Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Merchant Cash Advance Accounting – A How To Guide

January 13, 2015This is the introduction and first question in an interview between deBanked’s Sean Murray and accountants Yoel Wagschal, CPA and Christina Joy Tharp.

- 2. Do I Need a Special MCA Accountant?

- 3. and 4. Recording Merchant Cash Advance Transactions on the Books

- 5. Merchant Cash Advance Accounting Pitfalls

- 6. Revenue recognition for Merchant Cash Advance

- 7. Q&A – Real questions that MCA companies or syndicators have

Funding small businesses is the easy part of merchant cash advance. Anyone can fund. It’s what comes after that’s tricky and I don’t just mean capturing those receivables you’ve purchased, but also recording everything in such a way that you’re not scrambling around tax time.

I have a B.S. in Accounting but I asked the experts Yoel Wagschal, CPA and Christina Tharp his staff accountant for their insight on managing the books for a merchant cash advance company. We’re still a ways off from April 15th so now is your opportunity to fix whatever you might not have done in 2014 and start off on the right foot for this year. Thanks again to Yoel and Christina for answering these questions.

Q: As a funder, what systems should I have in place to make sure I can:

a. Prepare business tax filing

b. Be ready for an audit to raise capital

c. Know whether or not I am making money

A: First of all you have to understand that every type of business has this exact same question. The answer is that you need to have proper accounting entries and records which will then aid you in creating the financial statements (ie: balance sheet, income statement, statement of retained earnings, and statement of cash flows).

Whether it is a tax filing, a bank audit, or an internal inquiry, the solution is identical because all of those situations require the same financial material in order to answer them. In order to prepare a business tax filing a company must provide its profits and losses. That is the same information provided in an audit to raise capital and it is the same information a business owner needs to see how much money they are making (or losing!).

The exact system is obviously custom fit to your individual business model but it should follow these very basic steps:

i) Think the entire process through from cradle to grave

ii) Be sure to codify where funds are coming in from:

a. Investments from syndicators

b. Payments from merchants

c. Commissions

iii) Be sure to codify where funds are being sent to:

a. Funds to merchants

b. Funds to syndicators

c. Commissions

iv) Be sure there is a system of checks and balances which will alert you to the following common errors:

a. Funds not received from/sent to syndicator

b. Funds not received from/sent to merchant

c. Commissions not received

v) The bank account is the authority while the system is only a representation:

a. Your system balance should reconcile with your bank account

b. It is advisable to have a separate bank account for funding transactions

You will also want to pull up trial balances and earnings reports, which must be input correctly from the very beginning in order for these reports to be accurate and effectual.

What makes this industry different is that an accounting system can make or break an MCA company. For example, a supermarket usually has good POS software for inventory control. If an employee drops a “box of tomatoes” it’s not the end of the world. The loss is either immaterial or if it is material the accounting system will pick up the big monetary discrepancy.

In the MCA industry a “box of tomatoes” could be anything from a $0.05 loss to a $500,000 loss. Because the MCA industry deals with money as its product and is often processing transactions at breakneck speed, there needs to be safeguards in the system to catch any and all mistakes in real time.

Our accounting firm has seen where people built attractive systems which seemed good to the funder. However, if the funder lacks accounting knowledge when this “box of tomatoes” falls out they may not be able to place exactly where the loss occurred. Or even worse, they may not realize a loss has taken place until it is too late. For example, if you wait until the end of the tax year and then discover that merchant payments have been missed how do you recoup those funds? It’s the same situation if incorrect amounts are funded to merchants, if incorrect commissions are paid out, or if syndicators have not invested the funds they were expected to.

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

Should I Start an ISO With Only $2,000?

January 12, 2015A long time ago in a galaxy far, far away…

It is a period of civil war. Rebel sales reps, striking from a hidden ISO, have won their first victory against the evil Galactic Funder.

During the battle, Rebel spies managed to steal secret formulas to the Funder’s ultimate weapon, the UNDERWRITING ALGORITHM, an advanced code with enough power to destroy an entire industry.

Pursued by the Funder’s sinister sales agents, our hero races home with her flash drive, custodian of the stolen formulas that can save her merchants and restore freedom to the industry…

Breaking away to start your own ISO or brokerage in this industry used to be a rite of passage. You started somewhere, learned the ropes, then went off on your own like a Jedi Master.

The stories of reps and underwriters of years past who left their jobs to start their own ISOs are a bit nostalgic. Young twenty-somethings defying authority to plant their own flags in an industry they felt offered unlimited potential. For some, going solo was a rude awakening, a healthy taste of the real world, where you needed to be able to do more than just close the leads you’re given. But for others? Well, today they are the owners or managers of companies worth millions, tens of millions, or hundreds of millions of dollars.

