Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

deBanked Afterparty in Miami (Please read if you are planning on attending our event tonight)

January 25, 2018 Thank you so much to everyone who is attending our event tonight!

Thank you so much to everyone who is attending our event tonight!

The interest has exceeded all of our expectations… and the hotel’s.

That’s why we’re planning on heading across the street after 8:30PM (when our event ends) to the Delano at 1685 Collins Avenue for continued networking!

Funders, ISOs, if you were not registered through EventBrite tonight or if you’re registered and want to continue connecting with the industry, we’ll be happy to see you after 8:30!

Thanks again for all the continued interest. We have been receiving all your calls, emails and texts about trying to squeeze in to the Gale rooftop tonight. Unfortunately, there are capacity issues that prevent us from making last minute exceptions.

See you at The Gale 5:30 – 8:30. Open bar. Must be RSVP’d.

See you at the Delano across the street after 8:30 (On the main floor and out back on the deck)

MCA Helpline, A Debt Settlement Company, is Sued For Tortious Interference

January 25, 2018

Debt settlement is under fire again. This time it’s a trio of defendants, namely MCA Helpline, LLC, Decision One Debt Relief, LLC and Todd Fisch individually, according to a complaint filed by plaintiff Everest Business Funding on Wednesday in Broward County, Florida.

Everest is seeking damages for Defendants’ tortious interference with at least a dozen of its merchant contracts.

“Defendants have engaged and continue to engage in the business practice of making misleading representations to Everest’s customers; namely, promising to save the merchants money on their existing contracts with Everest when they have no intention or ability to uphold such a promise,” the complaint states. “In so doing, Defendants tortiously interfere with Everest’s merchant agreements by inducing the merchants to breach their contractual obligations to Everest in favor of entering a new payment relationship with the debt relief company.”

Fisch is alleged to be the mastermind behind both MCA Helpline and Decision One Debt Relief.

Complicit ISOs were also put on notice. “To the extent any specific ISOs or their affiliates who have ISO Agreements with Everest have leaked information about Everest’s merchants to Defendants, or to any other third party, such conduct constitutes both a breach of the ISO Agreement and tortious interference with Everest’s merchant contracts,” it reads. “Through the course of discovery in this lawsuit, Everest plans to add as additional Defendants, as yet unidentified ISOs, which have been working with Defendants to target Everest’s merchant accounts in violation of their contractual agreements.”

Everest has been vigorously pursuing debt settlement companies. In September, they, along with Yellowstone Capital, filed a lawsuit against eight defendants (later amended to include 1 more) in New York.

Another lawsuit examining similar issues was also filed last year in New York. In Pearl Gamma Funding and Pearl Beta Funding v Creditors Relief, Pearl tacked on a defamation claim in addition to tortious interference. That case is still pending.

deBanked Connects With Miami on Thursday, January 25th

January 23, 2018

We’re really looking forward to seeing you at deBanked Connect this week on Thursday at the Gale Hotel in Miami. Our 3-hour networking open bar cocktail party from 5:30pm – 8:30pm is sure to be a great opportunity for funders and ISOs. This event booked up to capacity really far in advance and I apologize to everyone who waited too long and missed out.

Thanks to our incredible sponsors, specifically Everest Business Funding who is the headliner, but also National Funding, Knight Capital Funding, NISO, Grand Capital Funding, and Venture Credit Solutions.

Our next event will undoubtedly sell out as well. SO DON’T WAIT UNTIL IT’S TOO LATE TO SIGN UP! Broker Fair 2018 on May 14 at the William Vale in Brooklyn is our signature event!! With so many big names in the industry sponsoring it, it’s a must-attend event for sales reps and ISOs. You’ll be hearing tons more about Broker Fair in the coming weeks and months and I can’t wait to have you be a part of it.

There will be 4 of us from deBanked at The Gale on Thursday, including myself. If you are interested in being cited in a future deBanked Magazine story, be sure to connect with reporter Paul Sweeney who will be there with us.

Controversial Legislator Proposes 4% Interest Rate Cap in New Hampshire

January 22, 2018New Hampshire’s Live Free or Die attitude could be challenged by a bill introduced by the state legislature. House Bill 1800-FN-LOCAL, AN ACT relative to usury, proposes a maximum annual rate of interest allowed in all business transactions in which interest is paid or secured to be capped at 4%. Any interest beyond that would automatically warrant a $10,000 fine to the state treasury by the violator. If passed, the law would go into effect beginning April 1, 2018.

New Hampshire currently has no law governing interest rate limits.

One of the Bill’s sponsors, 86-year-old Representative Dick Marple, was arrested twice in 2016. One of those arrests occurred on the day that he was re-elected.

Marple’s interest rate cap bill and the $10,000 penalty therein for violations, is similar to another bill he proposed last month that would recognize “sovereign citizens.” House Bill 1653, would allow individuals to levy $10,000 fines against corporations and municipal agencies for failures to comply with a proposed modified Uniform Commercial Code law.

