Archive for 2017

AMA Recovery Group Announces Joshua Pena as Director of Client Relations

April 4, 2017 Houston, TX — We are pleased to announce Joshua Pena has been brought on board to oversee our client services in the capacity of Director of Client Relations.

Houston, TX — We are pleased to announce Joshua Pena has been brought on board to oversee our client services in the capacity of Director of Client Relations.

Josh brings over 15 years of customer relations and operations experience to our team. Prior to joining AMA, Josh served as Vice President of Operations for a consumer products company where he was responsible for sales, customer service and distribution channel management. Josh’s hire builds on our unmatched client experience, further accentuating why AMA Recovery is the collector of choice for successful MCA companies. “We are very pleased to have Josh join the AMA team. Josh’s commitment to results, outstanding customer service skills and business experience will enhance our proven collection experience” said Anh Regent, Director of Legal Operations.

Please do not hesitate to welcome Josh to the team, ask questions or discuss your collections needs.

About AMA Recovery Group

AMA Recovery Group was founded in Houston in 2015. Our dedicated professionals, complete end-to-end collections process, access to real time status updates and results driven focus give our clients peace of mind. It’s our goal to exceed expectations in customer service and collection performance.

Contact:

Joshua Pena

jpena@amarecovery.com

713.322.5396

Blazing Trails in Unexplored Financial Markets

April 4, 2017 Once upon a time people with health insurance who were treated for medical emergencies, illnesses or chronic health conditions –an illness or accident requiring hospitalization, an appendectomy, or a hip replacement, say – could rest easy. Insurance underwriters like United Health, Wellpoint or Humana would surely handle most, if not all, of a patient’s medical expenses.

Once upon a time people with health insurance who were treated for medical emergencies, illnesses or chronic health conditions –an illness or accident requiring hospitalization, an appendectomy, or a hip replacement, say – could rest easy. Insurance underwriters like United Health, Wellpoint or Humana would surely handle most, if not all, of a patient’s medical expenses.

Today? Not so much. As healthcare becomes ever more pricey, employers are increasingly offering health insurance plans that are less generous and require consumers to pay higher deductibles. Individuals as well are finding that the same goes for them: The only way to afford health insurance is to purchase a plan with a high deductible.

“We’re at a tipping point where the cost of healthcare is outpacing GDP,” says Adam Tibbs, chief executive and co-founder of Parasail Health, a start-up alternative lender in the San Francisco Bay area. “As a result,” he adds, “the only way health insurance can work is either to raise (the cost of) premiums or opt for higher deductibles.”

Statistics confirm Tibbs’s assertion. As of last autumn, according to a September, 2016, survey by Kaiser Family Foundation, the average deductible for workers’ health insurance policies jumped to $1,478, up by more than 12% from $1,318 in 2015. The survey found, moreover, that – for the first time — slightly more than half of all covered workers have deductibles of at least $1,000. At smaller companies, the average deductible is now more than $2,000.

Parasail, a Sausalito-based alternative lender which opened its doors last September, is angling to fill that void. Funded with seed capital raised from four venture capital firms — Healthy Ventures, Montage Ventures, Peter Thiel, and Tiller Partners, reports online data-publisher Crunchbase – Parasail acts as a go-between, connecting the medical practitioners to third-party lenders.

In partnering with doctors, hospitals, and medical clinics, Parasail employs a business model that resembles an auto dealership. After the customers picks out a four-door sedan or a sport utility vehicle, he or she drives it home thanks to a five-year, monthly-payment plan from, say, Capital One.

Similarly, after agreeing to a costly medical procedure, the patient can strike an arrangement with a medical provider’s billing department for on-the-spot financing. Once the deductible is covered, the patient is cleared to glide into the operating room.