Empires were built not that long ago and they certainly were not in a galaxy far, far away. But today the prospects are much bleaker. The industry has matured and certain channels are saturated. Merchant cash advance and non-bank business lending are no longer part of a young unexplored universe.

So to those that have asked me whether or not it makes sense to start an ISO in 2015, I’d have to say in many cases it does not. It’s a little late in the game. Below is one of the most popular questions posed to me over the last six months:

Q: I’m thinking about starting my own ISO. I have about $2,000 to $5,000 to spend on leads. Do you think I can do it and where should I buy the best leads from?

Q: I’m thinking about starting my own ISO. I have about $2,000 to $5,000 to spend on leads. Do you think I can do it and where should I buy the best leads from?

A: There’s a few things to address here. If you are working out of your house and your rent/mortgage is already taken care of without you having to pay yourself from your new ISO, you may be able to turn a profit starting with something this small. The first problem though is that if you’re not absolutely positive where to get excellent leads, you’re going to spend a lot of money on experimenting with multiple sources. $2,000 might be the cost of an experiment with one lead provider. In other cases, it might be $5,000. Your entire budget could get wiped out in an experiment with just one source.

There may be no barriers to entry in this business, but $2,000 to $5,000 is entirely too little to give yourself a real chance to get off the ground. Direct mail takes a lot of trial and error and thousands of dollars. Google/Bing advertising takes even more trial and error and tens of thousands of dollars before you can get really meaningful results.

And if you’re going to put all your eggs in the UCC marketing basket because of budget, it’s going to be a tough climb uphill.

The companies that do actually have the best leads don’t need a $2,000 startup ISO to sell them to. A big ISO or funder is probably already paying double the price they’re worth.

So how do you stand a chance? You should realize that the odds are you won’t.

And if you need to allocate part of that 2-5k to pay for an office and get set up like a business, you might not have anything left for marketing at all. That’s a horrible place to be!

Lastly, I have seen many ISOs try to become a broker’s broker in order to acquire deals. That means trying to close ISOs to send you deals for you to forward on to a funder as a middleman where you will get a cut if the deal closes. It’s a hustle, and if you can swing this, great, but it’s not exactly a sustainable model especially if the ISO realizes they can go direct to the funder themselves. If you can’t acquire merchants on your own (and deals you stole from the last place you worked at don’t count as acquiring on your own), then you probably shouldn’t be in the ISO business at all.

If you’re going to start an ISO in 2015, I suggest having a minimum $25,000 (50k to be safe) in marketing to start off. And if you don’t know what you’re doing, well then may the force be with you.

Heather Francis Launching New Funding Company

January 5, 2015 One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

One of the Six Women of Alternative Finance is leaving their current position to launch their own funding company. Heather Francis, EVP of Merchant Cash Group appeared in the September/October issue of DailyFunder. A regular at the industry’s conferences and who was in many ways the face of Merchant Cash Group, Francis is moving on to start Elevate Funding.

When the news broke, deBanked asked Francis about the change. This was her response:

“So the start of the new year begins with something exciting for me as I will be leaving Merchant Cash Group to pursue heading up my own funding company. Elevate funding is still in the set up stages and will not be operational and funding until Mid February but I can assure you that with each unveiling of what we will be funding and what we will offer to the Alternative Industry as well as the business owners will help shape a new future. I enjoyed my time at Merchant Cash Group and I wish them all the best but I am excited for this new adventure and to take a lot of the ideas that have been kicking in my head for a while and see them come to fruition. I know it will be difficult and I am greatly looking forward to the challenge. In the words of a Fort Minor song : This is 10% luck, 20% skill, 15% concentrated power of will, 5% pleasure , 50% pain, and a 100% reason to remember the name… Best of luck to all in 2015!”

Elevate will be based in Gainesville, FL.

Despite FinTech Disruptions, Many Thing Stay The Same

January 5, 2015 2014 was an unbelievable year!

2014 was an unbelievable year!

I kicked off last year by opening an account with Lending Club so that I could understand their product. Today I have tens of thousands of dollars invested on their platform and picking up new loans has become part of my daily routine. You could say I’m not surprised they went public a few weeks ago.

I also launched the industry’s first trade publication and ran it as both publisher and chief editor. We produced 6 issues and distributed more than 20,000 print copies combined. Unfortunately the publication will not be continuing further. It is wild to think that it both started and concluded in 2014 as the magazine had a cult-like following.

7 conferences in 4 cities. Las Vegas (twice), San Francisco, New Orleans, and here in New York. I spoke at two of them. Hoping for at least 1 Miami conference this year. Please??? It’s so cold here right now.

OnDeck Capital took a lot of flak in 2014 from both industry insiders and the media. They shrugged it all off and went public on December 17th. Considering they’ve operated on the fringe of the merchant cash advance industry for so long, it was one of those things you had to see to believe. I didn’t get inside the building but I saw the IPO was real from the outside.

