Archive for 2017

Brief: New York’s Attempt to Over-Regulate Lenders Downgraded to Doubtful

March 14, 2017 The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The passage of this proposal now looks doubtful. The Assembly, one of two branches of the State’s legislature, introduced their own version of the budget on March 13th and removed the language.

“The Assembly rejects the Executive proposal granting DFS regulatory authority over any online lenders doing business in New York State,” the bill says. Notably, they also rejected “the Executive proposal to authorize enforcement of Insurance, Banking, and Financial Services Law against unlicensed individual or businesses, including bringing a civil action.”

The Senate echoed same. “The Senate denies the Executive proposal to authorize the Superintendent of the Department of Financial Services to expand the regulation of small loan lenders,” their bill states.

Industry trade groups, namely the Commercial Finance Coalition (CFC), had mobilized quickly to tell their members’ stories up in Albany two weeks ago. One of the group’s concerns was that they had not been consulted in advance, nor given any time to engage in a discussion about the proposal.

“They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director. With the proposal’s chances of making it through the final budget by the March 31st deadline waning, the group and others may finally get an opportunity to do just that at some point later in 2017. According to The CFC, they are looking for additional companies to support them in that endeavor. Anyone interested in finding out how they can help should contact Dan Gans at dgans@polariswdc.com.

On The Line With BlueVine After a Big Year

March 13, 2017 Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

BlueVine’s success comes at a time when some in the online lending space have lost their luster. Lifshitz feels his company, however, is positioned well. “The time of exuberance has disappeared,” Lifshitz says. “Investors are looking to create value.”

Part of what makes them different is that they not only factor invoices, but they also provide lines of credit to prime and near-prime customers. Factoring is still a bigger percentage of their overall business, Lifshitz says, but he asserts that their credit line segment is growing at a faster clip. And he insists that they are working on other products too, not just loans. It sounds like the beginnings of a bank, I tell him, while making references to SoFi and their ability to live on the threshold of banking without actually currently being one.

“People have been saying that PayPal would become a bank forever but they haven’t become one,” he points out.

Still, running a company as big as his does require prudent decisions. “We are very mindful of how we manage capital,” he says. I ask if he thinks his business model protects them from an economic downturn. “It doesn’t protect it,” he asserts. Instead, he explains, his model gives him the ability to make adjustments rapidly. Since BlueVine’s capital is typically repaid in a matter of months, they can react to economic changes quickly.

Big name backers aren’t afraid to show that they believe in this either since they have been funded by Lightspeed Venture Partners, 83NORTH, Correlation Ventures, Menlo Ventures, Rakuten Fintech Fund and other private investors. A recent announcement by BlueVine says that they are on track to fund approximately $500 million to small businesses in 2017.

New York’s State Government is Competing With Online Lenders on Pay-Per-Click and Misinforming Small Businesses

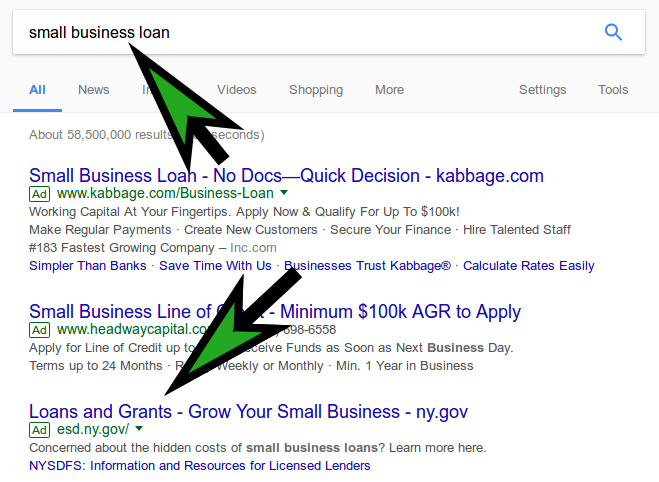

March 10, 2017Move over online lenders, New York’s financial regulator is apparently shelling out big bucks to steer away New York’s online small business loan searchers to THEMSELVES. As someone who has historically kept tabs on Google’s search results for lending related keywords, this new result is one of the more interesting developments I’ve seen yet.

