Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Maryland’s Latest Merchant Cash Advance Prohibition Bill Failed to Advance

March 18, 2021 Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

Despite the rapid advancement of the newest merchant cash advance prohibition bill in the Maryland state legislature, the bill failed to jump over the final hurdle in a House Committee hearing on Thursday. Delegate Seth Howard (R), who introduced the bill, vigorously advocated for it to move forward so that it could proceed to the Floor, going so far as to say he was willing to make some concessions to at least get “the regulatory structure” of the bill into law.

“I don’t want to snatch defeat from the jaws of victory,” he maintained.

There were several amendments up for consideration, including the inclusion or removal of a 24% APR rate cap on MCA transactions. The subject of APR dominated the light Q&A that took place, but one delegate voiced concern that creating restrictions on capital providers to businesses that might not be able to obtain funding elsewhere would probably be counterproductive. And when a roll call of votes was taken to determine if the Bill should advance to the Floor, he voted no, as did nineteen of his colleagues. Only three voted yes, so the bill did not advance, ending its prospects for the 2021 legislative session. However, it could be reintroduced again in 2022.

Committee Vice-Chair Kathleen Dumais (D) said that she thought the bill “was not ready” despite Delegate Howard “having worked hard on it.” This was Howard’s second try in two years to move it forward. His first attempt, introduced on February 7, 2020, was called the Merchant Cash Advance Prohibition Bill. The more recent one dropped the “prohibition” label but used language that would have effectively prohibited them in the state of Maryland.

Upstart Says Covid Had No Material Impact on Loan Performance, Believes All Loan Underwriting Will be Powered by AI in the Future

March 17, 2021 Yet another online consumer lender has reported that the Covid-era was good for business. Upstart, which went public in December, recorded $1M in profit in Q4 and $6M in profit for the year. Prosper Marketplace, an Upstart competitor, reported an $18.5M profit for 2020 just days earlier.

Yet another online consumer lender has reported that the Covid-era was good for business. Upstart, which went public in December, recorded $1M in profit in Q4 and $6M in profit for the year. Prosper Marketplace, an Upstart competitor, reported an $18.5M profit for 2020 just days earlier.

“Despite the COVID-19 pandemic, we delivered strong growth and profits in Q4 and for the full year 2020,” Upstart CEO Dave Girouard said in the company earnings announcement. “This combination is rare among FinTechs and demonstrates the growing advantages of AI-based lending.”

Upstart actually grew its revenue in 2020 by 42% over the previous year while keeping loan performance steady.

“We’re happy to report that the COVID-19 pandemic had no material impact on the returns that our bank partners and loan investors experienced this past year.”

The company is going full speed ahead on AI-based lending. “We believe virtually all lending will be powered by AI in the future, and we’re in the earliest stages of helping our bank partners successfully navigate that transformation.”

Keenly aware that AI is an overly used buzzword, the company reminded investors about what its AI can actually do.

Our AI models, like all AI systems, are fueled by incredible amounts of data and sophisticated software to interpret that data, while most lenders consider only a handful of variables as part of a lending decision, Upstart’s model considers more than 1,000 variables about each applicant. You can think of these as the columns in a spreadsheet. And as of December 31, 2020, our model was trained on more than 10.5 million unique repayment events.

These are like the rows in the spreadsheet. And we continually upgrade the machine learning software that interprets this data, enabling us to price the next loan on our platform just a bit more accurately. Upstart goes far beyond a singular AI model predicting default risk. We have discrete AI model that improve the entire lending process, including identity fraud, income misrepresentation, loan stacking, prepayment risk, fee optimization, and more.

But of course, our model that targets default risk is the centerpiece of our system. It predicts not just the likelihood that a loan will default, but when that default can be expected to happen.

Upstart also intends to bring that technology to auto lending. The company simultaneously announced that it had acquired Prodigy Software, Inc, a tech that’s been used to assist with selling more than $6B worth of cars.