I started off 2014 not knowing what a Bitcoin was. Now I have a copy of the entire blockchain, operate a full node (don’t worry I have port 8333 open), have 10 dedicated mining devices running 24/7, have made purchases with bitcoin, conducted countless transfers, and just finished coding a working prototype application using Coinbase’s API. And when I realized that bitcointalk.org and my cryptography books weren’t enough to satisfy my appetite, I found myself talking about bitcoin on IRC; #bitcoin and #bitcoin-pricetalk on irc.freenode.net. I also know who Satoshi Nakamoto really is now too but he made me promise not to tell anyone.

I rebranded Merchant Processing Resource to deBanked, retiring a name I’ve used for 4 years.

I interviewed former Congressman Barney Frank, one of the two architects of the Dodd-Frank Wall Street Reform and Consumer Protection Act (it was only a few questions).

I got asked by a credible movie producer if I would help him on a storyline for a script about Wall Street and the alternative business lending industry. Don’t worry I turned it down!

I jumped on the payment disruption bandwagon and used Square to process credit card transactions all year. You should know that I previously did merchant account sales. I could’ve boarded my own account and set my own fees but I went with Square anyway.

I finally got set up to syndicate on merchant cash advances.

I ran my first 5k in Central Park.

I moved to a different part of Manhattan.

Of course a whole lot more happened. It was a roller coaster year which leads me to believe that 2015 will be impossible to predict. There’s a lot more room to grow in FinTech but it might be time for fresh ideas. Everyone and their mom built an online lending marketplace platform in 2014.

Similarly, it’s also a tough time to become a loan broker or MCA ISO especially if you’re undercapitalized. The easy profit ship has sailed. Press 1s and UCCs aren’t winning business models, at least not ones that will invite outside capital or ensure survival long term.

2014 changed finance but in many ways it stayed the same.

It still takes 2-4 days to confirm an ACH didn’t reject! This is annoying all around. If I add funds to Lending Club on a Monday, it’s not accessible until Friday evening. If you debit a merchant on Monday, you won’t really know if you have it until a few days later. Believe it or not I actually mailed out more checks in 2014 than in any other year of my life. The ACH system appears to be fine until you use something that is far more advanced, something I will probably write about over the next month. Instantaneous payments, low transaction fees, no bank involvement. Yeah, it’s time for ACH to go away…

And with banks, well… I have opened business bank accounts over the last few years with 3 different banks. The one I opened in 2014 required a two hour in-person interview, a process that involved filling out forms by hand and being threatened that the government would shut everything down in a heartbeat if they found out that I so much as breathed wrong on an ATM. It was a repeat of prior account opening experiences. Although I’ve never had an account closed for doing anything wrong (because I’m not actually doing anything wrong), it is easy to see how much regulatory pressure banks are under. Swiping your debit card upside down could cause the entire bank to get an Operation Choke Point subpoena. They want your business but they’re scared to death of anything you might do with a bank account.

All the major peer-to-peer platforms of 2014 became centralized. Lending Club and Prosper don’t even fall in the p2p category anymore. The market trend has been to create a platform designed for the little guys and then hand it over to a bank or institutional money to do all the funding. In some ways it’s easier to deal with a handful of big players instead of thousands or millions of retail investors. But with the regulatory environment uncertain on so many new investment products, it’s probably also safer to deal with institutional investors, lest the regulators claim they violated a consumer protection law they thought up this morning.

Banks continue to be the biggest obstacle to innovation because at the end of the day, all payments flow through them. How can one deBank and truly disrupt?

Hopefully we’ll find out in 2015. Happy belated New Year.

With OnDeck IPO, Strangers Walk Among Us

December 18, 2014The future isn’t ours to make anymore. Not ours alone anyway. Last week the industry was a group of insiders. Today the outsiders walk among us.

$ONDK looking good, but surely this will fall by tomorrow.

— Nealio (@IpoBandwagonTagAlong) Dec. 17 at 11:07 AM

I don’t know who IpoBandWagonTagAlong is but he’s now an influencer in the industry. Almost 13 million shares of OnDeck Capital traded today, its very first day on the NYSE.

$ondk new ipo watching this..seems similar business to $lc

— kunal desai (@kunal00) Dec. 17 at 01:59 PM

It hurts to see “seems similar business to [Lending Club]” as the information being gleaned about OnDeck. I could spend an entire week contrasting the differences but it doesn’t matter anymore. Opinions about OnDeck and the industry they’re part of are about to be formed in tweet-sized pieces at rapid fire pace. Anything longer and the opportunity presenting itself on a trade might pass. Wild.

If you’re in the merchant cash advance business, you’re about to learn that describing the purchase of future sales in anything more than 140 characters is going to work against you. You will inevitably be asked if you do what OnDeck does and you better be concise.

