Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Lending Club (LC) Q4 Earnings Call

February 23, 2015 The first company to bring platform lending into the public eye will release their 4th Quarter and 2014 earnings on Tuesday, February 24th at 5pm EST. Anyone can join the live webcast by clicking here. If not by a computer, you can also dial in by phone at 888-317-6003. Use conference ID 4117710 ten minutes prior to the start of the call.

The first company to bring platform lending into the public eye will release their 4th Quarter and 2014 earnings on Tuesday, February 24th at 5pm EST. Anyone can join the live webcast by clicking here. If not by a computer, you can also dial in by phone at 888-317-6003. Use conference ID 4117710 ten minutes prior to the start of the call.

Investor attitudes are likely to be affected by the outcome of OnDeck’s earnings. While the two companies have different models, they have generally followed the same ups and downs. Many investors are still not clear how they’re different. Lending Club earns fee income by servicing loans and is not exposed to the risk of the loans themselves. Some critics believe that puts them at odds with their platform lenders over the long term.

Lending Club has already experienced a low of $18.30 a share and a high of $29.29. It closed yesterday at $22.89.

Since going public a few months ago, they announced a partnership with Alibaba and Google.

OnDeck 4th Quarter Earnings Call

February 21, 2015 OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

This is a surprisingly crucial moment for OnDeck who has recorded losses every quarter since inception except for the one just prior to the IPO. Since then the company has been confused as a Lending Club for businesses. The companies differ in that OnDeck’s core business is lending and Lending Club’s is servicing fees.

Critics have called out OnDeck’s high interest rates which top out at 99% APR.

In just a couple months, OnDeck has bounced from a high of $28.98 per share to a low of $14.52. It closed Friday at $18.37.

Announcement: Dwolla partnership U.S. Treasury

February 19, 2015Company Announcement

Dwolla to help U.S. Treasury go paperless, prepare for a secure digital future

Each year the The U.S. Department of the Treasury’s Bureau of the Fiscal Service collects 400 million transactions worth $3.7 trillion. Ensuring that its collection programs stay relevant, safe, and cost-effective, they recently launched a new Digital Wallet program. The new initiative aims to modernize the way our country collects and distributes payments through the convenient offering of safe and innovative payment options. In June of 2013, the Digital Wallet initiative issued a request for proposal, asking national payment platforms to help the 225-year-old Treasury Department improve its flagship revenue collections product, Pay.Gov.

Each year the The U.S. Department of the Treasury’s Bureau of the Fiscal Service collects 400 million transactions worth $3.7 trillion. Ensuring that its collection programs stay relevant, safe, and cost-effective, they recently launched a new Digital Wallet program. The new initiative aims to modernize the way our country collects and distributes payments through the convenient offering of safe and innovative payment options. In June of 2013, the Digital Wallet initiative issued a request for proposal, asking national payment platforms to help the 225-year-old Treasury Department improve its flagship revenue collections product, Pay.Gov.

With existing partnerships with Microsoft Government and state administrations, Dwolla’s flexible architecture makes for an ideal partner in helping modernize public payments. Today, we’re excited to announce our selection as the U.S. Treasury’s first Digital Wallet partners, alongside PayPal (and ApplePay).

What is Pay.Gov? It’s smart government.

Nearly 200 federal agencies, ranging from the Department of Interior to the Department of Defense, use the U.S. Treasury’s Pay.gov platform to create and host custom online payment forms, collecting over 100 million transactions worth approximately $110 billion per year. These simple forms, which hide a sophisticated software and accounting system, allow federal agencies to collect and track non-income tax payments for things like climbing Denali or court fees. It’s a lot like Dwolla Forms, but made exclusively for the federal government.

By outsourcing their revenue collection needs to Pay.Gov, federal agencies not only provide taxpayers an improved experience but also streamline their own payment operations. In doing this, they reduce the operational costs, inefficiencies, and foregone payments. Simply put, Pay.Gov increases revenue for agencies and saves taxpayers money.

How is Dwolla involved? How would this impact me?