Marple’s sovereign citizen beliefs played out in a trial last year where he was found guilty of driving on a suspended license. In the Court’s order, the Honorable M. Kristin Spath wrote, “Although the Court urged Mr. Marple to actively participate in the trial, he declined to do so because of his continued belief that this Court does not have the authority or jurisdiction to hear these matters.”

What’s Lending Got to do With Cryptocurrency?

January 10, 2018 Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

Facebook and Snapchat might be the last things that employees are being distracted by these days. Instead it’s Coinbase and Blockfolio, two cryptocurrency apps, that are quickly stealing the attention of young finance professionals. And the interest in Bitcoin, Ethereum and alt coins is causing some in the industry to wonder if the phenomenon can somehow be connected to online lending and merchant cash advance.

A meetup hosted by partners of Central Diligence Group (CDG) on Tuesday night in NYC, for example, was geared towards cryptocurrency enthusiasts. CDG is a merchant cash advance and business lending consulting firm. Those that attended, talked candidly about Ripple, Bitcoin, Ethereum, and the hot topic of Initial Coin Offerings (ICOs). And it did seem all connected. Companies successfully raised more than $3 billion through ICOs in 2017, for example, some of them online lending companies.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

ETHLend and SALT, blockchain-based p2p lenders, each raised $16.2 million and $48.5 million respectively through ICOs. What’s more, their crypto market caps currently stand at $325 million and $754 million respectively. The latter is nearly twice as valuable as online lender OnDeck. The founder of Ripple, meanwhile, briefly became one of the richest men in the entire world.

Whether these valuations are overdone is besides the point. A smart phone is all that’s required to get in on the action and trade thousands of cryptocurrencies online, many of which move up and down by astronomical percentages over the course of a day. Becoming a millionaire overnight by hitting on the right one is a dream sought after by many. And young people, especially millennials, are become unconsciously comfortable transacting in non-government-backed currencies through technology that completely shuts out banks.

And that may be the shift in all of this to pay attention to. It isn’t that a local restaurant is going to collateralize their Bitcoin to get a loan and outcompete an MCA company, but that a portion of the monetary system eventually starts to sidestep banks.

Trying to collect on that judgment? Good luck tracing the money in cryptos.

Need to freeze funds? You can’t freeze someone’s Bitcoins if they’ve got them stored on their own hardware.

Evaluating a business’s bank statements? The transactions can only be verified on a blockchain.

You might not believe me, but it’s incredibly likely that you’ve encountered a client that has defaulted on an MCA or loan whose stash of money has been obscured in cryptos all the while their bank statements appear to show insolvency.

It’s also likely that you’ve encountered a client that has used the proceeds of their MCA or loan to buy a crypto. Maybe not the whole amount, but with some of it. One study, for example, revealed that 18% of people have purchased Bitcoin using credit. Bloomberg reported that the phrase “buy bitcoin with credit card,” just recently spiked to an all-time high.

People are even taking out mortgages to buy Bitcoin, according to CNBC.

If you think cryptocurrency is an industry completely independent of your business, consider that the market cap of cryptocurrencies is currently valued at more than $700 billion. That’s nearly twice the market cap of Goldman Sachs and JPMorgan, COMBINED. The #3 cryptocurrency by market cap, Ripple, is being pitched almost entirely to traditional financial institutions.

Bet all you want on the prediction that this bubble will burst. Maybe it will. But the underlying technology, transacting without banks in non-government backed currencies that may be difficult to trace and recover, is a genie that’s not returning to its bottle anytime soon.

In the meantime, now might be a good time to poll your employees or colleagues about their knowledge or use of cryptocurrency. You may be surprised by what you find, especially among the younger crowd.

——–

Disclaimer: I currently hold a material amount of Ether, the currency of the Ethereum blockchain.

In 2018, Sell More and Make More Money

January 4, 2018Did you hear about the MCA sales rep that made a $160,000 commission this week on a single deal? It was a monster deal, the largest ever approved by the company that funded it. Numbers like that are proof that facilitating commercial finance deals is still red hot.

That’s me in that photo above, wearing that shirt back in 2009 when the industry was not even a fraction of the size it is today. Hat tip to the friend who found this. I used to joke about putting on your funding pants but perhaps in 2018 it’s time to put on a selling shirt too.

In 2018, will you sell more and make more money?

If you want to operate at the top of your game, I highly suggest you register to attend Broker Fair 2018. With 24 major sponsors already signed on, Broker Fair will be the place to learn, get inspired, and connect with the right people to do even more business.

May the next big commission check belong to you.

Will 2018 Be a Special Year?

December 29, 2017 2018 is going to be different, in a good way. That’s word on the street in the alternative finance industry, many of whom have told me that it’s just something they feel.

2018 is going to be different, in a good way. That’s word on the street in the alternative finance industry, many of whom have told me that it’s just something they feel.