Exactly 140:

“We provide working capital to small businesses by leveraging their future sales. It’s not a loan but it is in some ways similar to OnDeck :)”

Or you could simplify it further and just write:

“Seems similar”

Proud to have OnDeck join the NYSE’s community of the world’s leading, most-recognized companies (NYSE: $ONDK ) pic.twitter.com/ReozilWjbR

— NYSE (@nyse) December 17, 2014

The most striking thing I experienced on opening day was watching so many OnDeck bears transform into OnDeck bulls. Lots of buy orders were placed by those that have been chugging hater-ade for years.

I think that despite reservations with their business model, there was a desire to touch the company in some way, to feel like they were a part of the industry’s milestone. I totally get it. But that brings up an interesting question, how much of the stock can you touch until you start to hold some sway?

I mean shareholders are owners right?

Theoretically, could a terminated ISO buy up shares and then start making demands about re-establishing a partnership? What is the protocol here? Can OnDeck’s ISOs buy OnDeck? Or OnDeck’s competitors? I don’t mean a controlling stake but enough to make some noise. Imagine OnDeck being a funder for the ISOs by the ISOs! If a huge ISO is terminated, does that have to be announced to the public at the same time that the ISO community finds out?

This is a very gossipy industry and coincidentally, I run practically all the industry gossip websites so people like me want to know.

What if a merchant owns shares of the company it is applying to? Is that a positive underwriting data point?

With an office close to the New York Stock Exchange, I was able to at least snap off a few pics of the big banner displayed outside.

And if you’re wondering if I bought stock in OnDeck, I did not. I didn’t buy Lending Club either. It has nothing to do with how I feel about either company.

According to Crain’s, OnDeck’s “$1.32 billion market cap at its debut was the biggest for a venture capital-backed New York City tech company since 1999.” The stock exploded upward almost 40% from its open today. A lot of folks in the industry bought in and the rest is history.

Congratulations OnDeck Capital.

Confessions of a Bitcoin Miner

December 18, 2014If you’re even vaguely familiar with Bitcoin, you’ve probably heard that you can mine them. It’s one of Bitcoin’s most unfortunate pieces of jargon because it sounds like a scam. We can’t mine U.S. Dollars so there’s no frame of reference for what enthusiasts are talking about. We can mine gold and silver of course, but how the heck can one mine a digital currency? It’s clear there’s more to Bitcoin than just being a form of money and that frightens people. It certainly frightened me.

The first time I imagined bitcoin mining, I pictured sentinels from The Matrix drilling down with unrelenting intensity towards the last human city of Zion. Perhaps the humans were hoarding a vast trove of valuable bitcoins and a war was being waged to achieve digital hegemony. Like Ray in Ghostbusters, I couldn’t help it. The thought just popped in there.

The first time I imagined bitcoin mining, I pictured sentinels from The Matrix drilling down with unrelenting intensity towards the last human city of Zion. Perhaps the humans were hoarding a vast trove of valuable bitcoins and a war was being waged to achieve digital hegemony. Like Ray in Ghostbusters, I couldn’t help it. The thought just popped in there.

The next thought was that I better stay away from Bitcoin. It was easier to take the blue pill where “the [Bitcoin] story ends, you wake up in your bed and believe whatever you want to believe.” That’s what many consumers have done in the past. And who could blame them? I liked my life without Bitcoin in it, so why mess it up?

But the maniac I am, I took the red pill and explored just how the deep the rabbit hole goes.

I mined some bitcoins and the machines didn’t kill me, at least so far. I’m mining them right now as I type this. If you’re getting excited that I’m about to tell you that I’m getting rich while you fools sit on the sidelines, you’re going to be disappointed. There is no actual mining. It’s just slang for facilitating bitcoin transactions over the Internet. Womp womp. If people weren’t sending bitcoins back and forth, then there would be nothing to facilitate and therefore nothing to mine.

To illustrate simply, I’ll start off by reminding you that Bitcoin has no central authority. There is no Visa, no banks, and no Federal Reserve to sign off on a transaction. Instead Bitcoin transactions are validated by computers connected to the Internet running free Bitcoin software.

To illustrate simply, I’ll start off by reminding you that Bitcoin has no central authority. There is no Visa, no banks, and no Federal Reserve to sign off on a transaction. Instead Bitcoin transactions are validated by computers connected to the Internet running free Bitcoin software.

If I have 5 bitcoins and I send 3 to you, computers all over the world running this software are processing algorithms to validate this and make them permanent in a global ledger. The computers make sure you really have those bitcoins to send and then transfers them. You can’t create a fake bitcoin or spend one you’ve already spent because the Bitcoin system will know about it.

On just a single day there are nearly one hundred thousand bitcoin transactions. That’s too much for just a few computers to handle, not to mention that the processing power required to validate them is intense. Validating transactions requires lots of processing power and utilizing processing power has a cost in electricity.

