Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Wasted Leads, a Plague in the Business Financing Industry

May 1, 2015Many people don’t know this, but a few years ago I dabbled in online lead generation for business lenders and MCA companies. I did online marketing, captured prospects, qualified them using a very simple algorithm, and then directed them to the appropriate companies for a fee. I don’t do this anymore.

One of the first features I added to boost conversion rates of the recipients was auto-phone connect. It worked like this:

- Prospect fills out a web form with their phone number

- Algorithm qualifies it

- Data is sent to appropriate lender/funder via API or email

- My phone system dials the recipient’s live sales line

- Sales rep picks up

- My phone system then dials the applicant’s phone number and if they answer, they’re immediately connected to the sales rep on the other end

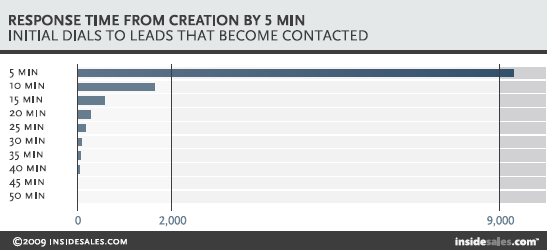

The entire process was fully automated. An applicant could fill out a form and be called with a live sales rep on the other end in literally 3 seconds. Basing the idea on studies performed by experts like Dr. James Oldroyd, who believes the odds of reaching a lead declines exponentially after the first five minutes, I thought my system was pretty damn brilliant.

Not quite. Every single company that tried it hated it. There were problems on all sides. The receiving companies would be too busy on other calls to answer the auto-connects, they’d be out to lunch, or the calls would come after working hours. Some receiving companies felt they didn’t have time to digest the lead they were being auto-connected to since the call was being connected before their CRM or email was even processing the data. That meant right after the merchant had just filled out a web form with all the necessary information, the sales rep being auto-connected to them didn’t have it yet and thus the merchant had to frustratingly state it all again.

Even worse, sales reps would answer the call and wait to be auto-connected to the applying merchant, but many merchants wouldn’t answer the phone on their side even though they had just literally filled out a form seconds ago requesting somebody call them. That meant sales reps were often answering dead calls. Doh!

Technological flaws aside, some of the casual feedback I got was that seasoned sales reps preferred to contact leads at their own pace anyway, with the belief that it improved their closing percentages. Why go into a call completely unprepared in seconds or minutes when you could mentally digest the prospect’s application and possibly do a little research on them online before reaching out?

But Oldroyd’s research would argue that it was better to reach out as soon as possible because waiting a span of mere minutes exponentially increases the likelihood the prospect will not even pick up the phone when you call.

So what was the happy medium or best method? It’s hard to say since I didn’t continue to evolve it or test further. I bowed to the pressure of the lenders and funders, all whom wanted it gone and I disabled the automatic phone connects for good.

Meanwhile in 2015

Meanwhile in 2015

An experiment conducted early this year by FinServ’s Steve Conner found that 100% of sampled business financing brokers/ISOs in the industry waited longer than five minutes to call an inbound web lead. That’s a long enough delay by Oldroyd’s standards to infer that many merchants will no longer be interested by then to even accept the call.

Conner pretended to be a merchant and completed web forms on the websites of 52 brokers and funders in the industry. The fastest broker called in 6 minutes, but the average (for those that actually called) was an astoundingly slow 742 minutes, MORE THAN 12 HOURS LATER! More than half never even called at all. What the heck?!

Back in September I said that lenders will pay as much as $200 for an exclusive inbound lead in this industry. The kicker? Conner’s experiment and Oldroyd’s data say that brokers are waiting until the lead is already pretty much dead by the time they finally attempt to make their first contact.

No wonder costs per acquisition are so high?

The numbers were better for direct funders even though more than half of them never called the prospect at all. For those that did call, the average time to make contact was 17.5 minutes, far better than the average of 12 hours for brokers.

While I do not know specifically which websites were sampled, Conner’s full report (which you can download online) says that they researched the companies beforehand.

One has to wonder what happened to the leads for which nobody called. Were they filtered out and rejected by an algorithm? And if so, shouldn’t the prospect deserve to know?

While receiving a phone call from a sales rep literally seconds after completing a web form may seem creepy or overly ambitious, there’s nothing more disconcerting than complete silence. Where exactly did your information go then?

