectories are to be used as a guide. With payday lending, for example, the CFPB RFI on the matter ended in early 2012 but to-date there still has been no final rule.