Articles by deBanked Staff

How Much Elevate Spends to Acquire Customers

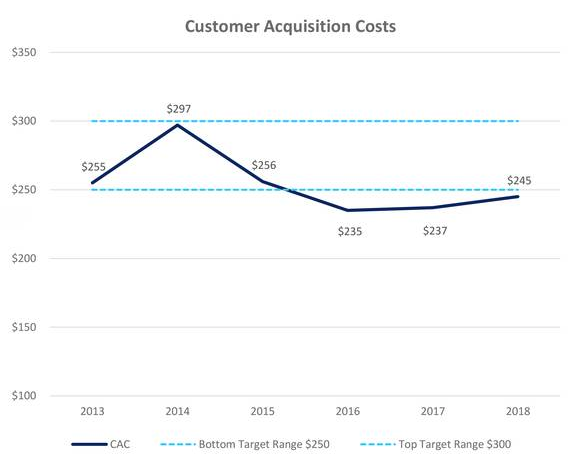

February 11, 2019How much does a non-prime consumer lender spend to acquire a borrower? According to Elevate’s Q4 earnings report, the company spent less than $150 per borrower to originate $31 million in loans towards their partnership with FinWise Bank. Overall, however, their cost of acquisition has hovered below $245.

Elevate’s direct mail channels made up 42% of acquisitions in 2018. That’s down from 54% in 2017. In the company’s earnings call, Elevate CEO Ken Rees said of the decreasing reliance on direct mail, “we believe this sets us up for strong future growth through these expanded channels.”

Elevate offers three products to non-prime customers: RISE, a state-licensed online lender that offers up to $5,000 in unsecured installment loans and lines of credit, Elastic, a bank-issued line of credit, and Sunny, a short-term loan product for customers in the UK. RISE and Elastic serve the US market.

Separately, Elevate reported $787 million in revenue for 2018, an increase of $113 million, or 17%, compared to 2017’s full-year revenue of $673 million.

New Jersey MCA & Business Loan Disclosure Bill Update (S2262)

February 6, 2019 Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

Bill S2262 in the New Jersey State Senate mandating disclosures on MCA and business loan contracts, was amended last week. In its current form, the bill, if it became law, would require MCA providers to disclose:

- the total dollar costs to be charged to a small business concern, assuming the small business concern delivers all purchased receivables to providers at the time they are generated or at a mutually agreed upon time, and all required fees and charges that are paid by the small business concern and that cannot be avoided by the small business concern;

- the amount financed, which shall mean the advance amount less any prepaid finance charges; and

- for a cash advance that calculates repayment costs dependent on the small business concern’s future receivables, the estimated annual percentage rate, provided as a range, with at least three different repayment times provided and a narrative explanation of how each rate was derived. Any estimated annual percentage rate is to be calculated using a projected sales volume that is based on the small business concern’s average historical sales or the sales projections relied on by the provider in underwriting the cash advance; or

- for a cash advance that calculates repayment costs as a fixed payment, the annual percentage rate, expressed as a nominal yearly rate, inclusive of any fees and finance charges.

Brokers would also be required to provide uniform fee disclosures to both the small business owner and lender or MCA funding provider in a document separate from the funding contract before a small business consummates a loan or MCA transaction.

Previously, the bill defined merchant cash advances as loans. The latest draft updated the definition to mean a financing option that allows a small business concern to sell all or a portion of its future sales collections or other future revenues in exchange for an immediate payment. It refers to this as an asset-based transaction.

You can follow the bill’s updates and read the latest drafts here.

S2262 was originally introduced 11 months ago in March 2018.

LendingPoint Gets Even More Financing

February 4, 2019LendingPoint announced today that it has closed an increase of its mezzanine funding, a hybrid of debt and equity financing. The company’s mezzanine financing now totals more than $67.5 million. Paragon Outcomes Management LLC is the primary investor and was joined for this round by an unnamed co-investor.

“Paragon Outcomes continues to provide outstanding support for the growth of the LendingPoint platform and balance sheet,” said Tom Burnside, LendingPoint co-founder and CEO. “Their support enables us to continue to build our high performing balance sheet and fuels our march towards profitability quarter. To have companies like Paragon Outcomes want to be part of our future is a strong wind at our back.”

This is a continued expansion of an initial credit facility from Paragon Outcomes for $20 million in 2017, followed by an increase to $52.5 million in June 2018.

LendingPoint provides consumer loans of up to $25,000 and has a platform, called LendingPoint Merchant Solutions, that allows merchants to offer loans to their customs for point-of-sale purchases.