Dwolla is now a live payment option for many US agencies (and this will grow over time)–allowing any taxpayer with a U.S. bank or credit union account to use Dwolla’s simple and secure online checkout experience to pay for a whole host of federal fees, products, and permits.

No cards. No checks. No pre-existing Dwolla account required. No sharing of sensitive payment information with the federal government.

What is Dwolla? A secure and modern way to make bank transfers.

When we began building the Dwolla payment network in 2008, we set out to create the ideal way to send money. What we quickly found is that the ideal way to move money has changed since the 1960s and 70s, and the only way to solve the problem was to start over.

Starting fresh with over 40 years of technological advancements, Dwolla was able to create an end-to-end payment network that modernized the legacy bank systems—making it easier to use, more accessible, and more secure. Today, we work with anyone or anything connected to the Internet, from solopreneurs to publicly traded companies, exchange infrastructures to software developers, state governments to financial institutions. We help our community rethink their payment operations, product offerings, and user experiences.

Create new standards in security and privacy: Dwolla has baked new technologies into its network, like authentication and tokenization, that eliminate sensitive financial information from a typical transaction.

Solve problems for all: Free turnkey products, like MassPay or Dwolla Forms, make it easy for anyone to send or receive funds without any existing technical know-how, while a healthy library of developer docs and APIs make it easy to plug Dwolla into nearly any platform, existing operation, or your own creation. Additional levels of support and customization are available and affordable.

Create a powerful, but flexible infrastructure: A simple, and dynamic platform, Dwolla was designed to handle the unique considerations of governments.

Create a platform for future innovation: Whether its mobile applications, real-time payments, or tokenization, Dwolla benefits are freely accessible via our API and developer documentation, allowing the network to scale and solve for the unique needs of an evolving payment landscape.

So what Dwolla can do for you? Grab a brochure from Dwolla.com/government or sign up for our upcoming webinar by emailing government@dwolla.com.

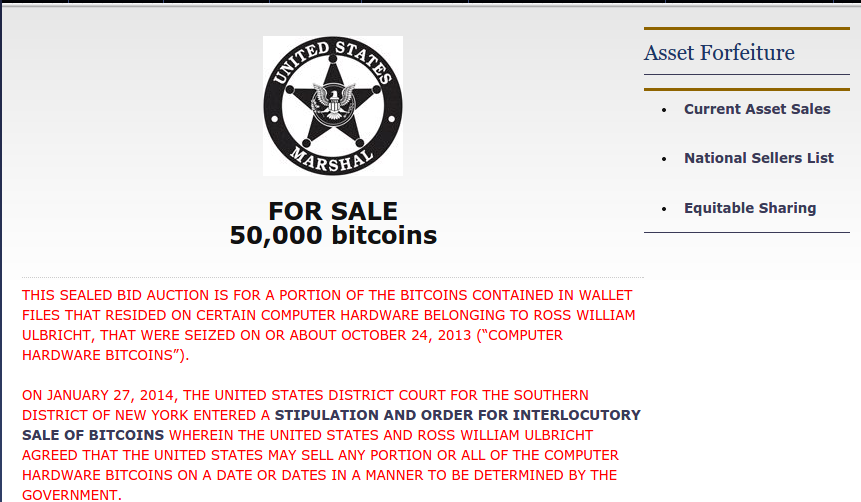

Federal Government Selling Bitcoins

February 18, 2015 If the webpage didn’t say www.usmarshals.gov in the address bar, it’d look like a poorly disguised scam. The page, which looks like it came out of the 1990s (no SSL either for a government website?) is offering 50,000 bitcoins for sale, an amount worth $11.8 million at current market prices.

If the webpage didn’t say www.usmarshals.gov in the address bar, it’d look like a poorly disguised scam. The page, which looks like it came out of the 1990s (no SSL either for a government website?) is offering 50,000 bitcoins for sale, an amount worth $11.8 million at current market prices.

This sealed bid auction is for 50,000 bitcoins separated into two series: Series A (10 blocks of 2,000 bitcoins), and Series B (10 blocks of 3,000 bitcoins). You will not have the opportunity to view other bids. You will not have the opportunity to change your bid once submitted.