From a New York IP, querying Google with the keyword small business loan produced not only an ad for Kabbage and other online lenders, but also prominent paid placement from New York State with a sitelink extension to the New York Department of Financial Service’s page about licensed lending requirements.

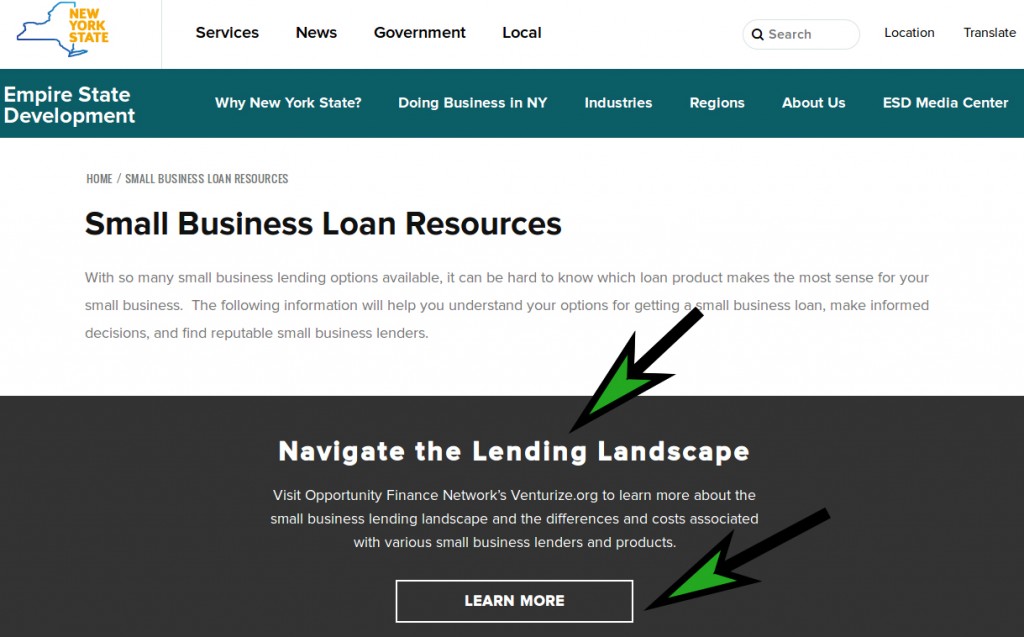

While there’s nothing that weird about marketing state-assisted development programs, the main Google ad link directs visitors to “Navigate the Lending Landscape” by clicking a “Learn More” button.

That takes you to Venturize.org, operated by Opportunity Finance Network, a Community Development Financial Institution (CDFI) that New York is apparently really doing the advertising for. And there’s a major problem with that.

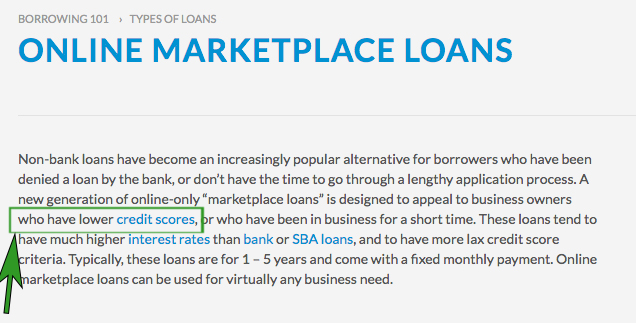

The information across that site is wildly incorrect. It explains online marketplace loans as “designed to appeal to business owners who have lower credit scores, or who have been in business for a short time.” That’s a pretty broad statement especially when many online marketplace lenders are in fact designed to appeal to business owners who have higher credit scores and have been in business for a long time.