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

In July 2011, I pretended to be a merchant (much like recently featured loan broker William Ramos did) and filled out a single MCA website form to find out who would call me and what they would say. I still remember the name of the make-believe business I used because I still get called and emailed regularly by that company to see if my delicatessen is ready to get funded. It is now four years later.

“I’m still shopping around,” I tell them.

The periodic emails don’t bother me. Many years ago, they paid for my contact information, possibly as high as $200 for it. They might as well keep trying.

1-call-close or bust

Ken Krogue, the CEO of InsideSales and a Forbes Contributor, discovered after his research that sales reps only make 1.3 call attempts on average to a lead before giving up. He tested over 10,000 companies in fifteen secret shopper studies. “We fill in a lead on their Web site with a real phone number and email address and track how fast they respond and how many calls or emails they make,” he wrote on Forbes.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

35% to 64% of sales leads never get called at all according to Krogue, whose results mimic the numbers Conner experienced in the business financing industry.

In off-the-record conversations I’ve had with a handful of lead generators in this space (companies that are neither brokers or funders), a leading challenge they face with buyers obsessed with costs and closing ratios is that the buyers don’t always end up calling all the leads or they call them once and never call them again.

There’s pressure on lead generators to provide 1-call-close quality leads. If the merchant can’t be closed on the first call, some reps are just throwing them in the trash, never to be remarketed to ever again.

“Spoiled,” was the word used by one industry veteran to describe the newer generation of sales reps who have walked into an industry growing by leaps and bounds. So many leads are coming in, that they don’t even know what to do with them all.

Research argues however they should be calling them inside of five minutes and of course following up. And there’s no reason that so many are never called at all.

One issue Conner discovered in his experiment is that several companies in this industry had broken websites. The HTML or javascript wasn’t set up right and the forms couldn’t even be submitted. :::face palm:::

A lot of money might be pouring into this industry, but a lot of money may also be getting flushed down the tubes.

Do you know your Web form-to-call response times? You should…

Letter From the Editor – May/June 2015

May 1, 2015 Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

Alternative lending is full of bubbles. I’m referring to the inefficient exchange of information, not runaway valuations, though that’s something to explore in a future issue.

New financial products can be just as intimidating to the professionals working within the wider industry as they are to the customers they’re being offered to. I’ve blogged often of my experience investing in Lending Club and Prosper notes, something I assumed everyone in the business finance world could relate to. Alas, I find that usually raises more questions with readers than it does answers.

Are you just nodding your head and smiling when your peers talk about their alternative lending portfolios? There’s no better way to understand today’s loan marketplaces than being an investor in them, even if it’s just a small amount. Whether it’s merchant cash advances, real estate loans, student loans, or credit card debt, there are plenty of opportunities and worlds to explore. You should conduct research, diversify, and be smart of course. You don’t want to be trapped in a bubble.

Outside the knowledge bubbles, we have regional enclaves. There are entire city neighborhoods being overrun by small business financing startups. In New York City, it had long been Midtown, but some shops started moving south and before anyone realized what was happening, Wall Street had been overrun by a new breed of broker. The culture in lower Manhattan is different than you might find in Midtown or in the next two largest industry hubs, Miami and San Francisco.

In this issue, we’ll begin to explore the industry’s bubbles, both geographically and structurally.

–Sean Murray

Defraud Merchant Cash Advance Companies, Go to Jail

April 27, 2015 We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

We once dubbed the summer of 2013, the summer of fraud, after merchants began exploiting alternative lenders at record levels. Well it looks like in at least one instance, there were consequences.

Just two months ago, the Essex District Attorney’s office in Massachusetts announced that, “six people were arraigned in Haverhill District Court on numerous counts of larceny, money laundering and fraud following a three-month investigation involving local, state and federal authorities into a false invoice scheme.”

But invoice factoring wasn’t the only thing on the crew’s hit list. Sources and research revealed that among the victims were at least five merchant cash advance companies, the names of whom we won’t mention.

At least one funding company’s UCC was filed two weeks after the defendants had been arrested, alluding to the possibility that they had obtained one last merchant cash advance in the days prior.

The Salem News reported that the group is alleged to have netted at least $700,000 over a five year period.

47-year old Susan Yerdon was fingered as the mastermind and was sentenced to three and a half to six years in state prison.