Bidding ends at Noon on March 2nd and in order to bid you have to wire the U.S. Marshals at least $100,000 upfront just to be considered a legitimate bidder.

The old fashion system instructs bidders to email them their driver’s license, completed bidder form, and receipt that says they wired them a hundred grand. There’s a special email address to do this and they should hear back from someone if they get approved.

I bet you never thought you’d seen an email address like this, USMSBitcoins@usdoj.gov.

So why are the U.S. Marshals in the Bitcoin business? Surely you know about Silk Road already…

If you want to get in but don’t have enough to cover a lavish bid, why not syndicate it out? That’s allowed:

Can I form a syndicate of buyers?

The person or entity that registers to bid on this auction must satisfy all registration requirements, including certifying that the bidder is not acting in concert with the defendant or defendant entity. This certification extends and applies to all members of a syndicate. The primary bidder should perform whatever due diligence the bidder feels is necessary in order to comfortably make that certification.

And if you don’t win, the Marshals will just ACH your deposit back, but not until after they’ve probably put you on some kind of watch list. Nothing says suspicious person like randomly wiring 100k+ to the U.S. Marshals just so you can be considered a bitcoin bidder. Expect them to be curious about who you are.

Hopefully their technology is more advanced than the way their website looks though.

It’s Okay For a Business to Act Like a Business

February 10, 2015 A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

A day after I delved into the fate of the industry’s bad paper, Fundera’s Brayden McCarthy discussed a paper of his own on Forbes, a Small Business Borrowers’ Bill of Rights. While our articles were quite different in substance, we both shared our beliefs on why the cost of commercial financing remains high.

McCarthy wrote that achieving a transformation, “will depend in part on facilitating greater transparency, accountability, and fairness across our sector, and reining in predatory actors.” He cuts right to the chase by attacking lenders all while ignoring the reality that businesses are regularly preying on financial companies too, especially in the technology age.

It’s an epidemic. There is actually an entire industry association that is dedicated to preventing repeat merchant fraud. Respecting that small business is the backbone of this country though, it probably wouldn’t be appropriate to draft a Lenders’ Bill of Rights, whereby merchants promise not to deceive, lie, or commit fraud against them. Instead the industry deals with it quietly, investing in new risk infrastructure and ultimately passing the costs on to the good borrowers.

Merchants aren’t inherently bad, but neither are the companies that provide them with financial services. Let’s agree that the world is good but that bad actors exist.

McCarthy’s argument for a Small Business Borrowers’ Bill of Rights is premised on the assumption that in every commercial financing transaction, one side is painfully unaware and uneducated about what’s going on around them despite being an owner, president, or CEO of a company.

I think a dose of self-deprecating reflection is healthy and 2014 definitely brought out many discussions about how to increase transparency and better serve small business. But there’s a line between self-improvement and self-loathing that nobody should lose sight of.

It’s okay to make a profit

It’s okay to make a profit

Imagine that the CEO of a widget retailer grossing $2 million a year is looking for a new widget wholesaler to buy product from. The CEO sits down with a prospective wholesaler and asks for a quote. The wholesaler says they have deals with domestic widget manufacturers and Chinese exporters and based upon these relationships and the circumstances they can sell them in bulk at a price of $2 per widget. Unbeknownst to the retailer, the wholesaler quoted a competing retailer a price of only $1.80 per widget earlier that day. But this is business and if the wholesaler can charge more to this company, he will.

Unsure if he should accept the terms, the retailer pulls out a Widget Retailers’ Bill of Rights and demands the wholesaler charge not a penny more than what would adequately compensate the wholesaler for his work in the name of fairness. He also demands to be presented with unbiased facts on costs, benefits, and risks of every widget manufacturer, so that they can compare products on an apples-to-apples basis without pressure. And if they don’t do this, they will get Washington involved.

If you think this is supposed to be silly, it’s not. It’s McCarthy’s worldview applied. What’s missing from this scenario is that the wholesaler has a widget cost basis of about $1 and is selling them for $1.80 to $2.00, a nice margin. The retailer will sell these widgets for $10 a piece in their stores for an even better margin.

