Articles by deBanked Staff

Long Island Business Loan Brokers Arrested in Bust

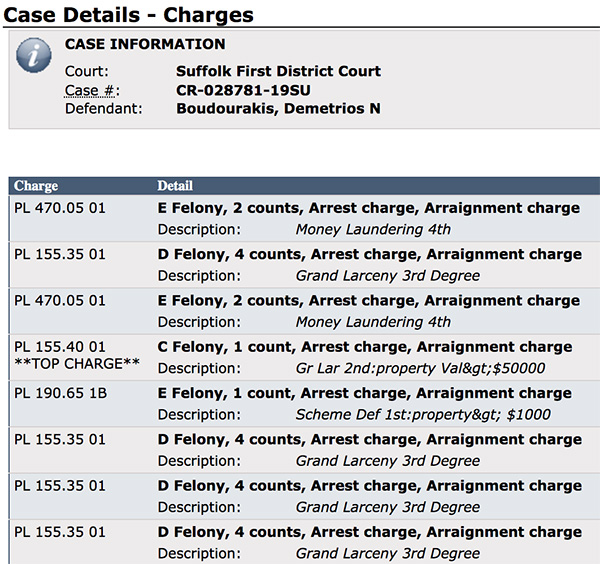

June 13, 2019 The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

According to Newsday, “Boudourakis and his associates, through the dark web, obtained the names of people who had been denied loans. They would then call those people to tell them they had qualified for loans but would have to pay interest and fees upfront.”

According to Long Island Business News, law enforcement agents who executed search warrants at several locations recovered electronic equipment, three handguns, a sawed-off shotgun and a pill press. The investigation leading up to the bust included court-authorized eavesdropping and audits of financial records and physical and electronic surveillance.

Previously, deBanked reported that JTT Funding, Boudourakis’ company, had been accused of forging a Confession of Judgment and impersonating rival companies. Those were civil cases, not criminal cases. Court records show that those cases remain ongoing.

Among the company names the ring used in the alleged scheme were Federal Business Lenders, Federal Business Funding, JTT Funding, JTT Global Holdings, Inc. Blackrock Funders, Inc. and Blackrock, Inc. It is possible that some of those names closely resemble names of competitors and the actual companies have not been accused of any wrongdoing.

Boudourakis is a retired MMA fighter. His nickname in the ring was “The Tyrant.”

Senator Elizabeth Warren Questions Federal Agencies About Discrimination in Fintech Lending

June 12, 2019 Senator Elizabeth Warren and colleague Senator Doug Jones (D-AL) addressed a letter to multiple federal agencies this week to inquire about their individual roles in overseeing fintech, particularly as it pertains to potential discriminatory underwriting.

Senator Elizabeth Warren and colleague Senator Doug Jones (D-AL) addressed a letter to multiple federal agencies this week to inquire about their individual roles in overseeing fintech, particularly as it pertains to potential discriminatory underwriting.

The senators cited a UC Berkeley study that examined discrimination in the era of algorithmic underwriting. “With algorithmic credit scoring,” the researchers write, “the nature of discrimination changes from being primarily concerned with human biases – racism and in-group/out-group bias – to being primarily concerned with illegitimate applications of statistical discrimination. Even if agents performing statistical discrimination have no animus against minority groups, they can induce disparate impact by their use of Big Data variables.”

The letter tasked the Federal Reserve Chairman, OCC Comptroller, CFPB Director, and FDIC Chairman with responding to 5 questions by June 24th. They are:

1. What is your agency doing to identify and combat lending discrimination by lenders who use algorithms for underwriting?

2. What is the responsibility of your agency with regards to overseeing and enforcing fair lending laws? To what extent do these responsibilities extend to the fintech industry or the use of fintech algorithms by traditional lenders?

3. Has your agency conducted any analyses of the impact of fintech companies or use of fintech algorithms on minority borrowers, including differences in credit availability and pricing? If so, what have these analyses concluded? If not, does your agency plan to conduct these analyses in the future?

4. Has your agency identified any unique challenges to oversight and enforcement of fair lending laws posed by the fintech industry? If so, how are you addressing these challenges?

5. Has your agency identified increased cases of lending discrimination in financial institutions that participate in the fintech industry? Are there additional statutory authorities that would help your agency enforce fair lending laws or protect minority borrowers from discrimination in their interactions with the fintech industry?

Do You Need a Mentor?

June 11, 2019 “You don’t need a f-ing mentor,” is the opening line of a short online video delivered to camera by Gary Vaynerchuk, the celebrated high energy marketing and sales guru. In the video, he concludes by saying: “Enough with the mentor horseshit. Go f-ing execute. There’s unlimited free mentors on f-ing YouTube. Go f-ing work.”