“…2021, from our perspective with auto, is really a building year,” said Girouard, “And the acquisition of Prodigy, we certainly view as an accelerator toward the point of sale, the majority of the market that happens at the dealership.”

Ireland’s Fintech Industry May Be Coming to North America

March 16, 2021 Americans asked to name an Irish fintech company often say Stripe, the company founded by two Ireland-born brothers that is dual headquartered in San Francisco and Dublin. Recently valued at $95 billion, its financial backers include Sequoia Capital and the Irish government via the National Treasury Management Agency.

Americans asked to name an Irish fintech company often say Stripe, the company founded by two Ireland-born brothers that is dual headquartered in San Francisco and Dublin. Recently valued at $95 billion, its financial backers include Sequoia Capital and the Irish government via the National Treasury Management Agency.

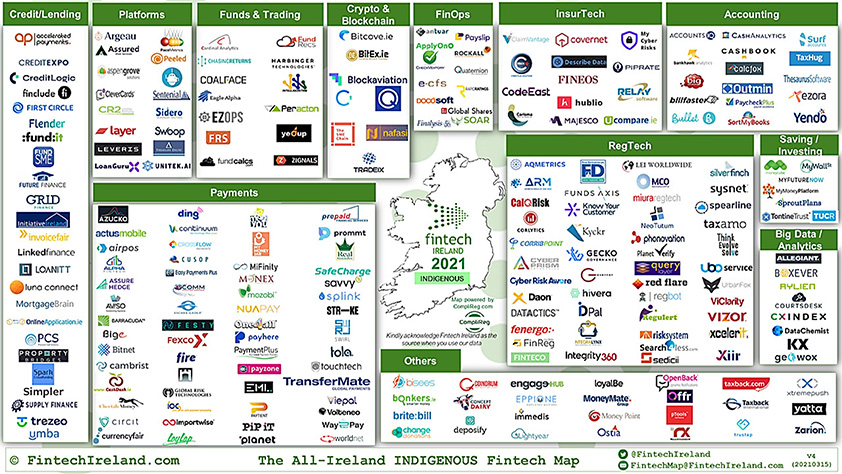

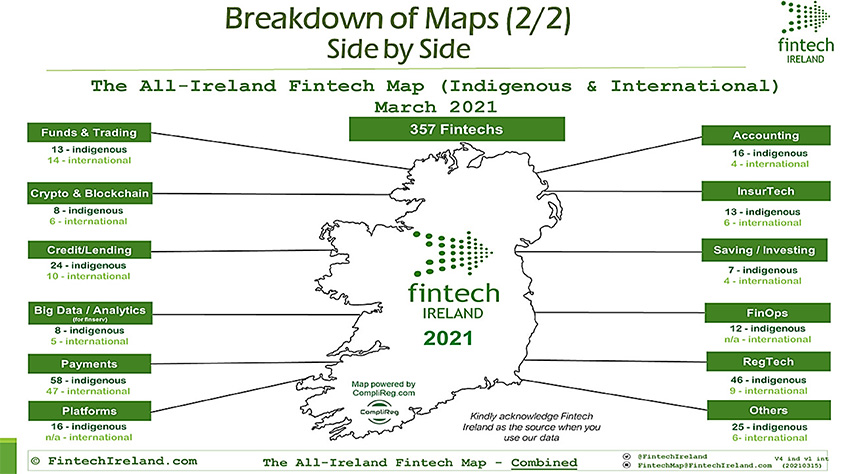

Stripe’s Irish roots may not be a one-off. Though the Republic’s entire population (4.9M) is less than that of New York City (8.7M), it is home to nearly 250 indigenous fintech companies, dozens of which offer lending and payment products, according to the latest Fintech Ireland map. And many have expansion plans in the works.

Despite the close proximity to the UK, the United States and Canada tied for the #1 priority region that homegrown Irish fintech companies said they want to expand to, according to Fintech Ireland’s industry survey. The UK came in 2nd. The majority of Irish fintech companies actually said they prioritized expansion plans for the US and Canada even over expansion in their home country.