So it pays

The Bitcoin system has a built in reward system to incentivize people around the world to keep the system in order. If your computer achieves a specific milestone while facilitating transactions, you are rewarded with bitcoins. Again, don’t get excited. These milestones are extremely rare to reach and totally random (for the record it’s called solving a block). You could facilitate transactions for 200 years and never get any bitcoins back as a reward.

But while random, it’s a probability game. The faster your processing power, the better your odds of being the lucky computer to receive the reward. That’s a necessary but unfortunate component to Bitcoin because there’s a built-in arbitrage opportunity. Why be a passive facilitator when you could arm your computer with a faster processor and rig the odds in your favor? If your computer was significantly faster than the other ones on the network, you could potentially get rewarded bitcoins often enough and with enough consistency to cover both the cost of your upgraded computer and the electricity to keep it cranked up.

And with that understanding, an international arms race began for increased processing power. Up until early 2013 you could quite easily profit from being a facilitator. Those folks didn’t see themselves as facilitators anymore but as miners. It wasn’t a passive activity. It was a business, like hauling ore out of a silver mine.

Today, so many people have tricked out their processors that it’s nearly impossible to get an edge. In fact, mining often results in losses. I have experienced a net loss in actual U.S. dollars through mining even though I’ve acquired fractions of bitcoins. Net loss? whuh?!

Forget about using your desktop or laptop to mine bitcoins. That’s so 2011. Engineers went on to build special hardware chips much better than household computers that do nothing other than process calculations for bitcoin transactions. Then came small boxes of chips, then large ones…

And when everyone started buying large bitcoin processing boxes, they began to buy two or three of them…

Then a stack of them…

Then a room full…

Then a warehouse full…

And of course a lot of additional money had to be spent on cooling, ventilation, and protecting against fires.

This is where a little problem started. Once everybody was using a million dollars worth of specialized hardware for speed and was spending tens of thousands of dollars per month on electricity, the edge was constantly being neutralized. Worse, the frequency that bitcoins are awarded per day does not increase. There will only be 21 million bitcoins ever placed in circulation. They’re awarded through mining at a fixed frequency. You can try to be the recipient of each reward but the frequency of which they’re awarded doesn’t increase.

Bummer for those that have amassed nuclear arsenal sized mining operations.

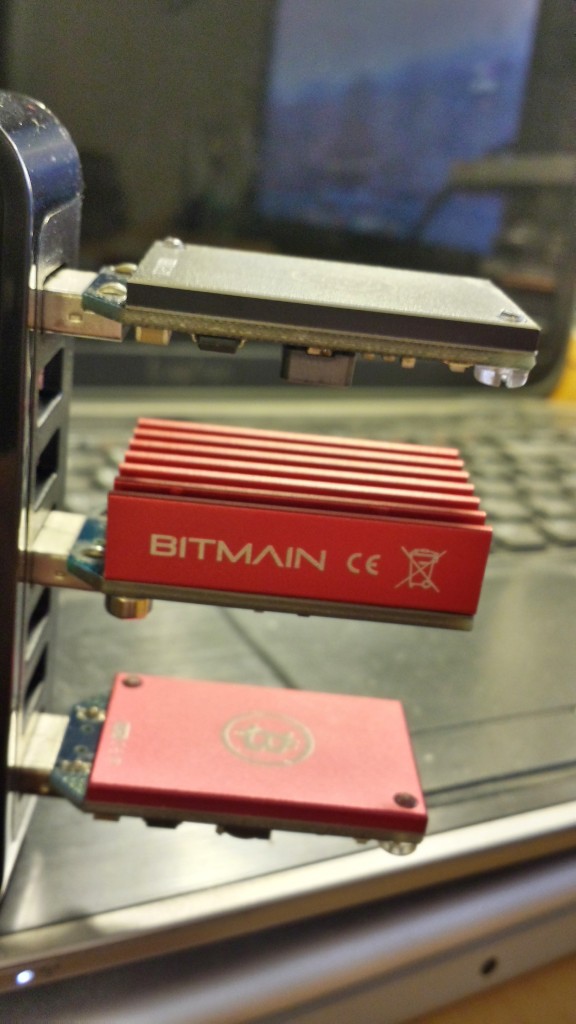

But also bummer for me. This is the extent of my mining equipment.

