Archive for 2019

Business Loan Brokers Indicted

March 16, 2019 Five business loan brokers were named in a federal indictment in Ohio for defrauding a 69-year-old business owner out of his money and cars. In addition to being asked for hundreds of thousands of dollars in upfront fees to apply for the loan, the victim signed over the title of 55 vehicles to a broker to serve as the collateral. The vehicles included a Ford Mustang, several dump trucks, several tractors, several restored classic vehicles, a Freightliner motor home, and trailers.

Five business loan brokers were named in a federal indictment in Ohio for defrauding a 69-year-old business owner out of his money and cars. In addition to being asked for hundreds of thousands of dollars in upfront fees to apply for the loan, the victim signed over the title of 55 vehicles to a broker to serve as the collateral. The vehicles included a Ford Mustang, several dump trucks, several tractors, several restored classic vehicles, a Freightliner motor home, and trailers.

In reality, there was no loan.

Text messages quoted in the indictment indicated that one of the defendants traveled from New York to Youngstown, Ohio by Greyhound Bus to begin driving the vehicles back to New York one-by-one, but their scheme faced challenges when they could not afford the gas to drive all of the cars. By the end, the victim was cooperating with the police and one of the defendants was lured back to Ohio in September to pick up a payment where he was then arrested.

deBanked discovered a message board post that appears to be published by one of the defendants months after the alleged crime. In it, she attempts to recruit other brokers to send her business with promises of high commissions, same day approvals, free leads, and a policy of no backdooring.

LinkedIn Posts Are Turning Into Deals & Dollars

March 14, 2019

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

On average, I sign up one ISO every time I post a message on LinkedIn, says Jennie Villano, VP of Business Development at Kalamata Capital Group. They don’t all end up submitting business, she adds, but overall it works. It costs her nothing more than her time and it produces results.

Villano is among the growing crowd of industry insiders attempting to convert social media posts into measurable business. With more than 600 million users on LinkedIn, there is no question about the potential to reach clients. The prevailing wisdom is that you need to be on social media and sharing, but share what exactly?

New Hampshire-based Everlasting Capital is building a window into the business lives of co-founders Josh Feinberg and Will Murphy. One of their recent social media posts focused on their search for a new office lease, while another was a video stream of Feinberg making a real live cold call. The rewards span the gamut, from merchants seeking funding to offers to speak professionally in front of large audiences. And it’s not just about them. “We have worked with our employees to get confident on camera which is making them a lot more comfortable on the phone,” Feinberg said.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

Anthony Collin, CEO of New York-based Smart Business Funding, also attests to LinkedIn. “We definitely generate sales from posting online,” Collin shared, explaining that it was a mix of ISOs and merchants who reach out. Collin said that he and two others in the company meet weekly to generate ideas for the daily posts. They try to make the posts timely, either related to something going on in the industry or to current events, like national elections.

For Jennie Villano, it’s not always a sales pitch. She has posted about being a single mom and about how to keep an upbeat attitude. “Your co-workers, your friends. Are they positive, or are they always complaining?” Villano asks in the video. “Try to surround yourself with positive people who see the best in everything.” She’ll typically extend the offer to do business in the videos that she makes and shares, but not all of them. She shares 2-3 videos a week and her posts typically receive thousands of views.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Sometimes a video needs a little bit of priming to draw the viewer in. Everlasting Capital, for example, filmed an executive making a sales pitch in their conference room to company CEO Josh Feinberg. But it’s something you must watch, or so the title of the post suggests, because they say the executive drove 10 hours to the office for the opportunity.

Though other social networks are being used in full force by many industry players, LinkedIn is definitely a platform to consider. “We’ve gotten tremendous value from posting to LinkedIn,” Smart Business Funding’s Collin said.

Competition Steps Up in Canadian Small Business Lending Market

March 11, 2019 Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Funding Circle started in the UK and expanded outwards to the US, Germany, and The Netherlands, but the UK still comprises of more than 60% of their global origination volume. Their foray into Canada is a good thing for small business owners and lenders, according to Paul Pitcher, founder and CEO of SharpShooter, a funder based in Toronto.

“I see it as win-win,” Pitcher said.

He said that a win for Canadian small business owners is a win for SharpShooter because it means more potential merchant clients. Pitcher said that he loves OnDeck, a rival, is in Canada, in part because OnDeck’s marketing has helped educate Canadian merchants about alternative lending products.

Similarly, Benaroch said he thinks that big companies entering the Canadian market will affect CanaCap positively. For instance, Benaroch said that CanaCap hopes to capture companies that get turned down from OnDeck. And perhaps CanaCap can also capture merchants that are declined by Funding Circle.