Maybe it’s the consumer that ends up getting screwed on price but even that seems unlikely since widgets are selling off the shelves at lightning speed. So what would be fair and adequate compensation for every party involved? What if the manufacturers are producing widgets for 7 cents each? Is there another layer of possible unfairness here?

Everybody has some kind of incentive and that’s how a marketplace works. If the price is too high, customers won’t buy, they’ll negotiate the price down or they’ll shop elsewhere.

In McCarthy’s Bill of Rights, he rejects the very notion of self-interest. “Some lenders charge higher interest rates just because they can,” he writes. This is how capitalism works. Find your customers price point and sell for a profit. Don’t forget we’re talking about commercial transactions only here!

You ever wonder why they’re called deals?

I’m reminded of someone from the peer-to-peer lending world that once asked me why folks refer to merchant cash advances as deals. They’re not loans, they’re not units, they’re deals!

And true to their deal making roots, terms on them are almost always negotiable. Two companies come together to make a deal… get it? Traditional merchant cash advances are also not loans. They’re literally contracts negotiated by businesses to sell future revenues at a discount in return for upfront cash flow. The concept couldn’t be any more commercial.

And over on the lending side, McCarthy might have you believe that the average small business CEO is unsophisticated shark bait in this unfair world so I pulled up the stats on the industry’s most famous small business lender. According to the S-1 filing, 90% of OnDeck Capital’s borrowers gross between $150,000 and $3.2 million a year in revenue and have been in business for an average of 7.5 years. These are bright companies.

Curiously there’s a group of financiers that are unabashedly capitalist. They will charge whatever they can get away with, take half a business if they want and even call their customers shark bait to their faces. Hopefully they clean up their act before Washington steps in! Thankfully the regulators have not yet put an end to ABC’s Shark Tank though I’m sure McCarthy will propose they do so.

That means you too Marcus Lemonis… Rumor has it you do things to make money all while applying high pressure sales tactics on TV to get people to agree and without telling the business owners the unbiased facts about every other financing option in the entire marketplace.

If it’s okay on TV, it has to be okay in real life.

Business on a deeper level

Business on a deeper level

I didn’t mean to take a stab at Brayden McCarthy personally but his message reflected a culmination of emotions that some people feel in this industry when they’re struggling to keep up. They can’t believe that a client would take something more expensive when they had an offer for something less expensive. Almost 7 years ago I competed against another salesman for a client to whom we both made almost the exact same offer; Same advance amount, same holdback %, same closing fees, but a different receivable purchase amount. The ONLY difference was that the other guy’s price was $2,000 more expensive. Everything else was the exact same and he knew it. And you know what happened? He went with the more expensive offer…

I remember confronting that salesman about it a few days later after I had let my anger cool down. A lot of thoughts had gone through my mind, that perhaps the other guy had lied, coerced him, or conducted some kind of shady trick. Why else could this have happened?! It seemed completely illogical. Of course it was none of those things. The other salesman developed a strong rapport with the customer and they spent most of their time talking about football on the phone.

“He freaking loved me,” the salesman said.

“That can’t be it,” I thought. Still hurt and determined to get the truth, I sent the lost prospect a very long email complete with mathematical formulas (I even used exponents, square roots, and fancy squigglies for good measure) to show how much he would’ve been better off with my offer. He responded almost immediately. “You see, this is exactly why I didn’t go with you,” he wrote.

While I was busy trying to open the customer’s eyes to the magic of the Black-Scholes model, the other salesman was talking to him about whether or not Eli Manning was really franchise quarterback material.

Still a very inexperienced salesman at the time, I had learned a new truth. Business went deeper than just prices, market efficiencies, and a desire to make money, it was also about relationships. Treating one side like an uneducated idiot has become a cornerstone of regulations to protect consumers, and perhaps even rightfully so but imagine the widget retailer grossing $2 million a year walks into a business negotiation and is immediately told that he is too dumb and too unaware to not only understand how to assess a deal but to foresee the consequences of his own decisions if he makes a deal.

