Articles by deBanked Staff

Update in the Argon Credit Bankruptcy Case

March 31, 2017On March 28th, United States Bankruptcy Judge Deborah L. Thorne, ordered the trustee in the Argon Credit case to transfer the net proceeds and loan portfolio payments to the biggest creditor, Fund Recovery Services (FRS). That cash will be used to satisfy the approved secured claim of $37.3 million. FRS is an assignee of Princeton Alternative Income Fund, LP. Argon Credit was an online consumer lender that made loans between $2,000 and $35,000 with APRs ranging from 4.99% to 149%.

Initially, Argon Credit had applied for Chapter 11 bankruptcy after “experiencing financial difficulty,” though allegations of improprieties and mismanagement have come up in the legal filings. When FRS tried to stop their collateral from being spent, Argon argued in court that such a thing was unnecessary because they had more than enough collateral to pay off their debt to FRS, including $5.5 million worth of leads. By FRS’s calculations, the leads were worth as little as $1,500, not millions. Ultimately, the judge attributed no value to them.

The case was converted to Chapter 7 and FRS should be able to get repaid.

StreetShares Reports $2.8M Loss on Just $277,000 in Revenue For Last Six-Month Period

March 30, 2017 StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares has so far charged off 23 loans for a combined principal balance of $380,804. Charge-off determinations are made after 150 days of delinquency.

The company made history last year by becoming the first lender in the US to be approved by the SEC to use funds from public investors to back loans to small businesses. This was done through Regulation A+ of the Jumpstart Our Business Startups (JOBS) Act. Reg A+ investors make up $656,675 of StreetShares’ liabilities on the balance sheet.

StreetShares currently makes loans to small businesses between $2,000 to $500,000 for terms of three months to three years.

The company also spent more than 5x their revenue on payroll and payroll tax for the six-month period and more than 3x their revenue on marketing expenses.

Earlier this month, StreetShares announced a partnership with Nor-Cal FDC “to assist small business and veteran business owners in obtaining funding needed to win new opportunities.”

In the release, StreetShares CEO Mark Rockefeller said, “we’re eager to provide veteran-owned small businesses with the funding solutions they need to grow.”

House Committee on Financial Services to Air ‘The State of Bank Lending in America’ at 2PM EST

March 28, 2017Update: The House has blocked streaming of this procession from any place other than Youtube

The Subcommittee on Financial Institutions and Consumer Credit will hold a hearing entitled “The State of Bank Lending in America” at 2PM EST on Tuesday. According to a memo, “the hearing will examine recent trends in lending and how the current regulatory climate impacts the availability of credit for consumers and small businesses.” The premise is that community financial institutions have been lending less since the passage of Dodd-Frank and that this may be constraining consumer and small business access to credit.

Speaking on the panel before the Committee is:

- Mr. Scott Heitkamp, President and Chief Executive Officer, ValueBank Texas, on behalf of the Independent Community Bankers of America

- Ms. Holly Wade, Director, Research and Policy Analysis, National Federation of Independent Businesses

- Mr. David Motley, President, Colonial Companies, on behalf of the Mortgage Bankers Association

- Mr. Michael Calhoun, President, Center for Responsible Lending

We will attempt to live stream it on deBanked’s homepage when it airs.

Amazon Sure is Making a Lot of Small Business Loans

March 26, 2017 Amazon had $661 million in seller receivables at the end of 2016, according to their earnings report, nearly double from the year before. These receivables are from loans made to small businesses (primarily to purchase inventory) who are sellers on their platform.

Amazon had $661 million in seller receivables at the end of 2016, according to their earnings report, nearly double from the year before. These receivables are from loans made to small businesses (primarily to purchase inventory) who are sellers on their platform.

Apparently the lending business is going well for them too, since they claim the allowance for loan losses is so small that it’s not even material enough to report. And similar to Square Capital, Amazon incurs virtually no cost to acquire these borrowers.

One year ago, company CEO Jeff Bezos said in a letter to shareholders that “there are over 70,000 entrepreneurs with sales of more than $100,000 a year selling on Amazon.” By then the company had already lent more than $1.5 billion to small businesses across the US, UK and Japan.

“We wanted to bring the same shopping experience that you have on amazon, which is the one-click shopping experience, to the lending program,” a spokesperson says in a 2014 video about the program. “Instead of going to a bank, having interviews, audited financial statements, a 3 week process and then only a small fraction of people getting approved, our process is literally 3 fields and 3 clicks.”

If Kabbage Wanted to Buy, Would OnDeck Sell?

March 24, 2017 A single line in a Reuters story was enough to cause OnDeck’s stock to jump by as much as 11% on Thursday. Industry blogs and news outlets had reacted pretty quickly to word of an unnamed source claiming that OnDeck is a potential acquisition target if Kabbage raises a new equity round. OnDeck closed for the day up only 6.5%.

A single line in a Reuters story was enough to cause OnDeck’s stock to jump by as much as 11% on Thursday. Industry blogs and news outlets had reacted pretty quickly to word of an unnamed source claiming that OnDeck is a potential acquisition target if Kabbage raises a new equity round. OnDeck closed for the day up only 6.5%.