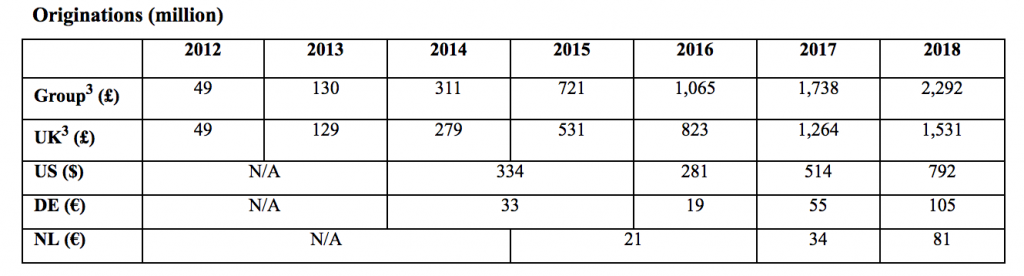

Funding Circle’s loan originations by country by year

Funding Circle’s loan originations by country by year

Benaroch noted that not all outside funding companies have succeeded in Canada, often because they never established a physical presence there. But Funding Circle will be opening a physical office in Toronto.

“We have been evaluating options for expansion over the last year,” said Tom Eilon, who will be Managing Director of Funding Circle Canada. “Canada’s stable, growing economy coupled with good access to credit data and a progressive regulatory environment, made it the obvious choice. The most important factor [in coming to Canada] though was the clear need for additional funding options among Canadian SMEs.”

Funding Circle’s announcement comes on the heels of OnDeck’s December 2018 acquisition of Evolocity Financial Group, a small business funder based in Montreal. While OnDeck started operating in Canada as early as 2015, CanaCap’s Adam Benaroch said that the acquisition of Evolocity is a significant step for OnDeck because Evolocity has an ISO channel in Canada. That runs counter to Funding Circle’s model of mainly going direct to merchant, at least in the US.

Common Mistakes Commercial Tenants Make

March 8, 2019 deBanked recently heard a live presentation given by Dale Willerton, “The Lease Coach.” Willerton is an expert in helping commercial retail tenants to find and negationate spaces. But much of his advice applies to commercial office tenants as well. Below are some common mistakes he urges tenants to avoid:

deBanked recently heard a live presentation given by Dale Willerton, “The Lease Coach.” Willerton is an expert in helping commercial retail tenants to find and negationate spaces. But much of his advice applies to commercial office tenants as well. Below are some common mistakes he urges tenants to avoid:

Not Looking at Multiple Spaces Simultaneously

You want the landlords pursuing you, not the other way around. Therefore, Willerton said that you want to see multiple spaces at once so that you have options and bargaining power. Particularly if you don’t have much time, you don’t want to be at the mercy of one landlord.

Making the First Offer

Let the landlord make the first offer, Willerton says. If you like a space, tell the broker or the landlord, “Why don’t you send me a proposal.” Otherwise, if you make the first offer, you could end up offering more than what the landlord was willing to accept.

Overpaying for Space

Commercial rent is often based on square footage. So if the space you’re looking at has an unusual configuration, or even if it doesn’t, measure it independently to make sure that you’re paying the correct amount. Even if you are already in the space, if you measure the space and see that you actually have less space than what you’re paying for, you can ask for money back from the landlord. Or at least a rent reduction moving forward.

Telegraphing Your Feelings/Intentions

Don’t let a landlord know that you really like their space or that you really want to renew a lease. It gives them leverage. They now know that you really want what they have and that gives them more negotiating power.

Not Walking Away from a Bad Deal

Like deals that include certain personal guarantees. Some tenants require a personal guarantee and others only ask for it. Find out which and avoid personal guarantees when possible.

Looking Too Successful

If the landlord sees that you’re now driving a Porsche to work, or that your 17-year-old daughter has her own Mercedes, he or she may assume that your business is doing very well and may increase your rent when it comes time for a lease renewal. You may, in fact, be doing well. Or you may just appear to be doing well and then get hurt by a rent increase. This doesn’t mean you shouldn’t drive a Porsche if you can afford it – just to fool your landlord. It’s just something to be aware of.

Not Doing Your Homework

Just as you would do your research on a merchant before funding them, research the building and the landlord. Try to find out how long previous tenants have stayed in the building. Why did the previous tenant leave? Are they expanding, or did they have a bad experience with the building or the landlord? Is the building up for sale? If a building changes ownership, that can impact tenants down the road.