Transparency is good, relationships are greater. There’s no need to codify sour emotions into an awkward Bill of Rights. Let two businesses make a deal. It doesn’t have to be the smartest, the fairest, or the best, just something both ultimately agree to. I can’t imagine it any other way.

The Industry’s Bad Paper

February 8, 2015 Sometimes deals go bad. But what happens next?

Sometimes deals go bad. But what happens next?

I just finished reading, Bad Paper: Chasing Debt From Wall Street to the Underworld on a recommendation from a friend. In it, author Jake Halpern walks readers through the shadowy world of consumer debt collection. It was eye-opening to say the least.

Halpern’s research uncovered that consumer debts with seemingly no original paperwork is sold, resold, and resold again to companies that the debtor never heard of and would not recognize. A debt’s record amounted to some fields on a spreadsheet where the information is not always correct and might even have been collected already by someone else.

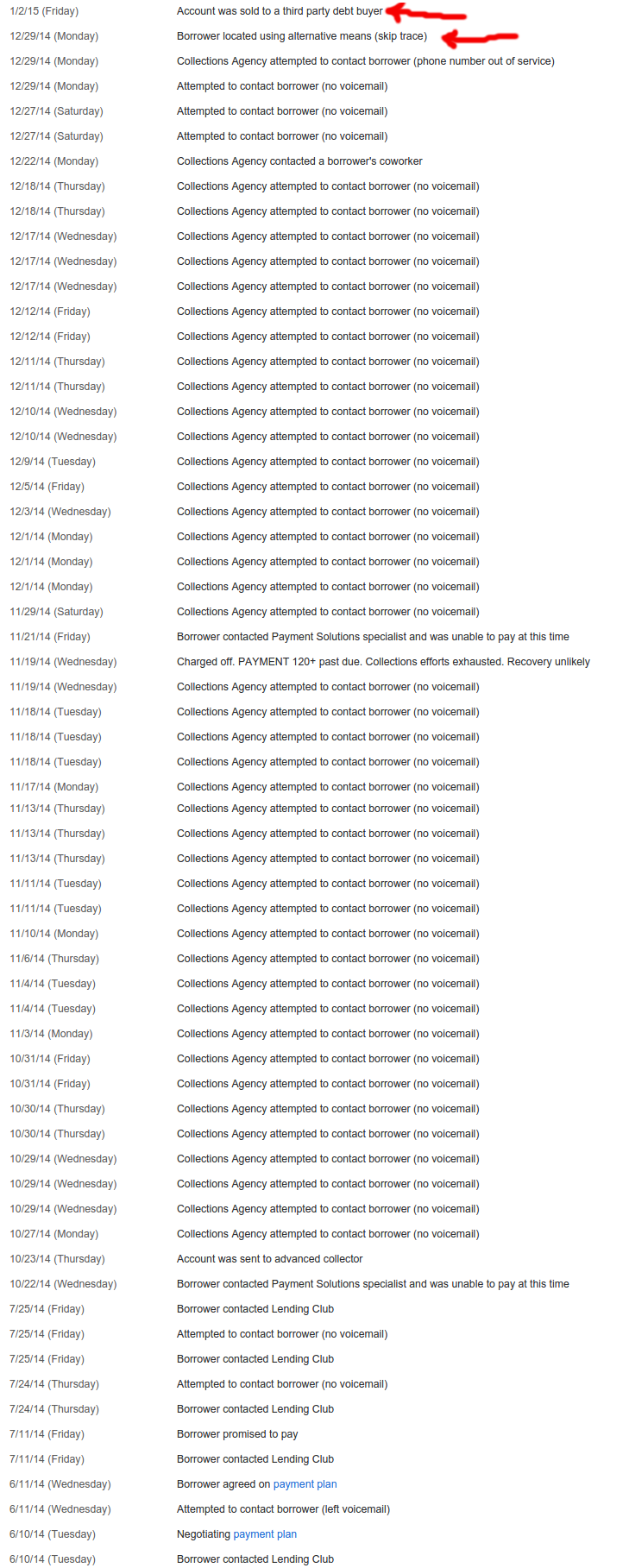

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

I’ve found that a lot of my defaulted loans thus far have gone bad in the first few months, a pattern that looked more like fraud than borrower hardship. It actually prompted me to call Lending Club and speak to a representative about it, who explained that they’re doing all they can to prevent fraud.