Despite being open for less than a year, Tibbs says, Parasail has enlisted as partners some 2,500 medical practitioners with unpaid patient debt of roughly $4 billion. The typical loan averages $6,000. “Our goal,” remarks Parasails marketing vice-president, Dave Matli, “is to create a normal retail experience” so that financing medical debts is as seamless as swiping a credit card.

Meanwhile, industry experts say that Parasail represents a new breed in the financial technology sector. As online alternative lending and the broader fintech industry grow more established, institutional investors and financiers are increasingly wagering bets on companies that promise more than disruptive technologies or cheaper loans.

Increasingly, they are hunting for companies like Parasail that are introducing new products or blazing trails in unexplored markets. “The area that I find most interesting,” says Phin Upham, a venture capitalist and board member at Parasail, is investing in companies that “are developing products that didn’t exist before, serving people who haven’t been served, and playing a unique role incentivizing long-term behaviors.” (Upham, who is a principal at Peter Thiel’s VC firm, emphasizes that he is speaking only for himself.)

Parasail’s fundraising and launch has taken place against a dramatic drop in both global and U.S. fintech financing, according to KPMG’s annual report on the industry, “The Pulse of Fintech.” The accounting firm reports that total funding for fintech companies and deal activity plummeted by more than 50% in the U.S. in 2016 to $12.8 billion from $27 billion the prior year. KPMG attributed much of the drop to “political and regulatory uncertainty, a decline in megadeals, and investor caution.”

Parasail’s fundraising and launch has taken place against a dramatic drop in both global and U.S. fintech financing, according to KPMG’s annual report on the industry, “The Pulse of Fintech.” The accounting firm reports that total funding for fintech companies and deal activity plummeted by more than 50% in the U.S. in 2016 to $12.8 billion from $27 billion the prior year. KPMG attributed much of the drop to “political and regulatory uncertainty, a decline in megadeals, and investor caution.”

The year “2016 brought reality back to the market” after the banner, record-shattering year of 2015, the report noted.

Venture capital financing in the U.S., however, did not slip as dramatically as overall funding, sliding some 30% to $4.6 billion from $6 billion in 2015. (Almost overlooked in the report was that corporate investment capital was “the most active in the past seven years,” KPMG’s report notes, representing 18 percent of venture fintech financing.)

Steve Krawciw, a New York-based fintech startup executive asserts that “the business has matured and, yes, there have been defaults, but the business model for fintech has stabilized.” The author of “Real-Time Risk: What Investors Should Know About FinTech, High-Frequency Trading, and Flash Crashes,” Krawciw expects more funding to stream into the industry as new players such as banks, insurance companies, hedge funds and private equity get involved. They’ll “go in a number of different directions,” he reckons, “especially direct lending by hedge funds and private equity firms.”

No figures have yet been released by KPMG for the first quarter of 2017, just ended in March, but fintech industry participants are mightily impressed at news of the $500 million financing for Social Finance Inc. (SoFi). Best known for its refinancing of student loans, the San Francisco firm reported on February 24 that it raised a half-billion dollars in a financing round led by private equity firm Silver Lake Partners. Other investors include SoftBank Group and GPI Capital, bringing SoFi’s total investment to $1.9 billion, the company said in a press release.

SoFi, which plans to use the funds to expand online lending into international markets and devise new financial products, is ambitiously transforming itself into an online financial emporium. Along with a suite of online wares that mimic traditional banking and financial products – savings accounts, life insurance policies and mutual funds – SoFi has also invented new online offerings.

SoFi, which plans to use the funds to expand online lending into international markets and devise new financial products, is ambitiously transforming itself into an online financial emporium. Along with a suite of online wares that mimic traditional banking and financial products – savings accounts, life insurance policies and mutual funds – SoFi has also invented new online offerings.

For example, SoFi formed a partnership with secondary mortgage lender Fannie Mae and, together, the companies are enabling borrowers to refinance both mortgage and student debt. The SoFi financing, says Krawciw, “is not a seminal deal, it’s a sign of what’s coming.”