Also, Be Mindful of Commercial Agents’ Motives

Willerton said he doesn’t believe that commercial agents are bad or are working against the tenant at all. But he said that if the agent is getting paid on commission by the landlord, it’s important to be mindful that their ultimate “boss” is the landlord and not you.

Storytelling Sales Expert Kindra Hall to Keynote Broker Fair 2019

March 7, 2019 Sales expert Kindra Hall will present at Broker Fair 2019 to teach attendees about the irresistible power of strategic storytelling. If you want to learn to sell differently and use the power of storytelling, her keynote is something you won’t want to miss!

Sales expert Kindra Hall will present at Broker Fair 2019 to teach attendees about the irresistible power of strategic storytelling. If you want to learn to sell differently and use the power of storytelling, her keynote is something you won’t want to miss!

According to Hall, the shift from a transactional economy to a connected one has people scrambling; when surveyed, companies admit they believe a substantial portion of their revenue is under threat as a result. Businesses, brands, sales forces, marketing teams and leaders at all levels are desperately trying to capture attention and resonate with consumers who expect more. Is there a secret weapon? A silver bullet to humanize and connect? Yes. The answer is strategic storytelling.

The problem? In its rapid rise in popularity, “storytelling” has been reduced to in-actionable jargon. Every day businesses and individuals miss critical opportunities to connect with their elusive audiences in powerful and profitable ways because they lack a storytelling skill. Until now.

About Kindra Hall

Kindra Hall is President and Chief Storytelling Officer at Steller Collective, a consulting firm focused on the strategic application of storytelling to today’s communication challenges. Kindra is one of the most sought after keynote speakers trusted by global brands to deliver presentations and trainings that inspire teams and individuals to better communicate the value of their company, their products and their individuality through strategic storytelling.

What began as a storytelling assignment in 5th grade, grew into a passion for not only telling stories, but a mastery for teaching others the methods and science of storytelling so they can better tell their own.

She was a National Champion storyteller (yes, they have those), member of the Board of Directors of the National Storytelling Network and has her master’s degree in communications where she conducted original research studying the role of storytelling in defining and revealing organizational culture.

Kindra is a former Director of Marketing and VP of Sales. Today, Kindra’s work can be seen at Inc.com, Entrepreneur.com and as a contributing editor for SUCCESS Magazine. Kindra’s message spans all industries and her clients include Facebook, Hilton Hotels, Tyson Foods, Target, Berkshire Hathaway and the Harvard Medical School. Her much anticipated book will be released by Harper Leadership in the fall of 2019.

Acquisition Costs Compared for GreenSky, Square, PayPal, OnDeck, Lending Club, and Prosper

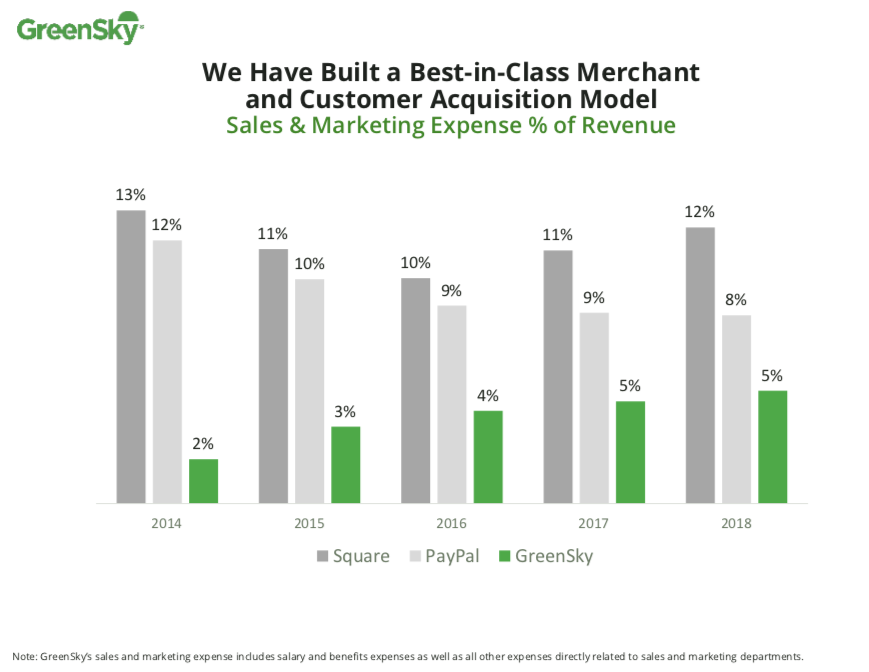

March 5, 2019 Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

Greensky, a consumer lending company, wants investors to know how low its acquisition costs are relative to the competition. The chart above, which appeared in their year-end earnings report, showed how much lower their sales & marketing expense ratio is versus Square and PayPal.