“You don’t need a f-ing mentor,” is the opening line of a short online video delivered to camera by Gary Vaynerchuk, the celebrated high energy marketing and sales guru. In the video, he concludes by saying: “Enough with the mentor horseshit. Go f-ing execute. There’s unlimited free mentors on f-ing YouTube. Go f-ing work.”

A discussion with industry insiders suggests that Vaynerchuk’s sentiment is somewhat controversial.

“Without mentorships, I wouldn’t be able to be where I am now,” said Josh Feinberg, co-founder of New Hampshire-based Everlasting Capital, a brokerage that has twice made it onto the Inc. 500/5000 list of the fastest growing U.S. companies, ranked #323 in 2017.

“Mentorship doesn’t just mean asking people for advice,” Feinberg said. “It means being able to build relationships with people who are on a greater level.”

For instance, Feinberg said that he and co-founder of BFS Capital, Cathy Bass, would speak about how she and others grew BFS, how they go to market and what is most important to them.

“And I was able to implement some of that into my own company,” Feinberg said.

Joe Cohen, who runs Business Finance Advance, a brokerage in Brooklyn, said he has mentored dozens of people, mostly his employees, throughout his career.

“You have to instill a solid work ethic,” Cohen said. “And you have to lead by example. Not by dictating, ‘You do this.’”

As for Vaynerchuk’s assertion that there are “unlimited free mentors on YouTube,” David Korchak, Managing Member of Primary Capital, a funder in Brooklyn, makes a clear distinction between a social media celebrity and a mentor.

“I don’t understand how anyone can say they have a mentor in someone with two million followers on Instagram,” Korchak said. “What did this person do for you? Maybe he helped you get to the gym in the morning…but that’s inspiration, that’s not mentorship. That’s the difference between someone posting a video on Instagram and someone sitting down with you at a desk and showing you ‘This is where you made a mistake. This is how you can make sure you don’t do that again, and this is how you can make it better for the future.’ That’s not inspiration, that’s guidance. And a mentor is a guide for you.”

“I don’t understand how anyone can say they have a mentor in someone with two million followers on Instagram,” Korchak said. “What did this person do for you? Maybe he helped you get to the gym in the morning…but that’s inspiration, that’s not mentorship. That’s the difference between someone posting a video on Instagram and someone sitting down with you at a desk and showing you ‘This is where you made a mistake. This is how you can make sure you don’t do that again, and this is how you can make it better for the future.’ That’s not inspiration, that’s guidance. And a mentor is a guide for you.”

But Chad Otar, a veteran MCA broker in New York, said that he agrees with what Vaynerchuk was trying to communicate in his video

“You can have a mentor,” Otar said. “But at the end of the day, you have to put your blood, sweat and grit into it. A mentor can only do so much.”

When asked if Otar has a mentor, he said it’s his brother, who introduced him to the MCA industry. This leads to the question of who can or ought to be one’s mentor?

“A mentor can be anyone in the industry who’s been there before,” Cohen said. “Someone who can tell you what’s going to happen if you do this and what’s going to happen if you do that.”

Cohen said that when he started out in sales years ago, his mentors were older colleagues of his on the sales floor.

“I saw in them commitment to the job and how they worked diligently to make every deal happen,” Cohen said. “They never gave up.”

Some ISO owners even pay to train their managers to be excellent mentors to their salespeople, like Edward Deangelis, founder of the fast-growing Pennsylvania-based brokerage, Amerifi.

Deangelis said that he has used Sandler Training for the last seven years, both for himself and his team. His managers go to Sandler Training’s management boot camps once or twice a month for 3 to 4 hours.

“They learn skill sets on how to be an excellent sales manager,” Deangelis said. “How to cultivate your team rather than just be a boss. And to really ask [their] salespeople what they’re struggling with.”

Deangelis also has a CEO coach that comes to the office once a month for him. He said that the coaching has helped him in many ways, including in his personal life.

Feinberg said that you really have to choose your mentors carefully because a lot of people can talk themselves up into being something they’re not. And he said that one person in the business who said he would guide Feinberg in the right direction ended up stealing his deals by the end of the relationship.

“Look at media exposure,” Feinberg suggested. “If they seem big but you can’t find them in the news or you haven’t seen proof, it’s probably not someone to take advice from.”

Prospa, An Online Business Lender, Goes Public In Australia

June 10, 2019 Another online small business lender has gone public. This time it’s Australia-based Prospa, a company founded in Sydney in 2012. Prospa offers daily and weekly payment business loans with terms from 3-24 months and competes with companies like OnDeck and Capify.

Another online small business lender has gone public. This time it’s Australia-based Prospa, a company founded in Sydney in 2012. Prospa offers daily and weekly payment business loans with terms from 3-24 months and competes with companies like OnDeck and Capify.