According to The Salem News, “she pleaded guilty to money laundering and other charges, will be required, in exchange for her sentence, to testify against some of her codefendants.”

“Police seized a Mercedes Benz E Class AMG, a GMC Yukon Denali, a BMW 328i, a Cadillac DTS, and a Pontiac Solstice.”

Rand Paul Speaks at Bitcoin Event

April 20, 2015 Yesterday, Senator Rand Paul spoke at a private Bitcoin event produced by Blockchain Technologies Corp in Midtown Manhattan. It was a gathering of monetary technophiles dressed in their Sunday best.

Yesterday, Senator Rand Paul spoke at a private Bitcoin event produced by Blockchain Technologies Corp in Midtown Manhattan. It was a gathering of monetary technophiles dressed in their Sunday best.

Paul’s main reason for supporting the Bitcoin movement/technology/currency was the ability to bypass the expensive fees tacked on by credit and debit card issuers. A business that only had a 3 or 4% profit margin could double its profits by eliminating merchant processing fees, he said.

The event lasted for about two hours with Paul only making an appearance for about 15 to 20 minutes.

Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

Is NAMAA Reborn? Meet the Small Business Finance Association

April 14, 2015Almost seven years ago exactly, the North American Merchant Advance Association announced their presence. As of today, they are now officially the Small Business Finance Association (SBFA). Back then, a release dated April 15, 2008 stated:

The North American Merchant Advance Association, Inc. (NAMAA) has recently been created to represent merchant cash advance providers and to promote competition and efficiency throughout the merchant advance industry. NAMAA’s members will have the opportunity to share industry education and professional development, ethical standards and best practices guidelines, the development of industry relevant products and services, and the engagement in regulatory and legislative advocacy.

Of the ten original members, a handful are no longer operating. NAMAA’s membership in 2008 arguably encompassed the entirety of the merchant cash advance industry sans AdvanceMe (now named CAN Capital). Today, the SBFA website currently lists seventeen members. The organization has clearly grown but it pales in comparison to the size of the industry in 2015.

Internal data indicates that there are well over one hundred direct providers of merchant cash advance. Several hundred more are ISOs/brokers that co-invest in merchant cash advance transactions (Strategic Funding Source has had more than 200). And there are more than one thousand ISO/brokers that resell the product nationwide.

On this basis alone, less than two percent of industry providers and resellers are members of the trade organization. Granted, the seventeen member companies likely make up at least 15% of the industry’s funding volume. Member company Merchant Cash and Capital for example, announced just last month that they had funded $1 billion since inception.

Some have viewed the organization’s membership as overly exclusive and resistant to change. A seasoned veteran of an ISO that wished to remain anonymous said prior to the organization’s announced changes that, “NAMAA served a purpose for a long time but as the industry has changed, they have not.”

Ironically, Goldin’s statement in today’s release couldn’t be any more well timed. “With the alternative financing industry growing exponentially into a multi-billion dollar industry, we felt it was time for the trade association to evolve with it and open itself up to all types of small business alternative financing providers hence the name change to Small Business Finance Association,” he said.

The shift clearly acknowledges the true dynamic of the industry’s growth, that it’s not all merchant cash advance anymore.

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

But with lenders added to the mix of potential constitutents, is the SBFA a little light? The SBFA will now represent less than 1% of the companies selling or reselling merchant cash advances and business loans. In growing membership however, patience may perhaps be a virtue.

Jared Weitz, CEO of United Capital Source, said, “NAMAA is a beneficial association in the industry and should be choosy with who they let in.” As a broker, his company has historically not been eligible for membership.

Similarly, Chad Otar, Managing Partner of Excel Capital Management, whose company has also not been historically eligible for membership, said, “The aim of NAMAA is to help out our audience to understand and remember the information we stand for as funders and ISOs.”

Otar’s point belies a troubling trend, that many players in this industry disagree about what it is they stand for.

In a deBanked Magazine article, titled, Stacking: Is it Tortious Interference?, Robert Cook, Cathy Brennan, and Kate Fisher of Hudson Cook, LLP delved into the industry’s most polarizing debate, the practice of entering into a cash advance transaction or loan knowing that the merchant has one or more open cash advances or loans with a competitor. They wrote:

On one side are companies that only originate first-position deals. These companies generally include a clause in their contracts prohibiting the merchant from obtaining another merchant cash advance or loan until the company receives all of the future receivables it has purchased or is fully repaid. First-position companies view stacking as a threat to recovery of money advanced or loaned to merchants. On the other side are companies that routinely offer second or third-position deals. These companies argue that merchants with adequate cash flow to support additional advances should be free to obtain them.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Lawyers at Hudson Cook, LLP echoed the same. “In the last several months, at least two first position companies have sued their stacking competitors, claiming that stacking constitutes tortious interference with contractual relations,” they wrote.