SoFi may also be providing a road map for fintech companies like Parasail. After building a customer base with health-care loans at 5.88% annual percent rate — compared with credit cards charging interest rates about four times as much – Parasail could be poised to sell additional products to its built-in audience.

Just as SoFi got big on refinancing student loans, Parasail could use healthcare lending as a springboard for future financial endeavors. Its revenues have been growing by 50% month-over-month.

By the first quarter of next year, Tibbs says, the firm will be breaking even.” And at that point, he adds, it expects to roll out a menu of new products too.

For Marketplace Lending Securitizations, A Bumpy Road But Strong Investor Sentiment

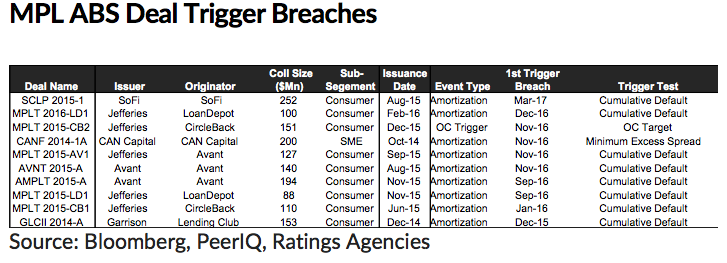

April 3, 2017A new report by published by PeerIQ contains 10 recent examples of trigger breaches in marketplace lending ABS transactions.

“Since the inception of MPL ABS market, we have observed 10% of deals breaching triggers historically,” the report says. It goes on to say that these events are typically manifestations of “unexpected credit performance, poor credit modeling, or unguarded structuring practice.”

“If an early amortization trigger is violated, excess spreads are diverted from equity investors to senior noteholders with the goal of de-risking the senior noteholders as quickly as possible.”

CAN Capital is the lone small business lender on the above list and we reported on their trigger breach back in December. Little public information has come out about the company since they stopped lending late last year.

![]() The most recent trigger breach on the list was SoFi, a company known for courting super prime borrowers.

The most recent trigger breach on the list was SoFi, a company known for courting super prime borrowers.

“Trigger breaching events do not necessarily imply credit deterioration of the collateral pool,” the PeerIQ report states. In another section of the report that addresses increased losses for non-bank lenders, it says that two of the three primary drivers of that are borrowers stacking loans and lenders shifting to riskier borrowers.

Nonetheless, Q1 was a record quarter for marketplace lending securitizations with seven deals priced for $3 billion. That’s a 100% increase over Q12016. “The industry continues to experience strong investor sentiment as evidenced by growing deal size and improved deal execution,” they say.

“We expect higher volatility from rising rates, regulatory uncertainty, and an exit from a period of unusually benign credit conditions. Platforms that can sustain low-cost stable capital access, build investor confidence via 3rd party tools, and embrace strong risk management frameworks will grow and acquire market share.”

Does Fintech Have a Distinctively British Accent? – From Congressman McHenry’s Speech

April 1, 2017Regulation around technology-enabled lending has generally been a point of contention in the US. Even regulators are finding themselves at odds with other regulators, like the OCC vs. the NYDFS for example. Might relationships like these be contributing to America’s innovative decline?

At LendIt last month, Congressman Patrick McHenry (R-NC) said, “Is it any wonder that Fintech has a distinctively British accent these days? It’s good reason. We have regulatory competition around the globe, but we don’t have the right regulatory competition here in the United States. And while we have a patchwork of conflicting, and overlapping, and confusing regulations, in places like the U.K., they’re creating an entire ecosystem of financial innovation and allowing it to flourish. And they become the model for the rest of the world and the intellectual property center for the rest of the globe when it should be here in the United States.”

Forward-looking regulation has helped a nation like Kenya make the movement of money cheaper in their country than it costs to move money here, McHenry said. “They’ve moved generations ahead overnight,” he exclaimed.