deBanked examined three additional fintech lending companies and ranked them as follows:

| Company Name | 2018 Sales & Marketing Ratio | 2017 |

| GreenSky | 5% | 5% |

| PayPal | 8% | 9% |

| OnDeck | 11% | 15% |

| Square | 12% | 11% |

| Lending Club | 39% | 40% |

| Prosper Marketplace | 76%* | 72% |

*indicates an estimate

The closeness between Square and OnDeck is notable in that Square markets its payment services first and then offers loans (and other products) as an add-on, while OnDeck only offers loans. Despite that, sales & marketing as a percentage of revenue are still virtually the same for each of them. Square is outspending OnDeck on marketing by more than 10:1, however, and is on pace to surpass OnDeck’s annual loan volume.

Prosper, meanwhile, is doing just as poorly as its wacky ratio looks. The company is losing tens of millions of dollars a year with no end in sight.

Download Previous deBanked Magazine Issues Free

March 4, 2019Did you know that you can download previous deBanked magazine issues for free? Simply click any issue on our digital bookshelf to download it in PDF. To receive future issues in print, subscribe here.

Analyzing Confessions of Judgment

March 4, 2019 Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP (“Platzer”) has built one of the leading Merchant Cash Advance practices in New York City. With years of experience handling traditional lending transactions, Platzer has expanded its representation to Merchant Cash Advance Companies (“MCA”) in all aspects of their business cycles, including Participation Agreements, Assets Utilization, Transactional related matters and litigation.

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP (“Platzer”) has built one of the leading Merchant Cash Advance practices in New York City. With years of experience handling traditional lending transactions, Platzer has expanded its representation to Merchant Cash Advance Companies (“MCA”) in all aspects of their business cycles, including Participation Agreements, Assets Utilization, Transactional related matters and litigation.

In the course of representing some of its MCA clients within the State of New York, Platzer has identified a potential issue in certain counties within New York State that are denying entry of Confessions of Judgment (“COJs”), notwithstanding language that has been contractually agreed upon and explicitly sets forth that the Confession of Judgment “may be entered in any and all counties with in the State of New York”, when the defendant is a non-resident.

The following is not a legal opinion but is our preliminary analysis:

It is Platzer’s position that New York Civil Practice Law and Rules (“CPLR”) 3218(a)(1) provides that when the defendant is a “non-resident” that judgment by confession may be entered in “the county in which entry is authorized.” Further, CPLR 3218(b) allows entry of judgment by confession as to a non-resident“ with the clerk of the county designated in the affidavit.” Platzer respectfully argued to the subject county that its jurisdiction is within the scope of authorization of “all counties” in the State of New York, and that the defendant “authorized” entry of judgment in the subject County, as contemplated by CPLR 3218(a)(1), and was also designated, as one of “all counties” in the State of New York, satisfying CPLR 3218(b), yet the Confession was denied entry.

As Platzer then noted, there is case authority for the proposition that non-resident defendants may subject themselves under CPLR § 3218 to the entry of judgment by confession in multiple counties. To Platzer’s knowledge, no Court has passed on the precise language of “all counties” or similar language. In the analogous situation where the confession of judgment executed by the non-resident defendant allowed entry in multiple but not “all” counties, Courts have routinely upheld entry of the judgment, while noting that there is no authority that would prohibit such entry under CPLR § 3218. Platzer has contended that this case law supports the notion that entry of confessions of judgment with “all counties” language is proper under CPLR § 3218.

As of March 4, 2019, Platzer is actively discussing these issues with the subject counties within the State of New York and hopes that its arguments will be persuasive based upon current New York law. Platzer is aware, however, of the state and national legislative efforts to curtail the entry of confessions of judgment and, specifically, the recent legislative proposal by Governor Andrew Cuomo to restrict entry of confessions of judgment to defendants doing business in New York and in amounts over $250,000.00. Platzer expresses no opinion as to these efforts.

Contacts:

Howard M. Jaslow

hjaslow@platzerlaw.com

Morgan S. Grossman

mgrossman@platzerlaw.com

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

475 Park Avenue South, 18th Floor

New York, New York 10016

Telephone: (212) 593-3000 ext. 248

Facsimile: (212) 593-0353