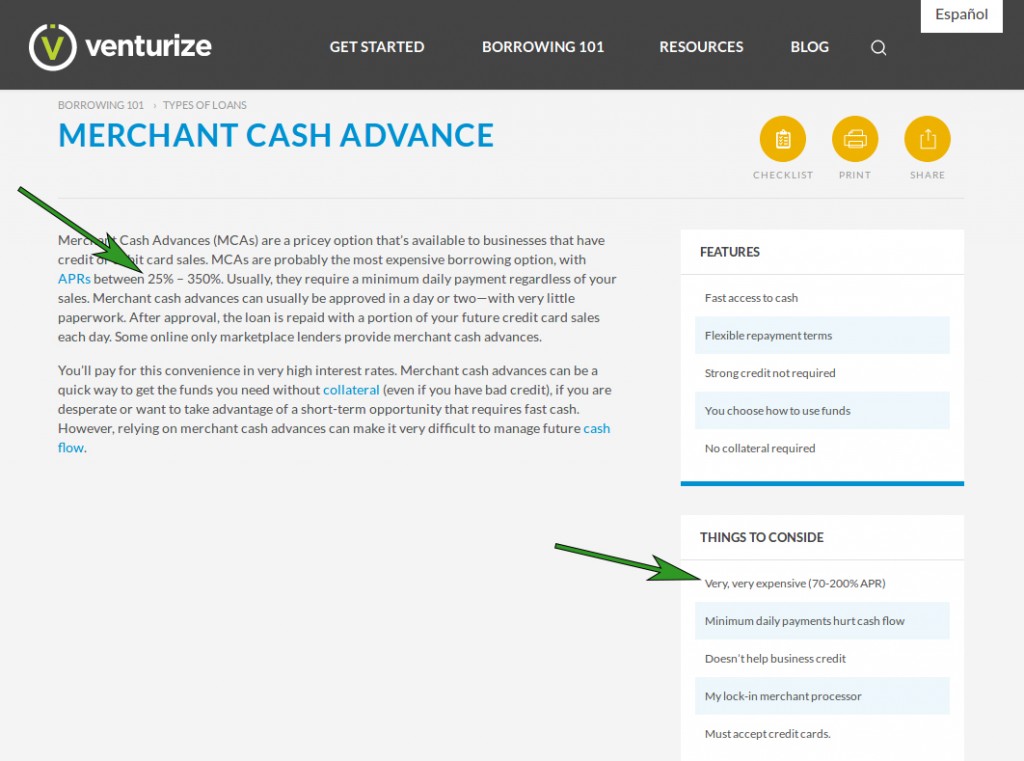

The description of merchant cash advances is even worse. Whoever wrote it has no understanding of them in the slightest. Good thing New York State is paying up to $100 a click with our tax dollars for premium keywords to teach businesses absolute nonsense! I quote what the website says below and my comments are in red next to them.

- “Usually, they require a minimum daily payment regardless of your sales.” – Um, no

- “After approval, the loan is repaid with a portion of your future credit card sales each day.” They’re not loans. This is mostly well settled in the New York Court system. Recently, see this and this

- “You’ll pay for this convenience in very high interest rates” – There are no interest rates

- “MCAs are probably the most expensive borrowing option, with APRs between 25% – 350%.” – Wrong. No APRs can be calculated on a purchase transaction

- “if you are desperate” – That’s a pretty unfair statement to say that a methodology is only for the desperate. New York State is insulting its small business constituency, private companies, and the jobs that have been maintained or created all at the same time

There are also typos and spelling errors throughout the page, as well as conflicting information. The very same page describes MCAs as having between 70% – 200% APR on one side and between 25% – 350% APR on the other side. You don’t need anymore proof that whoever wrote this stuff was just winging it on the fly to make it sound bad. These are the kinds of misleading figures that the CFPB sues financial institutions for and perhaps they should actually take a look at this.

It also says that businesses must accept credit cards. That’s not true either.

It’s strange that a CDFI would go to such great lengths to deliberately misinform small businesses, let alone have a state government foot the bill for them to do it.

Furthermore, as someone who recently used an online marketplace loan for my business, I’m personally offended that my state government would pay to market information that says it was designed to appeal to business owners who have lower credit scores. As my FICO score is over 800, the writer clearly does not understand the product, the market, or the appeal.

More troublesome of course, is that the NYDFS hopes to regulate these industries through language snuck in Governor Cuomo’s budget proposal. Given the above, what could possibly go wrong?