BloombergGadfly columnist Gillian Tan, wrote that a deal was not very likely because of how much investors are already down since the IPO. “Assuming Kabbage were to propose a traditional takeover at a standard premium, it probably would be swiftly rejected by On Deck’s earliest investors, who still own a combined stake of more than 45 percent, according to data compiled by Bloomberg,” she wrote. “With the stock trading at less than a quarter of its 2014 initial public offering price, it would take a generous premium to get them interested.”

OnDeck also lent nearly twice as much as Kabbage last year and obviously still has faith in leadership considering that their pre-IPO CEO is still in charge. There’s little to suggest at this time that OnDeck would be willing to throw in the towel and sell out to a smaller, younger competitor and book a big loss for shareholders who have been with them since the beginning.

The day before the rumor started, OnDeck actually announced that it had increased its asset-backed revolving credit facility with Deutsche Bank by approximately $52 million to a total of up to approximately $214 million.

OnDeck CEO Noah Breslow Talked Tech Worker Shortage in Canada on BloombergTV

March 22, 2017On BloobergTV Canada, OnDeck CEO Noah Breslow explained what he thought the country could do to boost innovation. The discussion stemmed from Canada’s decision to set aside C$800 million over the next four years to carry out that objective.

Breslow said that since Canada has excellent schools, those graduates can be nurtured into forming businesses and creating business investment opportunities. He also said that vocational training towards today’s new working-style job would be beneficial as well, whether it’s jobs for people who can design the latest algorithm or people who can build systems and data centers or can rack servers together.

When asked if perhaps government intervention was not the answer to achieve this, Breslow said that there are two ends of that spectrum, and where he believed intervention could be helpful was in the formation and talent development and formation incubation stage of companies. For later-stage companies, it was probably not appropriate, he said.

Breslow also expressed his belief that a permissive immigration policy is important and that there should be less friction to bring in skilled workers to Canada.

You can watch the full video below to hear the rest:

Prosper Lost A Whopping $119 Million in 2016

March 20, 2017 Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

Prosper might be the online lender for the who’s who of Wall Street these days, but the company still lost $119 million in 2016. To add perspective, Prosper only had $136 million in revenue for the year, meaning that for every dollar it earned it spent almost two. The loss was also more than 4x greater than the loss in 2015 even though the company earned significantly less revenue in 2016.

| Year | Revenue | Profit (Loss) |

| 2012 | $7.6M | ($16.0M) |

| 2013 | $18.3M | ($27.0M) |

| 2014 | $81.3M | ($2.6M) |

| 2015 | $204.2M | ($26.0M) |

| 2016 | $136.0M | ($118.7M) |

General and Administrative was the largest line item expense at $102.7M, which consisted mainly of employee compensation. The second largest expense was Sales and Marketing at $70.1M.

The company originated more than $2.2 billion in loans for the year, down from $3.7 billion last year.

“The decrease in originations we experienced during the year ended December 31, 2016 were primarily driven by a number of our largest investors pausing or significantly reducing their purchases of Borrower Loans beginning in the second quarter of the year,” their earnings report said. “We believe these investors have paused or reduced their investment activity because of an increase in their cost of capital; negative actions and publicity at competitors; and our limited use of investor rebates, which have become more prevalent in the industry.”

To try and correct course, Prosper offered to sell up to 35% of their company to a consortium of Wall Street’s elite who have the right to buy up to $5 billion of their loans over the next 2 years.

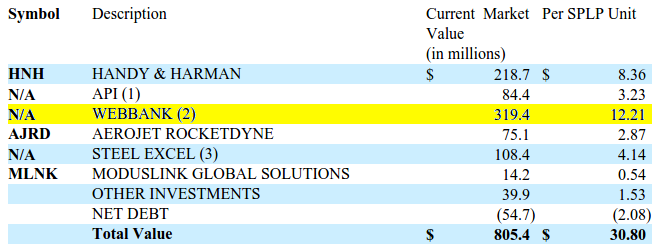

WebBank Releases Earnings, Market Valuation

March 20, 2017 WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

WebBank, a Salt Lake City-based bank commonly used by online lenders such as Avant, CAN Capital and Prosper to make loans nationwide, reported year-end figures last week through an SEC filing. The company is 91.2% owned by Steel Partners Holdings L.P (NYSE:SPLP). The bank reported net income of $29.2 million for 2016.

“Despite significant declines in a number of WebBank’s key programs, caused by capital market disruptions, WebBank successfully added new partners, new products and began holding more assets to maturity in 2016,” the report read.

Although Steel Partners also owns businesses in energy, defense, logistics, food products and more, WebBank is its most valuable segment with a market valuation of $319.4 million. That number, according to the release, is 12x the company’s after-tax net income.

Steel Partners got in on WebBank early, making their initial investment in the bank more than 20 years ago in 1996.

“WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank’s products,” the report says.”Revenue is largely derived from these loans, which provide fee and interest income.”