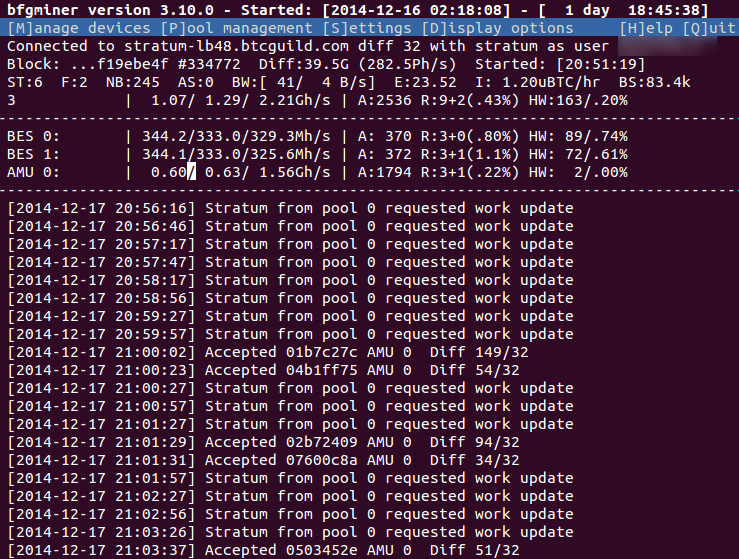

I have three small mining chips all connected via a USB strip. The outer pieces are ASICMiner Block Erupters and between them is a Bitmain Antminer U2. They run 24/7 connected to my home laptop. I can monitor their activity through this little window on my screen:

Combined they are crunching out an average of 2.2 Giga hashes (GH/s) per second, a speed so insignificant compared to the network’s competition that I will probably die without ever receiving a reward of bitcoins.

Unless…

Join forces

There’s a trick to mining to ensure you don’t die rewardless. You can combine your processing power with other miners and leverage your chances. Then if the group’s effort yields a reward, it’ll be distributed on a prorated basis. Someone got this idea a long time ago and in today’s ultra competitive environment, it’s practically a must.

They’re called mining pools. Pools aren’t just a couple of friends, they’re nearly small cities of miners working together collaboratively. The pool I mine in (BTC Guild) has 14,000 to 16,000 users mining together at any one moment and a single user could have an entire warehouse full of mining equipment. In the last hour, the fastest user provided 1,047,666.38 GH/s worth of power to our pool. That’s 476,211x more than what I contributed and he is just 1 of 15,000 users in our pool. woah!

What’s even more wild is that BTC Guild only makes up 5% of the world’s Bitcoin mining power. And yet because I am part of that pool I am paid a prorated amount for every reward the team earns. Surprisingly, that number is not zero. Running 24/7, I am earning an average of 60,000 satoshis a month.

The exchange rate of Bitcoin is extremely volatile but at this moment 60,000 satoshis is equivalent to 19 cents. Yes, 19 cents per month!

And don’t forget that the mining chips cost money to buy and running them 24/7 runs up more than 19 cents worth of electricity used. This means Bitcoin mining isn’t about getting rich. I’m losing money mining. It’s a hobby or benefit conferred upon the digital currency system to keep it running smoothly and accurately. Well at least for me…

Remember that miner that’s out-processing me on a scale of 476,211 to 1? He’s earning about $90,000 per month. I don’t know what his expenses are to run an operation like that but I’m sure it’s not cheap. His biggest enemy is that the value of Bitcoin to the dollar has fallen pretty heavily this year. $90,000 a month in revenue could become $45,000 a month just through exchange rate risk. Those are pretty high stakes to gamble with. But it could also become $180,000!

And whether the big players like that mine or don’t is irrelevant. Whether he makes money or not doesn’t matter. Arbitrage opportunities in the facilitation of transactions is for ultra geeks with big bucks. Mining as a hobby is for regular geeks. It’ll cost some money to do but you get to contribute to a system you believe in.

As for you, the potential average currency user, mining is not really of any consequence. The facilitation of digital transactions already happens with dollars, euros, and pounds. In My Journey to Bitcoin, I explained that buying a cup of coffee with a credit card requires 8 people to get paid for the transaction. Sure the process is completely different for Bitcoin but so what? Bitcoin is unique.

The problem is the mining terminology. It should be called facilitation but that doesn’t sound sexy especially if you are trying to convince an investor to give you $1 million to take advantage of potential arbitrage opportunities on the network.

And that’s about it. The real story behind mining isn’t so scary and you won’t necessarily be at any disadvantage if you still have no idea what the hell mining is. Bitcoin is full of technical nonsense best left to geeks, but you as an actual currency user do not have to worry about a lot of it.

If you’re at all like me though, obsessively curious about how things work and excited to try them out, I’m happy to clue you into the mechanics of mining and even get into the finer details behind it.

An ASIC Block Erupter costs about $10 on Amazon or eBay. I run Ubuntu Linux as my native desktop OS at home (geeky I know) but you should be able to do it with Mac or Windows. The mining software I use is BFG Miner 3.10 and I use BTC Guild as my pool. Admittedly, I am waiting for a delivery of two more Antminer U2s (5x faster than the Erupters but just as cheap) and a delivery of two Antminer U3s (210x faster than the Erupters). I will in all likelihood not achieve a profit even with the additional equipment. And that’s okay, it’s enjoyable just messing with the gizmos.