If you haven’t seen the video, check it out below:

Or you can read the full text from our transcription of it:

“And thank you all for being here. This is a wonderful celebration on, you know, a stereotypical February or March day here in New York. Cold as can be. Good to be inside. But thank you for taking the time to gather. The work that you’re about improves the American economy, gives more options for my constituents and for the citizens across this great country of ours, and gives them better options and opportunities to make decisions for themselves and put power back into their hands in a very competitive environment.

In fact, it’s really liberating to be out of D.C. especially at moments like this. You don’t know what the latest news story is gonna be or the latest tweet, so good to talk about something meaningful over the long run. And the reason why I’m here is because my focus legislatively has been around utilizing technology for innovative forms of finance.

I came about this in a very simple way that’s relatable to other people. But you know, the idea of Fintech, in 10 years, in 20 years, the term “Fintech” will be scoffed at kind of the way that we scoff at how they described Amazon 20 years ago. They said it was an e-Commerce site, that it was a webpage. Right? And we laugh at people that would describe it that way today. Every company that’s in the retail space has an e-Commerce site. Everyone is competing in this new form that Amazon represented the new wave of 20 years ago. So, the term “Fintech” may be much like referring to something as not a website, but a webpage. And in time, the way people are interacting with the banking system is going to continue to change in fundamentally different ways.

It’s exciting to think about how consumers and small businesses across America are gonna find these new ways to access capital over the next generation. And you all are at the forefront of that. And at D.C., I’ve tried to lead the change of that change in mindset. And you know, this is not only about helping Fintech companies, but also about fundamentally altering how regulators interact with innovative companies. And so, the focus on lending, helping families access capital as I said in the beginning, I came to it in a very natural way.

It’s exciting to think about how consumers and small businesses across America are gonna find these new ways to access capital over the next generation. And you all are at the forefront of that. And at D.C., I’ve tried to lead the change of that change in mindset. And you know, this is not only about helping Fintech companies, but also about fundamentally altering how regulators interact with innovative companies. And so, the focus on lending, helping families access capital as I said in the beginning, I came to it in a very natural way.

I saw my father start a small business as a child. When I was a child, the youngest of 5 kids, I saw my father start a business in the backyard mowing grass. Very simple, relatable thing. Most of us have mowed grass at some point in our life. And my father started that small business in our backyard and he used the great financial innovation of his time to buy his second piece of equipment, which he put on a MasterCharge. Great financial innovation and that helped him start a small business.

Now, that small business didn’t change the world, but it changed my brother’s and sister’s lives and put the 5 of us through college. That’s a meaningful thing and that is the American dream as my father defined it and as I define it. Now, that’s not creating Facebook. It’s not this other sort of revolution of internet technology, but it certainly made a huge difference in our community and for our family.

So, how did we utilize technology and help those small businesses like my father access and grow? The plight of small business in America though right now is real. The next generation of small business owners are struggling to get off the ground. The facts are that small business loans used to make up a majority of bank balance sheets. Now, 20 years— Well, in 1995, they were majority of the bank balance sheets. Now, it’s 20% of bank balance sheets.

Now, you also see small town America, which used to lead the country in small business starts, small counties, small communities across the country have lagged. So, smaller counties used to lead the nation in new businesses even as late as the 1990s, mid `90s. But just in this decade alone, small counties have lost businesses. U.S. counties with 100,000 people or fewer residents lost more businesses than they created. We see stagnation among small business owners and small business starts. This is why Fintech is so vital and so important. Technology is the only way to ensure that we spread and democratize capital outside of Austin, Boston, Silicon Valley, and New York.

How do we get the rest of the country, small town America, and even the urban areas that don’t get the focus and attention? And so, I think the power of harnessing big data is gonna fundamentally change the way we look at debt. It’s already happening. And you’re the leaders of it. Instead of relying on the credit score, which was a great innovation in the 1970s, fixed the problem in the 1970s, today, companies are using big data to better understand who will and who should qualify for loans. And what we’re discovering is that the way we help people out of debt is by understanding the data behind the debt.