They were pretty relentless on this particular file, a nurse that was making $60,000 a year sounded like a winner. They had virtually no debt but the loan was supposedly used to consolidate outstanding debt into one monthly payment at the rate of 9.67%. The story didn’t exactly add up but since I don’t actually get to talk to the borrowers or look at their paperwork, I’m essentially just playing a numbers game.

That debt has been sold off and I as a note holder do not appear to be entitled to any money on the sale of it, not even pennies on the dollar. Bummer.

Because of platforms like Lending Club, I wasn’t the only one to lose out. 277 other retail investors who I don’t know and have never met participated in it with me. We’re all playing the numbers and we lost on this one.

With 1907 notes acquired on the platform so far, I’m not emotionally invested in any of them. How can I be? I have no idea who the borrowers are. I don’t even know their names! All I can do is diversify and make decisions based off of statistical analysis. If the borrower stops paying, go after them hard whoever they are!

Meanwhile in commercial transaction land

When it comes to merchant cash advance and business lending, the collection rules are different but so are the relationships. Even with strong advancements in automation, phone interviews remain an integral part of the underwriting process. A risk analyst typically calls the business owner, their landlord, and even several of their suppliers. Large dollar amount deals may even be presented to an entire risk committee for approval.

Suffice to say, pesky things like signed contracts do not usually prove elusive when a collector in this world gets their hands on it. Many commercial funding providers even record phone calls with the business owners where they get an additional verbal confirmation to the terms and conditions of the arrangement.

The collections process usually begins with the sales person or sales office that negotiated the terms with the business. Back when was I was an account rep, my commissions were paid in two pieces, upfront and a residual. That meant almost half my pay on a deal was tied to its performance. If a deal started to fall apart or defaulted, I had a personal stake in restoring the business to good standing.

The Fair Debt Collection Practices Act does not cover commercial transactions. And in the case of traditional merchant cash advances, there is likely no debt at all in a default, but rather a possible case of stolen receivables.

In the event where a deal I brokered was suspected of diverting receivables, I’d be the first one to know about it and the first person tasked with fixing it. That meant calls to the business, their home phones, their cell phones, and when necessary their landlord. If none worked, then their suppliers. The first goal was to determine if the business was still operating and in the vast majority of cases where defaults happened, they were.

Hardship was sometimes cited as a reason for breaching the agreement but not always. With a chunk of my paycheck on the line, I had to talk them back into good standing and unlike debt collectors, I didn’t have the ability to renegotiate the terms, lower a payment or cut them slack. It was back to the way it was or nothing.

It escalates

Some returned to good standing and others played hardball. The deal’s original underwriter might then involve themselves and if they failed, then on it went to the internal funder’s portfolio management/collections team.

This is why the situation here on out is different: Imagine a doctor sells you the accounts receivable of all his patients for a discounted price. The doctor gets cash upfront and the buyer will hopefully collect the full value of the accounts receivable to earn a profit.

Now imagine the doctor accepts your cash upfront and then also collects the accounts receivable from the patients and shuts you out. In traditional merchant cash advances, collectors aren’t going after debt, but rather acquired property that is rightfully theirs. The business has shut them out of receivables they purchased.

If internal collection efforts fail, they can attempt to freeze various receivables the business might have. Merchant processing proceeds are usually the first stop. If the business accepts credit cards, the merchant processor can be instructed to freeze all or a percentage of the revenues without a court order. This is easier said than done but it does work and there are even a few third party collection firms that specialize in this.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

Some business owners are shocked to learn that a deal they made over the phone with people they never met will actually track them down and sue them. Unlike consumer debts which might only be a few hundred dollars, commercial transactions are typically tens of thousands or hundreds of thousands of dollars. They will definitely pursue it.