Brief: Former CAN Capital CFO Moves On

March 9, 2017According to the WSJ, Aman Verjee, who was CAN Capital’s CFO up until late last year, has taken the COO position at 500 Startups. The company has invested in more than 1,800 startups across more than 60 countries. According to the website, “500 Startups was founded in 2010 by former PayPal and Google alumni Dave McClure and Christine Tsai, along with many other friends and supporters.”

CAN Capital has not yet named a replacement CFO.

In Canada, Alternative Business Finance Industry Similar, Yet Different

March 8, 2017 David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

“We don’t view ourselves as directly competing with banks,” Gens says, suggesting that his target market is less than prime. It’s a point that his counterparts in the US have made often. But there’s a slight difference with that approach in their market, he adds. “Most Canadian consumers are prime.” And unlike the US, the banks are not necessarily portrayed as the enemy in Canada where five major ones dominate the market.

“It’s exceptionally difficult for an alternative small business lender to build a brand,” said Jeff Mitelman, CEO of Montreal-based Thinking Capital, on a panel at the LendIt Conference. Despite that, his company has funded half a billion dollars to 15,000 unique businesses over the last 10 years. A panelist besides him half-joked however, that there is such an inherent conservatism with Canadian small business owners that some don’t even want to grow and are content with running lifestyle businesses.

But of the deals that are getting done, they’re often acquired through direct marketing. “The ISO market is not like it is in the US,” Gens says. “There’s just a handful of them.” Where there are ISOs though, competitive pressures usually follow. He says that they’re competing on at least 50% of the deals they work on, in part because of these ISOs. Stacking is happening in Canada too, he admits. “It’s not as crazy as it is in the states,” he contends. “Philosophically, it doesn’t align with our business.”

Some deals in Canada are actually being facilitated by US ISOs, he acknowledges, before clarifying that they should be aware that they will get paid in Canadian dollars, which at present are worth about a three quarters of an American dollar. They are in a different country after all.

Gens and others like Bruce Marshall, vice president of British Columbia-based Company Capital, agree that OnDeck’s push into Canada has been good for the entire industry. Six months ago, Marshall said, “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

Over time, they believe alternatives will become more mainstream. For Gens, part of that is about doing right by the customer. “We pride ourselves on being very transparent,” he says. There are no hidden fees with their products and they can make things easy like use APIs to access a merchant’s bank statement history, provided an applicant wants to do it that way. “More than 50% of merchants are still submitting bank statements,” he says. That trend is still pretty much true in the US as well. “There’s a much lower incidence of fraud in Canada,” he asserts. It’s a nation of small businesses he’s content to serve.

Kabbage Prices $525 Million Securitization; Anticipates “A(sf)” Rating on Its Debt

March 8, 2017Kabbage®, a pioneering financial services, technology and data platform, today announced that on March 7, 2017, it priced $525 million of fixed-rate, asset-backed notes in a private securitization transaction. The facility is expandable to $1.5 billion. The notes will be issued in four classes by Kabbage Asset Securitization LLC, a newly formed, wholly owned subsidiary of Kabbage Inc. The senior class of notes is anticipated to be rated “A(sf)” on the closing date by Kroll Bond Rating Agency (KBRA). Guggenheim Securities is serving as sole structuring advisor and initial purchaser of the notes. The securitization is expected to close on or about March 20, 2017, and is subject to customary closing conditions.

The securitization was significantly oversubscribed with interest from top-tier institutional investors. This represents the largest asset-backed securitization of small business loans in the online lending industry, next to Kabbage’s prior, expandable, ABS note issuance in March 2014. This new facility will enable Kabbage to continue to broaden its product mix by offering larger credit lines and longer term loans.

“In a time when the FinTech industry has experienced challenges, our automated technology and data platform has demonstrated to investors Kabbage’s ability to deliver superior and predictable performance on small business loans as an asset class,” said Kevin Phillips, Head of Corporate Development for Kabbage. “Both the overwhelming investment interest and the anticipated strength of our bond rating are testaments to our proven approach to underwriting and managing small business loan performance through the Kabbage Platform.”

