Articles by deBanked Staff

Trump’s Two-For-One Regulation Deal

January 31, 2017Trump’s newest order is that for every new regulation proposed, two must be identified for repeal. If a new regulation goes into effect, the costs must be offset by the repealed regulations. The idea behind it is to strip away costs on small businesses and unburden the system. “There will be regulation, there will be control, but it will be normalized control where you can open your business and expand your business very easily,” Trump said prior to signing the executive order. Watch that below:

Trump later said that “Dodd-Frank is a disaster” and that “We’re going to be doing a big number on Dodd-Frank.”

When he does that “big number,” he should pay close attention to Section 1071 of the law, which many believe the CFPB will try to use to police commercial finance and business-to-business transactions.

Ironically, as Trump works to slash federal rules, states will likely be doing just the opposite. Already in New York, Governor Cuomo’s 309-page budget proposal includes edits to an existing law that would impose strict regulations on all non-bank business finance.

Biz2Credit – Citigroup Small Business Loan Partnership Spotted

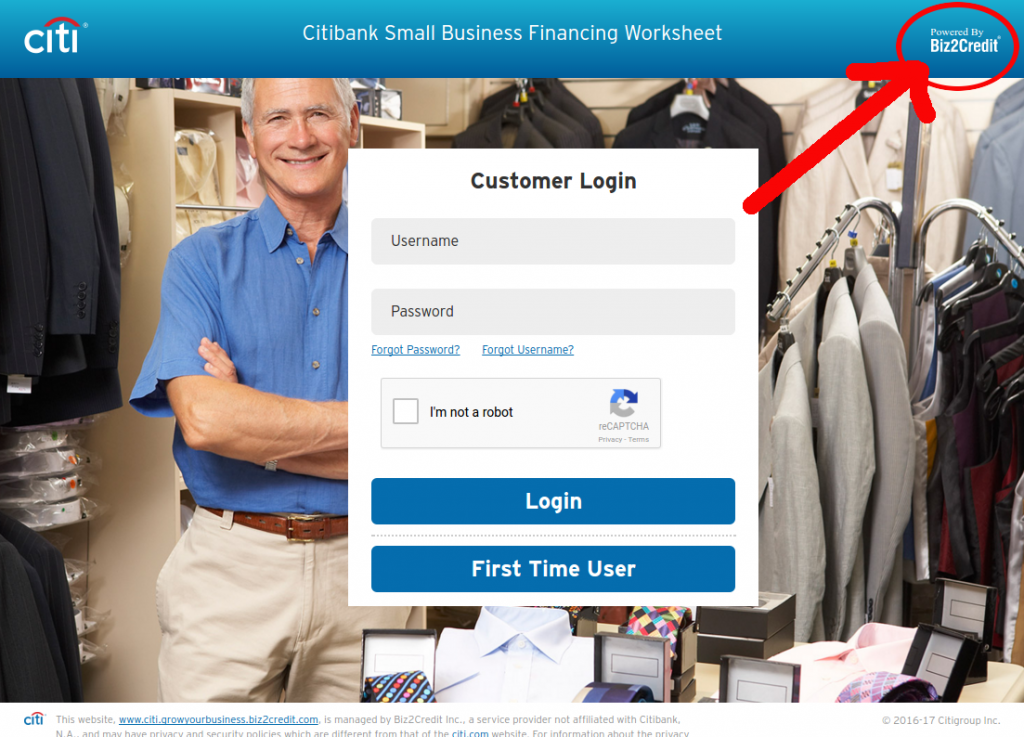

January 27, 2017Business Insider revealed that Biz2credit and Citigroup have quietly partnered up on a website to make small business loans up to $1 million. There was no actual link to it, so we’ve found it ourselves.

The link appears in several areas of Citi’s website under the small business finance category and that brings you here:

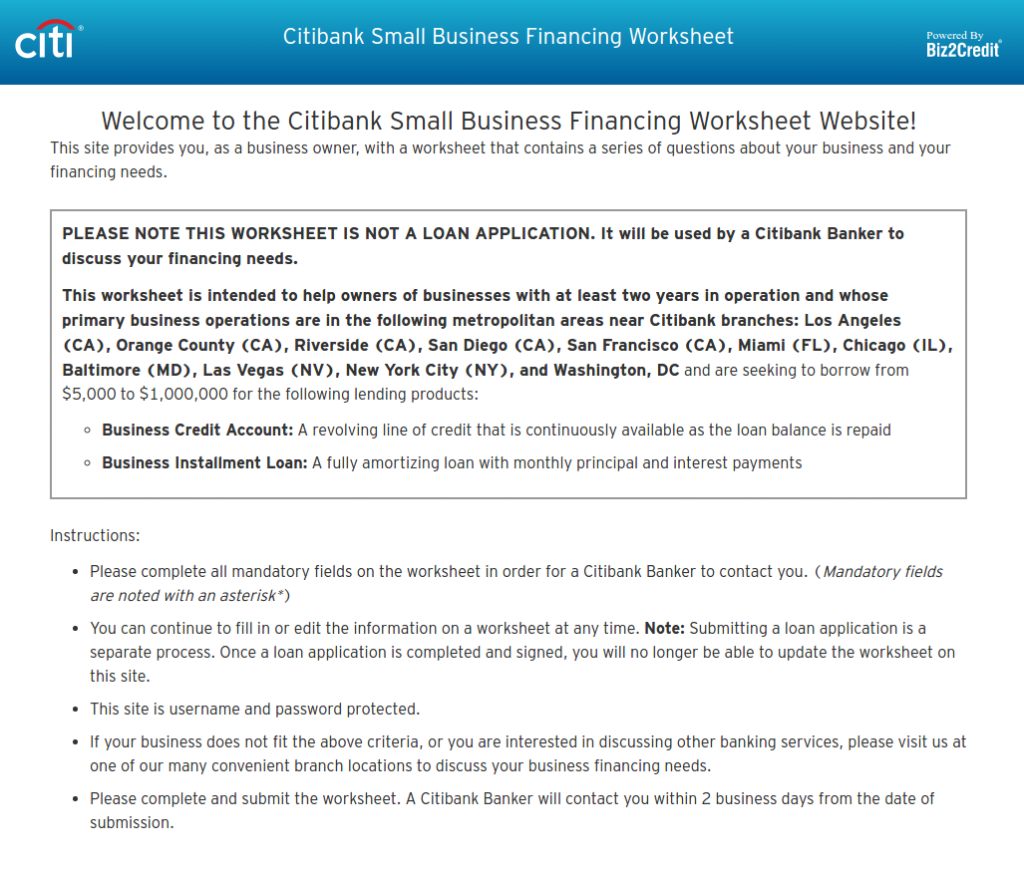

When you go to register, a page pops up insisting that this isn’t a loan application, but rather just a “worksheet” to have a banker from Citi call you within 2 days. “It will be used by a Citibank Banker to discuss your financing needs,” it reads.

The worksheet asks for very basic information such as name, business name, address, annual revenue, and financing requested.

If this doesn’t sound overly advanced, perhaps that’s why it’s being kept on the down low. According to Business Insider, Biz2credit CEO Rohit Arora said they have chosen not to publicize the effort because it’s in the very early stages.

The cat’s out of the bag now…

New FCC Chairman Ajit Pai Has Been Critical of Serial TCPA Plaintiffs, Record Shows

January 24, 2017 FCC Commissioner Ajit Pai is the commission’s new chairman, thanks to President Trump. A republican who believes free markets are better for American consumers than highly regulated ones, Pai is likely to offer a sympathetic ear to companies besieged by serial TCPA plaintiffs, a problem that has reached epidemic proportions in the small business finance industry.

FCC Commissioner Ajit Pai is the commission’s new chairman, thanks to President Trump. A republican who believes free markets are better for American consumers than highly regulated ones, Pai is likely to offer a sympathetic ear to companies besieged by serial TCPA plaintiffs, a problem that has reached epidemic proportions in the small business finance industry.

In 2015, when the FCC announced a broader definition of an autodialer under the TCPA, Pai strongly dissented.

Instead, the Order takes the opposite tack. Rather than focus on the illegal telemarketing calls that consumers really care about, the Order twists the law’s words even further to target useful communications between legitimate businesses and their customers. This Order will make abuse of the TCPA much, much easier. And the primary beneficiaries will be trial lawyers, not the American public.”

– Ajit Pai, 2015

If you’ve been threatened or sued by someone for violating the TCPA, you’re not alone. When we researched Smile, Dial and Trial, we reviewed dozens of lawsuits filed against small business finance companies and have since even discovered new ones filed since then.

The Top Small Business Lending Platform Finalists Named By LendIt

January 20, 2017The LendIt Industry Awards has named six finalists for the Top Small Business Lending Platform. They are:

- OnDeck

- Kabbage

- SmartBiz

- StreetShares

- Ascentium Capital

- iwoca

OnDeck you should know by now. They are publicly traded on the NYSE under ticker ONDK. We last sat down with them in October, shortly before they announced a $200 million credit facility with Credit Suisse.

Kabbage was one of the first online small business lenders to truly experiment with complete automation. In the last year the company has partnered with banking giants Santander and Bank of Nova Scotia.