The lawsuits come on the heels of the International Factoring Association (IFA) ban on merchant cash advance companies, citing tortious interference as the main driver.

After meeting with board members from both associations, the decision was made to deny membership to merchant cash advance businesses. This decision was based on numerous complaints and increased scrutiny that could negatively impact the factoring industry. By distancing ourselves from the merchant cash advance industry, we hope to diminish the chance of potential legislation.

-Commercial Factor July/August 2014

With several merchant cash advance companies left high and dry by the IFA, a potential leadership void has been created.

“As every industry evolves and shapes itself, some sort of governance and guidance is always needed,” said Otar. “This guidance is something that NAMAA holds itself responsible for,” he argued.

“The question is, can they reestablish themselves as a powerful voice that demands respect?” asked an industry veteran on the condition of anonymity.

Goldin assured me that the updated version of the organization’s best practices guide will be a public document.

Industry brokers like Otar are eager to comply with an established code of conduct and play any role they can in its creation. “Most of the business driven industry-wide is brought in through various ISO channels, which are the ones responsible in presenting the product offered by the funders to the end client,” he said.

That enthusiasm may be resonating with the SBFA. Goldin communicated that they are working towards different types of memberships, hinting at the possibility that brokers might one day be extended an invitation to join.

“We are exploring different levels of membership / pricing,” Goldin wrote in an email.

For the right price, they will likely find a lot of eager applicants.

A Q&A With LendingRobot

April 12, 2015 SEAN MURRAY (SM): I’m a casual Lending Club investor that has purchased more than 2,000 notes. I like to think that I’ve been pretty good with my picks but I feel like the rush to get the most attractive notes has only gotten more competitive. I’ve also got a perennial issue of idle cash and the pressure to put it to work on the platform can feel like a burden when I’m busy with everyday life. I feel like I can do better but I have reservations about relinquishing control.

SEAN MURRAY (SM): I’m a casual Lending Club investor that has purchased more than 2,000 notes. I like to think that I’ve been pretty good with my picks but I feel like the rush to get the most attractive notes has only gotten more competitive. I’ve also got a perennial issue of idle cash and the pressure to put it to work on the platform can feel like a burden when I’m busy with everyday life. I feel like I can do better but I have reservations about relinquishing control.

I noticed in January that you raised $3 million from Runa Capital, which caught my attention.

So for both myself and our readers, can you explain in a nutshell what LendingRobot does?

EMMANUEL MAROT (EM): First off, that ‘burden’ is the exact reason why we started LendingRobot, as my partner and I were feeling it as well! We automate the whole investing process (decision and execution) to simplify access to marketplace lending for individual investors.

EMMANUEL MAROT (EM): First off, that ‘burden’ is the exact reason why we started LendingRobot, as my partner and I were feeling it as well! We automate the whole investing process (decision and execution) to simplify access to marketplace lending for individual investors.

(SM): I think one of the biggest concerns for casual investors is the question of who physically possesses the cash. Obviously they have already come to accept that Prosper or Lending Club will hold their cash, but what about a service like yours? Do investors send you the money to invest it on those platforms?

(EM): That’s a very valid point. As of today, we do not have what the regulator calls ‘custody’ of the money. Our clients wire the money on the platform, they give us a programmatic access to their account there so we manage it for them. There is no way we can touch their money, and when the money is wired outside of the platform, it has to go back to the original bank account anyhow.

(SM): How do you bill for your fees? Do you need to provide bank account information? Credit card?

(EM): Since we cannot touch our client’s money, we need another way to charge our fees. We use credit card. Up to $10,000 we do not charge anything and clients don’t even have to enter a credit card.

(SM): What is the difference between your service and Lending Club’s Automated Investing?