A flight from New York to Dublin can be shorter than a flight from New York to San Francisco and Ireland’s primary language is English. 7,000 people work in fintech in Ireland, the bulk of which are based in Dublin.

deBanked evaluated the market in-person during the Fall of 2019 and determined that there are many cultural and operational similarities to the US. A follow-up piece in May 2020 captured how the industry there was faring through the Covid pandemic.

Maryland MCA Prohibition Bill Morphs Into MCA APR Limit, Broker Licensing, Double Dipping, Uniform Disclosure, and Go to Jail Bill

February 18, 2021Update: A Recording of the Hearing is Here

Plans to enact “prohibition” in Maryland on merchant cash advance transactions abruptly came to a halt last year, but the legislature there has brought the issue back front and center in 2021, designing a system of prohibition while dropping the actual word from the name.

No MCA transacted in the state would be permitted to have an estimated APR that exceeds 24%, for example. The penalty for violating such a statute can be imprisonment for up to 3 years.

Newly introduced House Bill 664 (SB0532) would “prohibit a person from engaging in the business of making or soliciting a sales-based financing transaction unless the person is licensed by the Commissioner of Financial Regulation” and would require that an applicant “for a license having $20,000 in available liquid assets and to have demonstrated a sufficient level of responsibility to command public confidence and warrant faith in the honest operation of the business.”

The 26-page bill includes a laundry list of requirements and restrictions like specific disclosures, how to calculate a forward-looking estimated APR on an MCA, and a limitation of 24% on that APR.

The bill draws heavily from the recently passed law in New York, going so far as to copy and paste the section requiring MCA funders to disclose if there is literally any “double dipping” in the contract.

The Commissioner of Financial Regulation would retain sole authority to judge compliance with the law.

A House committee hearing on the bill was conducted yesterday and a subsequent one in the Senate is scheduled for February 23rd at 1pm.

You can read the full version of the Maryland House Bill here.

CFPB’s Reach May Extend to PPP Lending

February 16, 2021 The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The CFPB’s Winter 2021 Supervisory Highlights Report that was published late last month, covered a section on small business lending. And it’s not related to the Bureau’s work on Section 1071.

The foray into non-consumer finance was instead driven by PPP lending.

“Consistent with its authority to ensure compliance with the Equal Credit Opportunity Act (ECOA), the Bureau conducted [Prioritized Assessments] to assess potential fair lending risks attendant to the institutions’ participation in the [PPP] program,” the report said.

Accordingly, the CFPB determined that small business lenders that restricted or limited eligibility such as banks who only permitted applications from existing customers, for example, “may have a disproportionate negative impact on a prohibited basis and run a risk of violating the ECOA and Regulation B.”

The CFPB conceded that it had not actually investigated if violations occurred and noted that the majority of institutions had argued that such limitations were either in place to comply with Know Your Customer legal requirements, to prevent fraud, or both.

The CFPB did not say that it had supervisory authority over non-banks that participated in PPP, but it did signal that its purview was larger than just consumers when it came to the institutions it supervised.

The report can be viewed here.

The CFPB is expected to have more proactive involvement in small business finance under its new incoming director, Rohit Chopra. Chopra’s nomination was formally submitted on February 13th. Dave Uejio, the Bureau’s Chief Strategy Officer, has been serving as Acting Director since President Biden took office.

Lawsuit Against Former MCC Executives Dismissed

February 12, 2021A lawsuit brought by various investment vehicles of Atalaya Capital Managment LP against former officers and/or senior management of Merchant Cash and Capital (later known as Bizfi), was dismissed on Tuesday.

In the judge’s decision, the Hon. Jennifer Schecter said that “plaintiffs seek to hold defendants, former officers and managers of Merchant Cash & Capital, LLC, liable for money plaintiffs lost by investing in the Company. […] Plaintiffs do not sue the Company for breach of contract; instead, they seek to hold the individual defendants liable for the Company’s deficient underwriting through causes of action for negligent mispresentation and fraud. Those claims fail.”

Bizfi failed in 2017 after a long run of being among the largest and earliest merchant cash advance funders in the US.