Look at the way technology is fundamentally changing lives and places like Kenya. Think of this. In Kenya, the phone, your smartphone, our smartphone is that way to financial inclusion in Kenya. The movement of money cheaper in Kenya than it is here because of this simple device. It’s more powerful in that jurisdiction than in ours because of regulation and forward-looking regulation. And instead of loading buses filled with luggage that’s filled with cash in moving money in Kenya, they’re now doing it through a fast transfer over their mobile device. They’ve moved generations ahead overnight. And in fact, in many ways, they’re leading the world in Fintech deployment. So, we’re living in a new and exciting era in financial services. It’s actually matched the best interest of consumer protection with the demands of global smartphone-led revolution that we, as consumers, are driving. Now, that’s what’s happening in the real world.

So, let me translate back to you what is happening in the analog world of Washington. D.C. The regulatory challenges of Fintech are real. It’s major in Washington. We have a diversity of regulators. That’s certainly part of our American system. And that’s not gonna change any time soon. So, what is the current landscape? If you are in Fintech and you wanna make sure you’re complying with financial laws and regulations, where do you go? Who do you ask? Who do you talk to? Is there an open door in Washington? Do you know who your regulator is? Do you know who your regulator should be? Do they meet with you? Are they willing to meet with you? What’s your legal and compliance cost before you even get a product hashed out? These are major things you have to wrestle with in starting your businesses or growing your businesses. So, believe it or not, the difficult question is who do you talk to in Washington? And there is no simple answer. And because there’s so little clarity on which regulator to go to, often there’s even less clarity of how the underlying laws or regulations are being enforced by that regulator in this new marketplace.

And so, this is the hidden secret of Washington. The regulators themselves are so behind when it comes to understanding technology that they themselves do not really know how to apply regulation to innovations in Fintech. They just simply do not know. And trust me, I realize this as a legislator. 5 years ago, I helped craft what is called the JOBS Act. I wrote a piece of the JOBS Act. It resulted in 14 pages of legislative text around investment crowdfunding. 14 pages of legislative text. 3 years later, the Securities and Exchange Commission wrote 700 pages of regulation around my 14 pages of law. And if you are all involved in investment crowdfunding under Title 3 of the JOBS Act,— three of you, right— there will be a lot more had they written good regulation and actually complied with the mindset of Congress when we passed the JOBS Act.

So, I see this when regulators don’t actually know how to meet the demands of innovation and what’s happening in this information revolution that we have. And so, as a result, America is actually falling further behind the rest of the world. And unlike other areas of the world, which have created regulatory sandboxes for banks and technology companies to innovate and find a light-touch regulation, here in Washington or there in Washington, regulators are struggling to adapt.

And is it any wonder that Fintech has a distinctively British accent these days? It’s good reason. We have regulatory competition around the globe, but we don’t have the right regulatory competition here in the United States. And while we have a patchwork of conflicting, and overlapping, and confusing regulations, in places like the U.K., they’re creating an entire ecosystem of financial innovation and allowing it to flourish. And they become the model for the rest of the world and the intellectual property center for the rest of the globe when it should be here in the United States.

Well, while we’re all trying to figure out whether or not virtual currencies are more like property or money here in the United States, top countries around the world are using digital currency to move payment platforms overnight, change payment platforms, make it cheaper, more affordable to move funds for the smallest and the biggest. So, while the world’s rapidly adopting new financial technology to expand the middle class, our country’s regulators have created capital deserts here in the United States in rural and in urban areas. We understand the notion of an urban food desert. If you can get good food that is close to your home in an urban area, you can actually feed your children wholesome meals. We understand that. That’s a big discussion. Well, likewise, we’re starving off small business innovators in urban areas and let’s say less desirable zip codes in urban areas and less desirable zip codes in rural areas. And so, we’re starving off opportunity and that has a result in small business starts and the rise from the turn in the economy from those that are living on the margins to those that move up to the upper middle class and upper class based off being starved from capital.