(EM): As the issuer of the notes, Lending Club cannot offer an ‘unfair’ advantage to some investors, therefore their automated investing cannot be used to get access to the most popular assets. Obviously, it’s also entirely based on their own credit model, and one cannot benefit from a second layer of risk modeling. At last, we tend to offer more features, such as additional filtering criteria, cascading investment rules or cash-flow forecast. We posted a comparative explanation a while ago that is still somewhat valid: http://blog.lendingrobot.com/post/69219879518/lendingclub-re-introduces-prime

(SM): If I use your service, can I cancel it at any time?

(EM): Absolutely, no setup or entry fees, no exit fees, no minimum usage period.

(SM): There seems to be correlation between a borrower’s home state and the default rate, can I filter out certain states with your service?

(EM): Yes, not only do we offer over 25 different filtering criteria, but it’s possible to mix them freely. Some clients start with our own proprietary model, then add extra criteria, such as ‘36-months’, or ‘Exclude Nevada’.

(SM): What did you guys do before founding LendingRobot?

(EM): Tons of stuff! My partner and I met at Microsoft, which we both joined after selling our respective startups. We decided to create something together even before knowing what to do. Incidentally, we started the company with a very different project (see http://www.eventiles.com/). As mentioned above, we started LendingRobot out of personal need.

(SM): What’s the smallest amount someone can allow LendingRobot to manage if they just wanted to try it out?

(EM): Right now, our smallest client has… $66.49 invested! That being said, we recommend people to invest at least $5,000 to be diversified enough.

Background on Emmanuel Marot

Emmanuel Marot is a polymath and serial entrepreneur. A French ‘grandes école’ graduate with a major in Computational Finance, Emmanuel started his career in product marketing at Apple. He also worked for the French intelligence agency to modernize the handling and presentation of highly classified information and acted as freelance graphic designer.

At age 26, he created his first company, a Web agency that he grew up to 15 people while keeping the net operating margin above 30%. The company created the first virtual reality cd-rom (Guinness book of records, 1995) and produced mobile Internet services as early as 1996. After selling it, he co-founded a larger communication agency, with 400 employees and an annual turnover of 30 million Euro. In 2000, Emmanuel patented a novel way to access mobile sites and created his 3rd company, which Microsoft acquired six years later. Emmanuel orchestrated the move of the entire operations to Redmond, WA, and became Director, Mobile Search at Microsoft.

He left in 2008 to research algorithmic trading, predicting market reversals from search engine queries. In parallel, Emmanuel did multiple executive consulting engagements for startups and corporations. He began to focus his work on the design of algorithms to automate decisions, and co-created Eventiles, an iPhone application that crafts meaningful stories from bulk pictures.

In 2013, he combined his interests in finance and algorithms and co-created LendingRobot, a solution for marketplace lenders to automate and optimize their investments. Emmanuel passed the Series 65 Investment Adviser law exam in January 2014.

From Lowes to Loans: Meet William Ramos

April 12, 2015Non-bank financing changed William Ramos’ life. Not as a borrower, but as a mover and shaker in the competitive world of financial deal-making. As an ambitious 20-year old, Ramos was working at both Lowes and ShopRite to try and put himself through Staten Island Community College. These were stepping stones, he told himself. He was dedicated to bettering himself, or more aptly to be the best at whatever he did.

Already on a path to success, he found himself growing impatient. The life of two jobs and school was a slow grind. Ramos wanted to do something big. He wasn’t sure what it would be, but he was confident that his attitude combined with his strong work ethic would eventually lead him to great success.

And so one day, he made a promise to himself to go out and find that big thing rather than wait for it to find him. It’s a bit of an American Cliché to say that his lucky break coincided with a sudden bout of adversity, but that’s exactly how it played out. Raised in the tough neighborhood of Brownsville in eastern Brooklyn, he didn’t have the connections to step right into the business world. Instead, Ramos had to start his search on the ground floor with millions of others on Craigslist.

His luck began with an interview for a job in telemarketing, a role that meant being connected to an autodialer nine hours a day as an opener. Undeterred by the challenge, Ramos had a feeling that this is where it would all begin. “I’ll do it,” he said.

There was only one problem, they didn’t want to hire him. The firm, which sold mostly financing products to small business owners, was very selective, even with cold callers. His interviewer at the time, who later became his boss, confirmed to me that he didn’t think Ramos was the right fit after they first met. But Ramos was determined to change his mind.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

After calling the firm repeatedly over the next week to convince them that he was up to the task, they finally acquiesced. It didn’t mean he was in. It just meant it was time to put up or shut up. “They gave me a three-day trial period,” Ramos said.