SmartBiz ranked as the number one provider of non-Express, SBA 7(a) loans under $350,000 for fiscal year 2016. An online platform, they generated $200 million in funded SBA 7(a) loans through its bank lending partners during that period.

StreetShares has a strong focus on funding veteran small businesses. The company is also one of a very few to get approved for Reg A+ under the JOBS Act, which allows them to accept investments from unaccredited retail investors (with some limitations).

Ascentium Capital actually funded nearly $900 million to small businesses in 2016 and was acquired by PE firm Warburg Pincus just a few months ago.

iwoca is based in the UK but also operates in Germany, Spain, and Poland. They offer lines of credit to small businesses up to £100,000 with repayment terms of up to 12 months. Interest rates range from 2% to 6% per month. iwoca has raised £46 million through debt and equity.

According to LendIt, finalists for this category were awarded to the top small business lending platform based on a combination of loan performance, volume, growth, product diversity and responsiveness to stakeholders.

A similar category, the greatest Emerging Small Business Lending Platform also had six finalists. They include:

- ApplePie Capital

- Capital Float

- Credibility Capital

- Lendio

- Lendix

- Wunder Capital

More than 30 industry experts will judge and select award winners. You can view all categories, finalists and judges here.

You can also get 15% off the LendIt Conference registration with promo code: Debanked17USA.

The NYDFS Opposes Fintech Charter Proposed by the OCC

January 19, 2017New York State regulators are not happy with the OCC’s willingness to grant bank-like powers to non-banks in the fintech movement.

“NY DFS disputes the OCC’s claim that it has the authority under the National Bank Act for this proposed new charter,” a letter by Superintendent Maria Vullo states. “Nonbank financial institutions are not banks nor are they similar to the entities encompassed by the National Bank Act.”

The letter goes on to make many points, one of which is the reminder of New York’s state sovereignty and another is the argument that such a regulatory experiment would lead to a financial crisis.

The letter follows similar concerns by Democratic members of Congress.

MCA Company Files Suit Against Debt Settlement Company

January 16, 2017Plaintiffs Pearl Gamma Funding, LLC and Pearl Beta Funding, LLC (Pearl) aren’t happy with what a debt settlement firm is allegedly telling their customers, according to a complaint filed in the New York County Supreme Court in November.

“Creditors Relief LLC researches customers who have entered into Merchant Agreements with Pearl, solicits them throughout the country, and advises them to breach their contracts with Pearl,” plaintiffs allege. They also cite an example in which an employee of defendant allegedly told a customer “that Pearl was engaging in illegal activity and its Merchant Agreements were unenforceable.”

Pearl’s causes of action against the defendant include tortious interference with contract, defamation and permanent injunction.

Creditors Relief, based in Englewood Cliffs, NJ, denied the allegations in their response but has asked the court to declare Pearl’s contracts with its customers unenforceable nonetheless.

Due to the nature of pending litigation, neither party was asked to comment.

The Small Business Lender Rankings (A preliminary peek)

January 4, 2017

Here’s a peek at how some of the industry’s largest alternative small business lenders were doing for the year in originations as they headed into the last quarter of 2016. This data should be considered an estimate and is obviously not comprehensive. Still, this should give you a clue where some players will end up:

| Lender | Q1 – Q3 2016 | FY 2015 | FY 2014 |

| OnDeck | $1,772,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal | $1,000,000,000 | $850,000,000 | |

| Square | $550,000,000 | $400,000,000 | $100,000,000 |

| IOU Financial | $87,500,000 | $146,400,000 | $100,000,000 |

Other small business finance companies do more than just loans, with many doing merchant cash advances. And some companies work to get customers funded through other platforms when prospective customers don’t fit their risk box. The numbers below are origination approximations regardless of whether the customer was ultimately placed on their balance sheet or someone else’s and whether or not the transaction was a loan or MCA.

| Funder | Q1 – Q3 2016 | FY 2015 | FY 2014 |

| Bizfi | $415,000,000 | $481,000,000 | $277,000,000 |

| Yellowstone Capital | $350,000,000 | $422,000,000 | $290,000,000 |

| Platinum Rapid Funding Group | $135,000,000 | $100,000,000 |

Platinum Rapid Funding Group Originated $180 Million in 2016

January 3, 2017A social media post by Platinum Rapid Funding Group CEO Ali Mayar, revealed that the Long Island-based company had originated $180 million in deal flow in 2016. That’s almost twice their 2015 volume, and is a new record for the company.

In Mayar’s post, he wrote, “Thank you to everyone who’s a part of this unstoppable organization for an amazing year and the best is yet to come.”