On the largest default I ever presided over as an underwriter, the business owner said something to the effect of, “I stole your money. Let’s see how good you are at getting it back.” He said this just 24 hours after we had wired him the money. Ouch!

That happened more than six years ago but it was something I’ll never forget. A quick Google search today reveals that guy is still alive and kicking as he was recently interviewed about his success in amassing a restaurant empire in Florida.

Over the next couple years, I would hear variations of that “I stole your money” line from other businesses, typically on deals larger than $75,000. These were strategic defaults designed to strong-arm the funding company into a settlement or an attempt to simply walk off with the funds altogether. In other words, fraud.

All this does is raise the cost for the next business that conducts themselves honestly. It’s a damn shame.

Merchants prey on Wall Street

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

One experience I had was with the owner of a steakhouse in NYC that flew up from his residence in Brazil to try and close me (as the underwriter) on purchasing roughly $400,000 of his future credit card sales. What he didn’t know is that the night before I checked out the place anonymously by having dinner there with my wife. When the bill came, the server told me they no longer accepted credit cards. The next morning, the owner who spoke only in Portuguese arrived in tow with a translator and a lawyer. They traveled directly from JFK to our office, to which I informed them of the decline. They had stopped accepting credit cards a day too early for their scam on us to work and the restaurant closed two months later.

In another case, a souvenir shop in NYC asked if I would come by to pick up his application and statements in person since we were locally-based. After spending a half hour with the guy at his shop, I returned back to the office only to find out that he gave me doctored bank statements.

And then there’s the owner of a florist that made a career off of robbing merchant cash advance companies. The store, which is close to my hometown, had obtained more than 20 merchant cash advances by late 2008 and defaulted on all of them, netting the business close to $1 million. They hoped to make me victim number 21 but we figured it out in the 11th hour before the funds went out. The business is still there today though I’m unsure if it’s still the same owner.

In 2015, fake documentation is an epidemic. Underwriters in the industry cannot rely on faxed or emailed statements alone. They should be verified through APIs or through direct contact with banks. Many funding providers go a step further and actually request the usernames and passwords to business bank accounts just to be absolutely sure that what they’re seeing is what they’re getting.

But as tech-savvy millenials become the face of American small business, the ante is being upped on fraud. One underwriter told me they saw something even more worrisome, a fake bank website.

The scam is this: Knowing the underwriter is going to request the username and password of the business bank account to verify the statements, the applicant has designed a functional replica of a bank website on a web domain they own, one that looks like the bank name. The unsuspecting underwriter logs in to it and verifies the account data. There’s only one problem, it’s all fake.

While this appears to be an isolated event, it just goes to show that the war on bad paper is entering another phase.

Bad paper

While fraud is a substantial cause of the bad paper in the merchant cash advance and business lending industries, hardship does have its place. It is perhaps fortunate that in the commercial space, the paper isn’t sold off into some convoluted world of debt collection. More than likely the business will be dealing with the actual funding provider the entire way through the collections process, not a debt buyer ten levels down the chain. That’s good and bad for them.

It’s good because the owner will able to discuss matters related to the default with the party directly familiar with the original contract.

It’s bad because any chance that the contract and proof of the agreement will somehow get lost in the shuffle is pretty much nil.

Jake Halpern discovered that debtors can win lawsuits by simply challenging the debt buyer to produce evidence the debt is owed. That might work in the consumer world where debt changes hands ten times. On the commercial side, bad paper is an enduring companion. It may be business-to-business but somehow it’s more personal.

Contrast that with the Lending Club nurse who I know only as Member XXXXXXX. His/her debt is in the wind. I have no idea who they are, nor anything about the 277 other people that invested with me.

Halpern spent 256 pages tracing the path of a debt, the companies that bought it, sold it, stole it, and sued for it. It’s amazing how complex it is.

If he were to do a book on bad paper in merchant cash advance, it would go like this:

The business defaulted, the funding provider tried to collect and then sued. The End.

