Articles by deBanked Staff

Prosper Lost A Whopping $119 Million in 2016

March 20, 2017 Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

| Year | Revenue | Profit (Loss) |

| 2012 | $7.6M | ($16.0M) |

| 2013 | $18.3M | ($27.0M) |

| 2014 | $81.3M | ($2.6M) |

| 2015 | $204.2M | ($26.0M) |

| 2016 | $136.0M | ($118.7M) |

General and Administrative was the largest line item expense at $102.7M, which consisted mainly of employee compensation. The second largest expense was Sales and Marketing at $70.1M.

The company originated more than $2.2 billion in loans for the year, down from $3.7 billion last year.

“The decrease in originations we experienced during the year ended December 31, 2016 were primarily driven by a number of our largest investors pausing or significantly reducing their purchases of Borrower Loans beginning in the second quarter of the year,” their earnings report said. “We believe these investors have paused or reduced their investment activity because of an increase in their cost of capital; negative actions and publicity at competitors; and our limited use of investor rebates, which have become more prevalent in the industry.”

To try and correct course, Prosper offered to sell up to 35% of their company to a consortium of Wall Street’s elite who have the right to buy up to $5 billion of their loans over the next 2 years.

WebBank Releases Earnings, Market Valuation

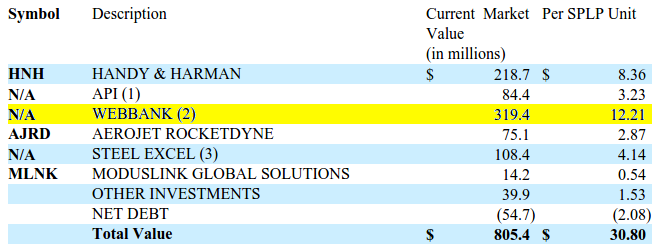

March 20, 2017 WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

“Despite significant declines in a number of WebBank’s key programs, caused by capital market disruptions, WebBank successfully added new partners, new products and began holding more assets to maturity in 2016,” the report read.

Although Steel Partners also owns businesses in energy, defense, logistics, food products and more, WebBank is its most valuable segment with a market valuation of $319.4 million. That number, according to the release, is 12x the company’s after-tax net income.

Steel Partners got in on WebBank early, making their initial investment in the bank more than 20 years ago in 1996.

“WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank’s products,” the report says.”Revenue is largely derived from these loans, which provide fee and interest income.”

Dear Fintech, The OCC Wants to Welcome You to The Family

March 16, 2017 Congratulations fintech, you did it. The OCC wants fintech companies who are interested and meet the criteria, to apply for a Special Purpose National Bank (SPNB) charter if they so choose, according to a licensing manual published by the agency.

Congratulations fintech, you did it. The OCC wants fintech companies who are interested and meet the criteria, to apply for a Special Purpose National Bank (SPNB) charter if they so choose, according to a licensing manual published by the agency.

“Providing a path for fintech companies to become national banks can make the financial system stronger by promoting growth, modernization, and competition,” is one of several arguments they make in their decision to move forward. And it would be optional, something a company could choose to pursue.

“The OCC will expect an SPNB applicant whose business plan includes lending or providing financial services to consumers or small businesses to demonstrate a commitment to financial inclusion,” they say and that commitment must be documented in an official plan which must be put up and submitted for public comment. Basically, the entire process will be very public so it’s unlikely that companies will slip through and become banks without anyone really knowing.

New York’s Department of Financial Services nonetheless issued a heated response to the proposal. “The imposition of an entirely new federal regulatory scheme on an already fully functional and deeply rooted state regulatory landscape will invite efforts to evade state usury laws and other consumer protections, stifle small business innovation, create institutions that are too big to fail, and increase the risks presented by nonbank entities,” they wrote. They see the move as an attack on their in-state regulatory powers. “The proposal threatens to create an entirely new federal regulatory program, creating serious regulatory uncertainty that threatens to invade state authority and sovereignty.”

Read the OCC’s charter licensing manual here

Read the NYDFS response here

How Whitepages Turned Their Data into an Identity Verification Tool for Online Lenders

March 15, 2017 Whitepages might be a 20-year old company but the data they’ve amassed over time can add significant value to online lenders, the company claims. Whitepages Pro, which offers identify verification, allows lenders to gauge if an individual is real. “It examines fraud risk, not credit risk,” company CEO Rob Eleveld said in a brief interview at LendIt last week.