We have to fix that. Fintech is the solution, but the regulation has to change. And that is something that I’ve been focused on over the last 6 years. And I think we have a trilogy of good ideas that I would submit to you this morning. First is let me just tell you my mindset in regulating and legislating. And to borrow from startup culture, the bills that I try to focus on are minimal viable bill. It’s a simple idea.

One idea that focuses on solving a discrete problem. Something in the marketplace that needs a regulatory fix in order to flourish. And it will help the greatest number of people and have the greatest impact on tech companies, bank startups, and small business folks and families. So, looking at the headache test, one of the areas of interaction with the government that’s creating unnecessary delay is the IRS not having a piece of technology that will allow people to verify income data.

And so, as a result of that, I’ve — legislation that is called the IRS Data Verification Modernization Act, 45060 for those of you who are in the game on this, but it simply will do this. It will automate a bottleneck manual process that is utilized via e-mail and fax with the IRS in verifying basic information that you, as lenders, need to allow mortgages, student debt, refinancing, and small business loans. It’s the taxpayer’s information. You pay for the service to verify it. We should have better service rather than the shoddy service IRS is currently giving you. You should be able to get this in an instant with an API rather than getting something faxed to you in 7 to 10 days. It’s absurd that the IRS can’t update and we’re gonna force them to update.

Our second bill, it goes directly to returning consistent uniform systems for our capital markets, which I believe is a fundamental thing in our 50-state regime with a variety of regulators. We have to have some base level of understanding on what is valid. And the bill is simple. It codifies the Valid-When-Made Doctrine that we’ve had in this country for nearly 100 years. And that was an established legal precedent prior to the Second Circuit Court’s decision in the Madden case. Madden versus Midland. And our view is the Second Circuit’s opinion was unprecedented. It’s created uncertainty for Fintech companies, banks, and the credit markets; making credit less available and more expensive. So, the simple fix is returning to the Valid-When-Made Doctrine. Congress under our constitutional system has the right to make this very clear to the courts of our intention when we pass the original law and nothing has changed when it comes to this. And this is the second bill that I’ll be pushing this year.

And finally, a third piece of legislation that is broader in discussion and it’s the Financial Services Innovation Act. This bill creates a new paradigm for regulators in Washington. It says in a first of a kind way, it forces regulators to meet the demands of rapid innovation in financial services. Instead of the old analog version of command and control regulation that’s messy and rigid based off of opinion, not fact, my bill requires agencies of jurisdiction to create offices of innovation that will engage with entrepreneurs and provide a regulatory on-ramp for financial innovation. It basically forces all the regulators, all the financial regulators to create a new door for financial innovation. A welcoming door. Come in with your ideas. Let’s talk about regulations that can enable this technology to flourish. And in getting data in return, the agency would be in permanent beta testing mode, which would give them data to prove out consumer benefit or consumer harm. It will give them data to adopt the whole footprint of regulation in all these financial regulators.

Now, that is a major mindset shift for our financial regulators, a major mindset shift for any regulator in our American system of governance. But with thorough analysis, I believe that innovators will be better off in this regime when you have data that is driving the decision making of regulators and regulators driving decisions that are informed rather than opinion based.

Now, saying that we’re gonna base our politics off of fact these days is its own enormous political challenge, but I think it’s important that we all agree facts are important things and we should base our decision-making solely on that set of facts in order to do the right thing for our country, the right thing for our economy, right thing for families, right thing for small business starts. So, permanent beta testing involves continuously evolving, testing, and proving. It’s what you do everyday as innovators.