I feel it too. The S&P 500 is at an all-time high, Bitcoin is up more than 1,400% for the year, lenders are lending in full force, and on top of it all, Donald Trump is president. The world is changing and from a one thousand foot view, it’s an exciting time for finance.

2018 will welcome Broker Fair, the inaugural conference for MCA and business loan brokers.

2018 will transform alternative finance into just finance. For example, a mailer I received from PayPal advertising a small business loan up to $500,000 in as quick as 1 business day, included a letter signed by a top manager of Swift Capital. PayPal acquired Swift in 2017. Yesterday’s alternative loan is simply today’s loan. The one-day small business loan is becoming normalized and being offered by widely recognized financial companies.

Ripple surpassed Ethereum this morning to become the 2nd largest cryptocurrency by market cap. Cryptocurrency, once the domain of Bitcoin-obsessed internet anarchists, is quickly being adopted by the world’s largest banks.

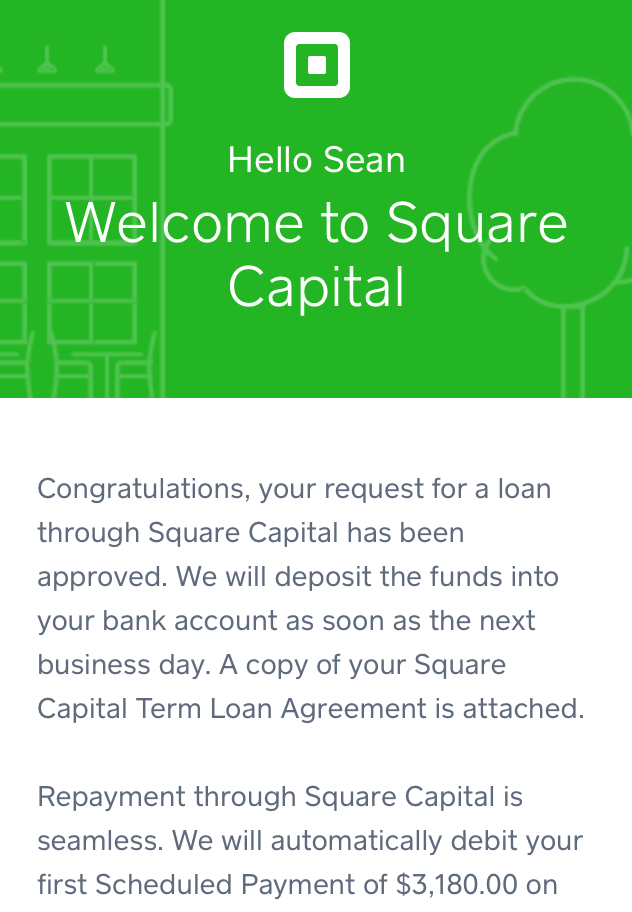

It’s one thing to just talk about innovations in finance and another to realize that you now rely on those innovations. My company got a loan from Square, I got insurance through CoverWallet, I have funds in Lending Club, Prosper, Bitcoin, Ethereum, and Bitcoin Cash. Coinbase is the new etrade. MCA and online business loans are the new community banks. Payments can be made instantly and cost effectively.

2018 will be special because the world that we predicted would come, has come. That means it will be time to think about what will come even next. Online lending has come, instant payments has come, cryptocurrency is fast approaching. What will be the cool edgy hip thing in the ’20s that we may once again refer to as alternative? Mull that one over for a bit and consider that in the next decade the sexy fintech companies of the 20-teens will be stodgy financial institutions in the 2020s. This decade’s innovation will become part of the boring normal manner in which finance is transacted. That’s a fact.

Enjoy 2018. I know I will.

Happy new year,

– Sean

Letter From The Editor

December 23, 2017 It was a year to remember, our sources declare

It was a year to remember, our sources declare

‘Twas the Jan/Feb issue I wrote about my loan from Square

Through March into April salespeople closed deals via text

Through March into April salespeople closed deals via text

As banks looked to fintech as their plan for what’s next

We went to Texas a nexus for finance and lending

We went to Texas a nexus for finance and lending

It was May, maybe June when Bizfi’s final days were pending

Merchants talked, banks adjusted, it was a summer of learnings

Merchants talked, banks adjusted, it was a summer of learnings

For the pressure was on to produce solid quarterly earnings

September, October, liens and judgements were removed

September, October, liens and judgements were removed

But the world hardly noticed and deals still got approved

Winter coats and furry hats meant the year would end soon

Winter coats and furry hats meant the year would end soon

But by golly 10k, no 19k! Bitcoin went straight to the moon!

And so boys and girls the story of ‘17 has been told

And so boys and girls the story of ‘17 has been told

What a time for finance, for money, and a world to behold

See you in ‘18, in ‘19, and the roaring twenties my friend

We’ll be right there, whether you deal in receivables or lend

– Sean Murray

.JPG){kind=link}