In March 2014, Kabbage was the first technology-enabled, financial services company to issue asset-backed notes secured by small business loans. This transaction was initially $270 million and was subsequently expanded to $545 million by the issuance of additional notes to multiple capital markets investors. This facility enabled Kabbage to dramatically scale its volume to extend over $2.7 billion through the platform.

The anticipated KBRA rating of “A(sf)” reflects an upgrade from the rating on Kabbage’s prior securitization. “Kabbage’s strong historical performance over the last three years played a key part in KBRA’s upgrade,” said Anthony Nocera, Managing Director at KBRA. “The upgrade is based on several structural improvements and the existence of more historical performance data relating to Kabbage’s collateral.”

About Kabbage

Kabbage Inc., headquartered in Atlanta, has pioneered a financial services data and technology platform to provide automated funding to small businesses in minutes. Kabbage leverages data generated through business activity such as accounting data, online sales, shipping and dozens of other sources to understand performance and deliver fast, flexible funding in real time. Kabbage is funded and backed by leading investors, including Reverence Capital Partners, SoftBank Capital, Thomvest Ventures, Mohr Davidow Ventures, BlueRun Ventures, the UPS Strategic Enterprise Fund, ING, Santander InnoVentures, Scotiabank and TCW/Craton. All Kabbage U.S.-based loans are issued by Celtic Bank, a Utah-Chartered Industrial Bank, Member FDIC. For more information, please visit http://www.kabbage.com.

The notes will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), or any state securities laws, and may not be offered or sold in the United States absent registration or an applicable exemption from, or a transaction not subject to, registration requirements. The notes were offered only to qualified institutional buyers under Rule 144A and to persons outside the United States pursuant to Regulation S under the Securities Act. This press release shall not constitute an offer to sell, or the solicitation of an offer to sell the notes, nor shall it constitute an offer, solicitation or sale in any jurisdiction in which, or to any person to whom, such an offer or solicitation or sale is unlawful.

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate

How Banks Are Coming Back to SME Lending (Summary)

March 6, 2017

The banks are no longer sitting on the sidelines of small business lending. At LendIt on Monday, a panel featuring representatives from two of the biggest banks in the country, reminded young upstarts that they intended to be the primary capital sources for small businesses.

Unlike JPMorgan Chase, which partnered with OnDeck, Bank of America (BoA) decided to build the technology to deliver loans easily and quickly on their own. BoA SVP Nadeem Tufail said that reputational risk had held them back from partnering with a platform back when they were considering it years ago. “We couldn’t make that leap,” he explained, citing factors like cost, which they saw as simply being too high on some platforms to feel comfortable with.

But that doesn’t mean that the opportunity has passed them by. “A Bank of America customer can get funded in 48 hours,” Tufail proclaimed, while adding that a business that doesn’t bank with them can get a loan from them in about 7 days. The bank is also now doing fully automated approvals on a very small scale with a sliver of their best clientele to test the concept.

Meanwhile, Julie Chen Kimmerling, Senior Manager at Chase, made it a point to say that they were also really worried about things like reputational risk but that they found OnDeck to be a perfect fit. The maturity of their management team and platform really impressed them, she said. Still, Chase governs how the loans are underwritten and keeps the customers on their balance sheet. So they haven’t exactly handed the keys over to OnDeck but obviously trust their brand to be affiliated.

BoA recognized that some of their customers were telling them that they shouldn’t have to submit all these documents when the bank should already have access to their financial histories, particularly their cash flow. Tufail said that this was one of the most important factors in their underwriting. “Does the business have cash flow?” he said. “Does the business have liquidity?” The bank should already be able to evaluate these metrics.

“We certainly have an advantage with transactional level data,” Chase’s Kimmerling said of banks doing loan underwriting. And Chase is no amateur in this market. Kimmerling said that her bank had provided $24 billion of credit to US small businesses last year alone, a figure prominently displayed in their last earnings report.

To boot, both banks retain brick & mortar presences around the country, an advantage for small business customers, who they say are pretty likely to visit a branch.

The banks it seems are coming back. Lendio CEO Brock Blake moderated the panel.

Quotes and paraphrases were derived from the panel. The summary is my own analysis of it.