In addition to today’s announcement, LendingPoint also secured an up to $500 million senior credit facility in August 2017 and an up to $600 million senior credit facility in May 2018. Both deals were arranged by Guggenheim Securities.

Founded in 2014, LendingPoint is a privately held company headquartered in Kennesaw, GA with offices in San Diego, CA.

New York Introduces Bill to Ban COJs in Financial Contracts

February 4, 2019 New York Assemblymembers Yuh-Line Niou and Crystal Peoples-Stokes have introduced a bill that would prohibit Confessions of Judgment (COJs) from being used in any contract or agreement for a financial product or service.

New York Assemblymembers Yuh-Line Niou and Crystal Peoples-Stokes have introduced a bill that would prohibit Confessions of Judgment (COJs) from being used in any contract or agreement for a financial product or service.

Peoples-Stokes’ district was one of the first districts to boycott COJs originated by merchant cash advance companies after Erie County Clerk Michael Kearns publicized that he would no longer approve them.

A03636 proposes the following:

§ 396-aaa. Confession of judgment requirement for certain contracts; prohibition.

1. No person shall require a confession of judgment in any contract or agreement for a financial product or service.

2. As used in this section the following terms shall have the following meanings:

(a) “Financial product or service” shall mean any financial product or financial service offered or provided by any person regulated or required to be regulated by the superintendent of financial services pursuant to the banking law or the insurance law or any financial product or service offered or sold to consumers except financial products or services: (i) regulated under the exclusive jurisdiction of a federal agency or authority, (ii) regulated for the purpose of consumer or investor protection by any other state agency, state department or state public authority, or (iii) where rules or regulations promulgated by the superintendent of financial services on such financial product or service would be preempted by federal law.

(b) “Financial product or service regulated for the purpose of consumer or investor protection”: (i) shall include (A) any product or service for which registration or licensing is required or for which the offeror or provider is required to be registered or licensed by state law, (B) any product or service as to which provisions for consumer or investor protection are specifically set forth for such product or service by state statute or regulation and (C) securities, commodities and real property subject to the provisions of article twenty-three-A of the general business law, and (ii) shall not include products or services solely subject to other general laws or regulations for the protection of consumers or investors.

PayPal Has a Lot of Merchants and Venmo Is Adding a Boost

February 1, 2019 More than 21 million merchants accept PayPal to take advantage of the 246 million consumers who use it. That’s a lot of merchants to offer value-added products like PayPal Working Capital and invoicing services. But then there’s Venmo, a fast growing digital wallet that PayPal also owns that processed $19 billion in payment volume last quarter and is projected to handle $100 billion worth across all of 2019.

More than 21 million merchants accept PayPal to take advantage of the 246 million consumers who use it. That’s a lot of merchants to offer value-added products like PayPal Working Capital and invoicing services. But then there’s Venmo, a fast growing digital wallet that PayPal also owns that processed $19 billion in payment volume last quarter and is projected to handle $100 billion worth across all of 2019.

Although Venmo itself is not a profitable business yet, it has gone from generating almost zero revenue to hitting a $200 million revenue run rate by the end of 2018. And it’s bringing in new users thanks to a network effect. When a network effect is present, the value of a product or service increases according to the number of others using it.

PayPal CEO Dan Schulman said on the company’s earnings call on Thursday that PayPal and Venmo will probably attract another 33 million new active users in 2019, thanks in part to the network effect and “the virality of Venmo.”

Meanwhile, PayPal COO Bill Ready said on the same call that merchants tend to come to them directly for services like working capital loans rather than to online marketplaces like Shopify or Wix because oftentimes merchants sell across multiple marketplaces. “PayPal becomes the aggregation point for them to connect to each of those platforms,” he said.

Top Accounting Officer at StreetShares Resigns

January 31, 2019Jesse Cushman, who served as StreetShares’ Chief Business Officer and Principal Financial & Accounting Officer, has resigned, according to a Form 1-U filed with the SEC this week. His exit was made effective as of January 1, 2019.

StreetShares president Michael Konson is currently filling the role in an interim capacity until a permanent successor can be named.

StreetShares’ financials have left something to be desired. The company recently reported a 12-month net loss of $6.5 million on only $3 million in revenue.

Parris Sanz Joins Petal as General Counsel

January 31, 2019Former CAN Capital CEO Parris Sanz is now the General Counsel for Petal, according to a company announcement. Petal is a US credit card aimed at the unbanked that recently closed a $30 million Series B round led by Peter Thiel’s Valar Ventures.

According to a story in TechCrunch, Petal had more than 100,000 potential applicants sign up during the company’s private beta phase. This latest capital raise will be used in part to expand the product to more customers.

deBanked CONNECT Miami 2019 Photos

January 28, 2019