Whitepages might be a 20-year old company but the data they’ve amassed over time can add significant value to online lenders, the company claims. Whitepages Pro, which offers identify verification, allows lenders to gauge if an individual is real. “It examines fraud risk, not credit risk,” company CEO Rob Eleveld said in a brief interview at LendIt last week.

A simple query of an individual’s name, phone number, email, address or business name will return results not easily accessible elsewhere, like how long that person’s email address has been in their system or the likelihood that the email address was generated by a bot, not a real person. A match is good, no match might not be good, they say. Their system can also do things like identify the carrier the phone number belongs to and whether or not that carrier, if it’s VOIP or something, might have a higher propensity for fraud.

Eleveld said that an impostor could try applying for a loan with a stolen social security number, but it’s harder for them to fake an entire online profile. These queries, he confirmed, can all be done through an API since online lenders are typically driven by speed. Big names are already using it such as Quicken Loans and loandepot, and those are just a couple of names from the online lending space alone.

“The company houses more than 5 billion global identity records,” according to their website, and customers such as “Wells Fargo, Microsoft, Western Union, Under Armour, Priceline, and American Airlines use Whitepages Pro data to mitigate risk and improve the customer experience.”

Kabbage CEO Rob Frohwein Pokes Fun at “Alternative Lending”

March 14, 2017 At LendIt, Kabbage CEO Rob Frohwein poked fun at alternative lending, suggesting that it should just be called lending. His presentation, titled “Alternative Lending is Dead Long Live Data,” put the last few years of irrational exuberance into perspective. Below are some of his one-liners:

At LendIt, Kabbage CEO Rob Frohwein poked fun at alternative lending, suggesting that it should just be called lending. His presentation, titled “Alternative Lending is Dead Long Live Data,” put the last few years of irrational exuberance into perspective. Below are some of his one-liners:

“You don’t disrupt banks by focusing on the advantages that banks have over you.”

“Most online lenders thought by calling themselves a technology company, they are one.”

“However, the biggest piece of technology that most of them promote is an online application.”

“There’s nothing special about an online application.”

Frohwein also revealed some interesting facts about Kabbage during the presentation, including that their customers borrow from them on average 20-25 times over the course of 4 years, whereas their competitors only make only 2.2 loans to their customers on average.

Brief: Former CAN Capital CFO Moves On

March 9, 2017According to the WSJ, Aman Verjee, who was CAN Capital’s CFO up until late last year, has taken the COO position at 500 Startups. The company has invested in more than 1,800 startups across more than 60 countries. According to the website, “500 Startups was founded in 2010 by former PayPal and Google alumni Dave McClure and Christine Tsai, along with many other friends and supporters.”

CAN Capital has not yet named a replacement CFO.

In The UK, Regulators Advise Where The Line Between Banks and Non-banks Lies

March 1, 2017Online lenders shouldn’t be borrowing money from other online lenders and using that money to lend, the Financial Conduct Authority in the UK warned on Tuesday. Doing so without regulatory permission, they explained, would constitute accepting deposits and be a criminal offense.

A copy of the official letter signed by Jonathan Davidson, Director of Supervision – Retail and Authorisations, is publicly available.

According to the Financial Times, the warning was prompted after RateSetter asked the government in October 2016 if such activity was acceptable. They had been engaged in such wholesale lending, as it’s called, since 2016 but have since stopped.

For Lending Club Borrowers, Interest Now Accrues During Grace Periods

February 26, 2017On February 24th, Lending Club eliminated a courtesy that had long been afforded to borrowers, interest waivers during grace periods. Specifically, borrowers who missed a monthly payment were given 15 extra days to make the payment with no extra interest assessed or late fees. Going forward, interest will indeed accrue during grace periods.

“we are eliminating the grace period interest waiver in order to better align borrower payment incentives as we seek to deliver solid returns to our investors,” Lending Club said in an email.

Since this will not affect a borrower’s monthly payment, all additional accrued interest will be extended to another month beyond the maturity date.