His former boss confirmed this relentless persistence.

39 working hours, 3,000 calls, and 3 days later, Ramos brought in two deals, one for $100,000 and another for $35,000. They both went through.

It was more than good enough to survive the trial and he was offered a job to work full time.

With a starting compensation of only $250 a week + commission, he still had a long way to go. “I would be the first one in and last one out,” Ramos shared with me. “I kept my head down and I wouldn’t leave my seat unless I needed to use the bathroom or eat. All I would do is make my calls.”

His former boss explained to me that Ramos had a knack for bringing in the firm’s larger deals even from the very beginning. He was too junior early on to be making a lot of money, but they were very focused on developing his skills. The firm saw his potential and was committed to nurturing him.

Within the first three months he managed to save $700 and he used it to buy a Mercedes-Benz C240 from a co-worker. After a life of taking the bus to work, Ramos had reached his first milestone of success.

While it was obvious that he still harbors pride in that first car, it sadly became all that stood in the way of homelessness. He had sacrificed everything for this job including college. Unfortunately there would be just one more thing to lose.

Adversity struck when a series of unfortunate events suddenly left him without a place to live. Ramos’ car was now both his ride and his home, though with the long hours he was putting in at the office, he might as well of lived at his desk. His boss took a special interest in his life and soon discovered just how much his young protégé was struggling.

“He was literally sleeping in his car,” his former boss told me. “I offered to let him sleep on my couch or at the very least let him stay in the office,” he added. Ramos took him up on the latter and began sleeping at the office. At the same time his commission percentage was bumped up, which sweetened the potential and only encouraged him to keep going.

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Always looking for an edge, he sometimes pretended to be a customer himself. “I would call up lenders as a merchant to hear what pitches their sales teams were using,” he said. “I would then take that pitch, tweak it and make it my own.”

Soon he was regularly closing more than $500,000 a month in deal flow and his financial situation and lifestyle began to improve significantly. A little more than a year later, Ramos had risen up to become a sales manager and was overseeing a team of five members.

Now some people in his shoes might’ve decided not to press their luck. He had taken a major gamble and it had paid off, so why do anything to jeopardize it?

But Ramos didn’t leave everything behind to settle for pretty good and a middle class lifestyle. After two years, he gave his boss and mentor some bad news.

“I’m going off on my own,” he explained. They parted on amicable terms and to this day still do business with each other. Ramos’ last commission check there was for $15,000, an amount he had never imagined back in his Lowes days.

In 2013 he founded Supreme Capital Group, a firm that primarily brokers merchant cash advances but will fund A paper deals on its own. With only two years in business, they are already on pace to generate more than $1.5 million in revenue over the next 12 months. He excitedly recalled a recent deal that generated $66,000 in commission. And that was just one deal!

He attributes part of his success to strong organizational skills. “I don’t think brokers realize how important keeping track of all their data is,” he said. He went on to explain that he can email the list of all his old leads and turn that into six to ten closed deals easily. He doesn’t have to work as much as he used to, but he still does.

With 10 callers working for him now, he’s not content with just being the boss. “I am still currently pounding the phones, doing email marketing, and sending out mailers,” he said. “We use the mailers to follow up with merchants, and we get a great response from it,” he added.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

After working incredibly hard for several years, Ramos has at least found the time to play hard too. In the summer of 2014, he had made enough money to buy a white Maserati GranTurismo MC Sport Line, of which he shared several photos with me. He’s since upgraded to a 2013 Ferrari California in a color he described as Pepsi blue. And while that might be the kind of car some people would dream of sleeping in, Ramos has said those days are long over.

He just bought a house in Mesa, Arizona where his fiancée grew up and he plans to relocate his office there. “It’s already in the process of being built,” he said.

Ramos is now just 25 years old. He said he regrets not finishing school and he plans to go back. But he wouldn’t change everything that happened to him. He stressed more than once that asking questions is something he considers to be very important to success, especially in the business he’s in. “For all the newcomers in the industry, my advice would be to work hard and ask a lot of questions,” he said.

He was certain he had found the right opportunity almost from the beginning. “I knew that if I made those commissions the first week that I could make more,” he said.

It wasn’t easy.

William Ramos is the President of Staten Island, New York-based Supreme Capital Group.