Now, those are 3 major pieces of legislation that can have an impact, but the mindset in Washington is much— Well, it’s much different than you might think. Legislators are eager for new ideas, for new information. They’re eager to hear what you are about and what you’re doing. And given the nature and the speed of innovation, you have an obligation to be engaged in Washington. If you’re not engaged in Washington, Washington is still gonna be engaged in what you do. You’re just gonna get worse rather than better. So, if you inform decision makers you have data to backup what you’re expressing, what you’re advocating for, we’re gonna be better off, but you all in your pitches, right, have to— The basic startup pitch, you’ve got to answer one question. Why now? Why now? I think American financial innovation is at an inflection point. I really do. We’ll either lead the world in the next few years or we’re gonna be left behind. It’s our choice. It’s our choice. And it’s time that regulators treat innovation no longer as a threat, but as an opportunity to consumers. It’s time to recognize that regulators need to recognize— I think it’s time that they recognize that consumer protection and innovation are not mutually exclusive. Now, that’s the reason why it’s now, but it’s not gonna happen unless you engage in Washington and make your voices heard. You’ve gotta make your voices heard in order to get the results we need so we can have innovation flourish in this country, that we can be the market leader for the world, that we can be an exporter of these ideas rather than having to export ourselves to different markets in order to take that data and that mindset and deploy those resources globally.

Let’s make sure that we can lead this market to better and greater things. With your engagement, we can. Without your engagement, we’re gonna be left behind. So please, please engage in Washington. Make your voices heard. And with your voices being heard, I think we can have change for the better. So, thank you for your leadership. Thank you for the opportunity to be here with you. God bless.”

Update in the Argon Credit Bankruptcy Case

March 31, 2017On March 28th, United States Bankruptcy Judge Deborah L. Thorne, ordered the trustee in the Argon Credit case to transfer the net proceeds and loan portfolio payments to the biggest creditor, Fund Recovery Services (FRS). That cash will be used to satisfy the approved secured claim of $37.3 million. FRS is an assignee of Princeton Alternative Income Fund, LP. Argon Credit was an online consumer lender that made loans between $2,000 and $35,000 with APRs ranging from 4.99% to 149%.

Initially, Argon Credit had applied for Chapter 11 bankruptcy after “experiencing financial difficulty,” though allegations of improprieties and mismanagement have come up in the legal filings. When FRS tried to stop their collateral from being spent, Argon argued in court that such a thing was unnecessary because they had more than enough collateral to pay off their debt to FRS, including $5.5 million worth of leads. By FRS’s calculations, the leads were worth as little as $1,500, not millions. Ultimately, the judge attributed no value to them.

The case was converted to Chapter 7 and FRS should be able to get repaid.

StreetShares Reports $2.8M Loss on Just $277,000 in Revenue For Last Six-Month Period

March 30, 2017 StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares has so far charged off 23 loans for a combined principal balance of $380,804. Charge-off determinations are made after 150 days of delinquency.

The company made history last year by becoming the first lender in the US to be approved by the SEC to use funds from public investors to back loans to small businesses. This was done through Regulation A+ of the Jumpstart Our Business Startups (JOBS) Act. Reg A+ investors make up $656,675 of StreetShares’ liabilities on the balance sheet.

StreetShares currently makes loans to small businesses between $2,000 to $500,000 for terms of three months to three years.

The company also spent more than 5x their revenue on payroll and payroll tax for the six-month period and more than 3x their revenue on marketing expenses.

Earlier this month, StreetShares announced a partnership with Nor-Cal FDC “to assist small business and veteran business owners in obtaining funding needed to win new opportunities.”

In the release, StreetShares CEO Mark Rockefeller said, “we’re eager to provide veteran-owned small businesses with the funding solutions they need to grow.”

In Advance Capital Secures $50 Million In Additional Financing

March 29, 2017New York, NY — On March 27th, Times Square-based In Advance Capital secured a $50 million credit line to continue the rapid growth of its merchant cash advance business. The eighteen-month-old company, led by founders Shalom Auerbach and Thomas Corliss, attributes its portfolio transparency, discipline, and strong relationships with investors as the key contributing factors in securing the additional capital.