The best way to learn about Bitcoin is to try it yourself. Hey maybe you’ll hate it, but at least it’ll be based off experience. You can buy fractions of a Bitcoin, even just a few dollars worth from Coinbase. From there you can shop online, convert them back to cash, or send them all to me. 😉

I’m not afraid to say that I mine bitcoins, even if it’s infinitesimally small amounts. What else did you expect from a guy running the deBanked website?

I put my bitcoins where my mouth is. If you’re into alternative finance too, it’s finally time you gave in and tried it.

Through OnDeck Capital, An Industry Wins

December 16, 2014 Call it merchant cash advance, non-bank business lending, or financial disintermediation. Whatever floats your boat. On December 17th an entire financial methodology will be validated, the daily repayment method. Daily payments don’t exist anywhere else in lending but ’round these parts it’s the standard. It’s what makes unbankable businesses bankable.

Call it merchant cash advance, non-bank business lending, or financial disintermediation. Whatever floats your boat. On December 17th an entire financial methodology will be validated, the daily repayment method. Daily payments don’t exist anywhere else in lending but ’round these parts it’s the standard. It’s what makes unbankable businesses bankable.

OnDeck is a lender. They target small businesses. The costs are high. Anyone could feasibly do those things and plenty are doing them, but only a certain segment of fintech companies utilize daily payments and most of those are merchant cash advance companies. OnDeck is a lender but like it or not their core repayment mechanism overlaps with an industry well known for being even more expensive.

Daily payments are so unique and so revolutionary that it hasn’t sunk in to the masses yet. Even the press glosses over this fine detail to instead dwell on things like APRs and social media’s role in approvals. Daily payment and daily repayment look like tech jargon, some kind of code for a backend computer process to hotwire an anomalous rate algorithm.

Daily payments mean borrowers have to make payments every single business day. It’s daily, get it? If the sun rises and it’s not Saturday or Sunday, it’s time to make a payment. I’m not saying there’s something wrong with this. I’m a proponent of this mechanism. It works for business owners that struggle to make a single lump sum payment each month and it works for lenders who need to mitigate and monitor their risk as much as possible.

I feel it’s better to know there was a problem that started yesterday than to learn there was a problem that started 29 days ago. That’s how OnDeck thinks too. And business owners can incorporate the daily deduction into their normal business operations instead of fretting to cover the balance for a big debit the day before a monthly payment is due.

I feel it’s better to know there was a problem that started yesterday than to learn there was a problem that started 29 days ago. That’s how OnDeck thinks too. And business owners can incorporate the daily deduction into their normal business operations instead of fretting to cover the balance for a big debit the day before a monthly payment is due.

This isn’t just a theoretical design that can’t function in practice. It’s been working for lenders and factors since AdvanceMe (Now CAN Capital) started doing it in 1998. The daily payment methodology has survived the Dot Com Bust and the Great Recession. It’s grown to a $3 – $5 billion a year industry. By some measures, it’s taken a hell of a long time to go this mainstream.

But it’s here. The press will call OnDeck a lender, a tech company, or a combination of both. They’re a sign of the times but they are unique in that they will show the world that daily payments have a place in the modern economy. With OnDeck leading the way, traditional lenders may consider leveraging their methodology to serve categories of risk they usually shy away from.

I’ve never heard of a business credit card that required payments to be made every day. Some might think that defeats the purpose of credit. OnDeck proves it doesn’t. And 100+ merchant cash advance companies serve as a secondary validation. Perhaps there are lenders that have considered a daily payment system previously and feared the political or legal environment was too risky. But OnDeck is making no apology about what they’re doing or how they’re doing it. They’re putting themselves on the open market, surrendering themselves to total scrutiny.

CAN Capital is gearing up to follow them, the pioneers who first experimented with daily payments 16 years ago. And while OnDeck bemoans their loan program being compared to merchant cash advance, CAN is made up of two departments, one of which is undoubtedly a merchant cash advance service provider.

CAN Capital is gearing up to follow them, the pioneers who first experimented with daily payments 16 years ago. And while OnDeck bemoans their loan program being compared to merchant cash advance, CAN is made up of two departments, one of which is undoubtedly a merchant cash advance service provider.

And there you have it. It’s not all about algorithms or tech or using facebook activity to judge a borrower. Those are old ideas now. OnDeck smashes down the door with something completely different, something that nobody is even talking about, daily payments.

December 17th is Wednesday and just about all of OnDeck’s borrowers will be making a payment. A good many of them won’t even notice. That’s the great part about layering it in as a daily cash flow expense. There’s no worrying about it at the end of the month. If they underwrite the borrower financials well enough, it should be completely painless. That’s not always the case, but it’s the goal.