A Bitcoin Moment

February 1, 2015 I had a moment recently. It was late at night and I was ready to hit the hay.

I had a moment recently. It was late at night and I was ready to hit the hay.

“Oh wait, there’s something I need to get out of the way,” I told myself.

I had kept delaying the purchase of a new printer cord to replace the one I mangled. It was time to end that procrastination now! Even though it was 1 AM, I was sure that it would only take a few minutes to place an online order and I summoned the motivation to go for it.

Addicted to Amazon’s 1-Click ordering feature, I was bummed to discover they didn’t have the cord I needed. With no time to waste, I used Google to find a site that did carry it.

Found one.

Add to shopping cart.

Select payment method.

Ugh…

I didn’t have my credit card number memorized and I looked across the unlit room to see if my wallet lay nearby. It was somewhere in a pile on the coffee table, or maybe it was upstairs, or maybe I left it in my pants pocket. Unsure and too tired, I selected PayPal to speed things up, a service I hadn’t used in a while.

Incorrect password.

Incorrect password.

Ugh…

I entered my email address and completed a captcha.

No email…

Refresh email.

Still nothing.

Refresh email again.

Nothing.

Agitated, I started Googling for help about not receiving a PayPal password reset email and instead ended up on a message board where people griped about PayPal in general.

After perusing that forum like a zombie, I got up and walked around. My wallet wasn’t downstairs or at least I couldn’t find it.

Thirty six minutes had gone by since I first encountered the checkout screen. I stopped caring about the cord and I resolved to never print anything ever again.

Before shutting down the computer for the night, I checked my phone. The only news alert I had was about bitcoin. I laughed out loud and went back to the checkout screen. Bitcoin was a payment option. I selected it, copied and pasted the payment address and sent bitcoins stored on my computer to it.

Order placed.

—–

tl;dr

I needed to buy a cord online. Credit card was out of reach. PayPal password was forgotten. Bitcoin saved Gotham.

What’s up (or down) with OnDeck? [ONDK]

January 29, 2015 OnDeck took the market by storm back on December 17th, achieving a high share price of nearly $29. If 2014 was the breakout year for alternative lending, then early 2015 is feeling a bit like a hangover.

OnDeck took the market by storm back on December 17th, achieving a high share price of nearly $29. If 2014 was the breakout year for alternative lending, then early 2015 is feeling a bit like a hangover.

OnDeck closed at $14.75 today, down almost 50% from its high and well below its IPO price of $20.

With stock analysts mostly bullish about the company’s prospects, retail investors may be wondering why the tide is moving in the other direction.

$ONDK weird stock sold im out..

— BullyBear13 (@BullyBear13) Jan. 22 at 09:59 AM

Q4 Earnings will be announced on February 23rd at 5pm EST. Anyone can listen in to it as the event will be webcast live on the company’s Investor Relations website or can be accessed toll free by dialing (877) 201-0168 for calls within the U.S, or by dialing (647) 788-4901 for international calls, and using conference ID 71535376.

OnDeck sailed into the market on Lending Club’s coattails just as investors were celebrating platform and marketplace lending. Lending Club is down 33% from their high.

The two have largely been lumped in together as disruptive financial technology companies, but as Stern Agee analyst Henry Coffee pointed out, OnDeck “should be considered a high-growth specialty finance lender.”

Perhaps worried that description might stick, OnDeck countered two weeks later with news that their Marketplace Platform would become generally available to institutional investors. While clearly trying to communicate what they want to be known for, investors seem skeptical.

Welp, you can now get in $ONDK under the price Tiger paid to lead the pre-ipo private round // @pkedrosky

— Justin M. Overdorff (@jmover) January 29, 2015

So is a share of OnDeck on the cheap right now? It’s hard to say. Investors seem confused by it all. That might complicate plans for CAN Capital and Prosper who are rumored to be next in line for IPOs.

Given OnDeck’s long history of losses, many will be wondering if they can reproduce the magic of 2014’s Q3, the first time they ever recorded a profit. We’ll find out on February 23rd.

—-

Note: I do not own stock or have a market position in OnDeck or Lending Club