“In an industry that is increasingly difficult to access capital, we are very pleased to have earned the confidence of sophisticated investors who have provided capital that aligns their objectives with ours, which is to provide fast and flexible working capital to small business owners experiencing the challenges and opportunities of high growth,” says Shalom Auerbach, IAC’s CEO. In Advance Capital has focused on creating a more streamlined process to facilitate its own growth, including a quicker underwriting process, while seeing 220% more applications within the last two months.

“In Advance is a testament that you can build and grow a company in a competitive industry if you concentrate on hiring top talent, servicing, and listening to your customers,” Corliss says.

“It’s all hands-on deck at In Advance which also makes our work environment a special place to work.”

In Advance is also please to announce its recent Executive Management addition to staff, Keith Nason as Chief Operating Officer. Keith Nason brings over 10 years of expertise to driving operational leverage, streamlining process and data science analytics.

About In Advance Capital

Founded in 2015, the company provides working capital to small business owners. To learn more, visit http://www.inadvancecap.com or call 646-412-3303.

Enrolling a Merchant’s “Debt” May Be Harmful… to the Merchant

March 29, 2017 How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

For merchants, the allure of a restructuring company’s help might just be payment terms tied to their monthly budget. That’s allegedly what one NJ firm’s agreement says, in fact. “I hereby authorize [the company] to negotiate my unaffordable business debts and to enter into affordable repayment terms on my behalf based on my monthly budget,” reads a document submitted in a New York Supreme Court case involving Creditors Relief. And based on the marketing materials deBanked has reviewed from several similar companies, their definition of debt is so broad that it can even include things that aren’t debt, like merchant cash advances, for example.

Even if the restructuring company held a critical view of MCAs and believed them to be loans, treating them as such for the purpose of negotiation might actually cause harm to their customers. That’s because a well-formed MCA contract already offers payment adjustments at regular intervals to appropriately match a merchant’s sales activity. Depending on what the language says, a merchant might just have to call their funder and ask them to reduce the debits to reflect their current sales activity. And yes this goes for ACH-only deals. Even ones that could appear to have fixed payments do not actually have fixed payments. This is basically how all MCAs work by the way, so if you are a broker or funder and this all sounds foreign to you, you need to take this course ASAP.

The point is this: a merchant need not pay a fee to an outside company to restructure anything when sales drop because a free remedy already likely exists and is a key benefit to MCAs in the first place. And yes, I’m talking about MCAs with daily ACH debits. If you’re confused by this, you need to take this course ASAP.

The best advice a restructuring firm can give a merchant struggling with an MCA due to slow sales is to tell them to look for a reconciliation clause in their contract that explains how to get the payments reduced. Once the merchant finds it, have them call the funder and execute it. There’s no need to enroll anything, negotiate anything, risk breaching a contract, or pay a broker tens of thousands of dollars in commissions. The debt restructuring firm might not want merchants to simply take advantage of what they’re already entitled to however, because they stand to make no money that way. In this regard, mischaracterizing future receivable sales as loans only serves to carry out their agenda to confuse merchants about what their rights might be under those agreements.

I myself, am occasionally contacted by merchants who claim to be facing hardship and in one instance where a merchant had spoken to a negotiator, the negotiator didn’t tell him that the remedy he sought was already a natural provision of his contract. I helped him find it. He didn’t have to pay any fees which would’ve gone to pay someone a huge commission or end up in some crazy situation where he’s being sued for breach of contract. Think about this the next time you encounter a distressed merchant. Not everything is debt and that can be very much to the merchant’s benefit.

If you work for a debt restructuring, settlement, or negotiation company, you should probably take this course too. It will help you understand MCA agreements and what remedies merchants already have at their disposal.