You can’t possibly understand OnDeck until you understand daily payments. With this IPO, an entire industry wins.

How to Use Bitcoin

December 8, 2014 The best way to get comfortable with bitcoin is to just try using it yourself. Even though there are many technological, mathematical and confusing layers to bitcoin, the currency aspect of it is by far the easiest to use and understand.

The best way to get comfortable with bitcoin is to just try using it yourself. Even though there are many technological, mathematical and confusing layers to bitcoin, the currency aspect of it is by far the easiest to use and understand.

With that said, here’s how you can dip your toes in and become a big bitcoin kahuna:

1. Open an account on Coinbase.

2. You will need to buy/exchange bitcoins using your regular currency such as US dollars. To do this you will need to connect your bank account to Coinbase. This is what I did. Also it will ask you to enter your cell phone number for two-factor password authentication to prevent hacking.

3. Decide how many bitcoins you want to buy. I bought 1 whole BTC but you can buy fractions of 1 if it makes you feel comfortable. Choose whatever amount you want. You can always buy more or sell your bitcoins back into dollars.

4. Bitcoins will be deposited in your account. Coinbase will store them for you along with the private key to use them. You can choose to export your bitcoins but you don’t have to. I keep mine at Coinbase.

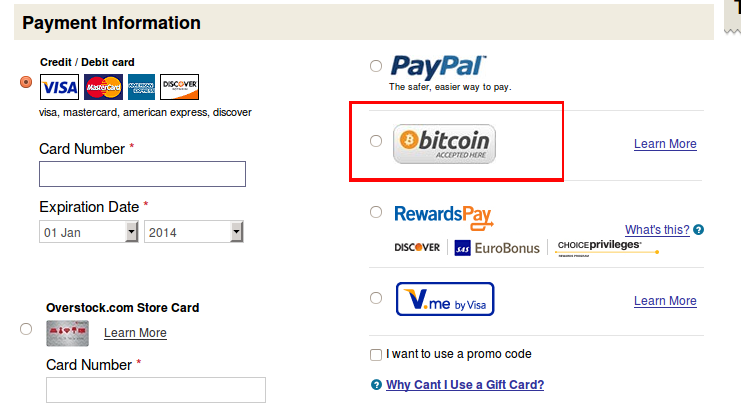

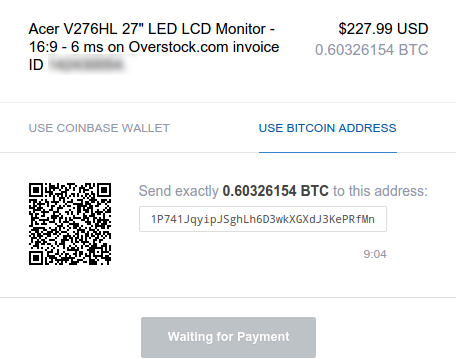

5. Shop anywhere that accepts bitcoin. I shopped at overstock.com.

6. On overstock.com, I selected the item I wanted and placed it in my shopping cart. For payment method, I selected bitcoin.

7. There are two ways you can initiate the bitcoin payment to overstock:

— A. Manually send bitcoins to the address provided. A random receiving address is created for each transaction.

— B. Use your Coinbase wallet (the option on the left. This is easiest and what you should do)

8. If you used option B above, Coinbase will automatically transfer the bitcoins to overstock.com and your order will be placed instantaneously.

All finished. You’ve officially joined the world of bitcoin!

—————–

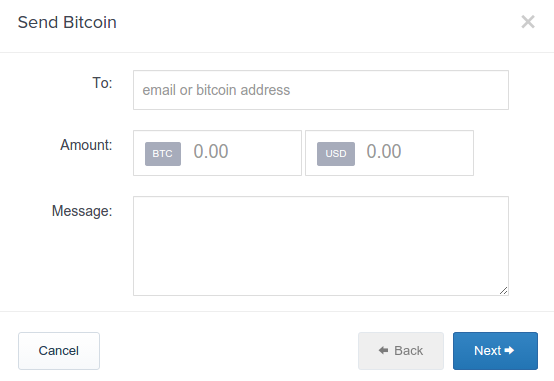

Need to send a payment manually? It’s easy!

1. Log on to Coinbase.

2. Click “My Wallet” on the left hand side.

3. Click “Send”

4. Make sure you know the recipient’s bitcoin address. If you are making a payment to advertise here on debanked.com, this is an address I will supply you with. Some parties create a unique receiving address for each transaction but they can be reused.

5. Internet connected bitcoin miners around the world will automatically facilitate the transaction. This should take about 10 minutes at most. There is nothing you need to do other than wait for the receiving party to confirm. It is impossible for them to deny receipt of the bitcoins as all transactions are verified and public in the Bitcoin Blockchain.

All finished. You’re now a pro!