Earlier this year Prospa surpassed $1 billion in loans funded to 19,000 small businesses. In a 2015 interview with deBanked, cofounder Beau Bertoli said, “The market in Australia has been very ripe for alternative finance. We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

Prospa was slated to go public on the Australian Securities Exchange last June but it was cancelled in dramatic fashion 15 minutes before being listed as rumors swirled that the Australian Securities and Investments Commission (ASIC) had questions about their business practices. By September, Prospa agreed to revise its loan disclosures to be more fair. Those revisions were published by ASIC.

Prospa’s IPO raised AUS $110 million and was valued at AUS $610 million. The share price jumped nearly 20% in early trading on Tuesday.

SEC Seeks Partial Summary Judgment Against Ruderman in 1 Global Capital Case

June 10, 2019The SEC filed a motion for summary judgment against defendant Carl Ruderman last week as part of its ongoing lawsuit against 1 Global Capital and related parties. The motion applies to Ruderman on Count 1 of the SEC’s amended complaint alleging violations of 5(a) and (c) of the Securities Act of 1933 in addition to summary judgment on Ruderman’s second affirmative defense alleging the instruments he and Defendant 1 Global Capital LLC sold were not securities.

Ruderman has until June 18th to file his opposition to the motion.

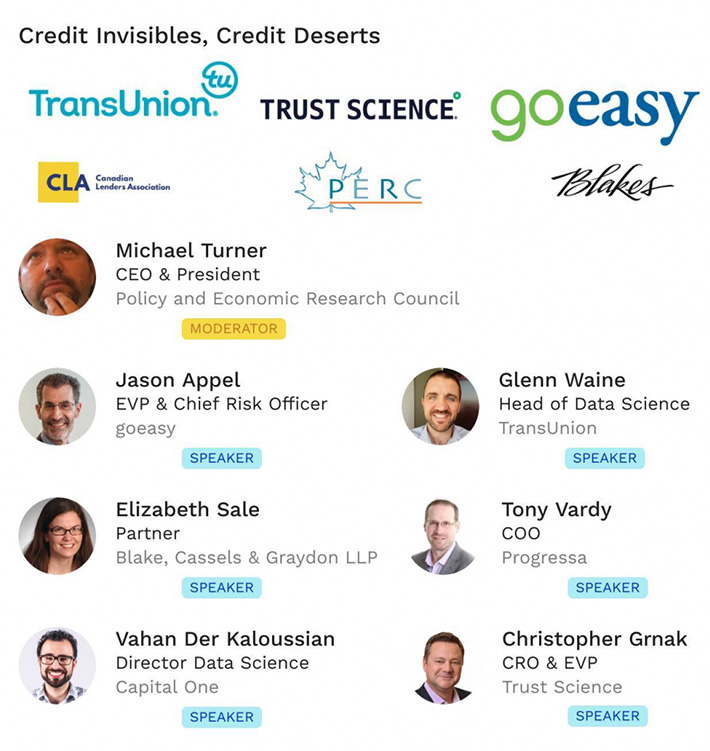

CLA’s Credit Invisibles Event Kicks Off

June 5, 2019The Canadian Lenders Association event kicks off today in Toronto. Hosted by Perc Canada and TransUnion at Blake, Cassels & Graydon LLP, this is the second in the series on “Credit Invisibles” and “Credit Deserts.”

The CLA’s purpose is to support the growth of companies that are in the business of lending, or providing other means of credit, to small business and individuals by non-conventional or innovative means to exchange ideas and explore ways of improving the sector; encourage principled and professional practices by Innovative Lenders; educate the public at large about Innovative Lending; encourage individual potential borrowers to be informed about the appropriateness of Innovative Lending to the borrowers’ circumstance; and to advocate on behalf of, and represent the interests of Innovative Lenders.

deBanked president Sean Murray will be in attendance.

One New York COJ Bill Moves Forward

June 5, 2019A bill that would prevent companies from using Confessions of Judgment against out-of-state debtors is progressing through the New York Assembly. A07500 cleared the judiciary committee on Tuesday despite some Republican opposition. The milestone comes as no surprise as the judiciary committee chair, Assemblymember Jeffrey Dinowitz, is also the bill’s sponsor.

Assemblymembers Niou, DenDekker, Wright, Wallace, and Schimminger are bill co-sponsors.

A07500 now heads to the Codes committee.

IOU Originates $32.8M in Loans in Q1

May 30, 2019IOU Financial funded $32.8M in loans in the first quarter of 2019, according to publicly filed financial statements. The company also continued its profitable streak and plans to grow originations by:

- Identifying, recruiting and partnering with business loan brokers;

- Forming new strategic partnerships with entities such as banks and small business suppliers and leveraging their relationships with small businesses to add new customers;

- Expanding its product offering to allow it to serve small businesses whose needs are not met by its current products;

- Investing in direct marketing and sales; and

- Continuing its expansion into Canada.