The case was in the NY Supreme Court under Index No: 655593/2019

New Functionality For Digital Advertisers

February 9, 2021 Today, we’re announcing a new feature for digital advertisers. Businesses advertising on our website now have the option to login with a deBanked account and track their ad click figures in close to real time.

Today, we’re announcing a new feature for digital advertisers. Businesses advertising on our website now have the option to login with a deBanked account and track their ad click figures in close to real time.

We began to roll this out in January to all ad clients that expressed an interest in it. A press release went out this morning.

It’s one of several things that we’ve been working on for a while. Our clients can also view what their current ads are when they log in, even if it’s more than one campaign.

The data is updated on an automated basis and the identities of the visitors that clicked is kept anonymous. We’re also offering white-labeled deBanked-hosted landing pages as a service to assist with managing the conversion process. As everyone knows, we also have designers that can create the ad artwork itself.

deBanked serves a business-to-business market and I think the elephant in the room is that much of the industry’s referral business is being sourced through our website. We outpace all of our competitors on a page view basis by a long shot and we’ve determined that it would be valuable for our digital clients to track the activity we’re generating, and then if further assistance is needed, facilitate the conversion process as well. We think about it from the user perspective too. We want the user clicking those ads to find whatever it is they’re seeking. We’re ultimately striving for an end-to-end experience where all parties are satisfied.

We’ve also compiled a short FAQ about how to interpret the click data.

You can email questions to info@debanked.com.

Thanks so much for being part of the deBanked universe.

– Sean Murray

Enova Pleased With The OnDeck Acquisition, Looking to Divest ODX, OnDeck Canada, OnDeck Australia

February 5, 2021 “We’re very pleased so far with the OnDeck acquisition and as we view the economic landscape, we continue to believe that it’s an excellent time to be increasing our focus on SMB lending,” Enova CEO David Fisher said on the company’s Q4 earnings call. Enova originated $120 million in small business loans in December and $95 million in November. The October figure wasn’t specified, but back-of-the-napkin math based on other provided statistics suggests it was about $54 million.

“We’re very pleased so far with the OnDeck acquisition and as we view the economic landscape, we continue to believe that it’s an excellent time to be increasing our focus on SMB lending,” Enova CEO David Fisher said on the company’s Q4 earnings call. Enova originated $120 million in small business loans in December and $95 million in November. The October figure wasn’t specified, but back-of-the-napkin math based on other provided statistics suggests it was about $54 million.

Growing those originations will continue to be their primary agenda as the economy improves, the company said, while the ODX side of the business may be shown the door.

“While ODX has been able to sign some high-profile bank clients, divesting ODX will allow for more efficient use of capital as the business has over 70 employees but less than $10 million in revenue,” Fisher said.

OnDeck Canada and OnDeck Australia may also be on the chopping block.

“The Australian and Canadian businesses are viable businesses in their respective market,” Fisher said, “but are small compared to OnDeck US operations and are unlikely to have a significant impact on Enova’s overall growth. In addition, OnDeck only has partial ownership of those two businesses.”

Meanwile, OnDeck’s portfolio outlook is improving.

“The percentage of OnDeck receivables past due 30 days and more declined during the quarter from 23.2% in closing to 15.6% at December 31,” said Enova CFO Steve Cunningham.

On the call, JMP analyst David Scharf asked when OnDeck would return to quarterly origination levels of $550M to $650M as it had been enjoying prior to the pandemic.

“I mean I think there’s just way too much uncertainty to be able to answer that,” Fisher replied. “I mean, does the vaccine work great and the economy opens up soon or is there a new strain of the COVID virus that requires lockdowns during the summer? I mean, there’s no way to know. But I think there’s a couple trends that are super encouraging for us and we saw great sequential growth as we talked about throughout the call.”

Fisher also added that they’ve seen a bunch of competitors go out of business. “We think we have a lot of share in the market that we don’t think has shrunk and so we think we’re really well positioned as this pandemic winds down,” he said.